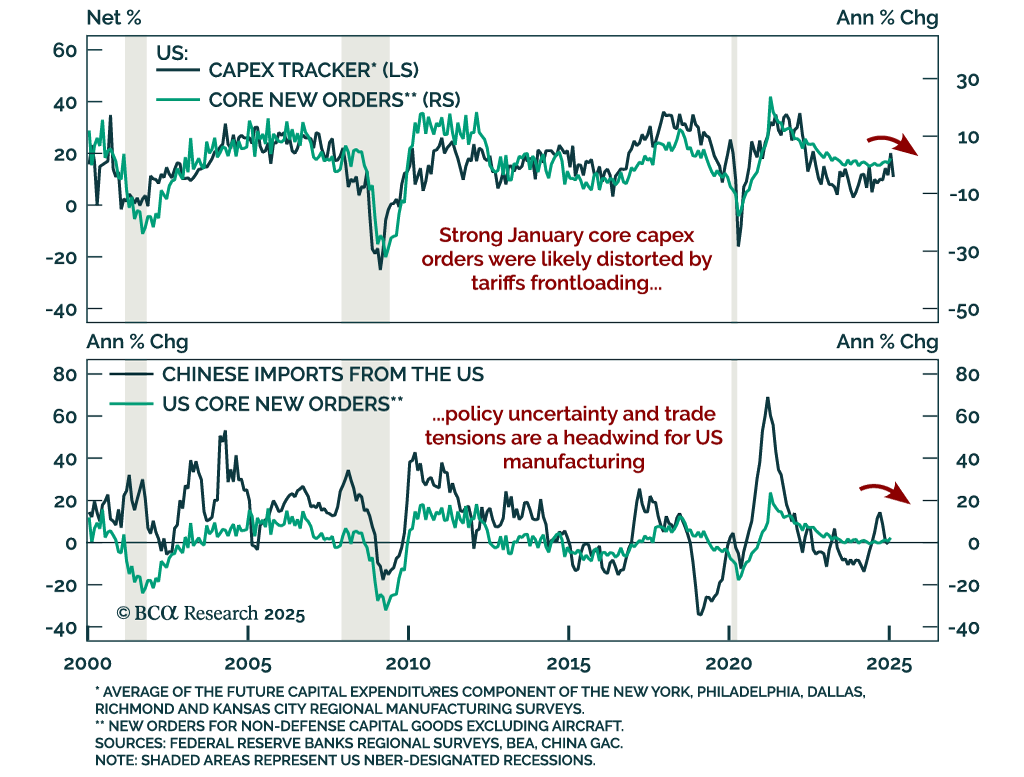

Capex

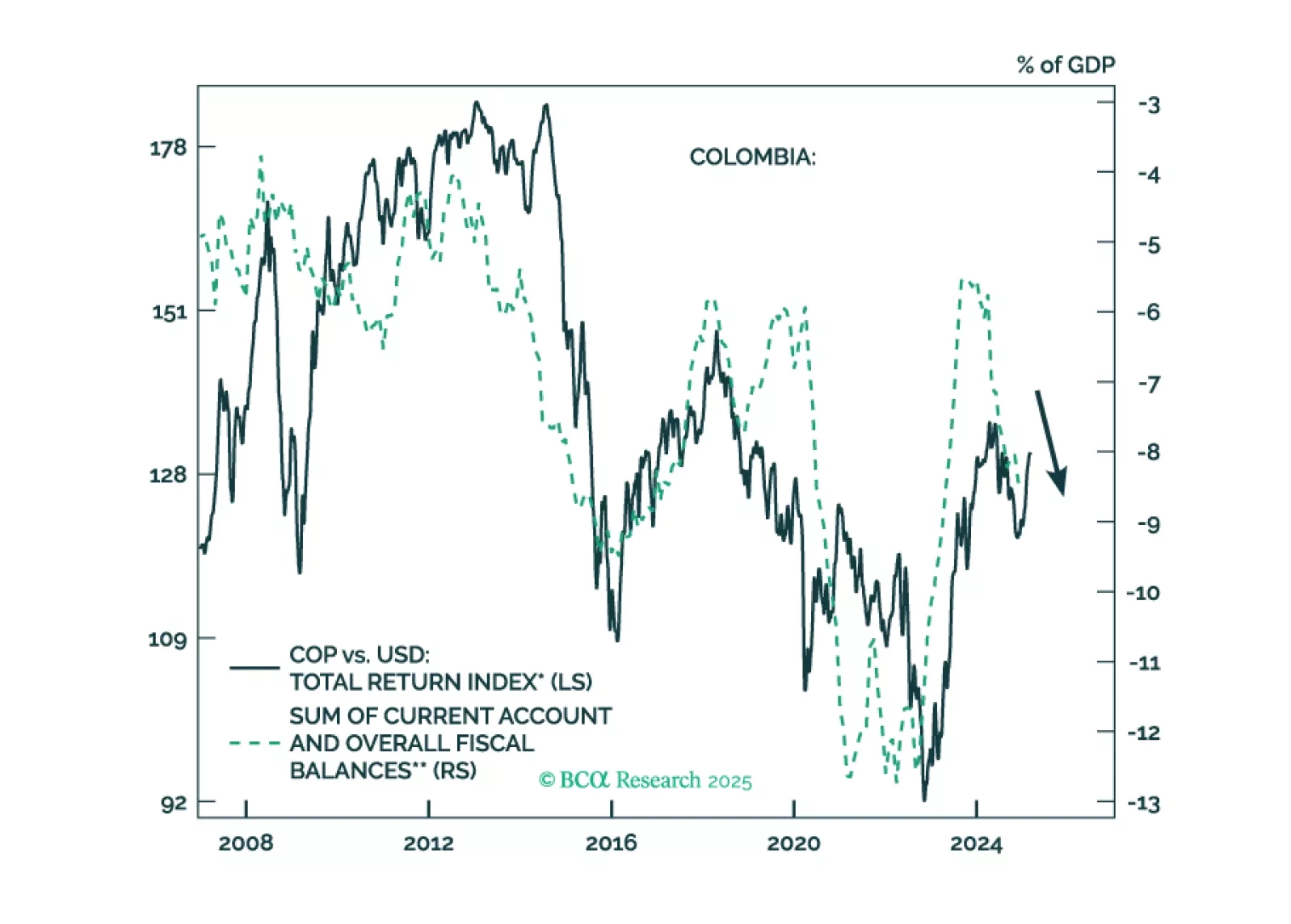

Colombian financial markets have rallied on the expectation that a right-wing government will be elected in 2026. We take a contrarian bearish stance on the nation's financial markets. Colombia is suffering from two structural macro issues – unsustainable public debt and plunging energy exports – that will not be easily solved by a conservative administration in 2026. Continue underweighting Colombia within EM equity and fixed-income portfolios, continue shorting the COP versus the USD and the CLP, and bet on yield curve steepening.

