Singapore

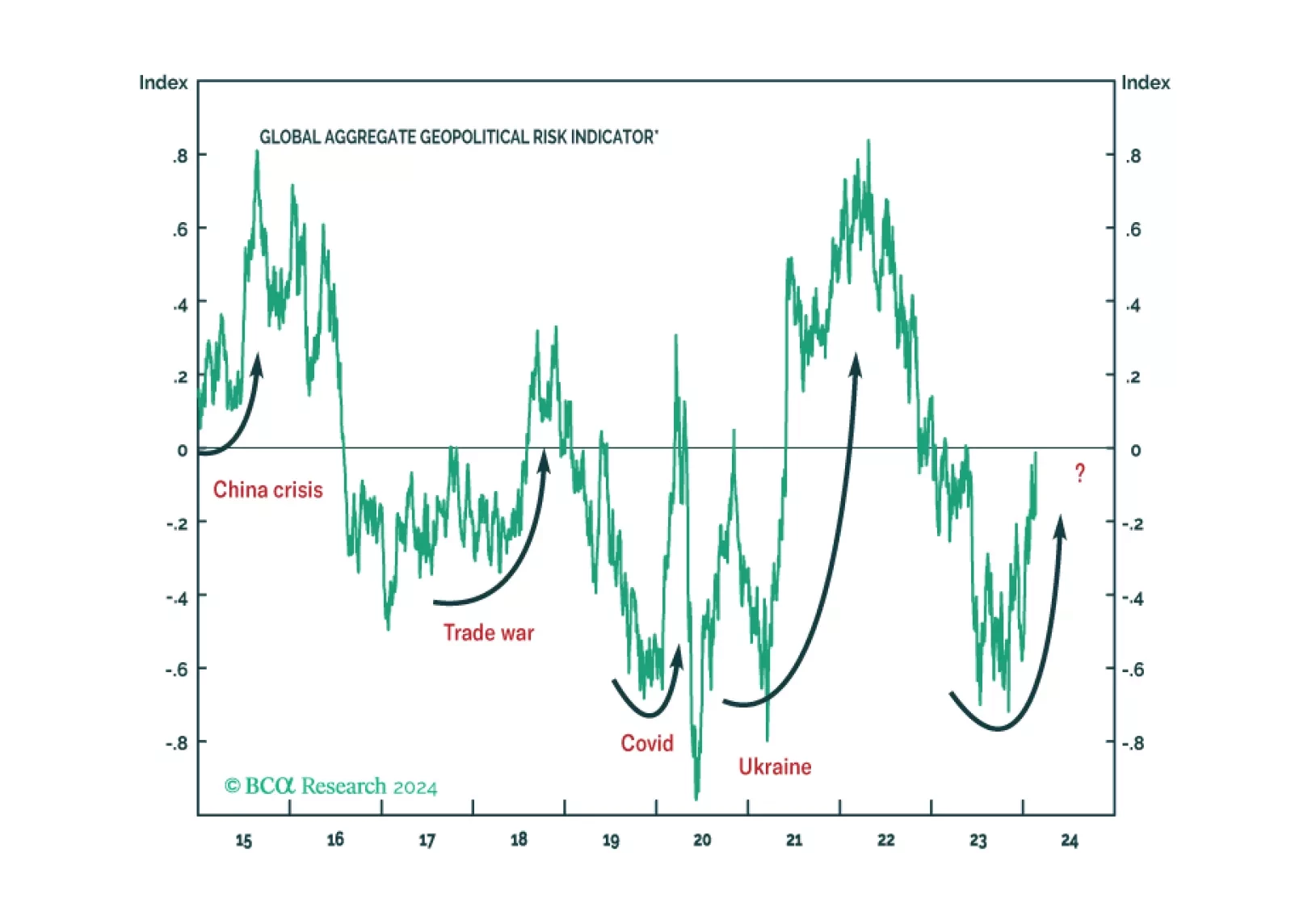

While 2024 will see various election risks, global geopolitical uncertainty is driven by the US election and its struggle with Russia, China, and Iran. The stock market can manage local domestic political risk. But it will correct upon a major outbreak of geopolitical uncertainty.

