Economy

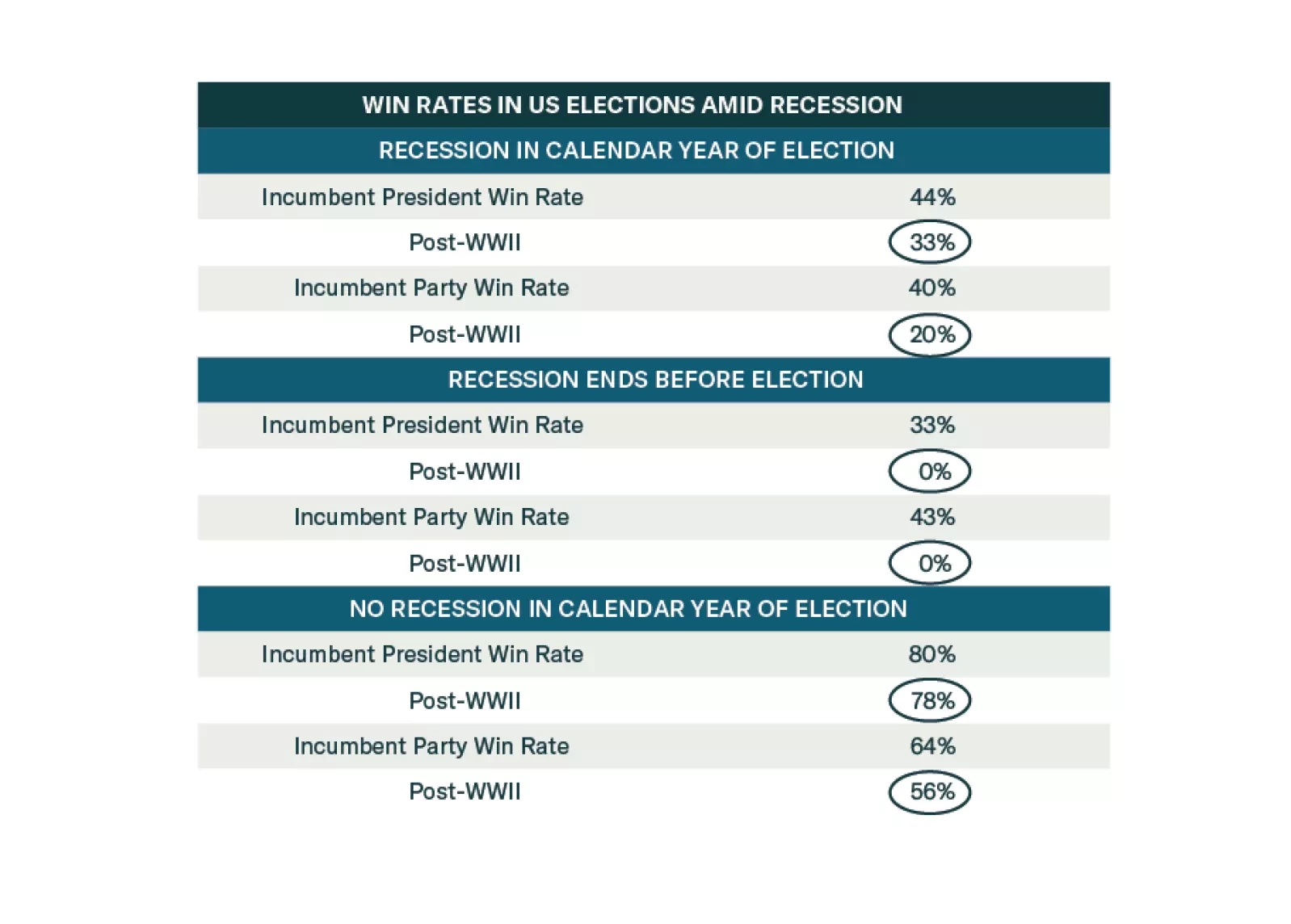

Democrats are favored to win the election until recession materializes. But recession risks are high. Investors should adopt a defensive and conservative strategy in 2024 amid extreme US policy uncertainty.

