Financial Markets

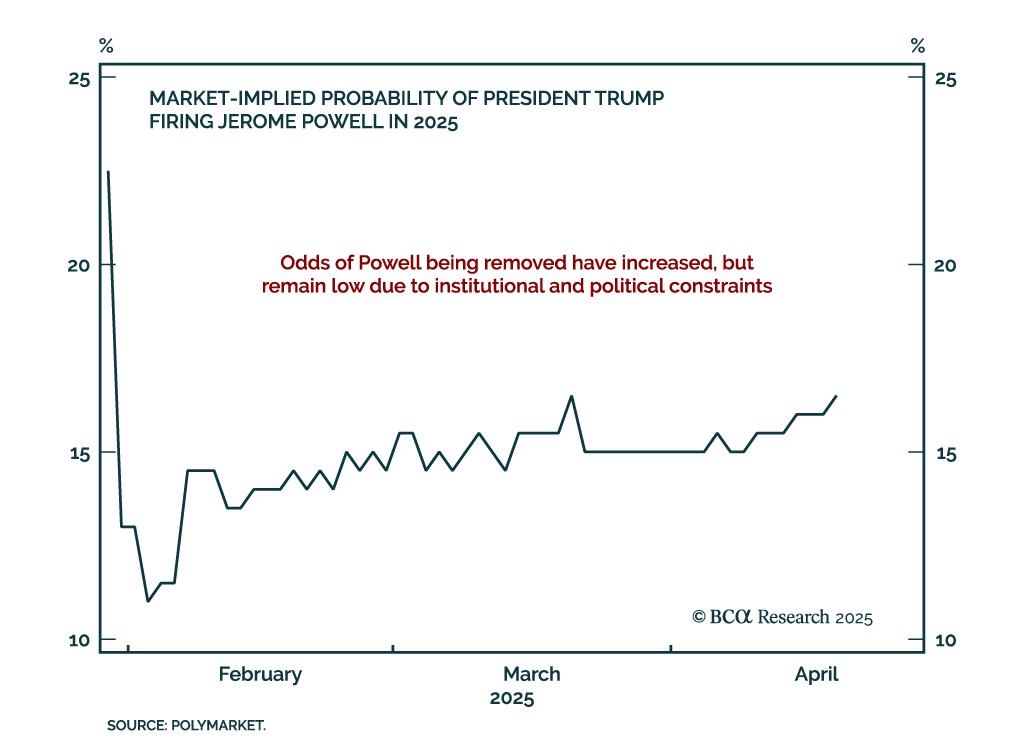

Trump’s renewed attacks on Fed Chairman Jerome Powell raise policy uncertainty but are unlikely to lead to Powell’s removal, reinforcing our expectation for continued restrictive policy and supporting our long duration stance. Trump's intensified criticism…

