Consumer

The conventional 30-year mortgage rate eased further to 6.2% from above 7% back in the spring, spurring a 20.3% surge in refinancing activity last week. Mortgage applications rose 11.0%, marking a fifth consecutive week of increase and the Conference Board…

In a widely expected move, the Riksbank lowered its policy rate from 3.5% to 3.25% in September, marking its third cut this year. It embarked on its easing cycle in May, leading many other DM central banks, and has been sending increasingly dovish messages…

The Conference Board Consumer Confidence index unexpectedly shed 6.9 points to 98.7 in September. Both the Present Situation and Expectations components declined, by 10.3 and 4.6 points respectively. The decline in morale in September was broad-based across…

In a widely expected move, the Reserve Bank of Australia kept the cash rate unchanged at 4.35% in September. All measures of Australian CPI inflation remain well above the RBA target range. The Commonwealth Energy Bill Relief Fund and other…

Canadian retail sales grew by a higher-than-expected 0.9% m/m in July from a 0.2% contraction in June. A 2.2% monthly rise in vehicle sales led an otherwise broad-based increase. Ex-auto retail sales also surprised positively, growing by 0.4%. A measure…

The Norges Bank kept its policy rate unchanged at 4.5% at its September meeting and signaled low odds of policy easing before the first quarter of 2025. The inflation backdrop does not warrant easing policy. Although core CPI cooled to 3.2% y/y in August,…

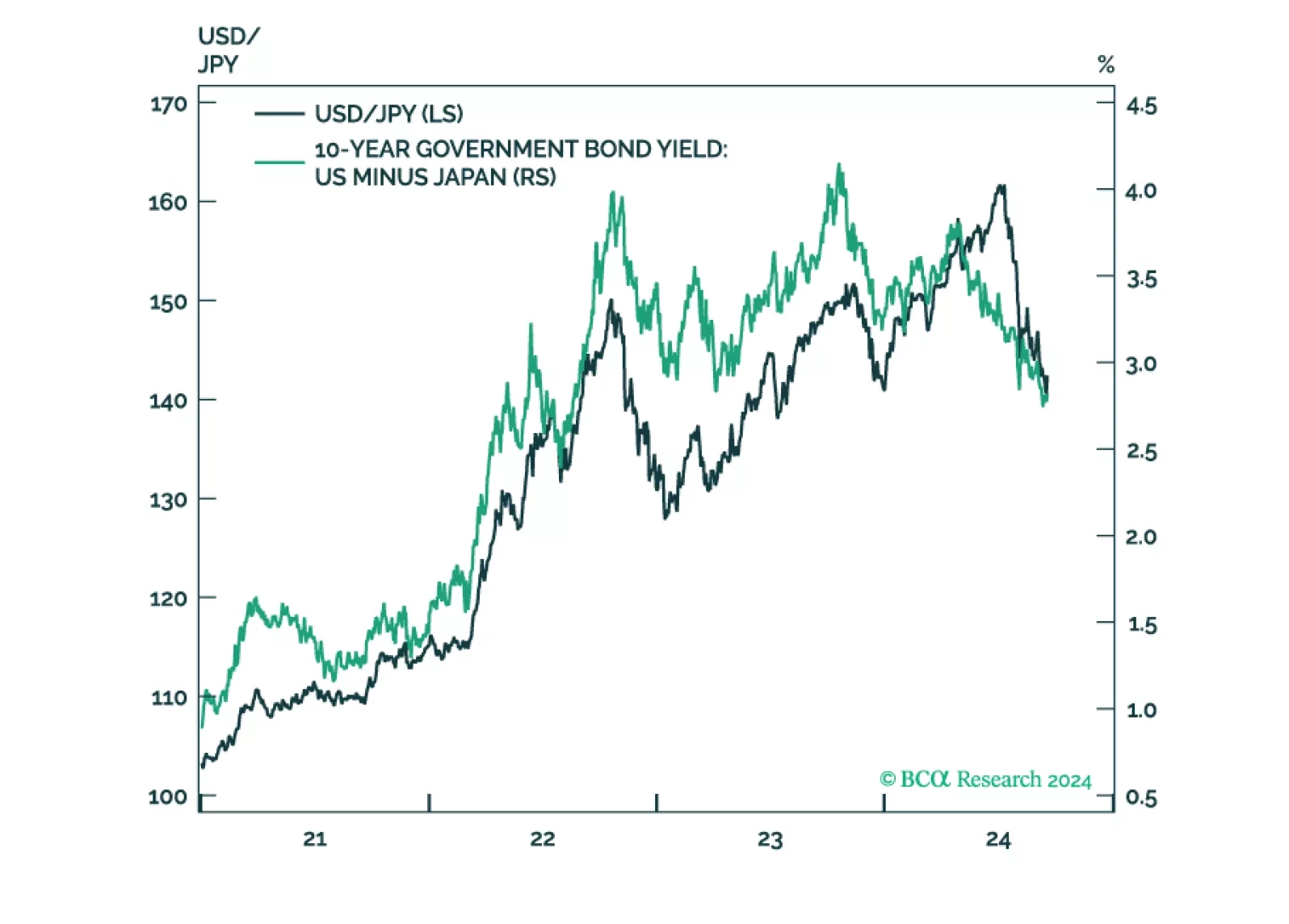

In this report, we argue that the Bank of Japan is unlikely to hike interest rates this week, but the relative trajectory of bond yields in Japan is higher. This warrants an underweight position in JGBs and a leveraged bet on a higher yen. The positioning for equity investors is murkier, as progress on corporate reforms is necessary for a rerating in Japanese shares. That is not yet very clear. The bottom line is: Stay long the yen.

Stress among lower-income households is often cited as an early indication of deteriorating aggregate consumer fundamentals. The data indeed suggests that this cohort’s cash holdings are depleting. However, the Fed’s quarterly estimates of household wealth…

US retail sales grew 0.1% m/m in August and beat expectations of a 0.2% monthly contraction. The positive surprise seemingly spurred equity market gains on Tuesday morning. However, details do not paint as rosy a picture as the headline number…