Commodities & Energy Sector

Investors should prepare for economic data to weaken even as policy uncertainty and geopolitical risk skyrocket ahead of the US election.

Central banks are in a dilemma whether to prioritize supporting growth or bringing inflation back to target. This is unlikely to end well. Investors should be defensively positioned.

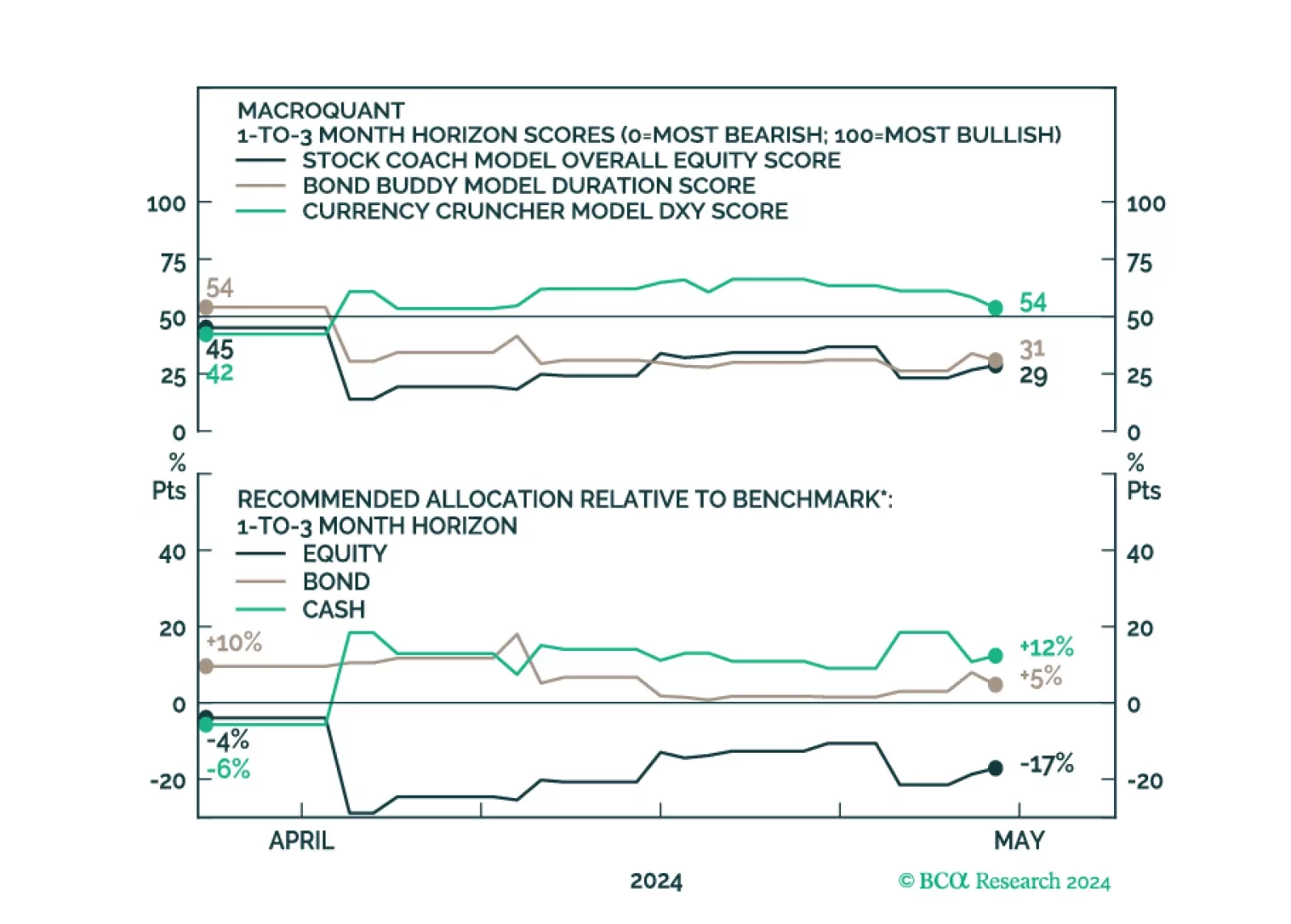

MacroQuant downgraded equities from neutral to underweight on a 1-to-3 month horizon. The model suggests increasing exposure to cash.

