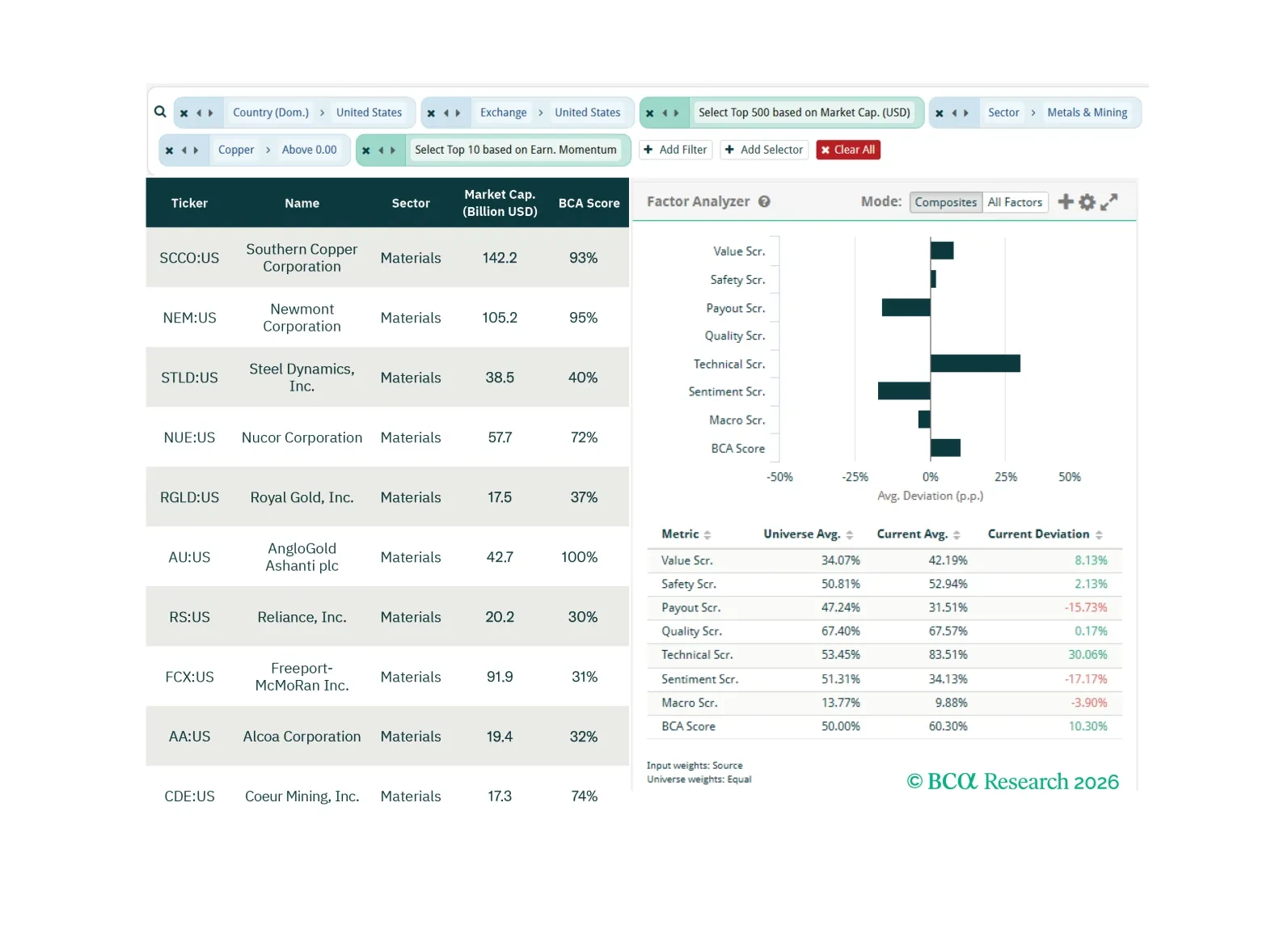

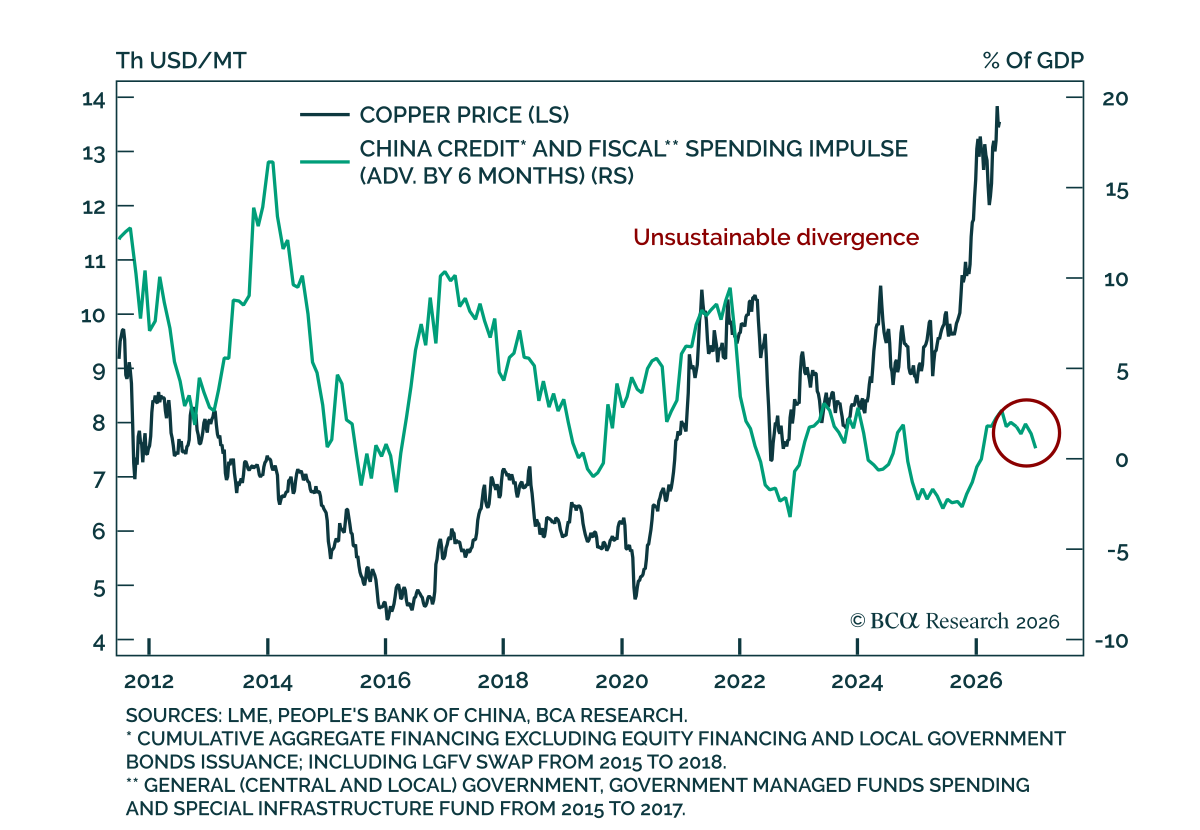

Copper