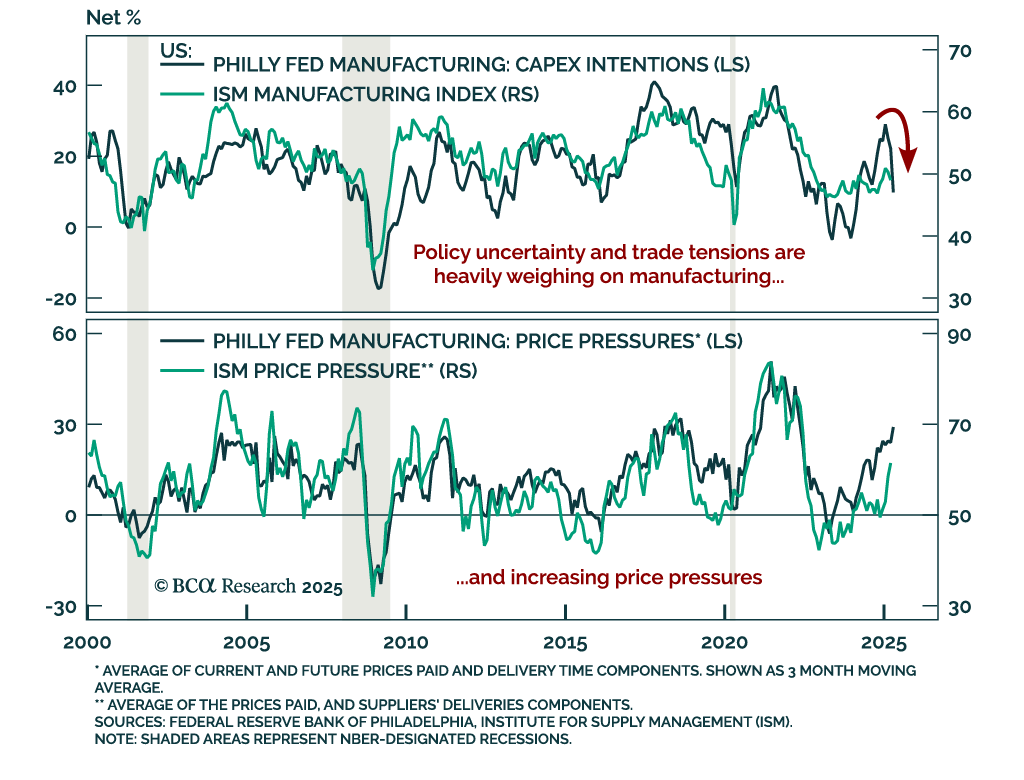

April’s Philadelphia Fed survey adds to recent stagflationary signals, reinforcing our defensive commodities positioning. The headline index collapsed to -26.4 from 12.5 in March, missing expectations and confirming the April deterioration seen in the Empire…

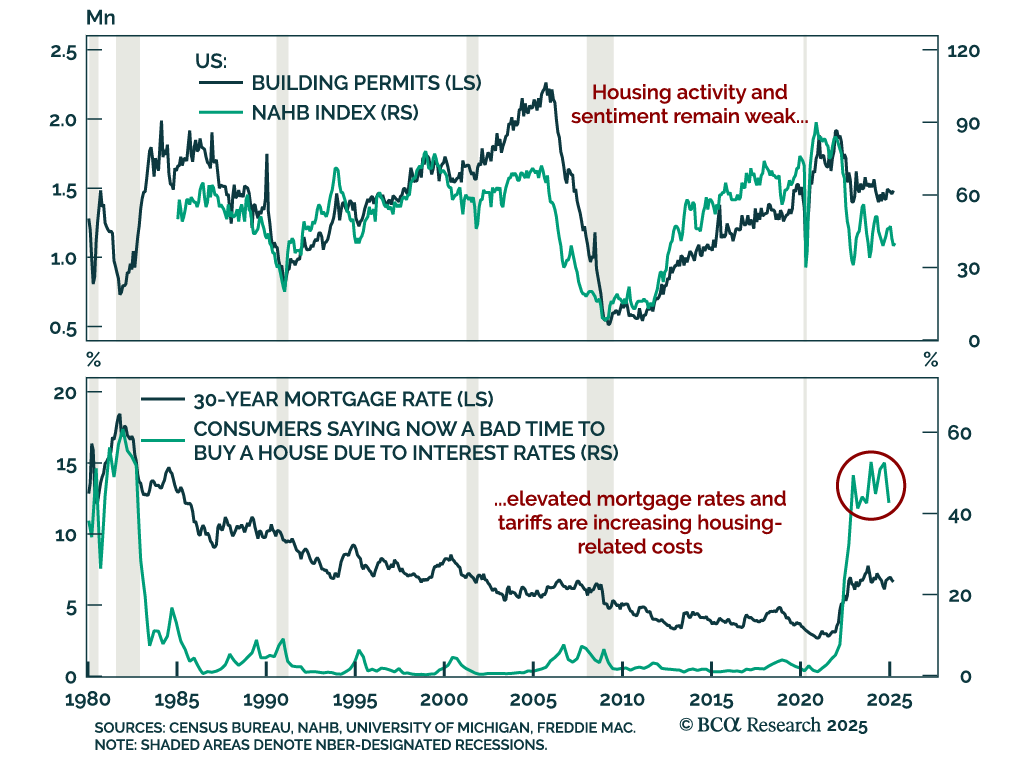

Weak housing data reinforces our defensive positioning, as recession odds remain underpriced in risk assets. US housing starts fell sharply, declining a larger-than-expected annualized rate of 11.4% in March after a 9.8% rebound in February, which was driven…