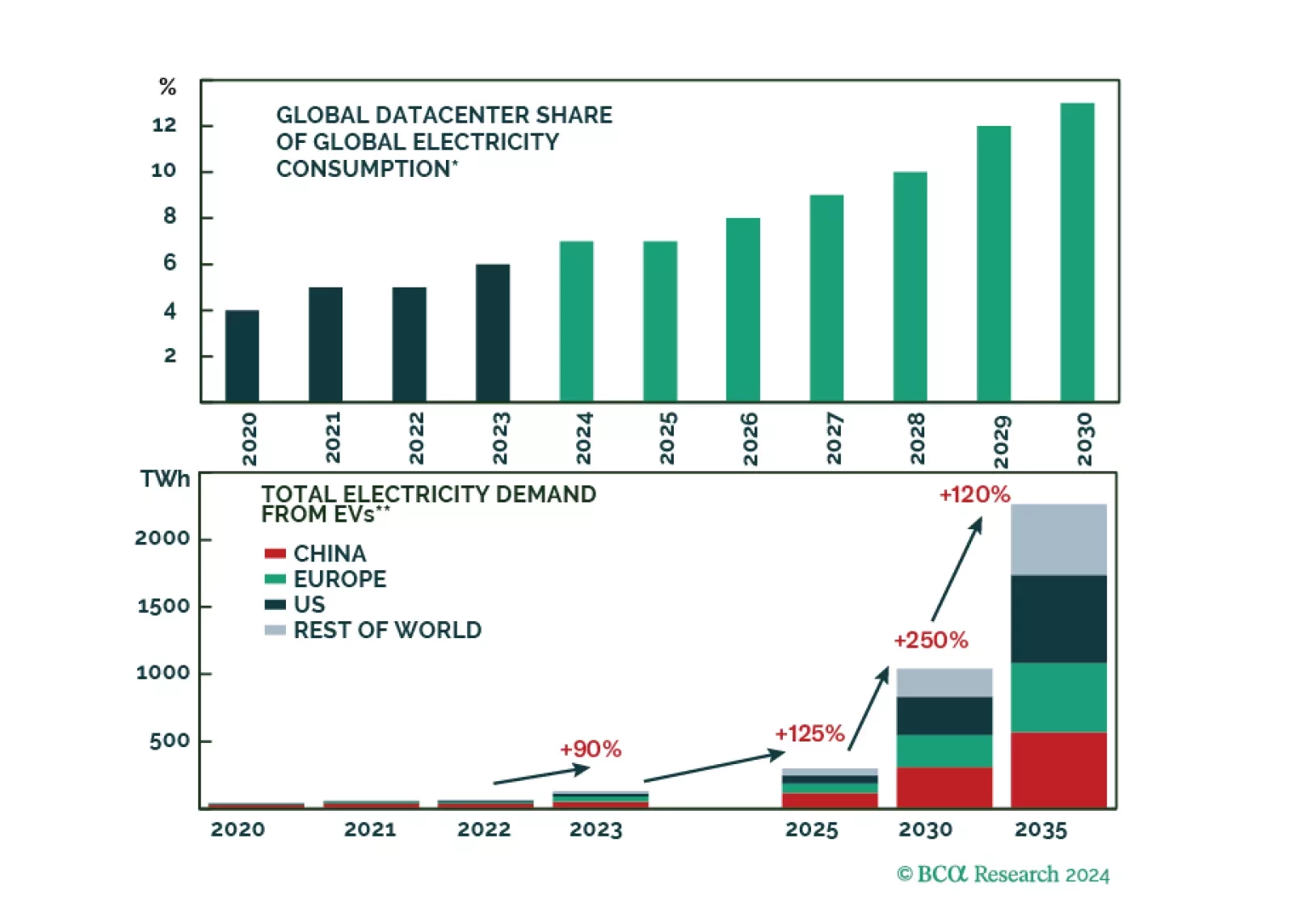

AI, EVs, and reshoring will lead to a massive surge in demand for electricity. Carbon-free, cheap, baseload nuclear energy stands to greatly benefit from these megatrends going forward.

