Corporate

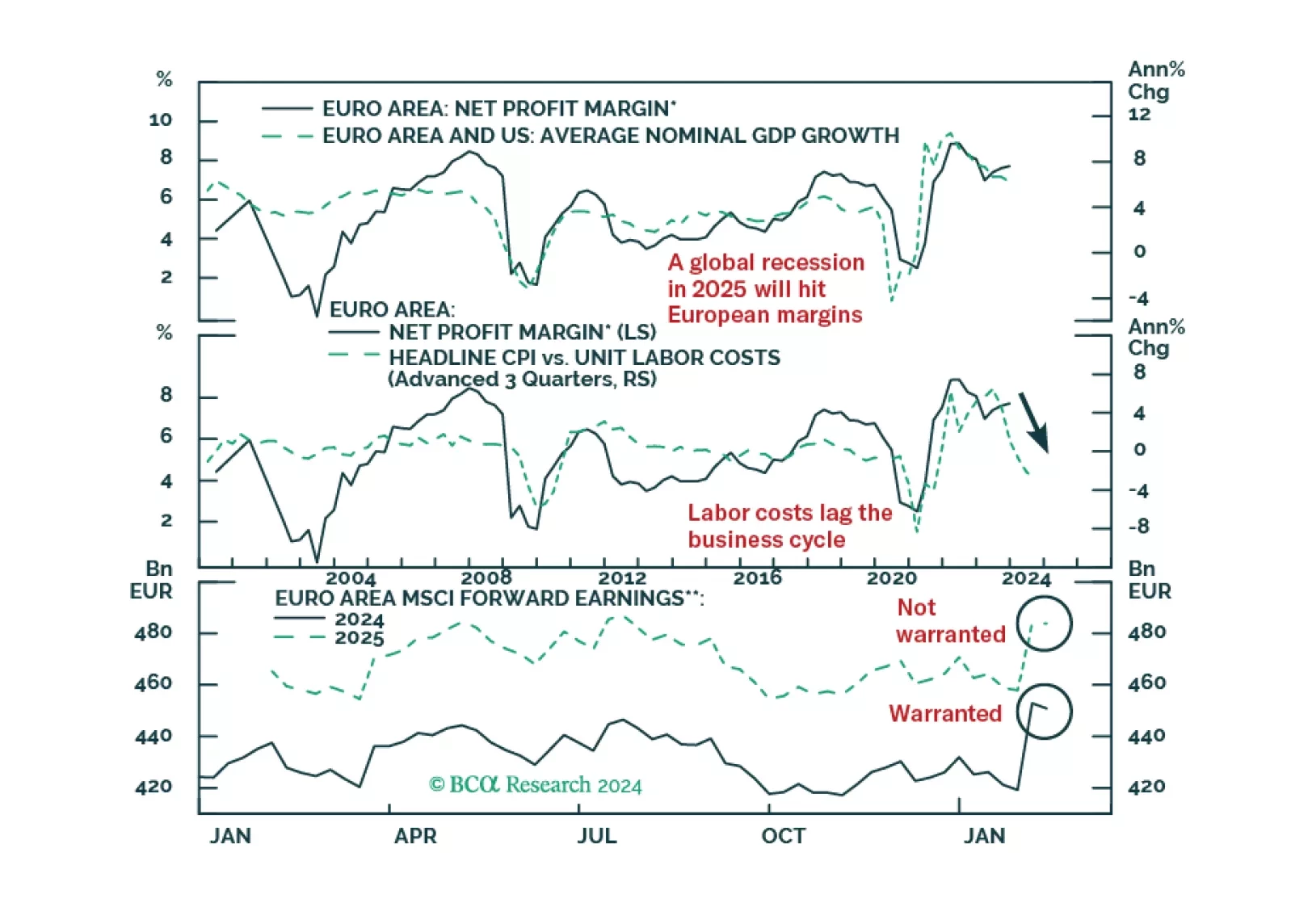

According to BCA Research's European Investment Strategy service, European profit margins have downside because they are both elevated and procyclical. European net margins stand at 7.7% above their long-term average of 5%. Analyst expectations…

European profits margins are elevated. Will a mild recession be enough to bring them down?

Nvidia has amassed staggering sales from AI. Last year its data center revenues exploded, going from just over $4 billion in 2023 Q1, to over $18 billion in 2023 Q4. That said, its competitors have not done as well. In the same time frame that Nvidia added…

BCA Research’s US Equity Strategy service provides its take on US Q1-24 earnings expectations. Room for surprise? Positive earnings surprises have been a fixture of nearly every earnings season since the darkest days of the pandemic. This quarter will…

Global material stocks have underperformed over the past 12 months, returning only 11.3% vs 21.4% for the overall market. But could they be a buy now? There are several arguments to argue that they will: The ISM has begun to stabilize and seems to be…

Some of the biggest US banks will kick off the reporting season in earnest this Friday, leading increased market focus on Q1 2024 earnings. According to Factset, analysts expect S&P 500 year-over-year earnings growth to expand for the third straight…

The US economy expanded at a faster pace than previously believed in 2023Q4. GDP grew at an annualized 3.4% q/q rate, thus annulling the second estimate’s downward revision. Notably, consumption growth was revised even higher to 3.3% q/q, from 3.0% q/q and…

Chinese industrial profit growth surged to 10.2% y/y in the first two months of the year after having contracted by 2.3% in 2023. Does this rebound in profits suggest that investors should become more optimistic about the Chinese economy and risk assets? A…

According to BCA Research’s Counterpoint service, ‘bad unemployment’ is on the rise in the US, despite resilient growth. There are two ways that you can become unemployed. Either by losing your job. Or by entering the labour force to look for a job. The…

According to Factset, analysts are forecasting S&P 500 earnings and revenues to grow by 11.0% y/y and 5.0% y/y respectively in 2024 (an acceleration from 0.9% and 2.8% in 2023). Information technology and communications services (broadly-defined tech) are…