Country In-Focus

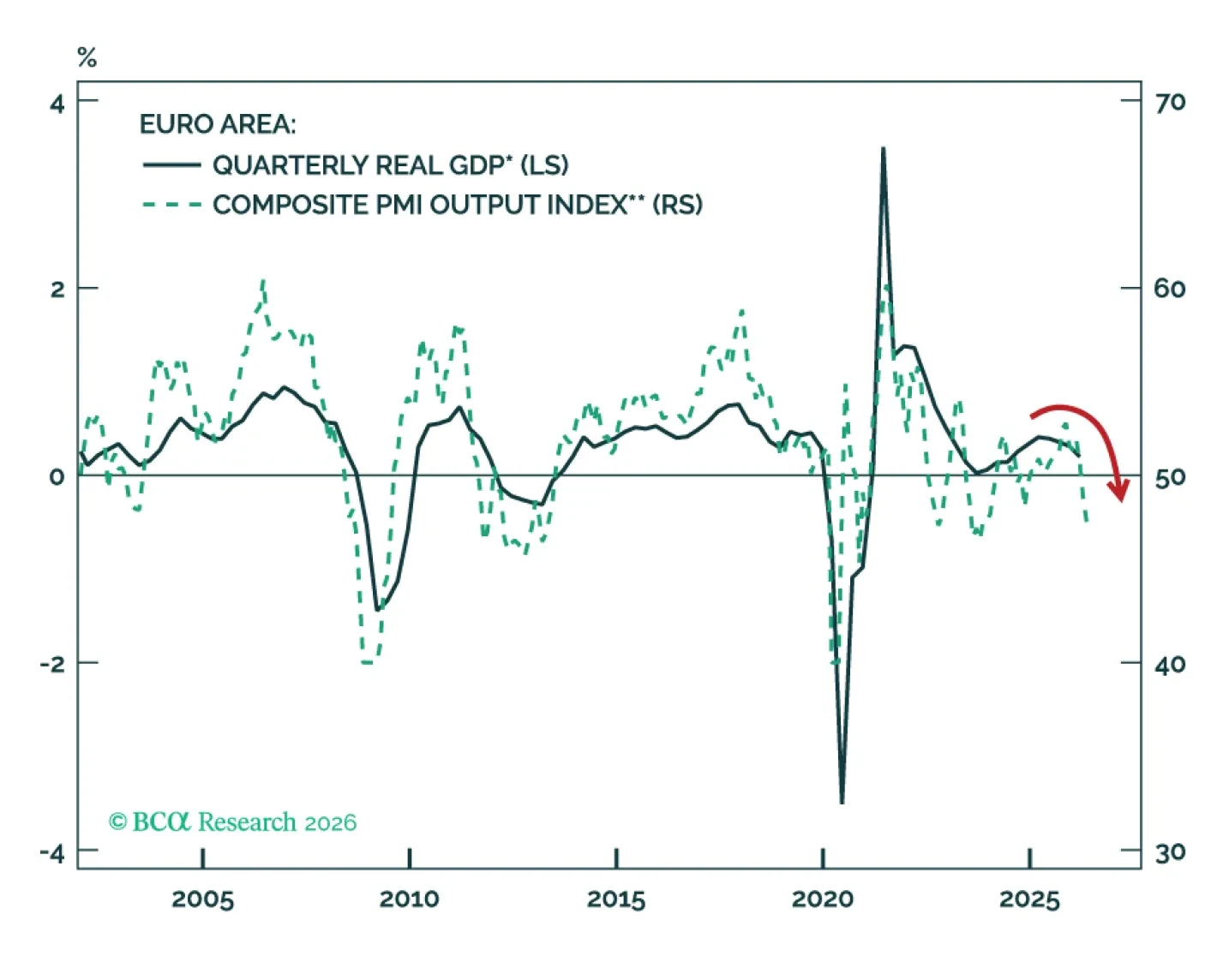

Europe is sliding from stagflation toward recession as prolonged disruptions in the Strait of Hormuz weaken growth, labor markets, and supply chains while keeping inflation elevated. Even if a US-Iran deal is reached, limited fiscal support and rising food inflation leave the Euro Area increasingly vulnerable to a deeper economic downturn.

