Copper

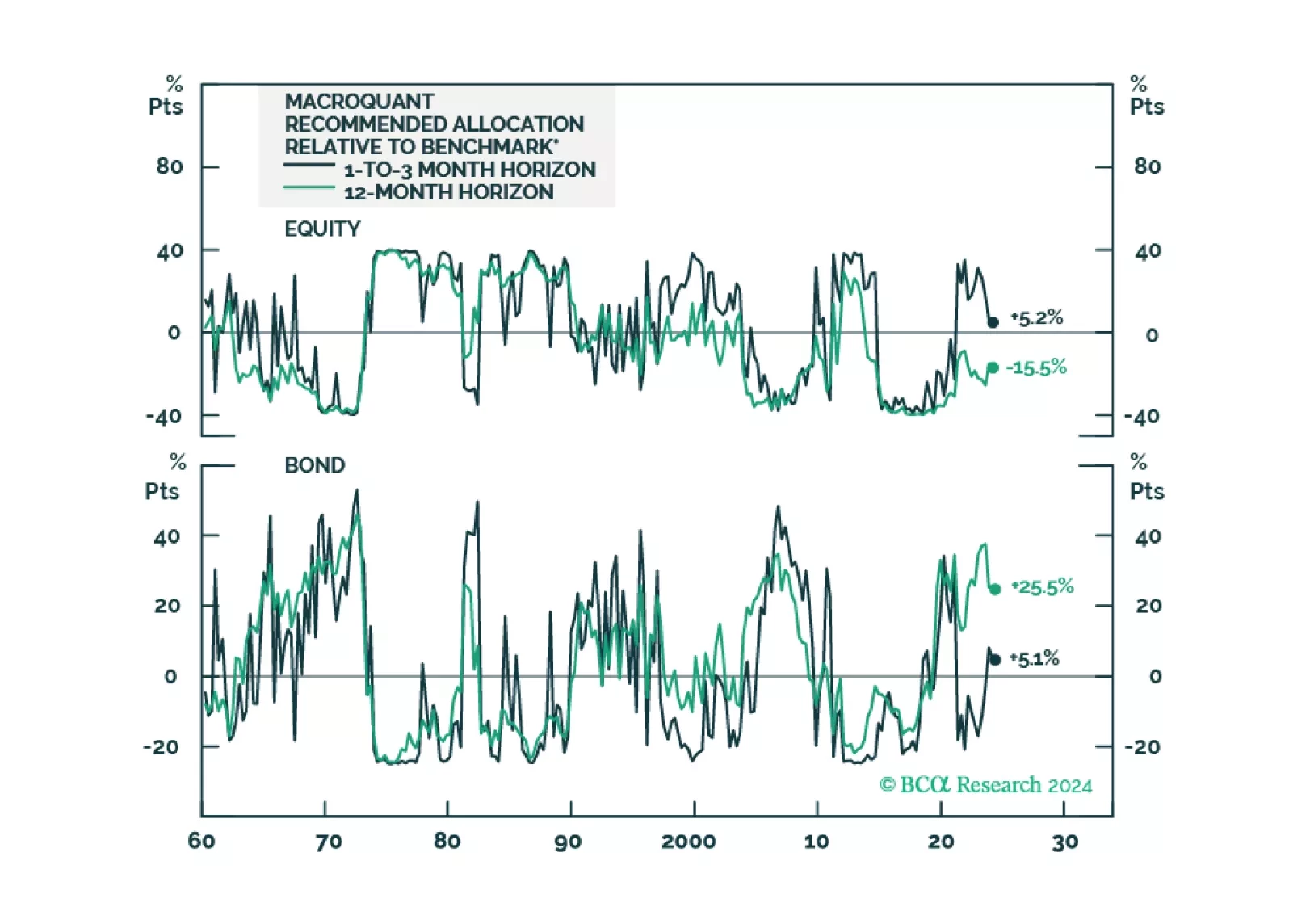

Following the release of the white paper yesterday, today we are sending you the inaugural issue of the MacroQuant Monthly, a report summarizing the output of our next-generation MacroQuant 2.0 model.