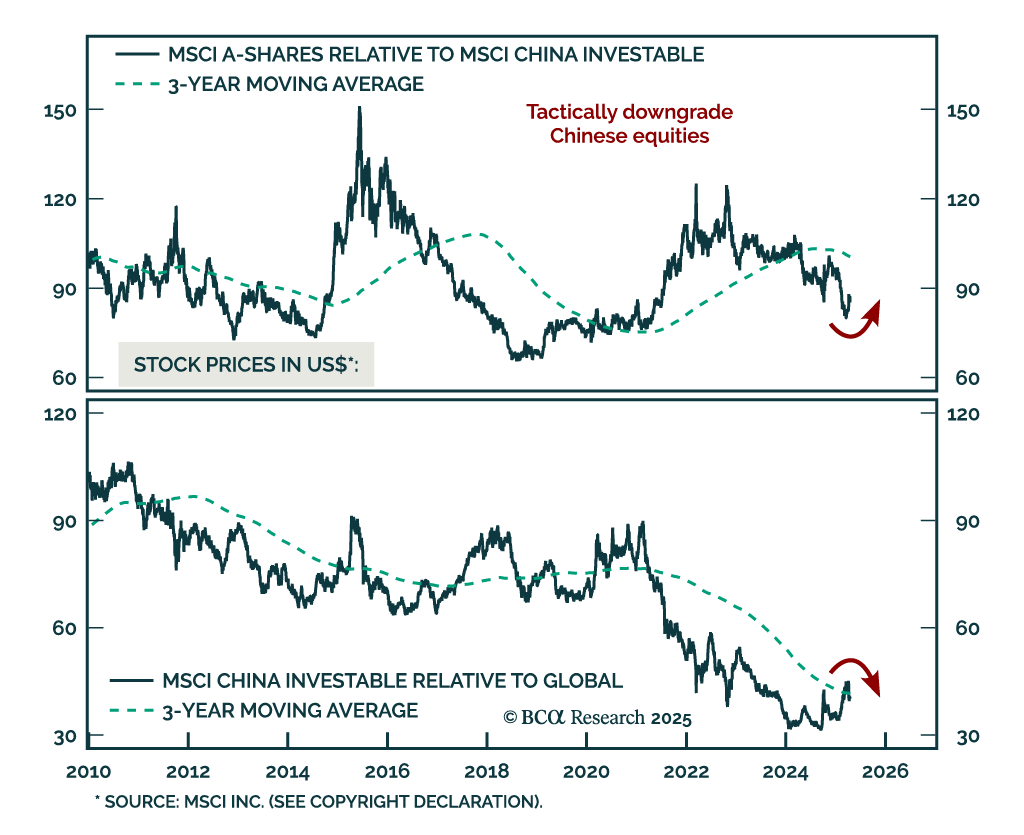

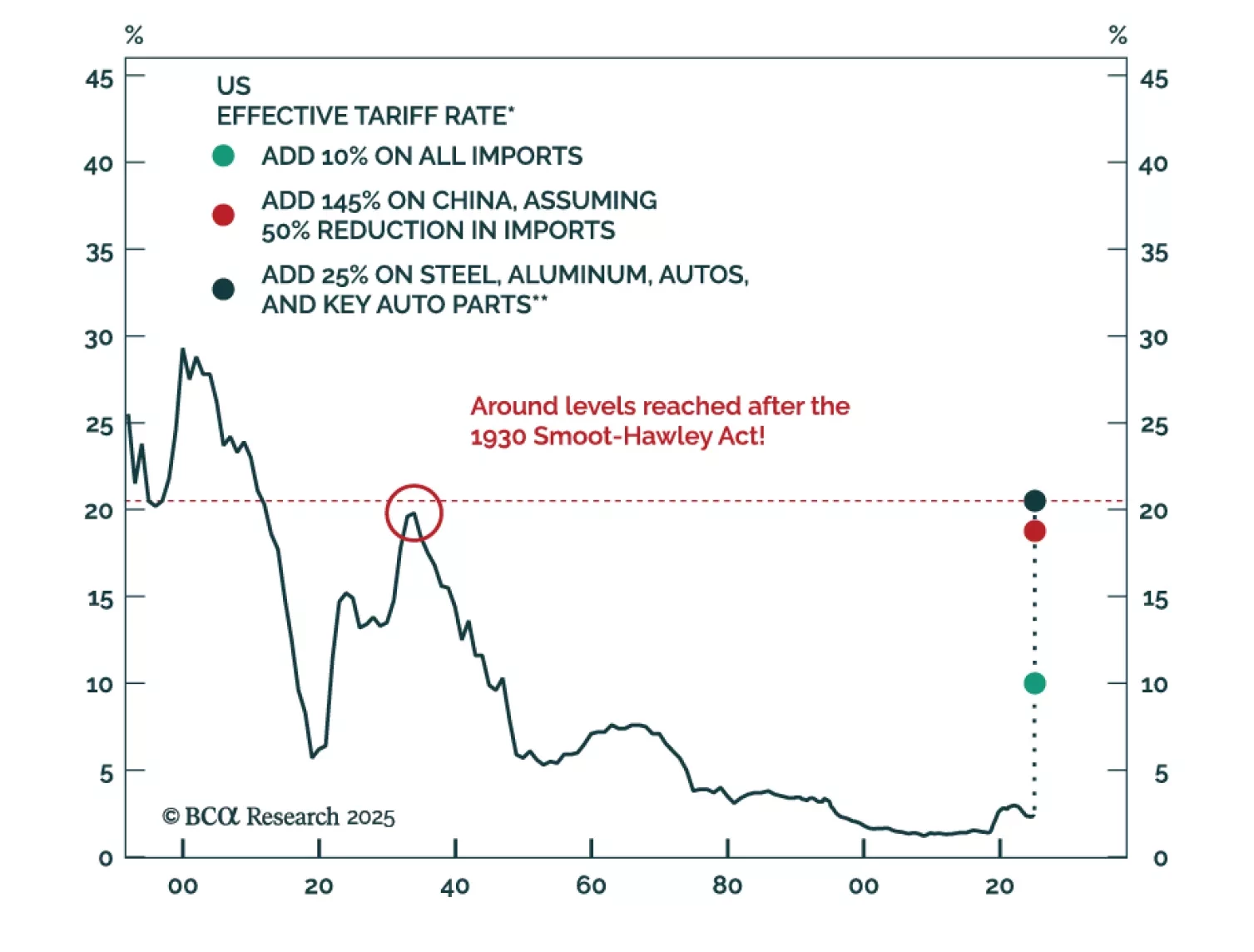

Our China strategists remain defensive and tactically downgrade MSCI China to underweight, citing escalating US China tariff tensions and subdued domestic demand. Favor government bonds over equities, defensive sectors, and A-Shares over offshore Chinese…