The overarching macro theme for China in 2024 will be deflation and its impact on the economy, macro policies, and financial markets. Widespread deflation, in combination with high debt levels and falling real estate prices, has unleashed debt deflation and balance sheet recession dynamics. The latter are rendering monetary policy inefficient.

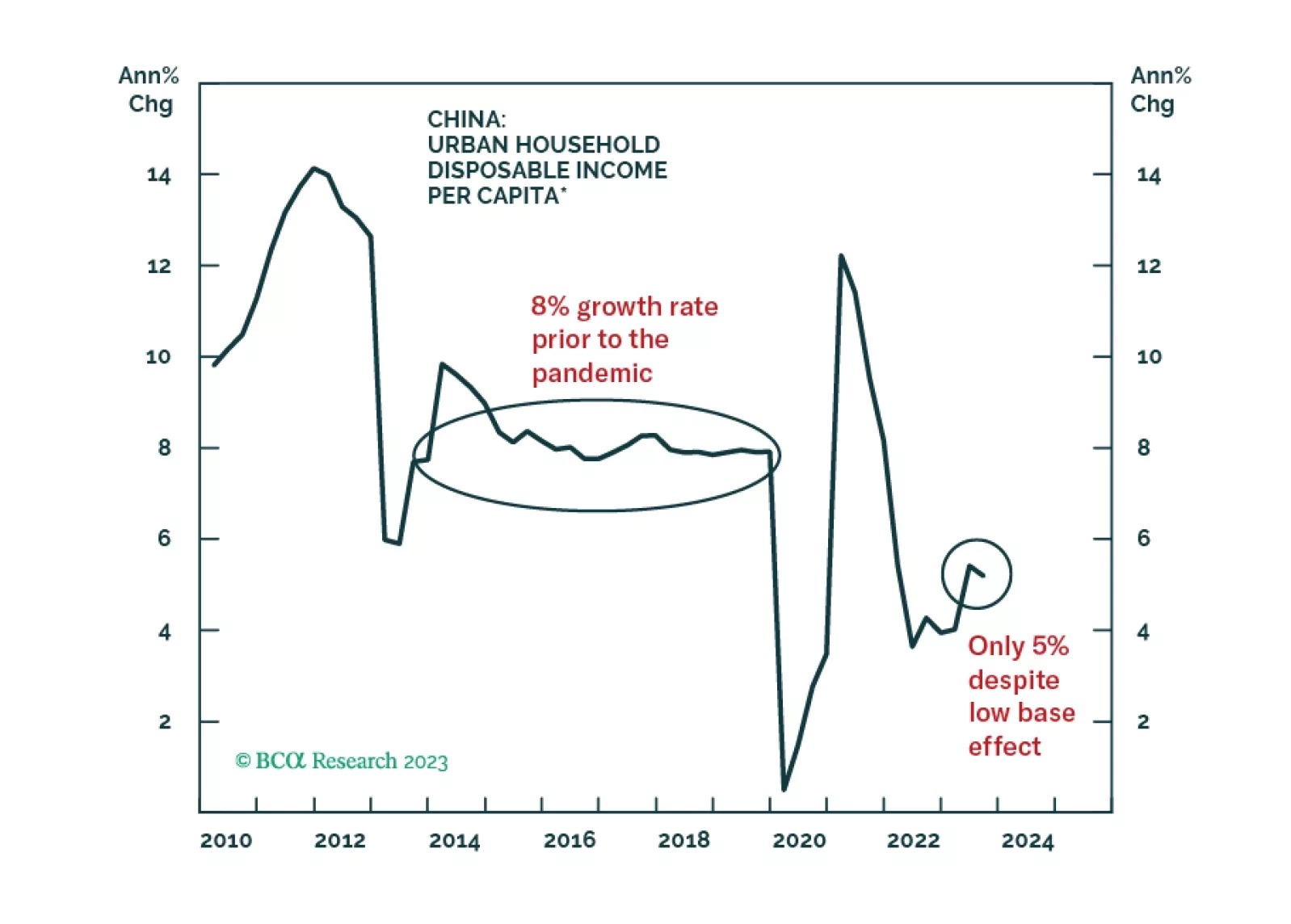

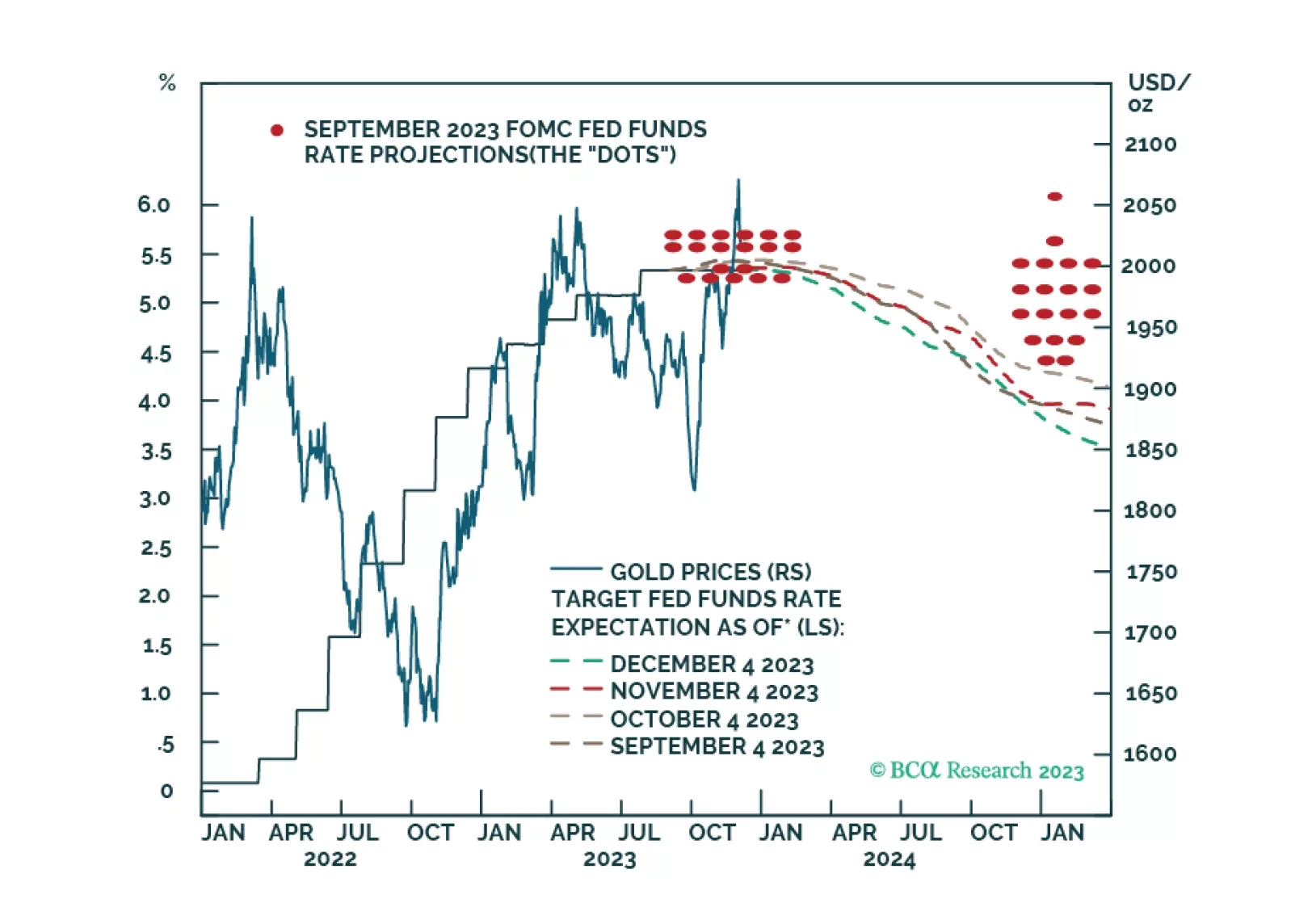

Falling core inflation in the US over the short run will boost real disposable household income, which will keep consumption – ~ 70% of US GDP – strong. Over the medium- to-longer term – 3 to 5 years out – inflation risks rise as fiscal dominance becomes the Fed’s modus operandi, and economic fragmentation becomes entrenched. War and the expansion of war remains an inflation risk. In this environment, gold remains our preferred hedge.