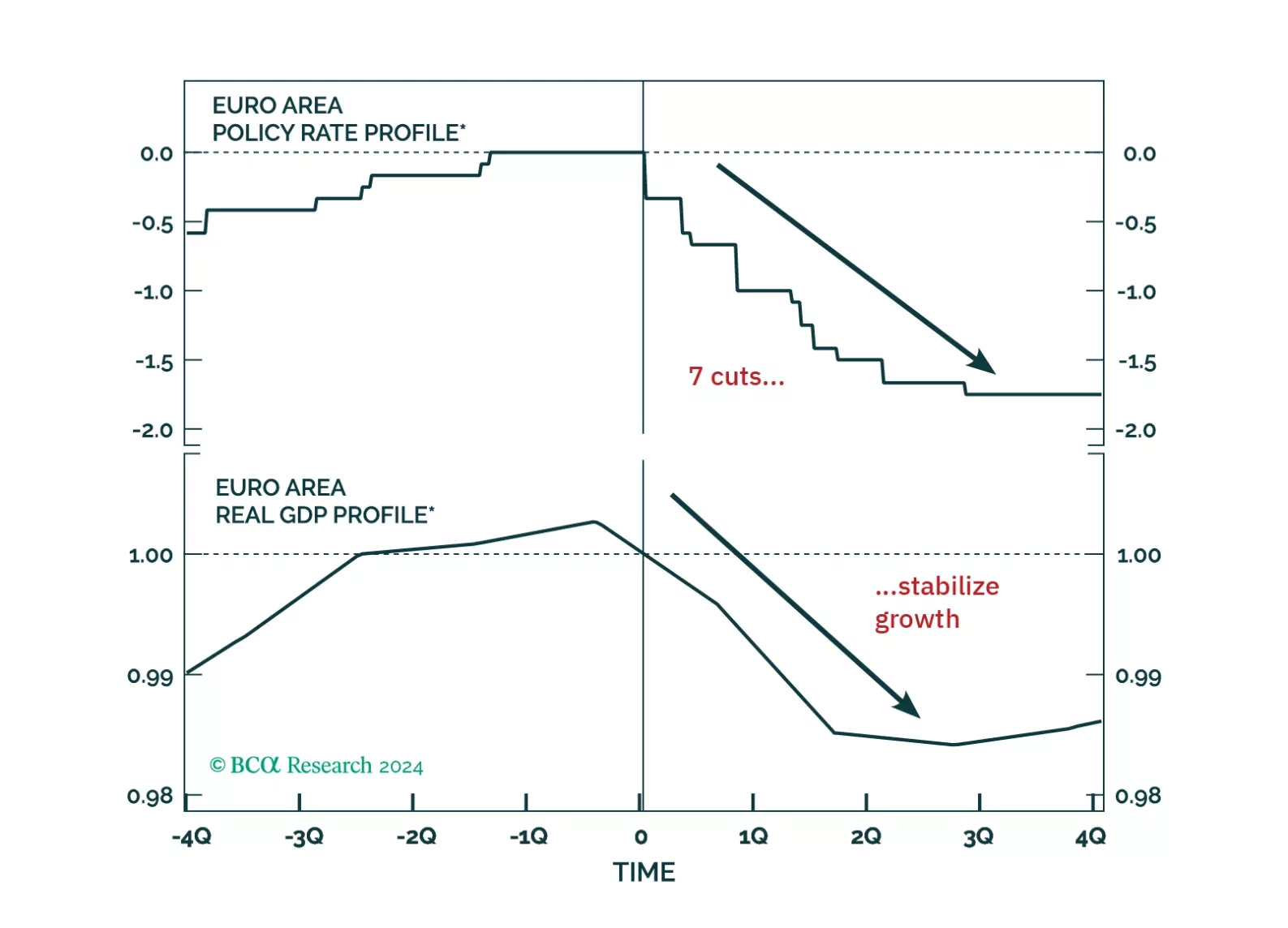

The ECB cut rates as expected, but rising yields and a stronger euro are tightening financial conditions just as fiscal policy shifts the macro landscape. With more rate cuts ahead and market positioning stretched, we outline the key risks, investment opportunities, and our updated call on the ECB’s terminal rate. Read our full report for actionable insights.

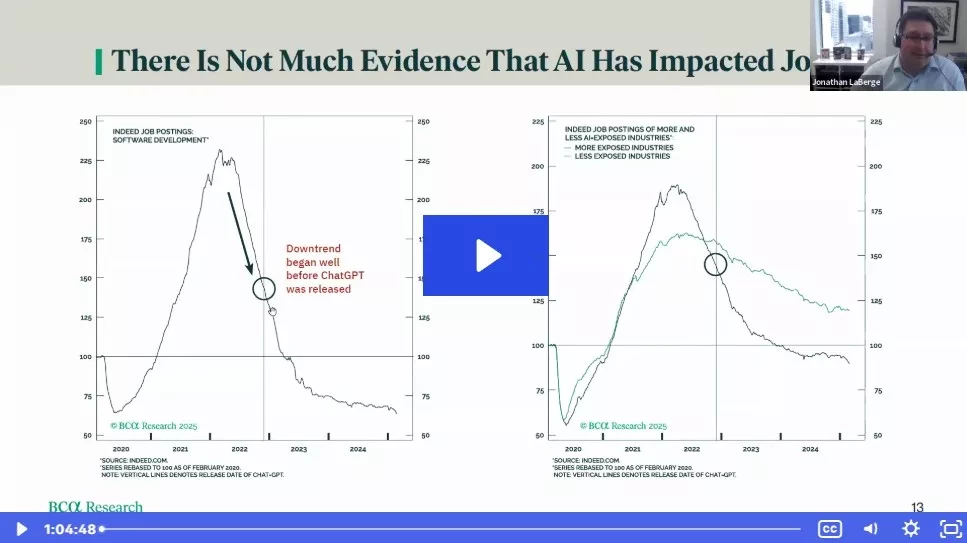

In Section II, Jonathan presents a checklist that investors can use to confirm whether AI’s purported productivity gains are real. The checklist does not currently suggest that artificial intelligence is meaningfully boosting productivity growth. US equity valuation reflects very significant optimism about AI, underscoring the profound risk facing equity investors if the narrative about AI shifts in a pessimistic direction.

In Section I, Doug notes that the chaos of the new administration, including bellicose tariff threats and DOGE’s abrasive and indiscriminate approach, are sowing uncertainty and fortifying economic headwinds. Lowered guidance of prominent retailers, alongside weakening services PMIs, bode poorly for economic activity considering that improving manufacturing PMIs likely reflect tariff frontrunning. A recession remains our base case, suggesting that investors should be underweight stocks within multi-asset portfolios. In Section II, Jonathan presents a checklist that investors can use to confirm whether AI’s purported productivity gains are real. The checklist does not currently suggest that artificial intelligence is meaningfully boosting productivity growth. US equity valuation reflects very significant optimism about AI, underscoring the profound risk facing equity investors if the narrative about AI shifts in a pessimistic direction.