Singapore is a small open economy that is highly sensitive to fluctuations in the global manufacturing activity. As such, Singapore’s non-oil domestic exports (NODX) are a bellwether for global growth. Singapore’s NODX delivered an upside surprise on…

Singapore is a small open economy that is highly sensitive to fluctuations in global and Asian economic activity. This characteristic makes its exports a good bellwether for global growth. On this front, the upside surprise in Singapore's non-oil domestic…

Singapore’s trade data continue to send a pessimistic signal about global manufacturing conditions. The year-over-year contraction in non-oil domestic exports (NODX) deepened to -15.5% y/y in June from -14.8% y/y – marking the ninth consecutive month of…

With easing inflation, Singapore’s domestic liquidity is set to improve meaningfully. Put this bourse on an upgrade watch list. A new trade: go overweight Singapore domestic bonds relative to EM.

Singapore’s exports have historically acted as a good gauge for the health of the global economy. As a small open economy that is extremely exposed to fluctuations in the Asian and global manufacturing cycles, Singapore’s exports – particularly of electronics…

Singapore’s trade numbers continue to send a warning for the global economy. The year-on-year pace of decline in non-oil domestic exports deepened in April after slowing in the prior two months. Importantly, the weakness is particularly pronounced among…

Executive Summary Singapore stocks are at risk as an impending contraction in global trade will hurt this very open economy and its markets. The country’s foreign reserves are already shrinking as the balance of payments has slid into deficit. The Monetary Authority of Singapore’s (MAS) attempts to rein in inflation by pushing up the currency is also causing foreign reserves to contract, and local money supply to decelerate sharply. Inflationary pressures in Singapore are not entrenched and will soon subside. Wage growth is under control, and unit labor cost increases are subdued. Singapore’s export competitiveness remains robust; yet that does not preclude it from a period of shrinking exports over the next 6-12 months. Falling exports, shrinking foreign reserves, decelerating money supply and peaking inflation will dissuade MAS from pushing up the Singapore dollar much higher from current levels. Manufacturing Cycles Dictate The Performance Of Singapore Stocks Recommendation Inception Date RETURN Downgrade Singapore stocks from overweight to neutral May 10, 2021 2.3% Bottom Line: Equity investors should reduce their exposure to Singapore stocks in EM and Asian portfolios by downgrading their allocation from overweight to neutral. Absolute return investors should wait for a better entry point. Feature Chart 1Singapore Stocks' Outperformance Is Set To Take A Breather Like most global markets, Singapore stocks have sold off materially since early this year. Relative to EM and Asian counterparts, however, they have fared well – in line with our call back in May 2021 when we upgraded this bourse to overweight (Chart 1). The question is, given the changing macro backdrop − where a whiff of stagflation has permeated global investment landscapes – what should investors now do about this market? We believe that higher inflation in Singapore is a temporary phenomenon and will subside sooner rather than later. Contracting global trade, on the other hand, is a much more vital risk for this very open economy and its equity markets; and is a reason to downgrade this bourse. Indeed, Singapore stocks in absolute US dollar terms face more downside over the next several months. Relative to its EM and Asian counterparts also, this bourse’s outperformance is likely to take a breather. Asian and EM equity portfolios would therefore do well to downgrade this market by a notch from overweight to neutral in EM and Asian equity baskets. Absolute return investors should stay on the sidelines for now. Unfavorable Settings Contracting global trade and tightening liquidity will weigh on Singapore stocks in the months ahead. Global trade volumes will fall as developed countries’ demand for goods (ex-auto) shrinks following the pandemic-era binge. Chinese growth will also likely be struggling to recover. What this means is that both global manufacturing and exports are heading towards a contraction. As a very open economy where goods exports make up 115% of GDP (and services exports another 55%), manufacturing and exports of goods drive income for the entire Singaporean economy and influence its stock market cycles. Chart 2 shows how ebbs and flows in manufacturing new orders dictate Singapore’s equity market performances. Chart 2Manufacturing Cycles Dictate The