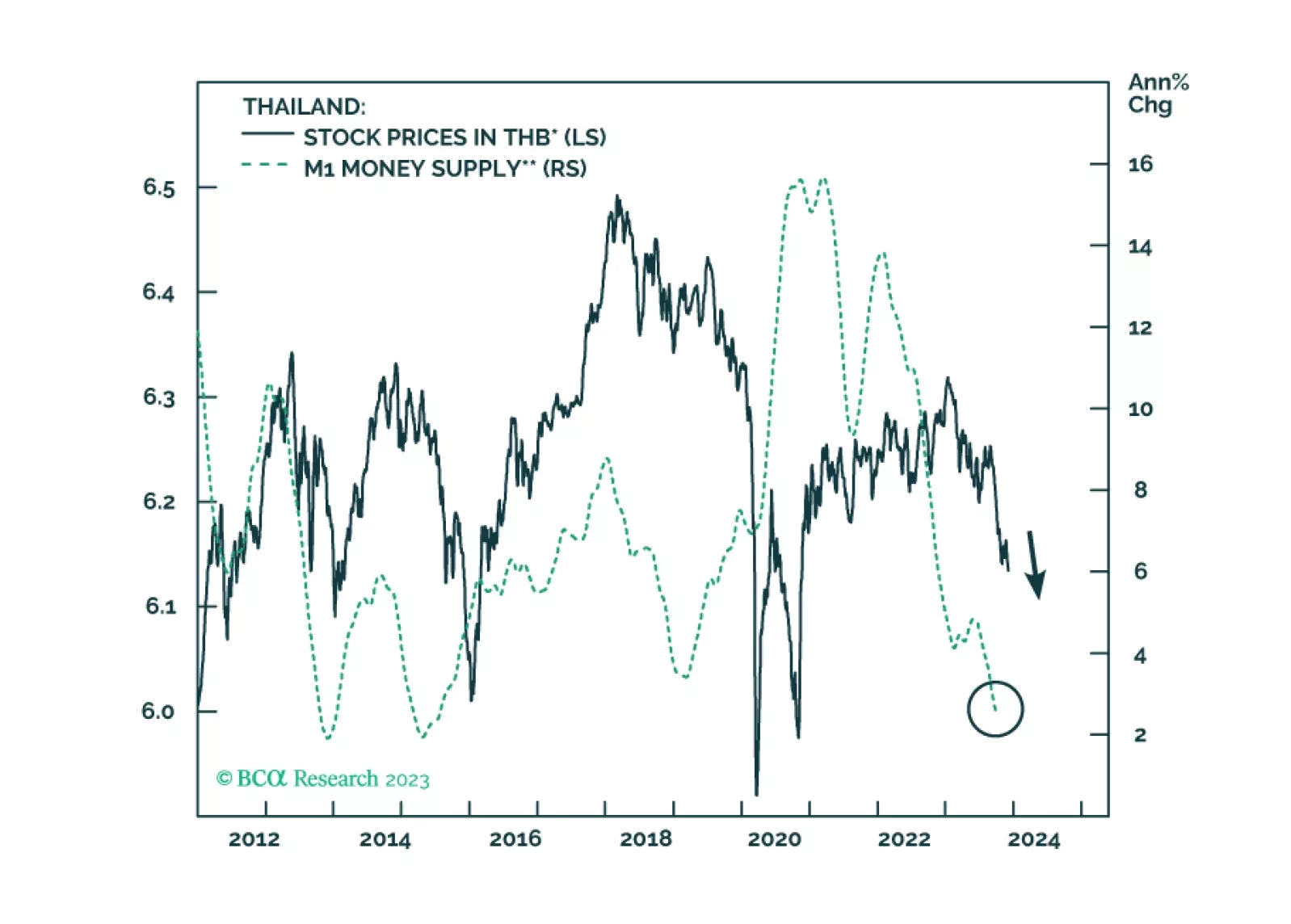

Meager credit growth and shrinking real wages will keep Thai inflation very low in the coming months. The currency will get support from an improving current account surplus. Fixed-income investors should upgrade Thailand from neutral to overweight within EM domestic bond portfolios.