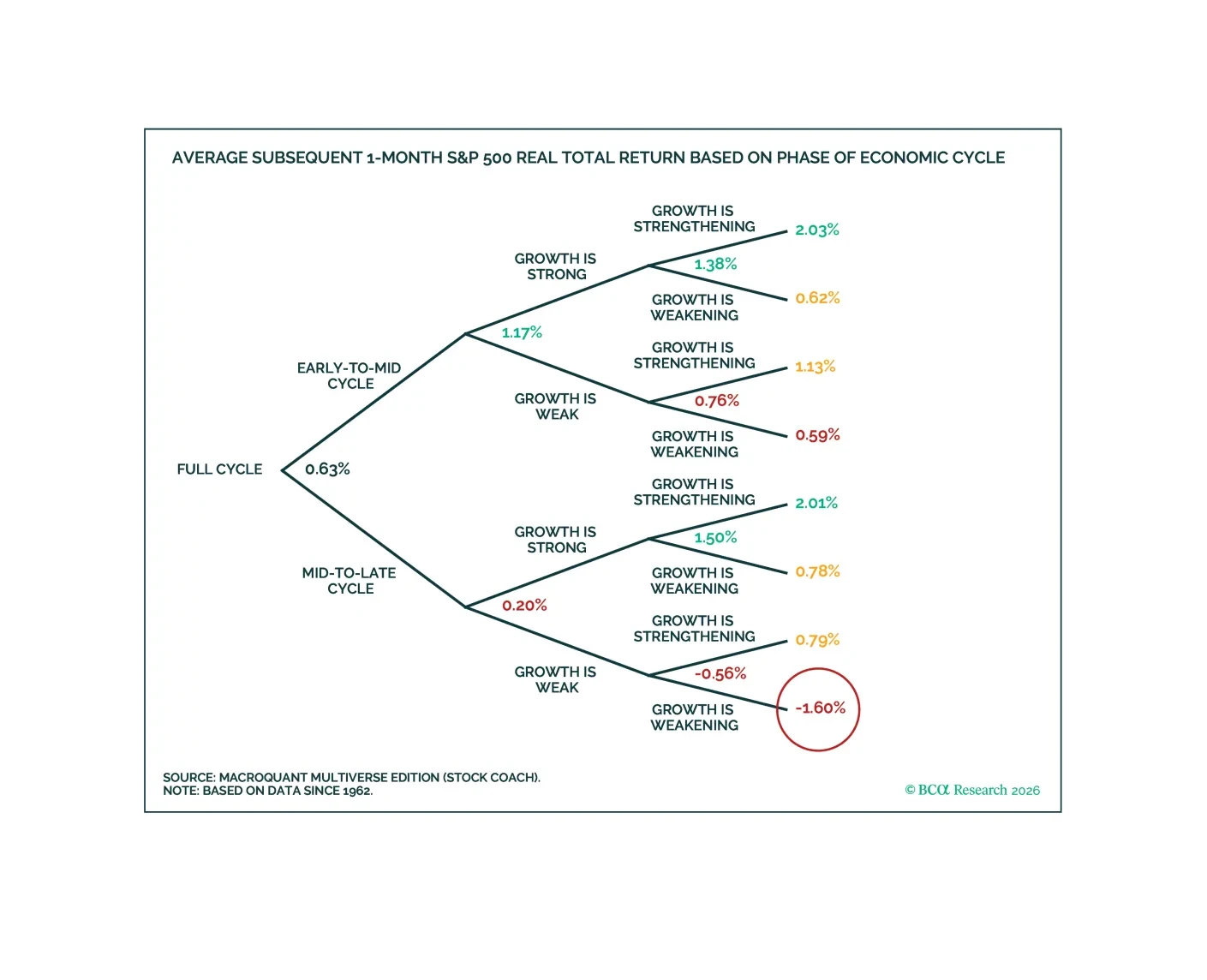

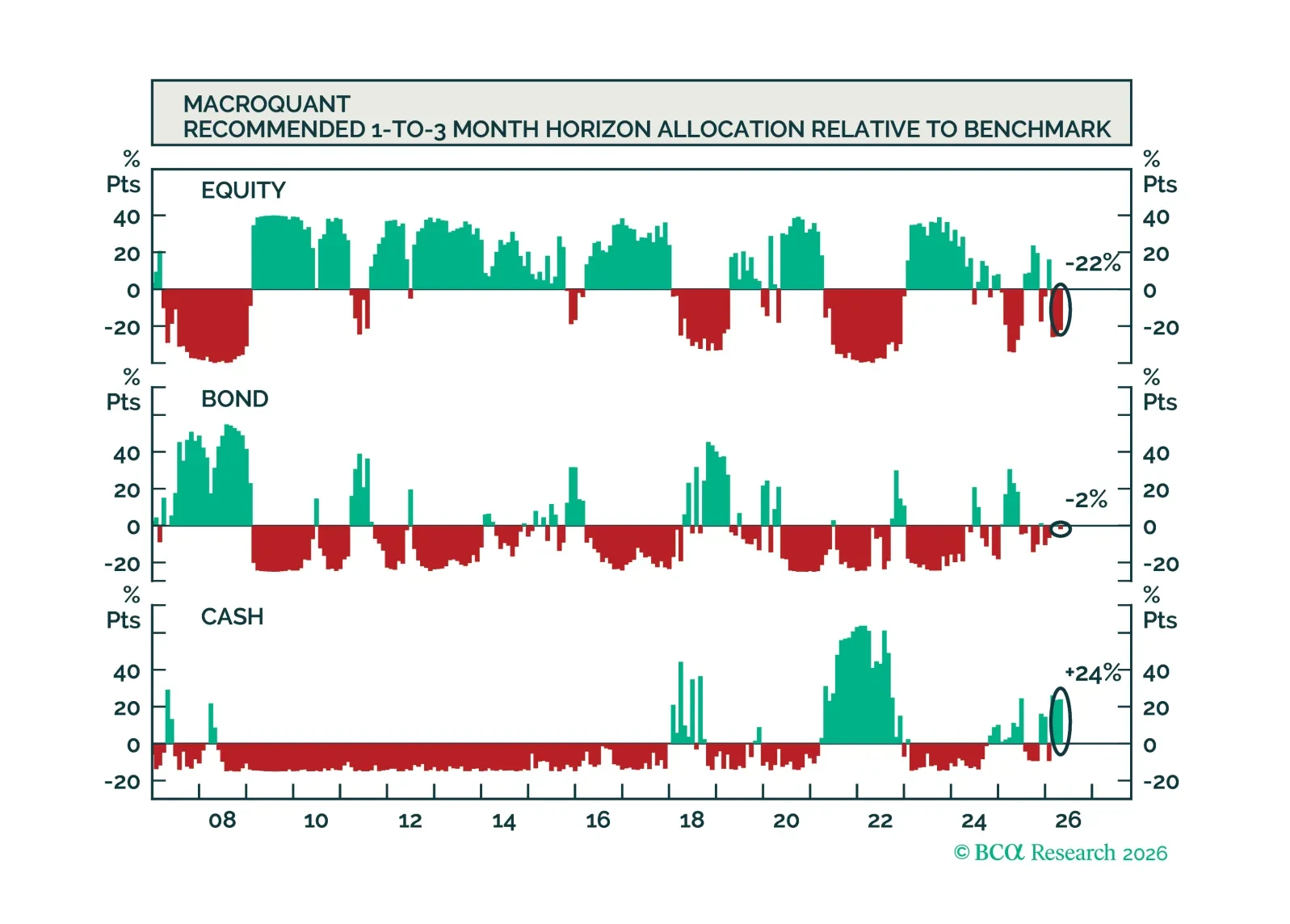

MacroQuant recommends underweighting equities and adopting a benchmark duration stance in fixed-income portfolios. The model is very positive on the US dollar, bearish on gold, neutral on copper, and bullish on oil.

