Australia

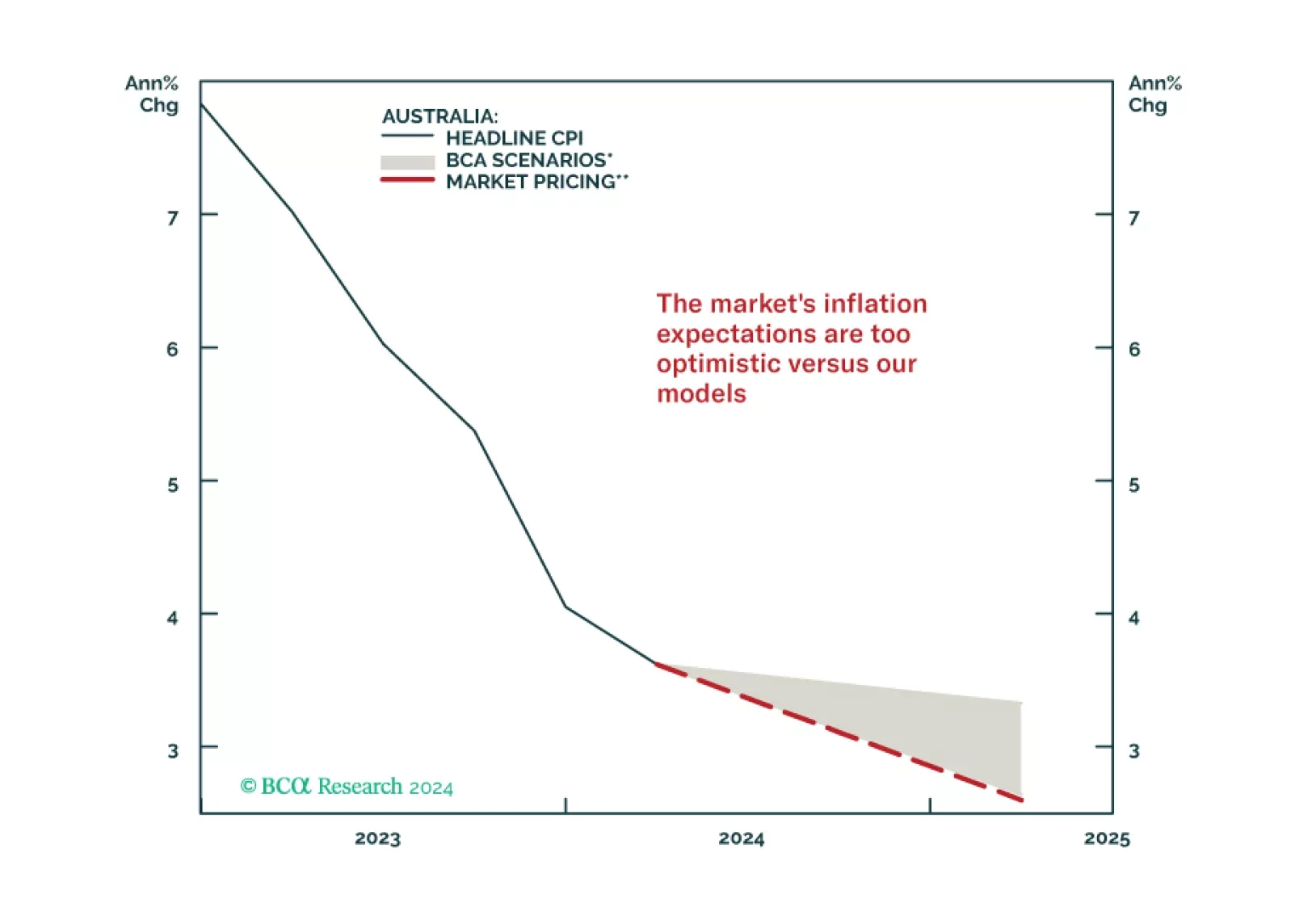

Australia’s inflation for May was released on Tuesday. Annual headline CPI increased from 3.6% in April to 4%, outpacing expectations of 3.8%. Trimmed-mean inflation also increased from 4.1% to 4.4%. Individual components diverged. Food and non-alcoholic…

The Reserve Bank of Australia kept its cash rate at 4.35% at its policy meeting on Tuesday, in line with market expectations. Australia’s monthly measure of headline inflation came in at 3.6% in April, still considerably above the midpoint of the RBA’s 2-3%…

In light of this week’s RBA decision to keep policy on hold, we look at the best possible trades in fixed income markets. In our view, inflation-linked bonds, relative to nominals remain a good bet.