Eurozone banks have quietly outpaced the Magnificent 7—can they keep winning? With strong balance sheets, rising profitability, and structural tailwinds, European lenders still offer value despite short-term risks. Meanwhile, German equities continue to defy expectations, but is a near-term pullback on the horizon?

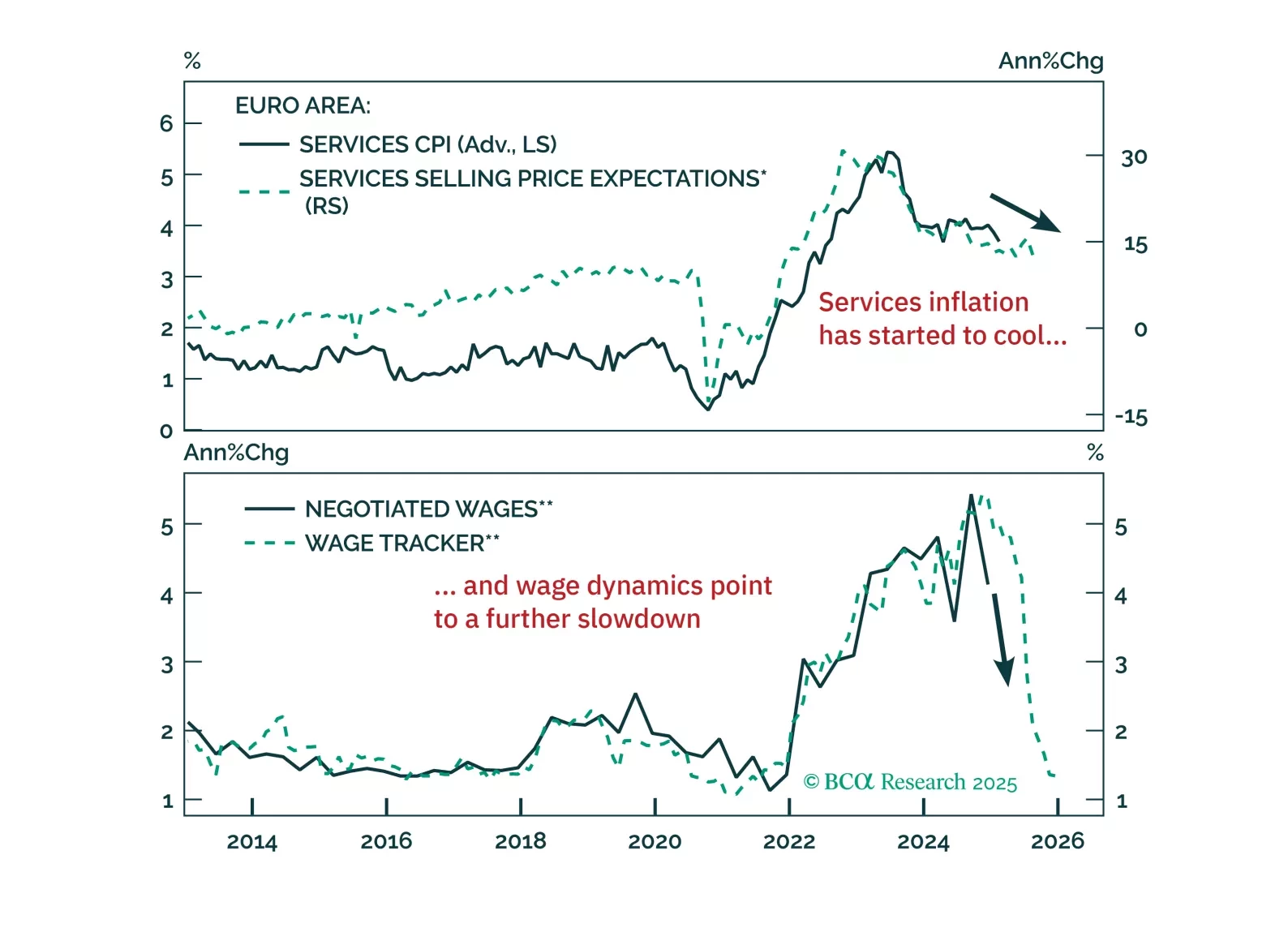

The ECB cut its deposit rate to 2.75%, as was widely anticipated. President Christine Lagarde did not provide any fireworks, but the Governing Council’s message was clear: Policy is restrictive, and inflation will fall further. As a result, if we combine our economic forecasts for the Eurozone with Frankfurt’s data dependency, we continue to expect the ECB’s deposit rate to settle below 2%. Consequently, German bond yields have downside, and the euro has yet to bottomed.