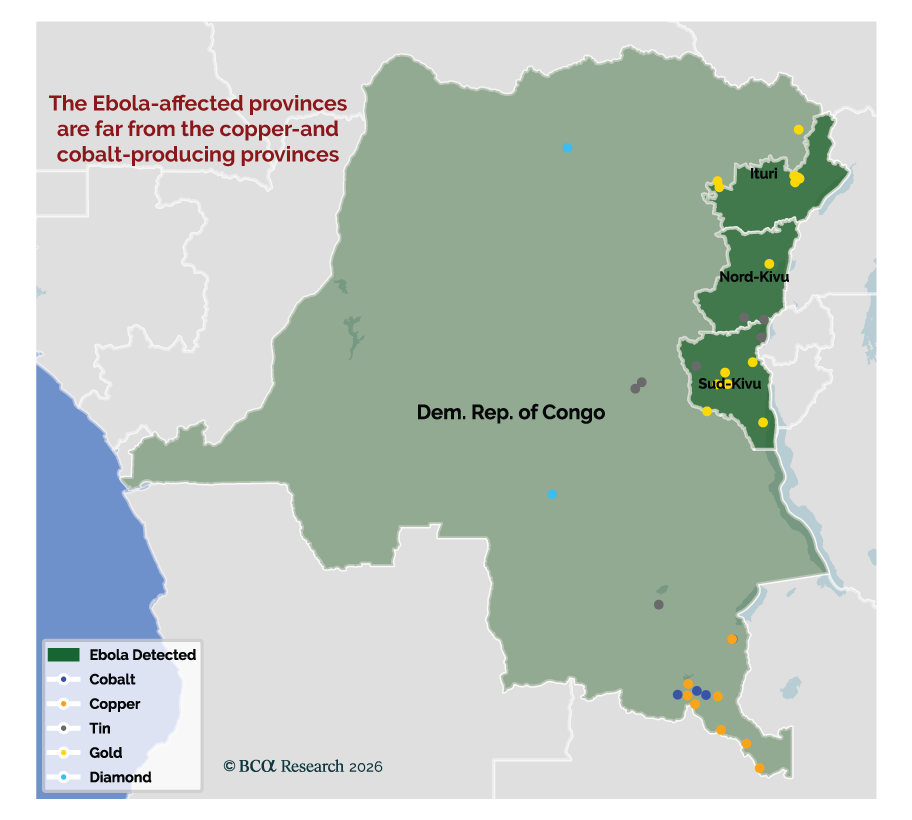

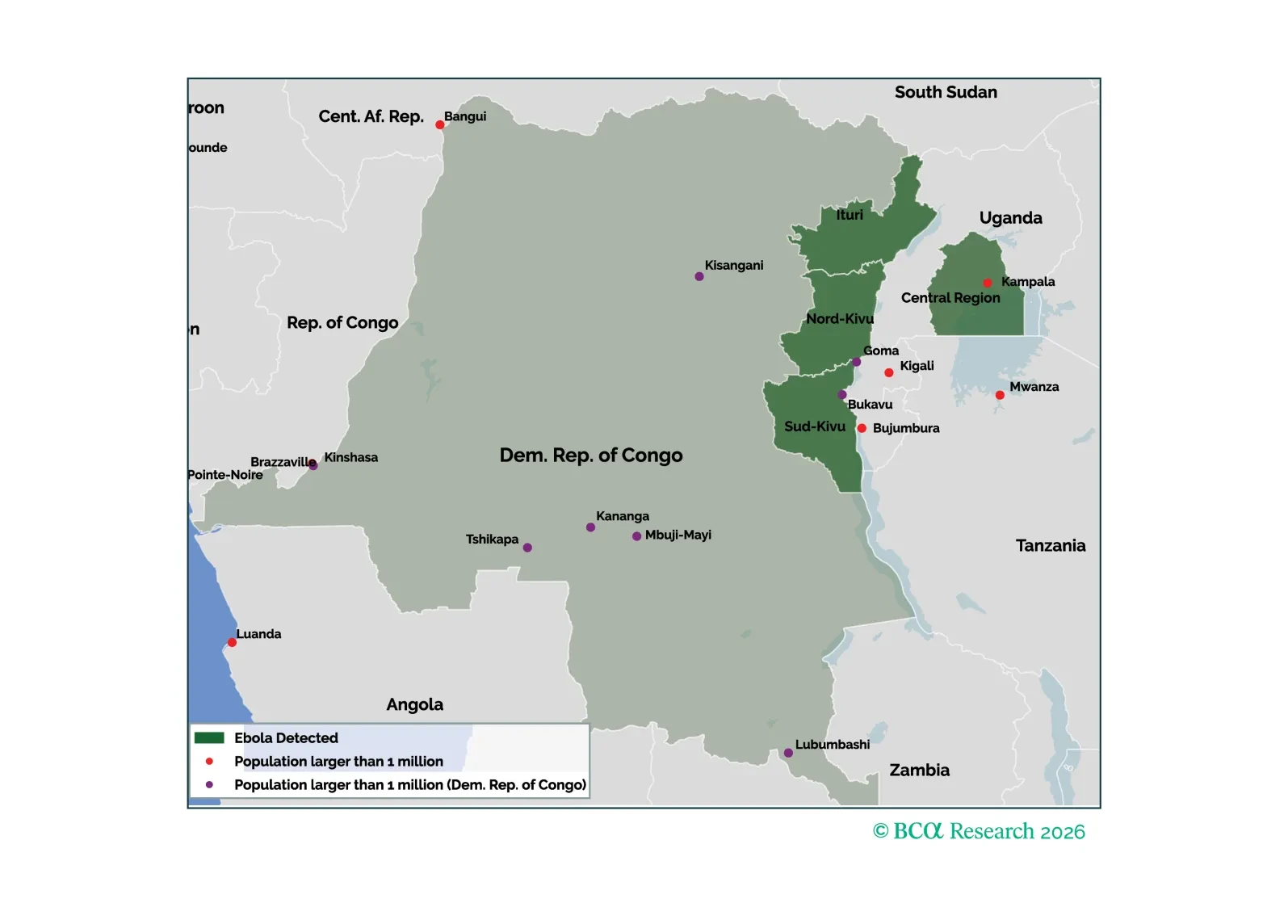

Ebola remains one of the world's deadliest viral diseases, but it is far less transmissible than COVID-19 or influenza. The most likely outcome remains containment rather than a global pandemic.

In this screener report, we explore opportunities in: US copper beneficiaries; Australian Materials, Energy, and Industrial stocks; and US reinvestment-led Tech stocks.