According to BCA Research’s Global Investment Strategy service, aggressive fiscal stimulus and labor market flexibility contributed to the relative strength of the US consumer. However, adverse region-specific effects also played a role. Most notably, the…

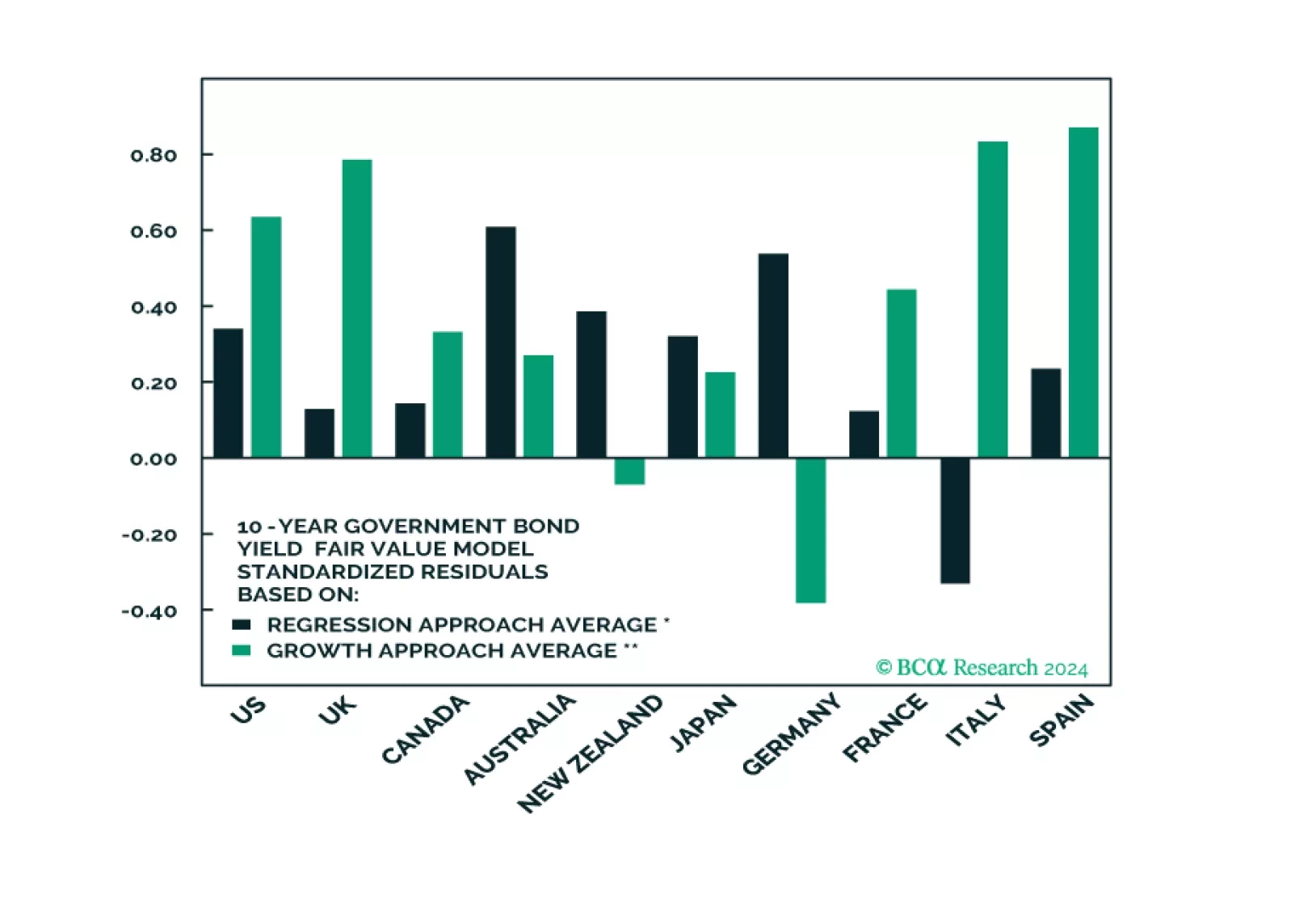

In this Special Report we assess the absolute and relative attractiveness of developed market government bonds using several fair value models. Longer-term investors who are focused on value should overweight US long-maturity bonds, and favor Spanish, Australian, and potentially UK government bonds within a DM ex-US allocation.

Despite historically high interest rates and the fact that variable-rate mortgage issuances dominate the mortgage market landscape, Australian home prices continue to climb at a close to double-digit annual rate. The Core Logic House Price index is now…

The Reserve Bank of Australia (RBA) left its policy rate unchanged at 4.35% at its May meeting, in line with expectations. The statement highlighted that inflation continues to moderate, though at a slower-than-expected pace. Board members also pointed out…

Tuesday’s Australian inflation release came in hotter than anticipated. Quarter-on-quarter headline inflation increased from 0.6% in Q4 2023 to 1% in the first quarter of this year, above expectations of 0.8%. Although annual inflation declined from 4.1% to…

It is too early for the RBA to begin cutting rates. Inflation remains above target, with core CPI currently standing at 3.4%, one of the highest numbers amongst major economies. The labor market is also fundamentally strong. Australia’s unemployment rate…

The Aussie dollar was among the worst performing G10 currencies on Tuesday on the back of a shift in tone in the Reserve Bank of Australia’s post-meeting statement. Specifically, the RBA replaced the hawkish bias that “a further increase in interest rates…