AI and Markets

This report addresses five frequently asked questions from our Greater China clients over the past few months.

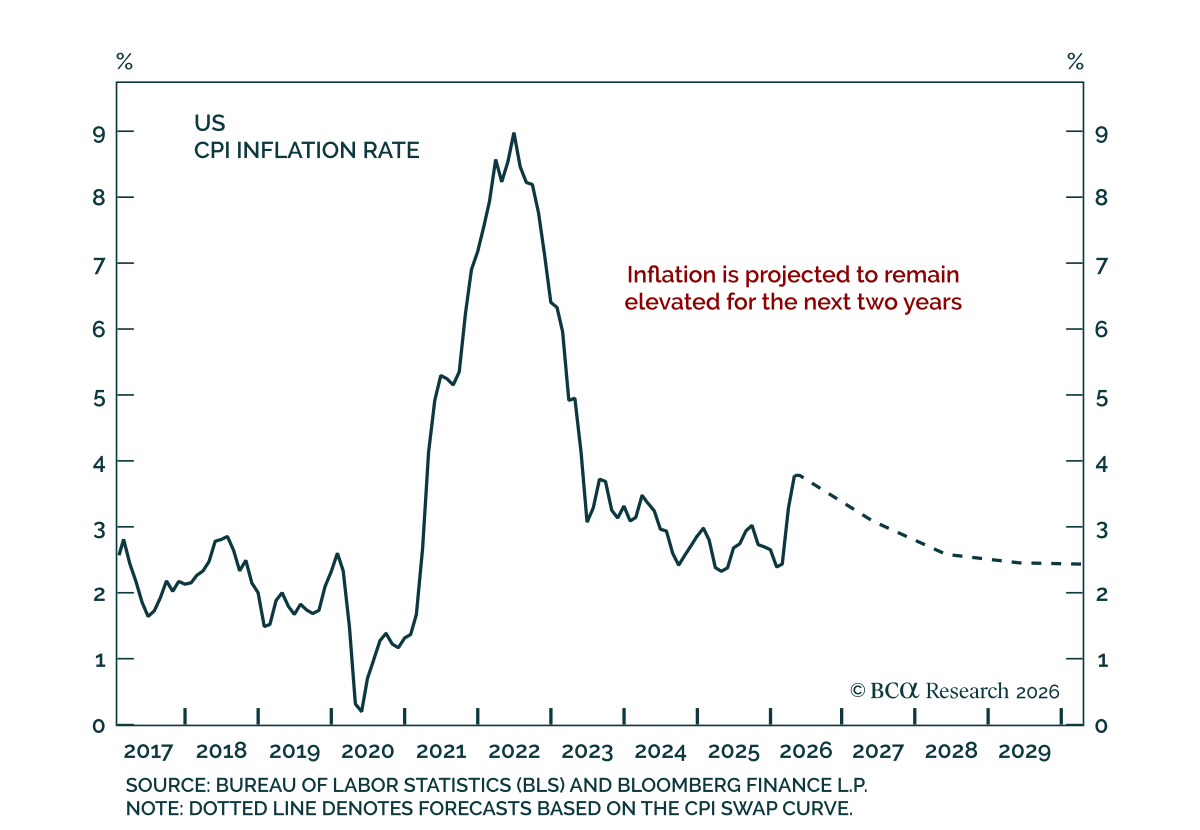

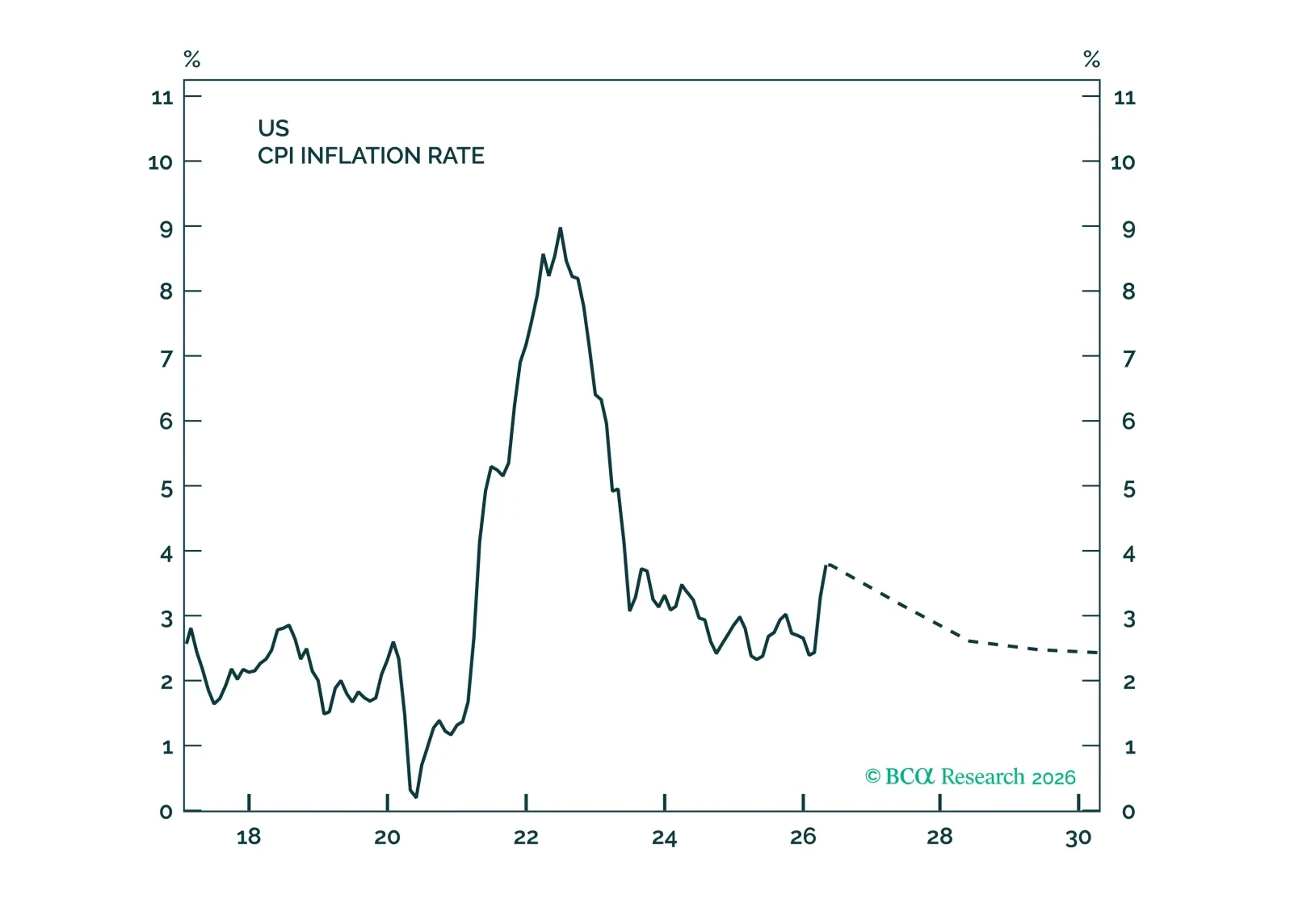

The AI boom will increase inflation in the near term and could also raise it over the long term. The Fed’s reluctance to hike rates is understandable, but it risks amplifying what may already be a brewing stock market bubble.

