Economy

Our US fixed income team’s key investment views for 2024.

Our recommendations for blogs and X’s (on the economy, financial markets, asset allocation, bonds, quants, energy, real estate, geopolitics, and specific countries and regions) to try over the holidays.

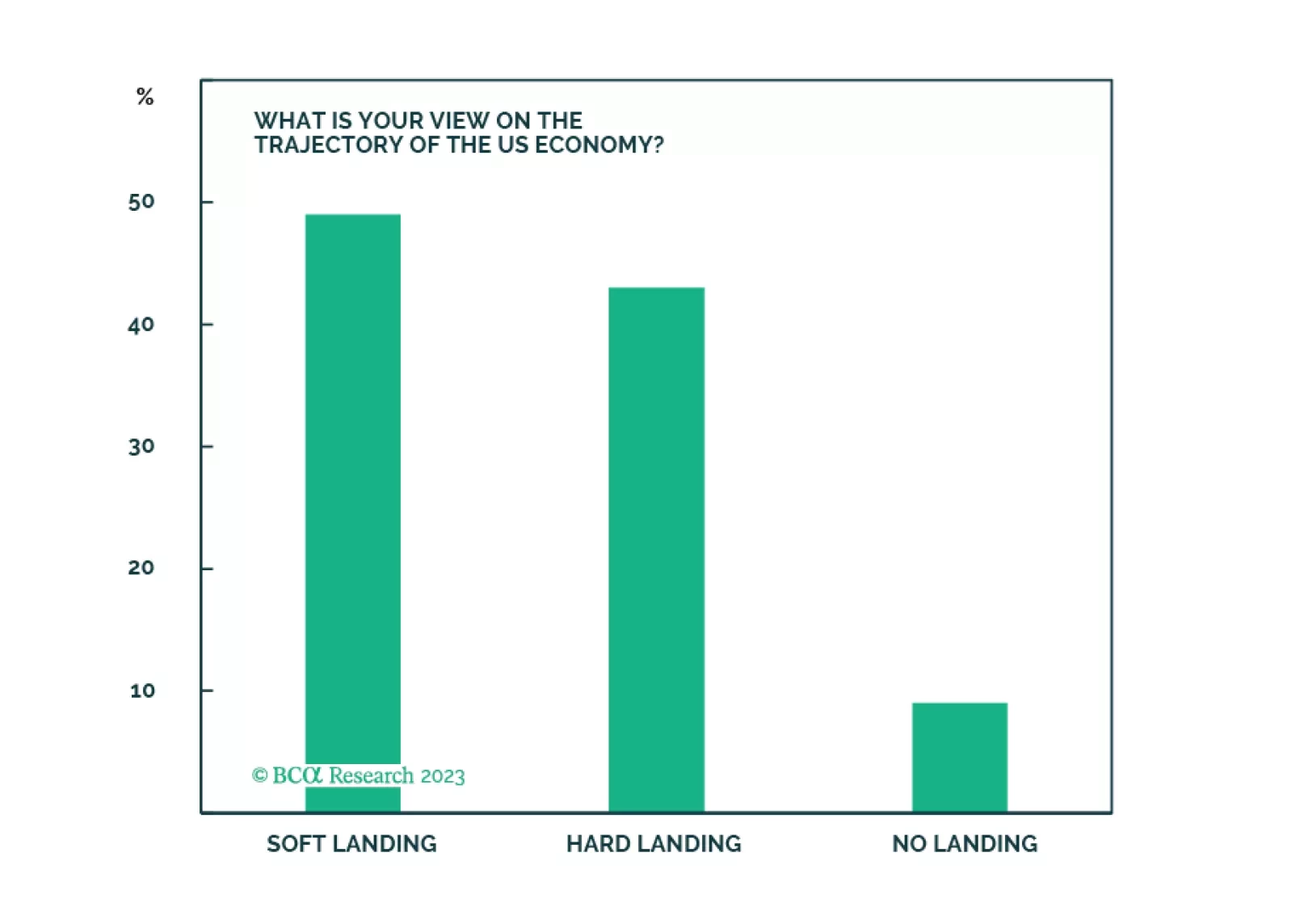

The Santa Claus rally is a repricing of the "soft landing" scenario as a likely economic outcome. Yet, many investors remain cautious, and harbor significant cash balances. Next year, repricing of various scenarios will continue, and volatility will be elevated. We remain in a "hard landing" camp and recommend defensive stance on a strategic investment horizon.