Performance Of Singapore Stocks The performances of financial and real estate stocks, which make up two-thirds of the MSCI Singapore index, are also highly dependent on business cycles − which in turn, are driven by swings in manufacturing and exports (Chart 3). One reason for that is, at 23% of GDP, manufacturing is the single largest sector in the economy. By comparison, finance and insurance make up 14% of the nation’s output, and real estate 3%. Any acceleration or deceleration in manufacturing activity therefore has a strong impact on the performance of tertiary sectors, including those of banking and real estate. In addition, MAS’ tightening is causing local money supply to decelerate (discussed in more detail later). Slower money growth is never bullish for stock prices (Chart 4). Chart 3Banks And Real Estate Stocks Also Move With Manufacturing And Exports Chart 4Decelerating Money Supply Is A Bad Omen For Share Prices In sum, given the changing global macro backdrop of slowing manufacturing and trade, and elevated US inflation, Singapore stocks have not yet found a sustainable bottom in absolute terms. Relative to their EM counterparts, Singapore’s outperformance could also take a breather. During periods of weakening global trade and manufacturing, Singapore stocks usually do poorly relative to their EM peers. The top panel of Chart 5 shows US manufacturing PMI new orders as decelerating rapidly. Periods of falling and/or sub-50 PMI prints usually herald Singapore stocks’ underperformance relative to EM, with a few months lag. Singapore’s own new export orders are also about to slip into contraction territory. If history is any guide, this too entails a period of underperformance of this bourse versus EM going forward (Chart 5, bottom panel). Is Inflation Genuine In Singapore? The short answer is no; there is little genuine inflation in Singapore. The country is not witnessing any wage-price spiral either, unlike in the US. What we see there instead is just a one-off surge in inflation. Average monthly wages in Singapore have accelerated in the past year but are not out of line when compared to the past 20 years (Chart 6, top panel). Chart 5Weakening Manufacturing Orders Foreshadow Singapore Equities' Underperformance Chart 6Limited Wage Growth And Subdued Unit Labor Costs Will Rein In Inflationary Pressures A controlled rise in wages has helped keep Singaporean firms’ unit labor costs (ULCs) in check. The middle panel of Chart 6 shows ULCs for the overall economy vis-à-vis the consumer price index. ULCs are much below pre-pandemic levels. This happens to be the case even in the service sector of the economy where productivity gains are much harder to achieve. In the goods producing sector, where productivity gains are relatively easier to achieve, ULCs have remained particularly low (Chart 6, bottom two panels). What this means is that firms are facing little wage-related cost pressures. They are, therefore, less likely to pass it on to customers via higher selling prices. That, in turn, will help cap inflationary pressures in the economy. Chart 7Sharply Slowing Money Growth Points To Peaking Inflation In fact, much of the recent rise in headline and core consumer inflation in Singapore has had to do with the explosive money growth seen during the pandemic. Both narrow (M1) and broad money (M3) growth rates in Singapore accelerated in 2020 to levels not seen since the Global Financial Crisis of 2008-09. Inflation usually follows money growth with several months lag, and this time was no different. That said, both measures of money have since decelerated markedly this year. This will rein in inflationary pressures going forward (Chart 7). Looking forward, money supply itself will likely decelerate further in the months ahead. A critical reason for that is the manner in which the central bank (MAS) uses the currency to achieve its monetary policy objectives (i.e., to maintain price stability). When inflation rises, MAS typically guides the trade-weighted Singapore dollar to appreciate, in an attempt to rein in inflation. In so doing, MAS buys local currency and sells foreign currency. This reduces local liquidity and money supply. Chart 8 shows that MAS is indeed guiding the Singapore dollar up: the trade weighted currency has risen by over 3% in the past six months tracking inflation. Not surprisingly, money growth in Singapore has decelerated meaningfully. In time, that will help pull inflation lower. There was an external factor too. In the past couple of years, the country had witnessed a massive improvement in its balance of payments (BoP). It skyrocketed from a minus 3% of GDP in 2019 to a plus 27% in 2021. To prevent the currency from surging, the central bank had resorted to