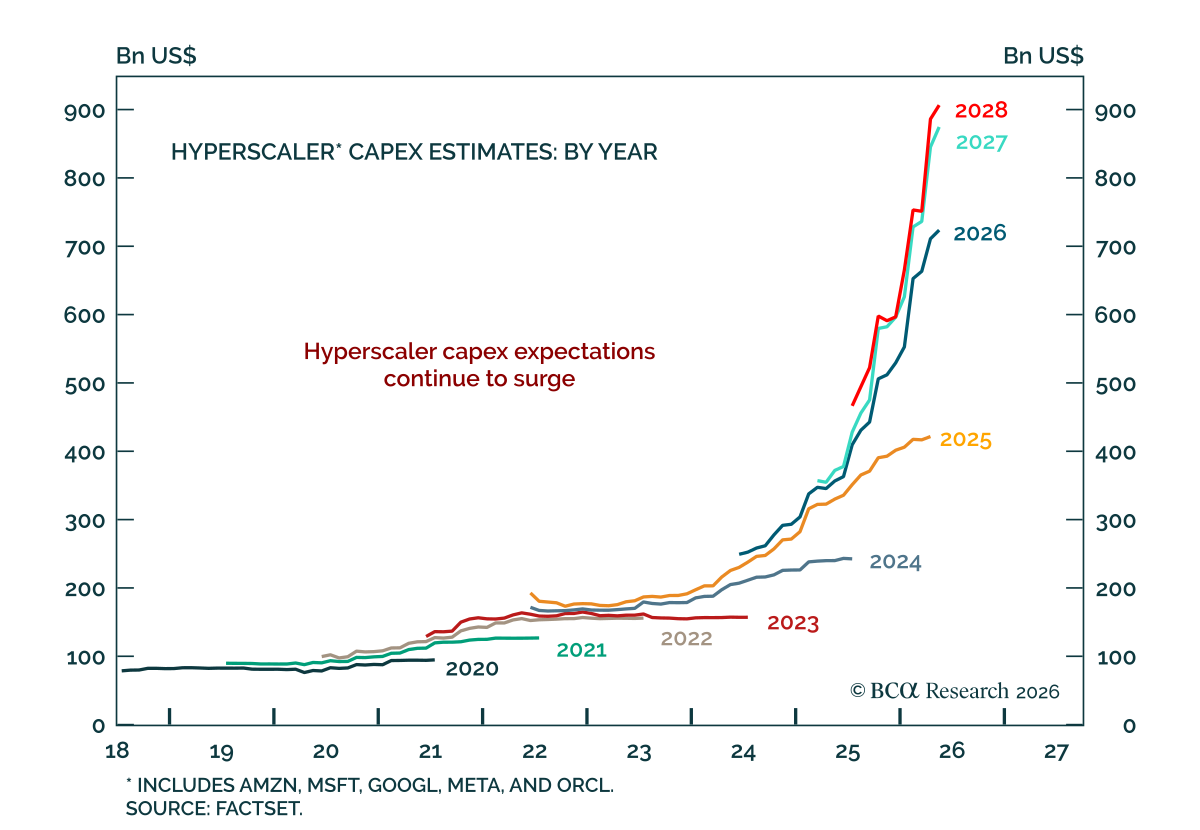

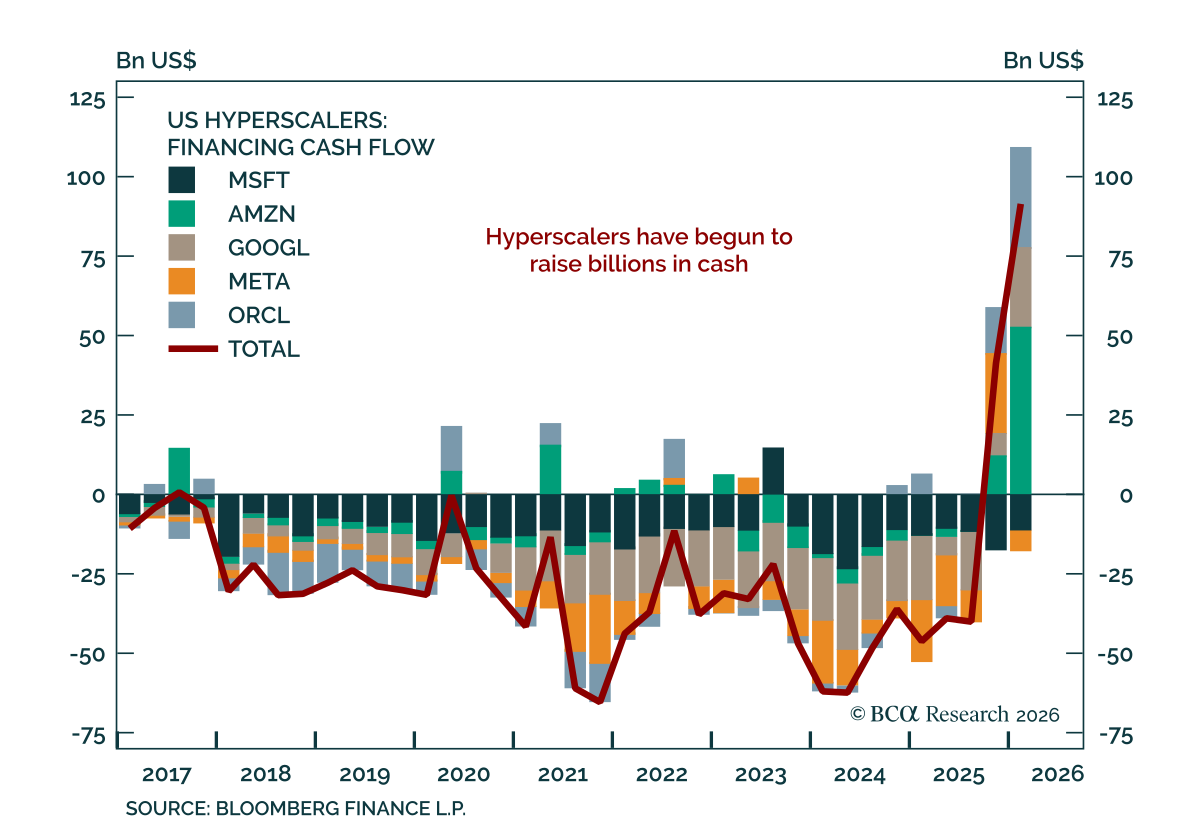

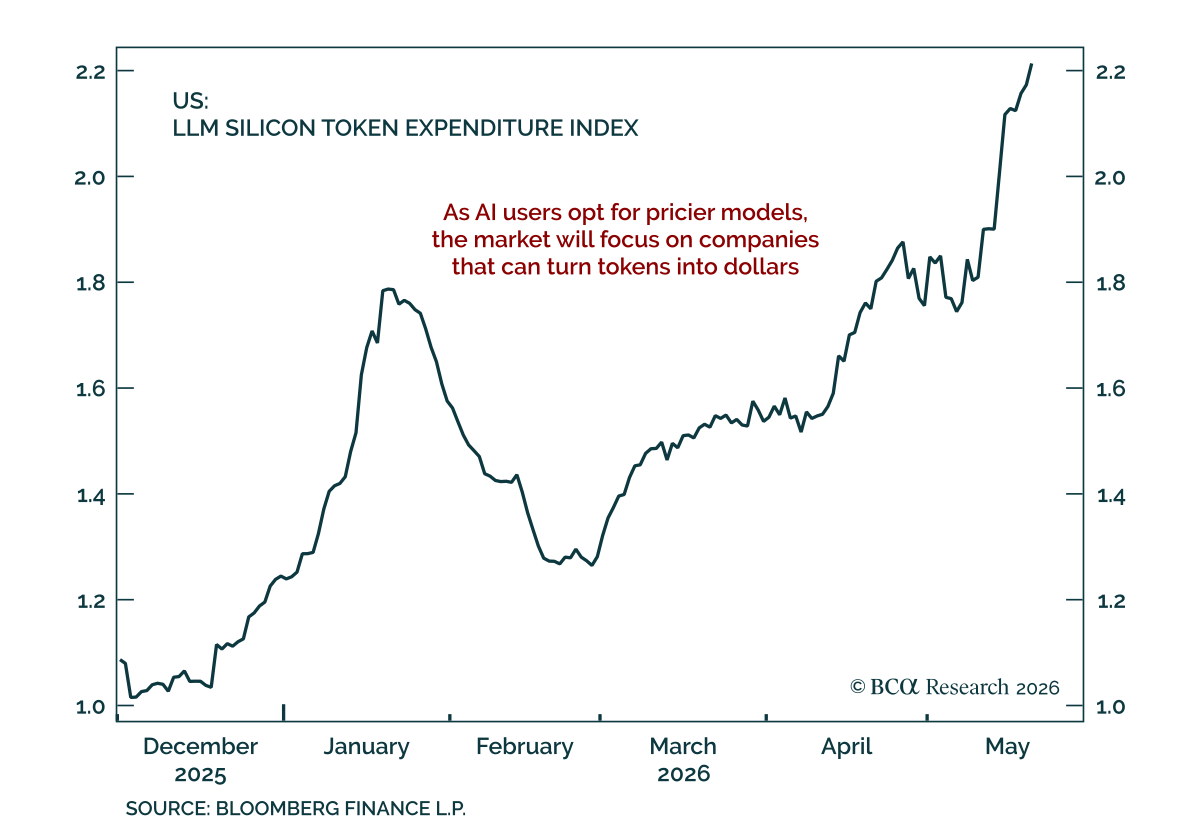

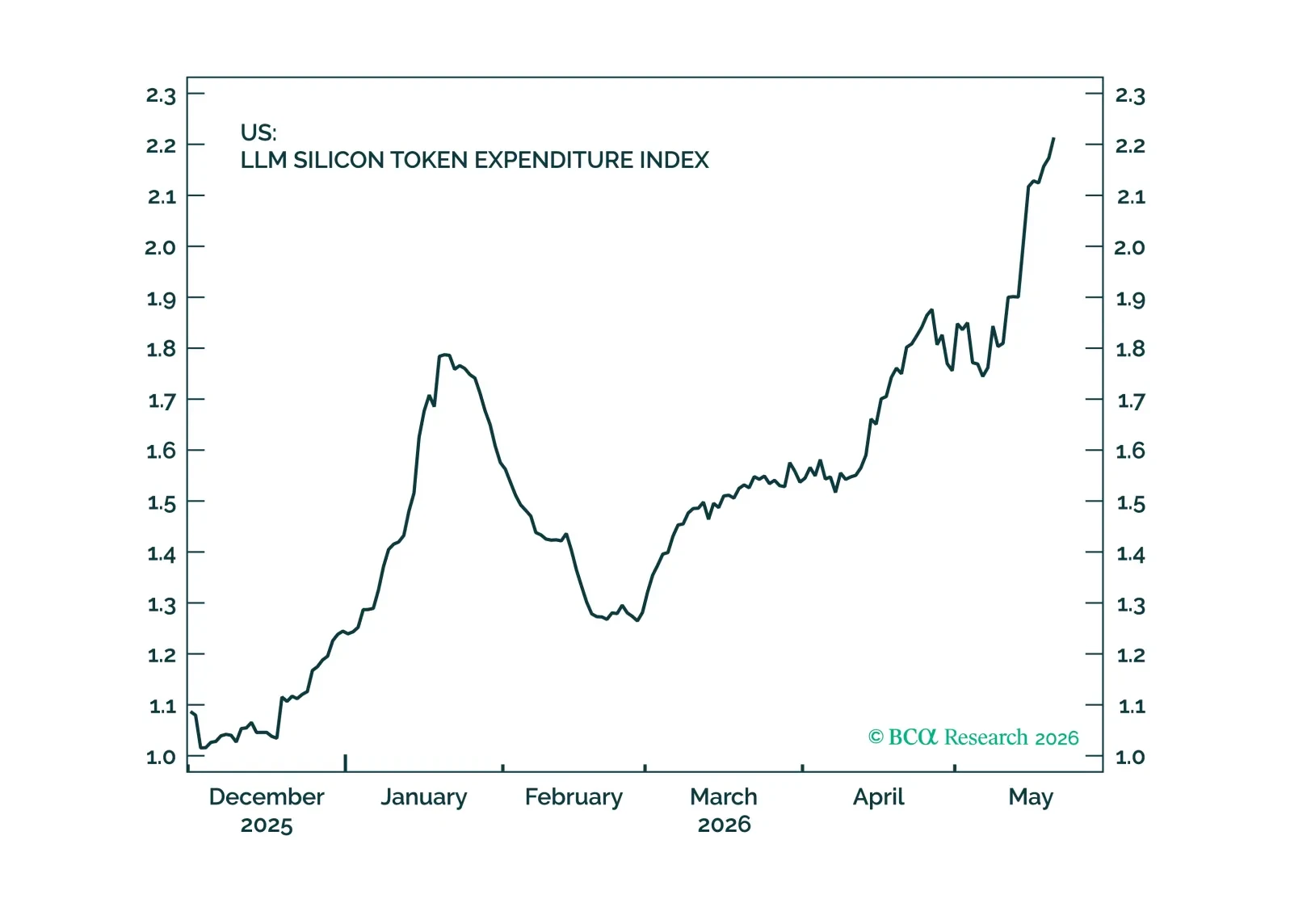

So far most of the value in the AI supply chain has been captured by hardware companies. However, as model providers shift to usage-based pricing, value will begin to accrue to models and applications. Communications Services and Software should benefit from this shift. This broadening of the AI story, along with solid economic momentum should keep the rally going for the rest of the year. Remain overweight equities. Downgrade Energy to Neutral. Buy Software.