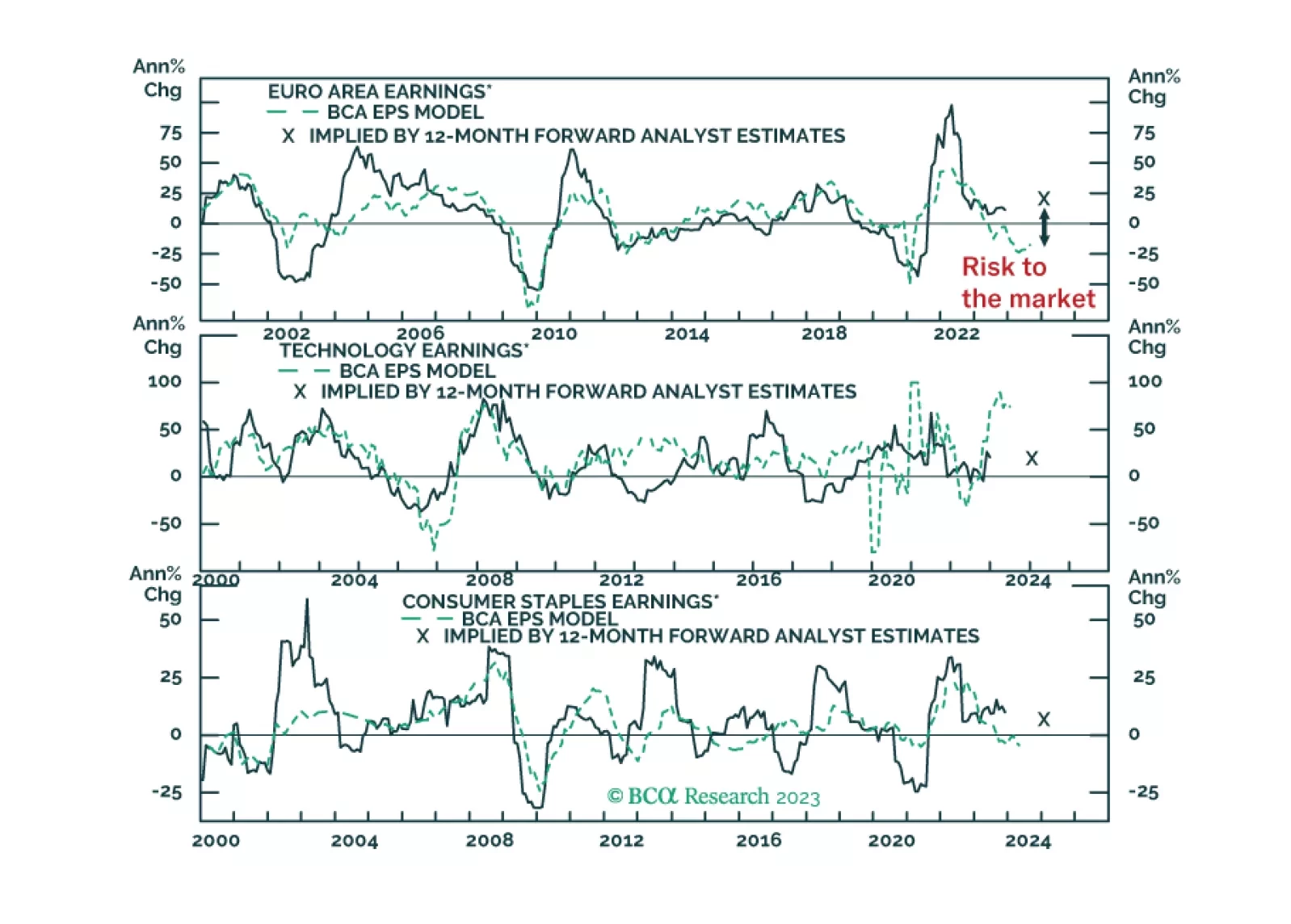

The recent decline in yields has powered European equities higher, however, this rally cannot last if earnings decline meaningfully. With this in mind, are our earnings models flagging risks for stocks next year?