The implication is that Israel chose not to escalate the risk of direct war with Iran. Hence we remain in our base-case “Minor War, Minor Oil Shock” scenario.

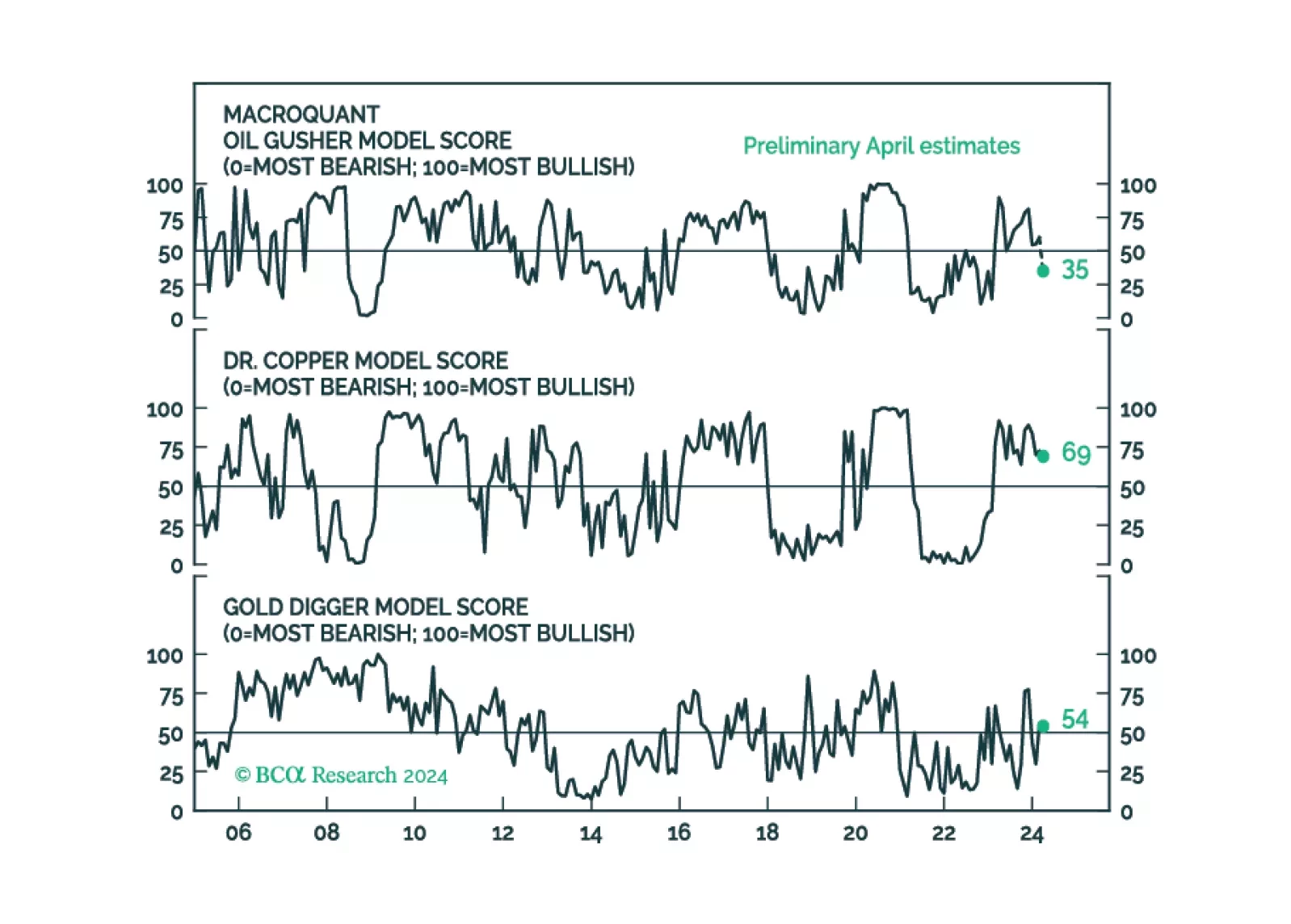

This year’s rise in commodity prices represents a blow-off rally rather than the start of a durable bull market. The global economy is heading for a recession. Stocks, commodities, and other risk assets are vulnerable.