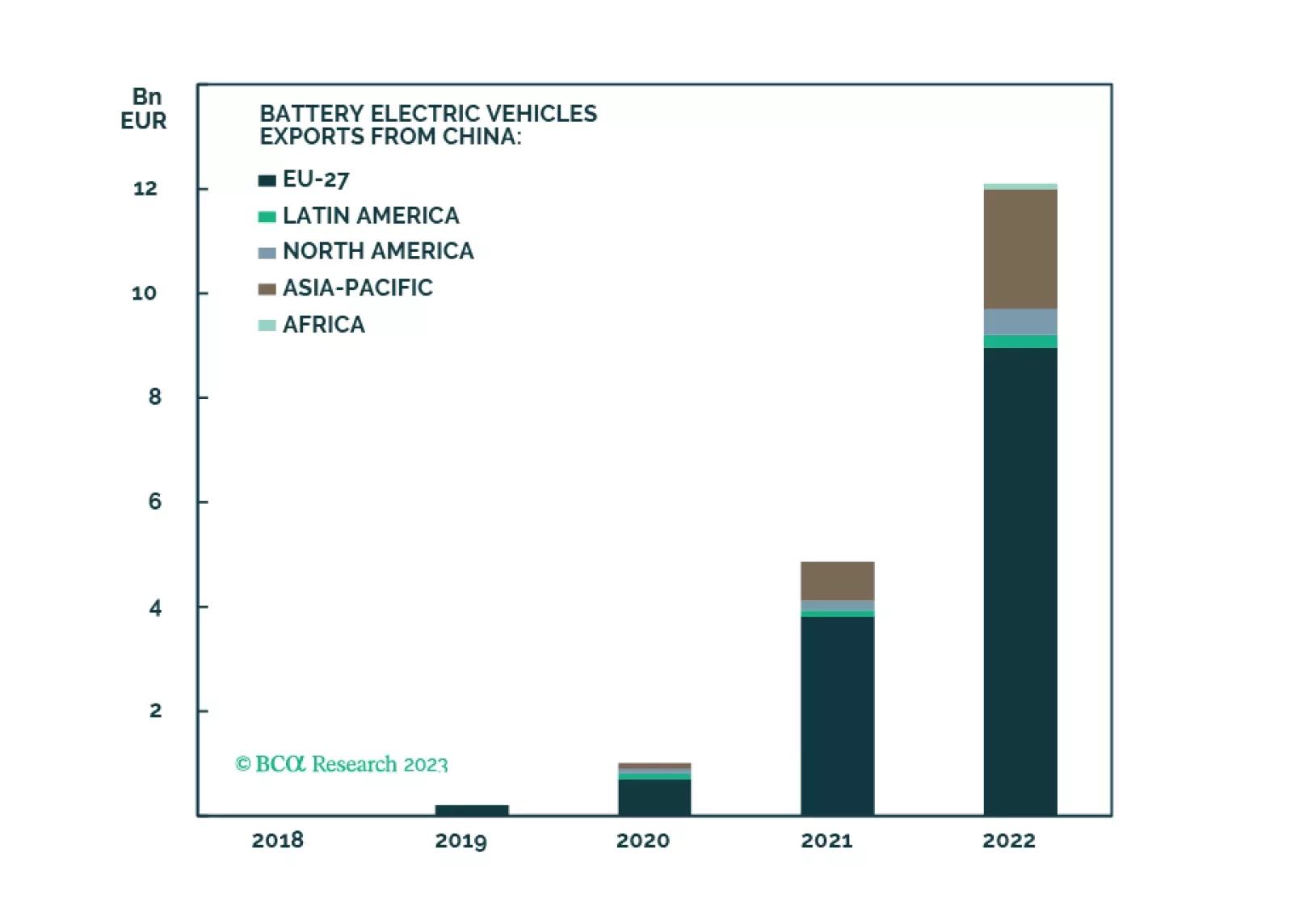

China’s push to dramatically expand its copper-refining capacity will be complemented by further vertical integration of mining assets. However, surplus refining capacity will push treatment and refining charges lower in the short run. The threat of EU tariffs on Chinese EV imports looms large, and could be costly to China’s expansion of its already-dominant supply-chain ecosystem for EVs and metals refining. We remain long the XME and COMT ETFs to retain exposure to metals miners and refiners.

The global energy transition will become more disorderly, if oil-and-gas capex growth continues to outpace that of critical minerals. We remain long exposure to the equities of oil and gas producers via the XOP ETF; the COMT ETF to retain direct commodity exposure, and $100/bbl December 2024 Brent calls. Slower supply growth of metals facing off against steadily increasing demand also favors exposure to metals miners and refiners via the XME ETF.

Contrary to the widespread belief in the investment community, the global copper supply-demand balance is no longer in deficit. Red metal prices are set to decline by another 10-15% as the global copper market will shift to a larger surplus in the next six months.