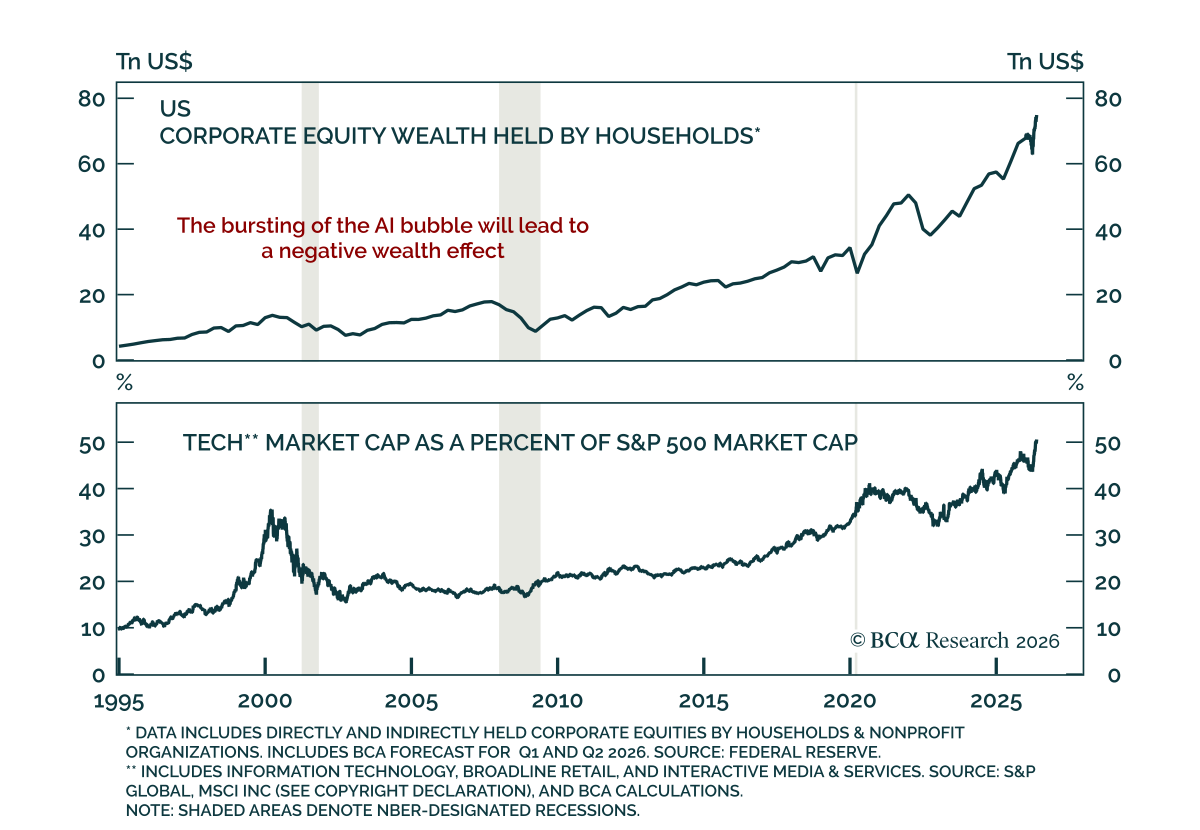

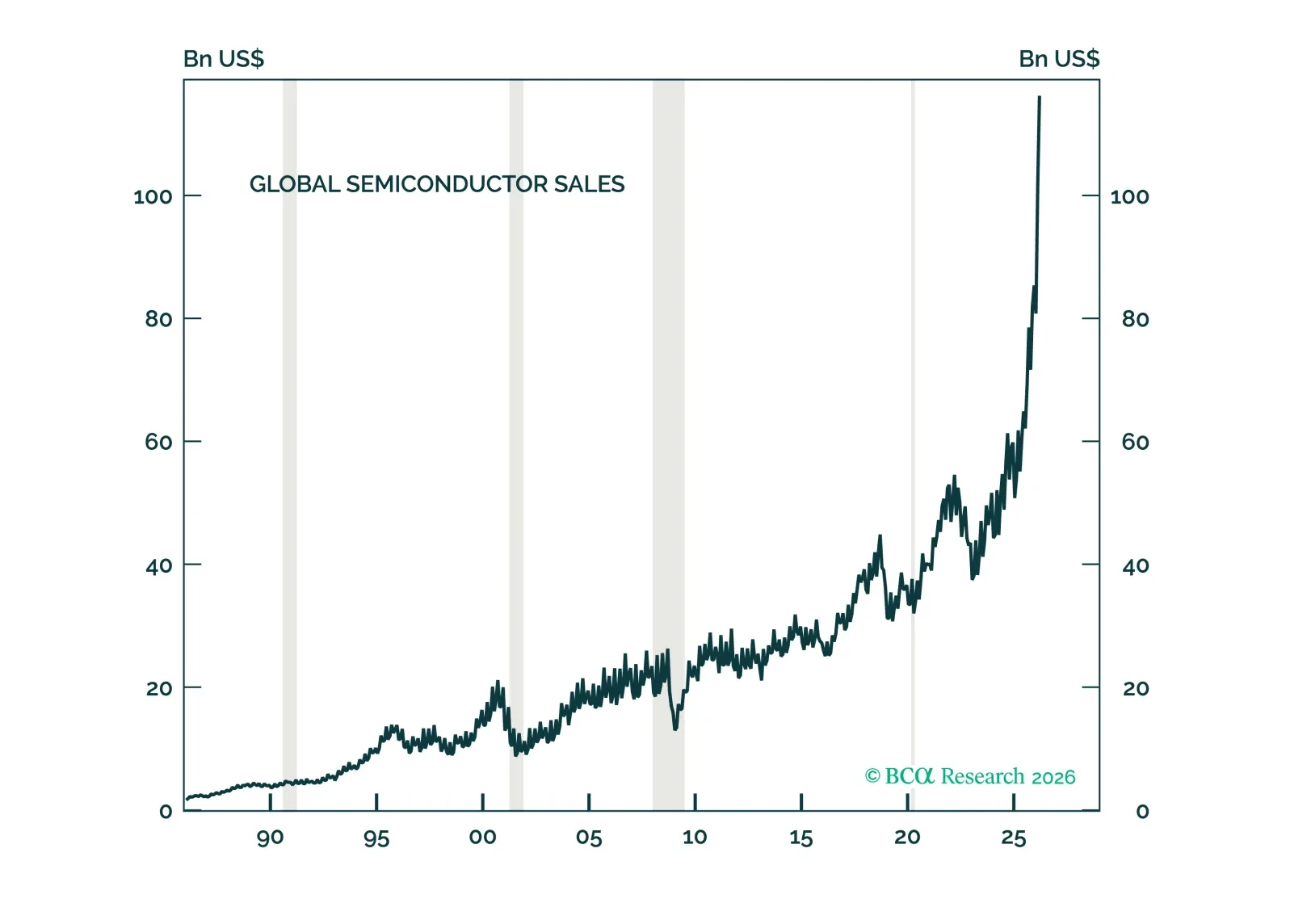

The AI bubble is a different type of bubble. It is primarily an earnings bubble rather than a valuation bubble. Like all bubbles, the AI bubble will burst. For now, however, our AI demand indicators do not suggest that this is imminent.