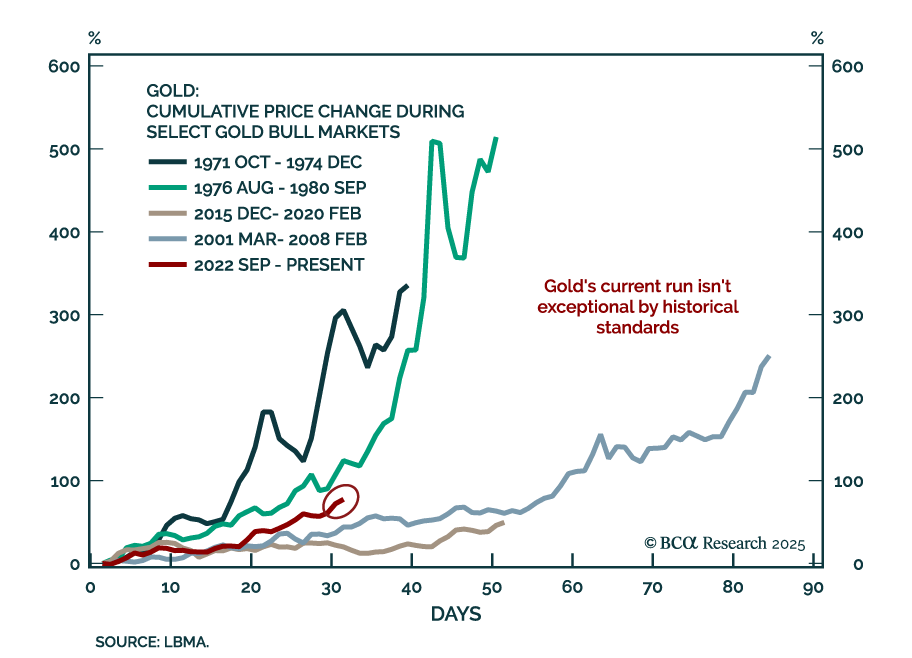

Our Commodity strategists remain defensive as both demand- and supply risks abound. Stay long gold and underweight oil and copper as increasing OPEC+ supply and tariff-driven demand risks will hurt energy and industrial metals prices. The motivations…

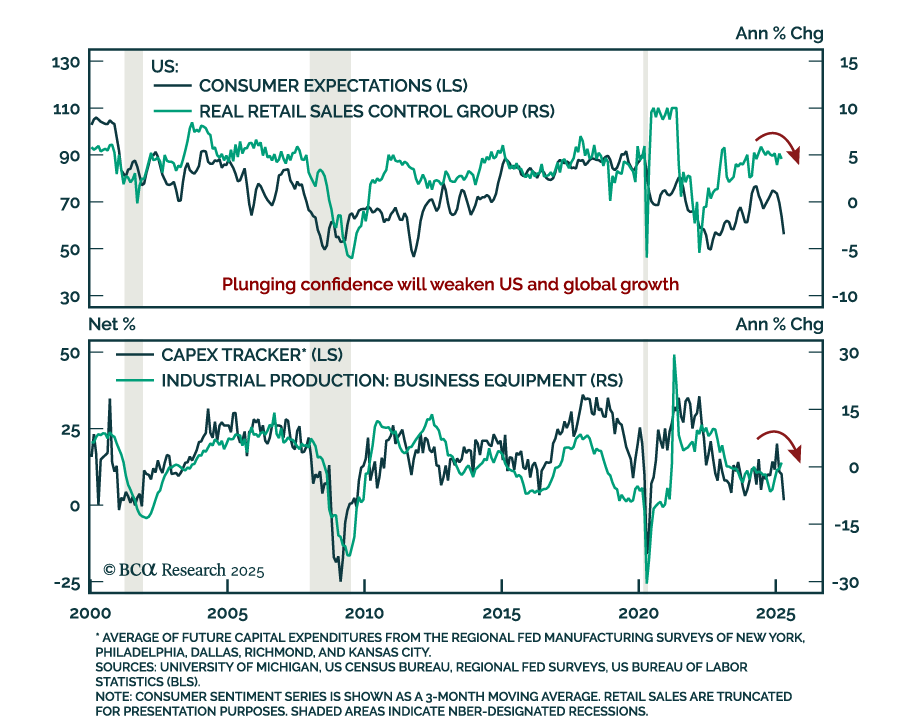

Soft data continues to deteriorate and hard data will soon follow, reinforcing our defensive asset allocation. Consumer and business confidence have plunged as policy uncertainty and inflation expectations rise, with spending, hiring and capex plans…