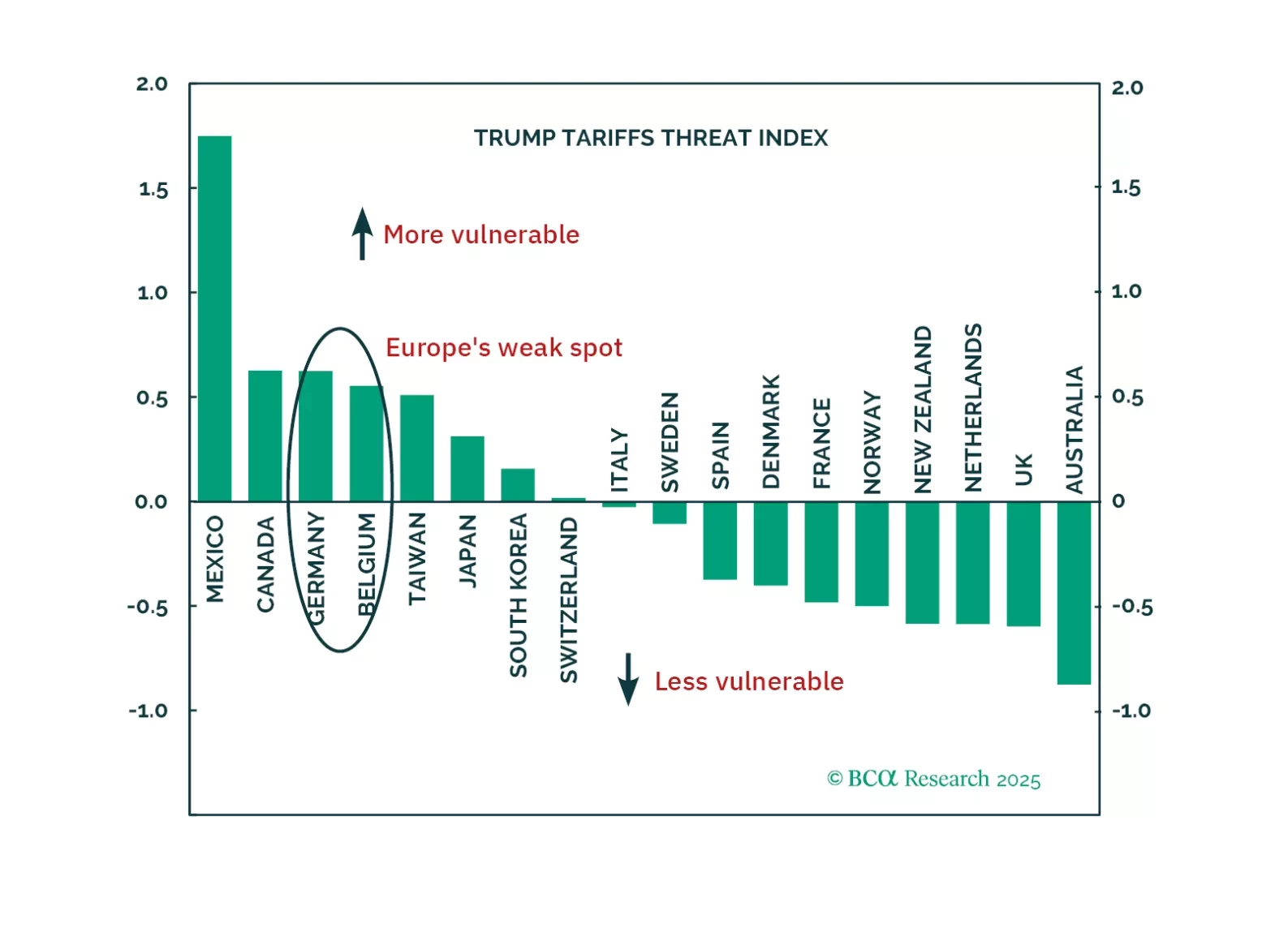

President Trump is about to be inaugurated. Investors often assume all his policies will hurt Europe, but the reality is more nuanced.

For our last publication of the year, we explore five key themes that will dominate the European macro landscape and markets next year. While the start of 2025 will be challenging for European assets, the latter part will offer some much-needed relief.