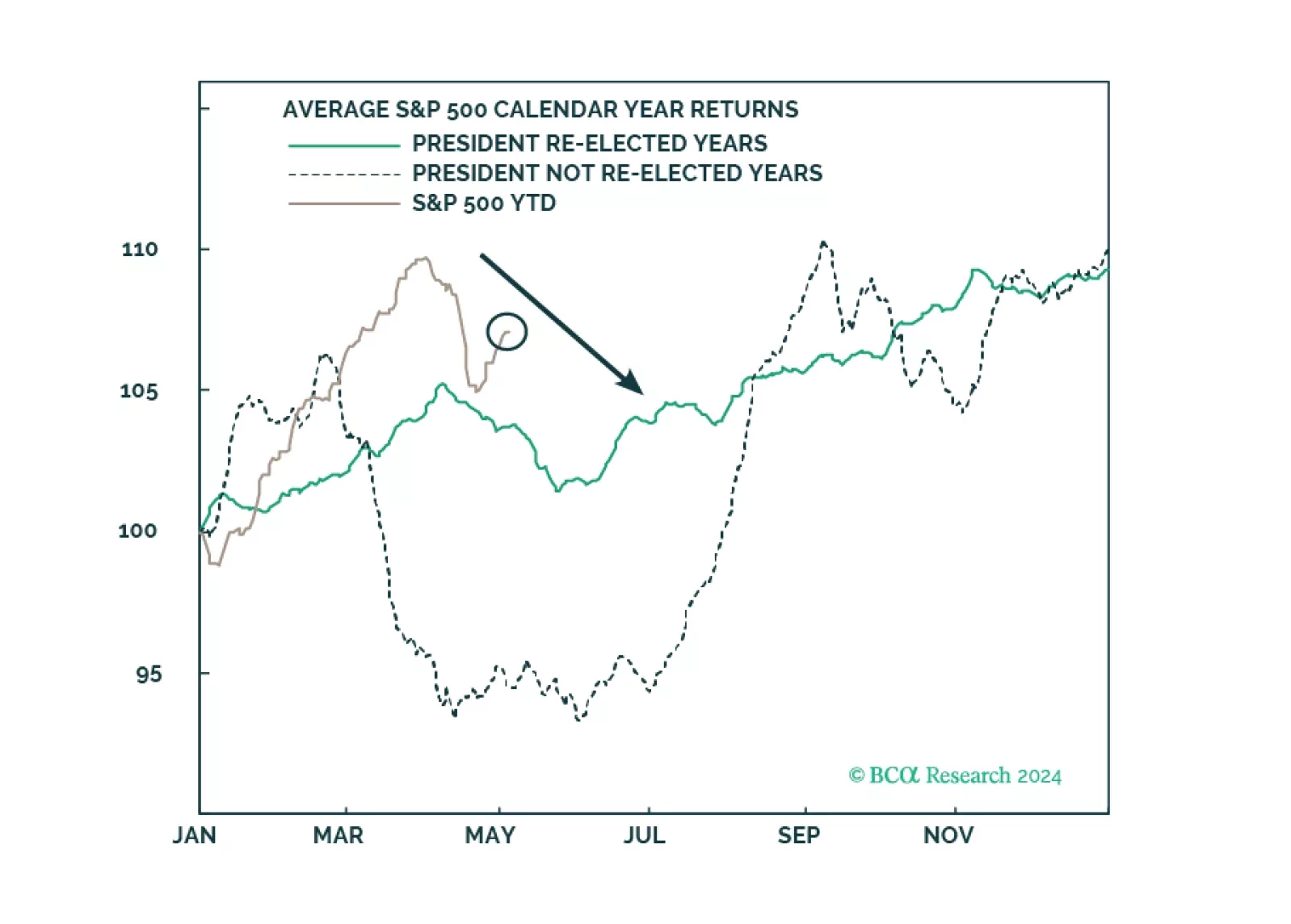

Our quant models suggest Democrats are still slightly favored for the White House. Our Senate model favors Republican control, though Montana and Ohio are the weak links that could deliver Democrats a de facto Senate majority in the event they keep the White House. But there are still six months before the vote. An oil shock from the Middle East or other negative economic news would force a major change to these models.