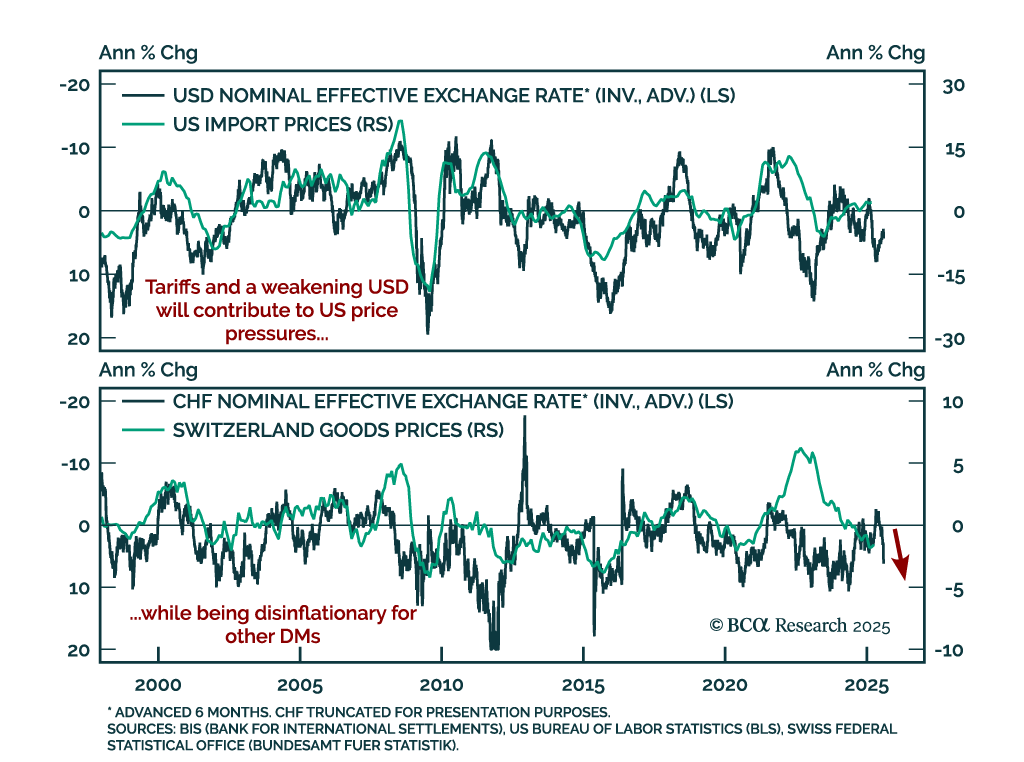

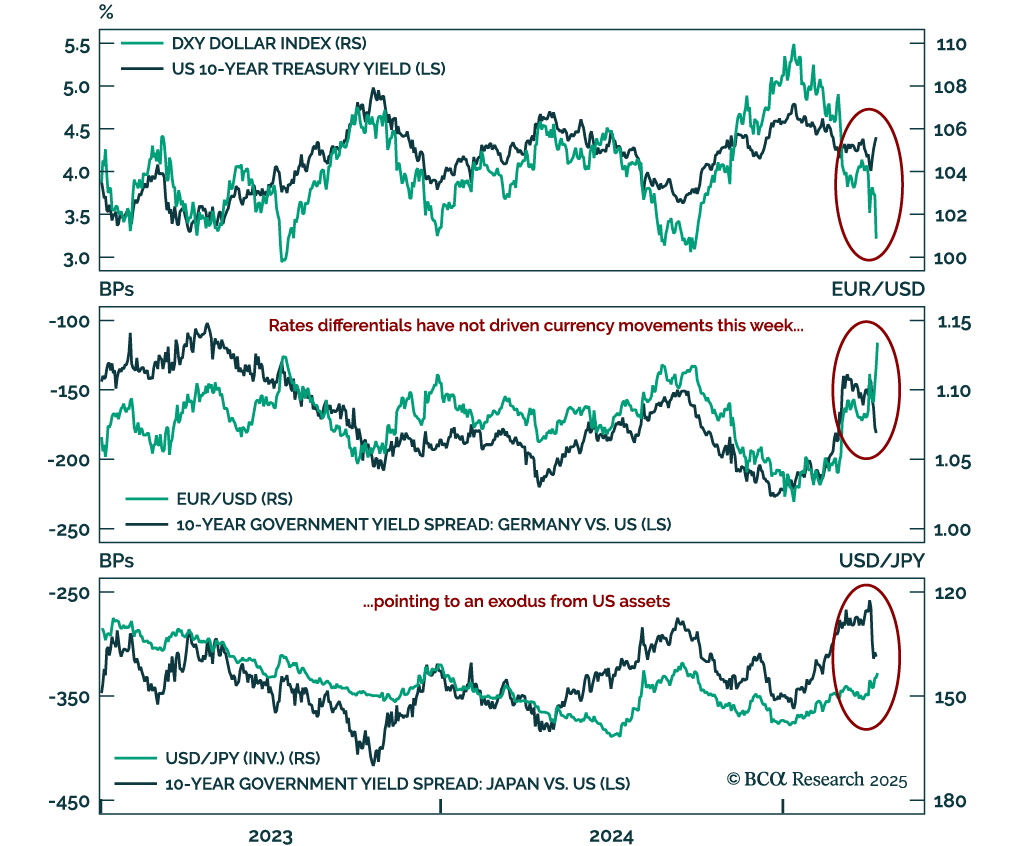

Tariff-driven inflation is diverging across economies, with the US facing mounting pressures while disinflation persists elsewhere. In theory, US tariffs should strengthen the dollar and weaken targeted currencies. In practice, the opposite has occurred: The…

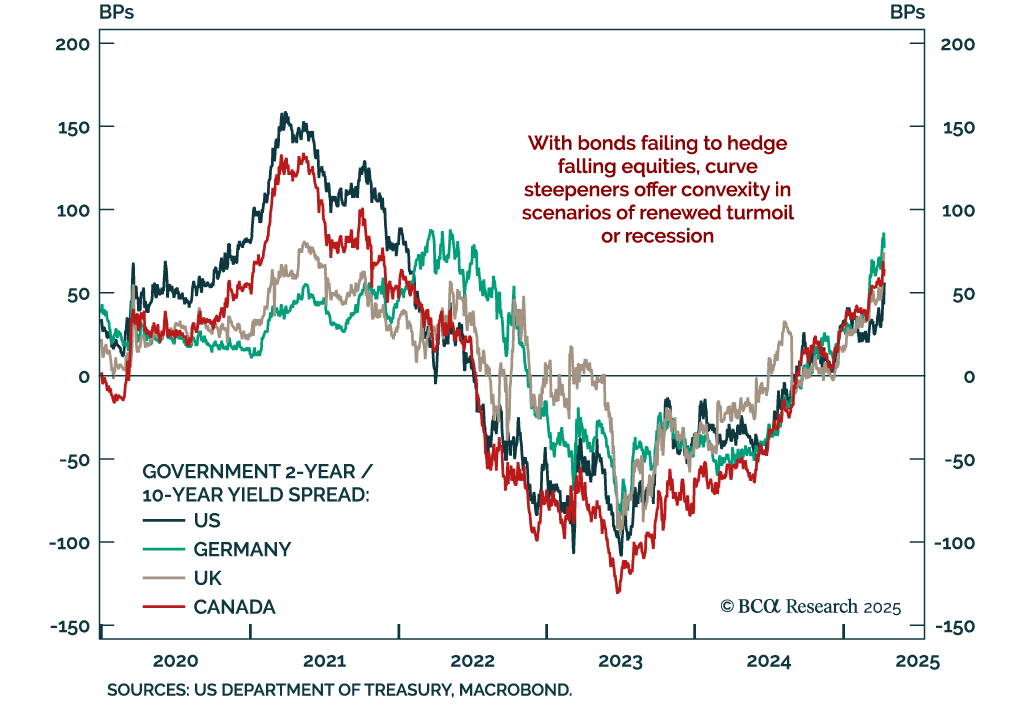

Bonds are failing to deliver defensive convexity; asset allocators should look to tactical curve steepeners for protection. Despite rising growth fears, Treasury yields have risen sharply at the long end. This is a clear break from the typical recession…

The recent breakdown in cross-asset correlations highlights mounting risk premia on US assets. Last week, the long-standing correlations underpinning our understanding of global markets violently broke down. The Treasury market turmoil had already broken the…

Barring a dramatic further de-escalation of the trade war, the US and much of the rest of the world will enter a recession over the next few months. Investors should remain defensively positioned for now.