a rapid accumulation of foreign reserves. As MAS pumped local currency into the system while purchasing foreign currencies, local money supply boomed (Chart 9). Chart 8In Order To Check Inflation, The MAS Has Pushed The Singapore Dollar Up... Chart 9...Causing Foreign Reserves To Drop, And Money Supply To Decelerate Materially Chart 10The Trade Surplus Will Narrow, Putting More Pressure On The Balance Of Payments But the tide has turned this year. The trade surplus has rolled over and will continue to shrink as global trade is set to weaken further this year as explained above. As such, Singapore’s current account surplus will also likely roll over. The capital account has already slipped back into massive deficits; so has the BoP (Chart 10). The upshot is that foreign reserves have begun to contract. This means MAS is now selling foreign reserves to buy back local currency. This is causing a deceleration in local money supply (Chart 9, above). In sum, the absence of meaningful wage pressures, a decelerating money supply, and a strengthening currency will help Singapore see its inflation ease sooner than in the US. Can Singapore Withstand A Stronger Currency? As discussed above, Singapore’s monetary policy entails tackling higher inflation by letting the Singapore dollar appreciate in nominal terms. But given the high inflation prints, an appreciating currency would mean that it gets even stronger in real terms (i.e., in inflation-adjusted terms). An expensive currency in real terms could erode competitiveness. So, the question is, can the Singapore economy withstand a stronger currency? The short answer is yes. Chart 11 shows that while the Singapore dollar has appreciated to new highs in nominal trade weighted terms, in real terms (ULC-based) it remains at around 15-year lows. As such, currency competitiveness should not be an issue anytime soon. Notably, real exchange rates calculated using ULCs are more representative of currency competitiveness than the use of consumer prices allows. The reason is that employee compensation is a major component of any company’s overall cost structure; and therefore, ULCs matter for a company much more directly than do consumer prices. The very low levels of the ULC-based real exchange rate indicates that the Singapore dollar is still very competitive. Indeed, Singapore’s export volumes have been on an upward trend relative to global exports (Chart 12). Chart 11The Singapore Dollar Remains A Highly Competitive Currency Chart 12Singapore Is Grabbing Export Market Share From The Rest Of The World Notably, Singapore continues to attract a very high amount of FDI. This will help raise productivity going forward, thereby keeping ULCs in check down the line. All that said, strong competitiveness (i.e., the ability to maintain global market share) does not preclude Singapore from experiencing a drop in its export revenues over the next 6-to-12 months. The reason is faltering goods demand in the US and Europe after a pandemic-era overconsumption. Falling exports, in turn, will lead to shrinking foreign reserves, decelerating money supply, and finally slowing growth and inflation. This will discourage MAS from pushing the Singapore dollar much higher from current levels. As Chart 11 showed, the Singaporean currency is already at an all-time high in trade-weighted terms. The rally in the trade-weighted Singapore dollar is therefore in late stages. Investment Recommendations Chart 13The Singapore Dollar's Outperformance Vesus Other Asian Currencies Is Late Singapore stocks, with a P/E ratio of 21.5, have become relatively expensive vis-à-vis their EM (13.1) and Asian (14.1) counterparts. In terms of the price-to-book value ratio however, they are not expensive. Considering all, we recommend that investors reduce their exposure to Singapore stocks in EM and Asian equity portfolios by downgrading their allocation from overweight to neutral. Our overweight stance since May 10, 2021, has yielded a gain of 2.3% so far. Absolute return investors should wait for a better entry point. The depreciation of the Singapore dollar vis-à-vis the US dollar likely has some more room given the impending deterioration in global trade. But the latter will also soon check the appreciation of the Singapore dollar versus other Asian currencies − as MAS will be dissuaded from guiding the currency up in view of peaking domestic inflation and shrinking trade (Chart 13). Rajeeb Pramanik Senior EM Strategist rajeeb.pramanik@bcaresearch.com

Singapore is a small open economy that is extremely sensitive to fluctuations in the Asian and global manufacturing cycles. The country’s exports have historically been a good leading indicator of global economic activity. This is especially true for its…