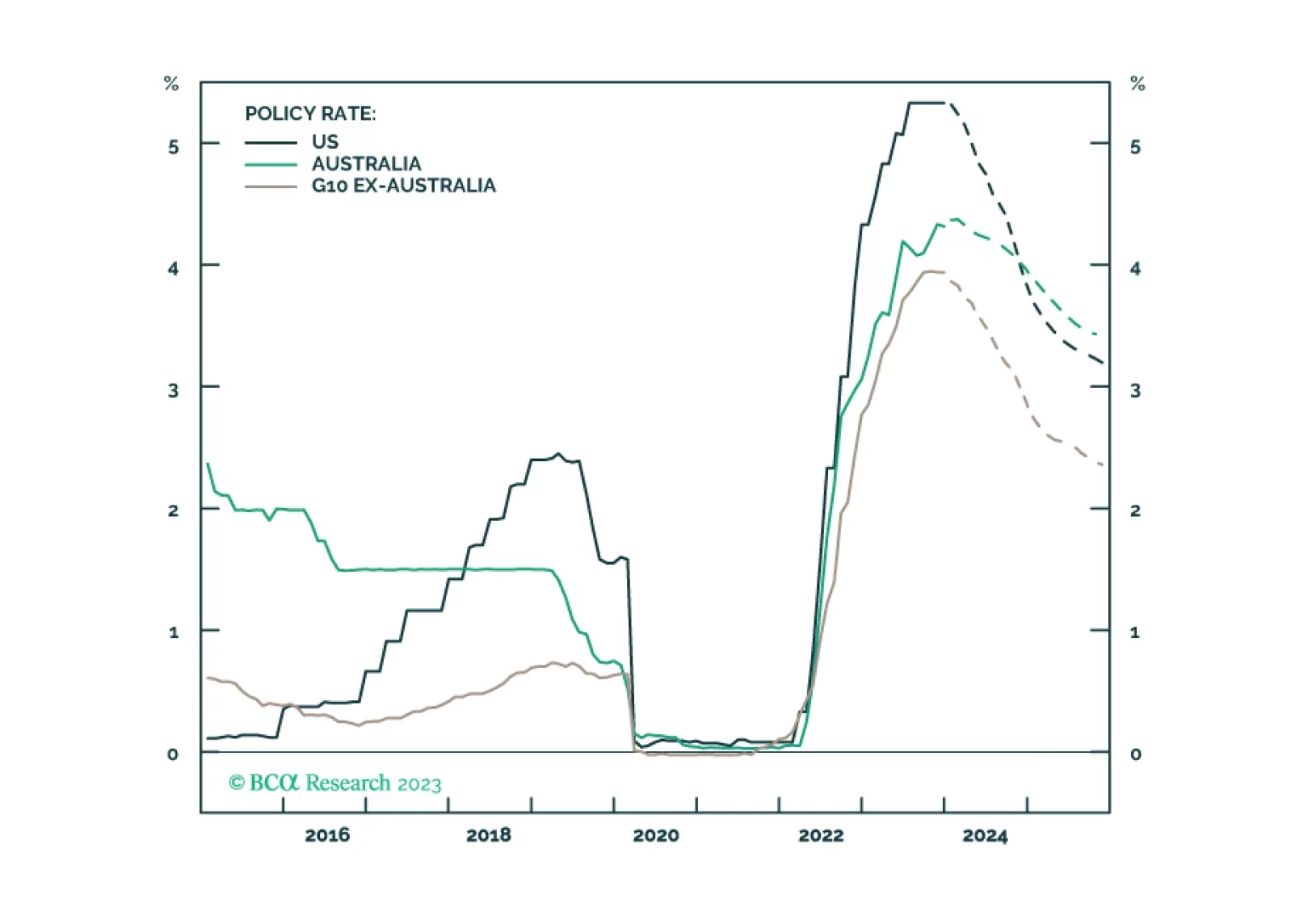

In this Special Report, we take an in-depth look at the outlook for monetary policy in Australia and discuss the impact of an elevated policy rate on the economy. We recommend an underweight country allocation to Australian government bonds and look for opportunities to go long the Australian dollar.