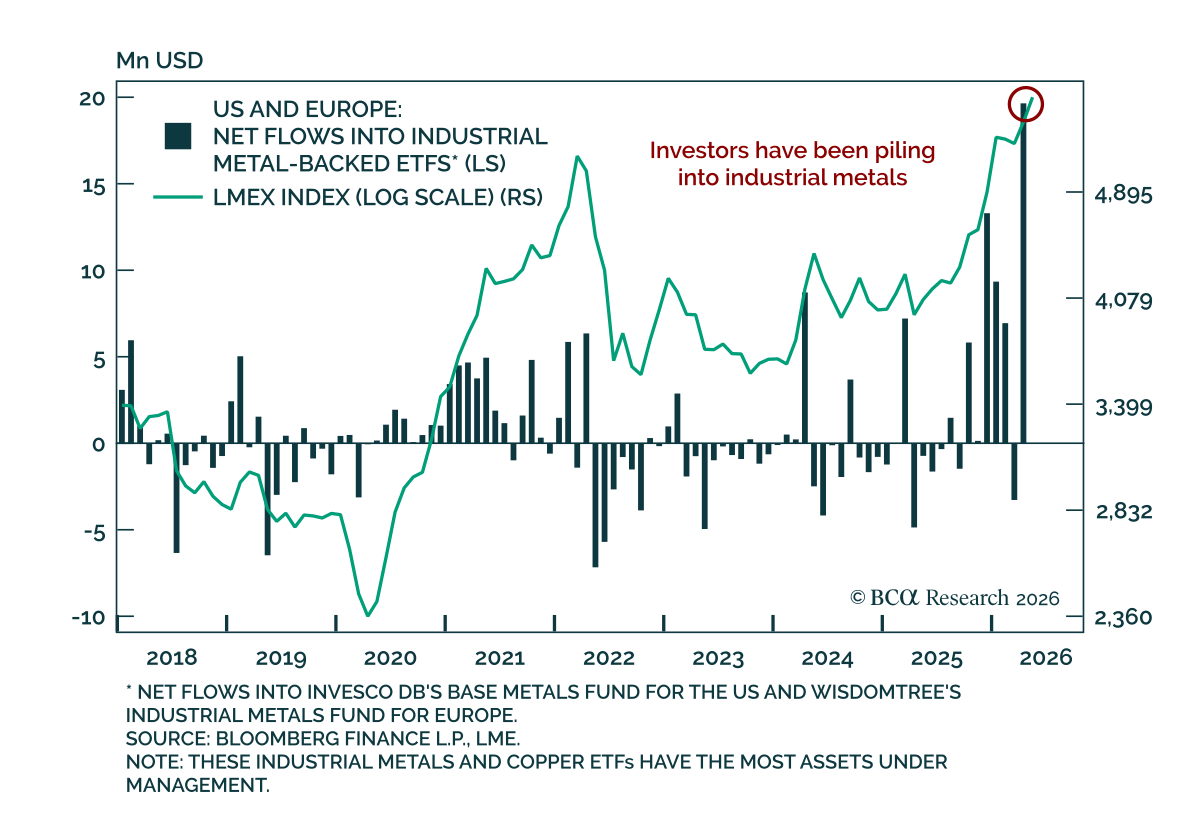

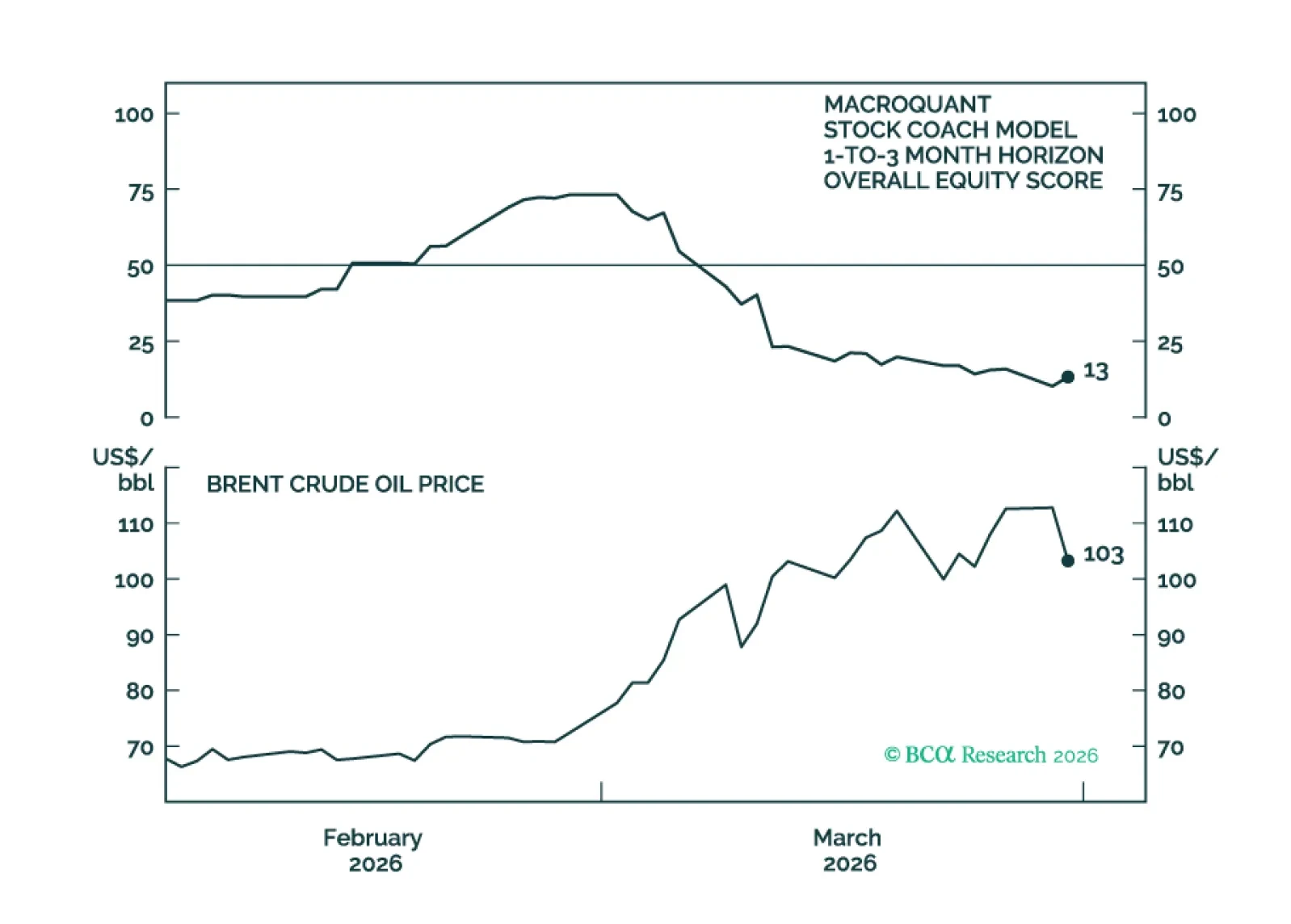

Copper prices are surging again after a brief pullback in the first quarter.

What is driving the renewed strength, and can it persist?

MacroQuant recommends a slight underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is very positive on the US dollar, downgrades gold to underweight, upgrades copper to overweight, and remains very bullish on oil.