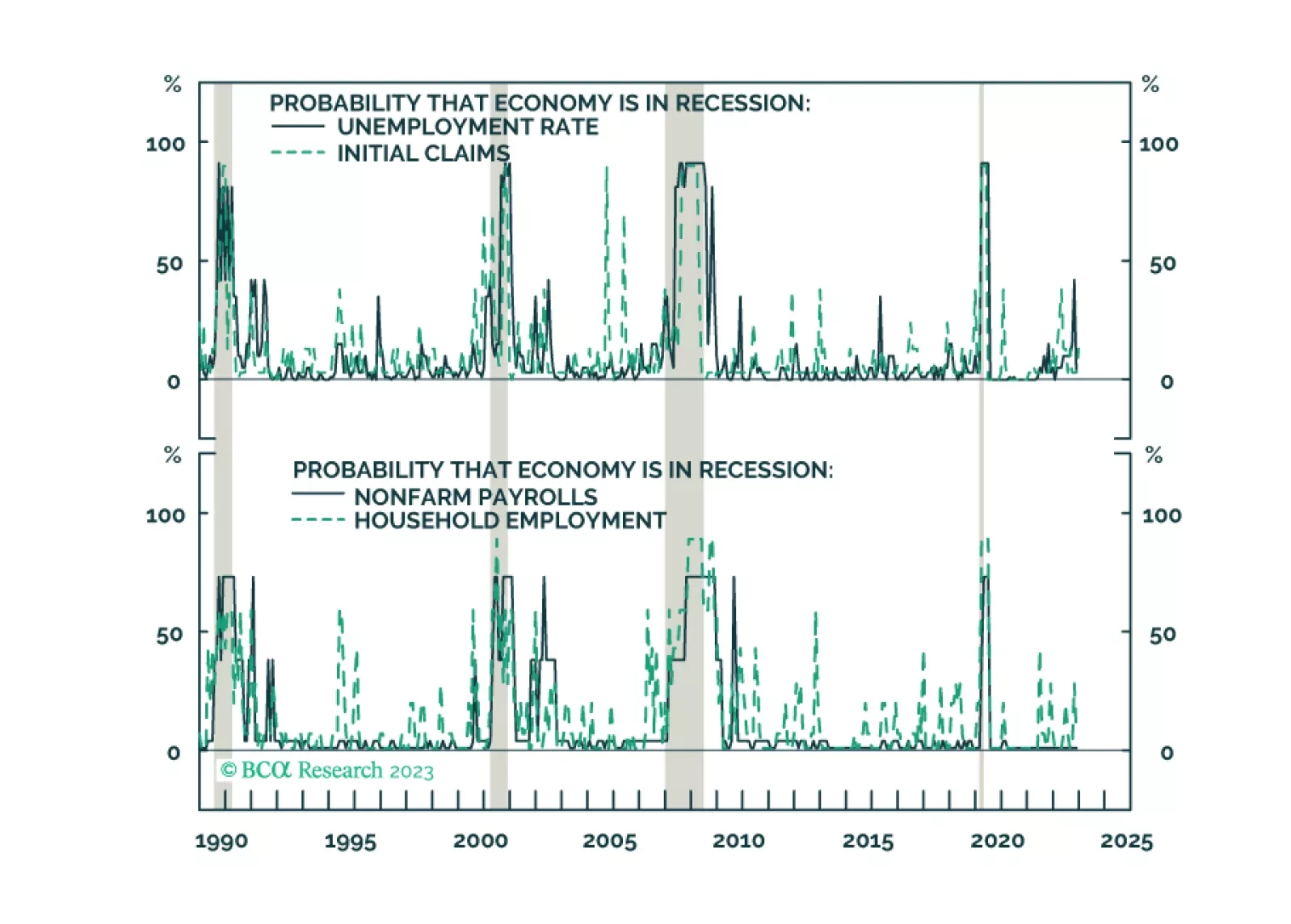

Global Investment Strategy predicted the surge of inflation in 2021/22 and the immaculate disinflation of 2023. Now their unique framework is predicting a recession in the second half of 2024.