MacroQuant recommends an underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is neutral-to-slightly positive on the US dollar, remains neutral on gold, upgrades copper to neutral, and is very bullish on oil.

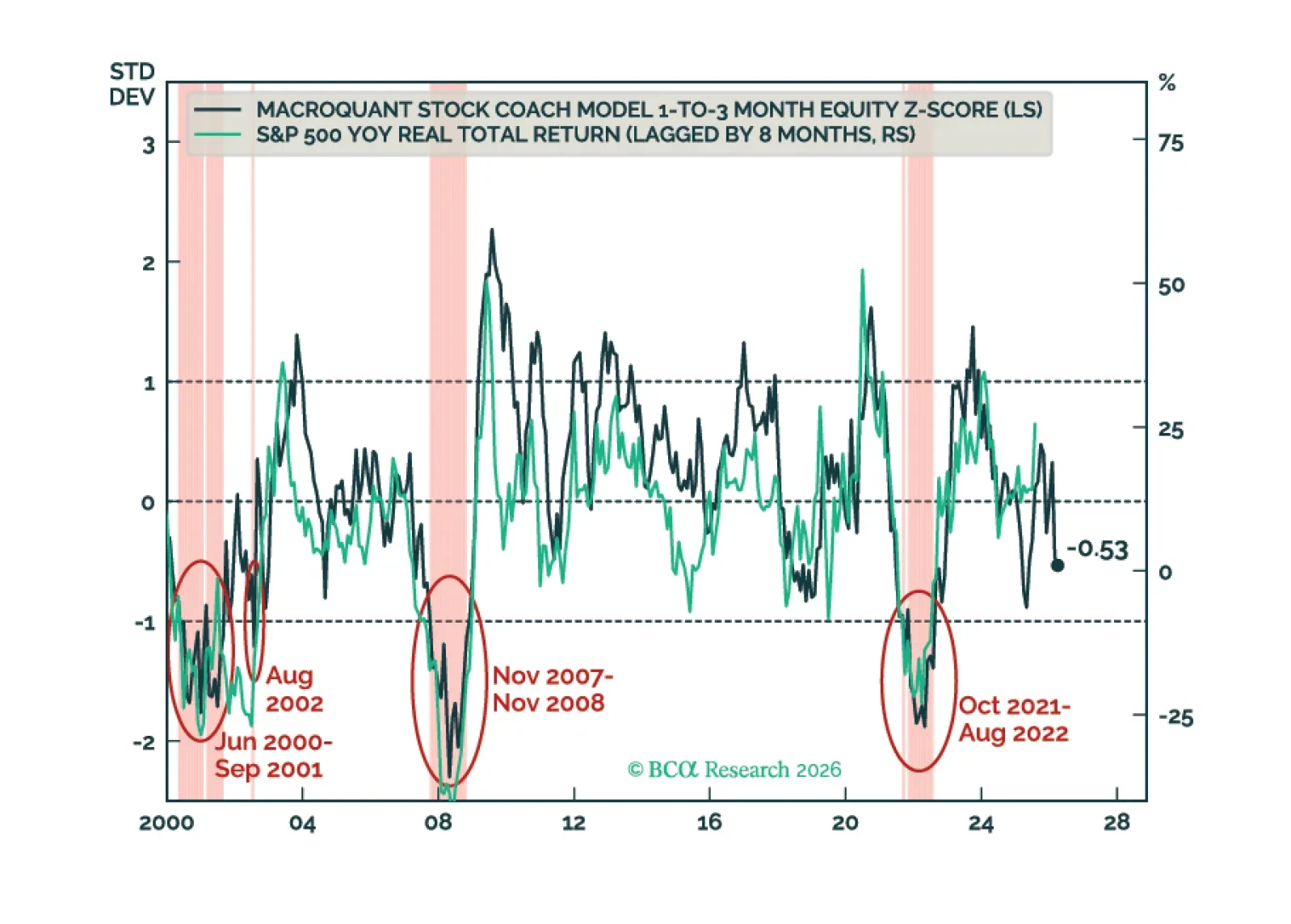

MacroQuant recommends a strong underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, has become neutral-to-slightly positive on the US dollar, has downgraded gold to neutral and copper to a strong underweight, and is bullish on oil.