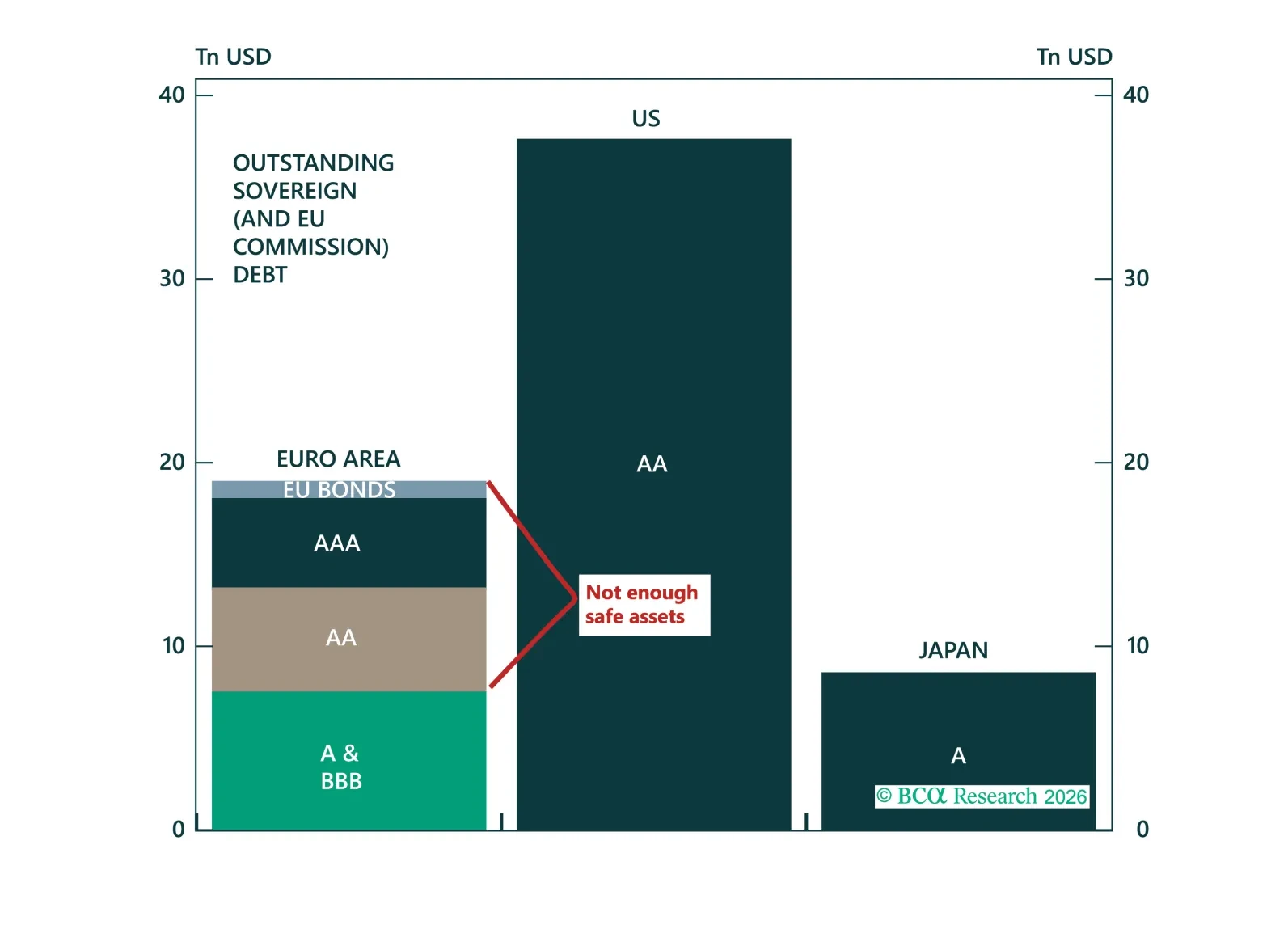

The dollar's retreat is creating the most compelling window for euro internationalisation since Maastricht, but Europe is missing the one instrument that would make it real. In this report, we make the case for the Eurobond, assess which model is most likely to prevail, and explain why the trade is long euro on dips and overweight Central and Eastern European sovereign spreads.

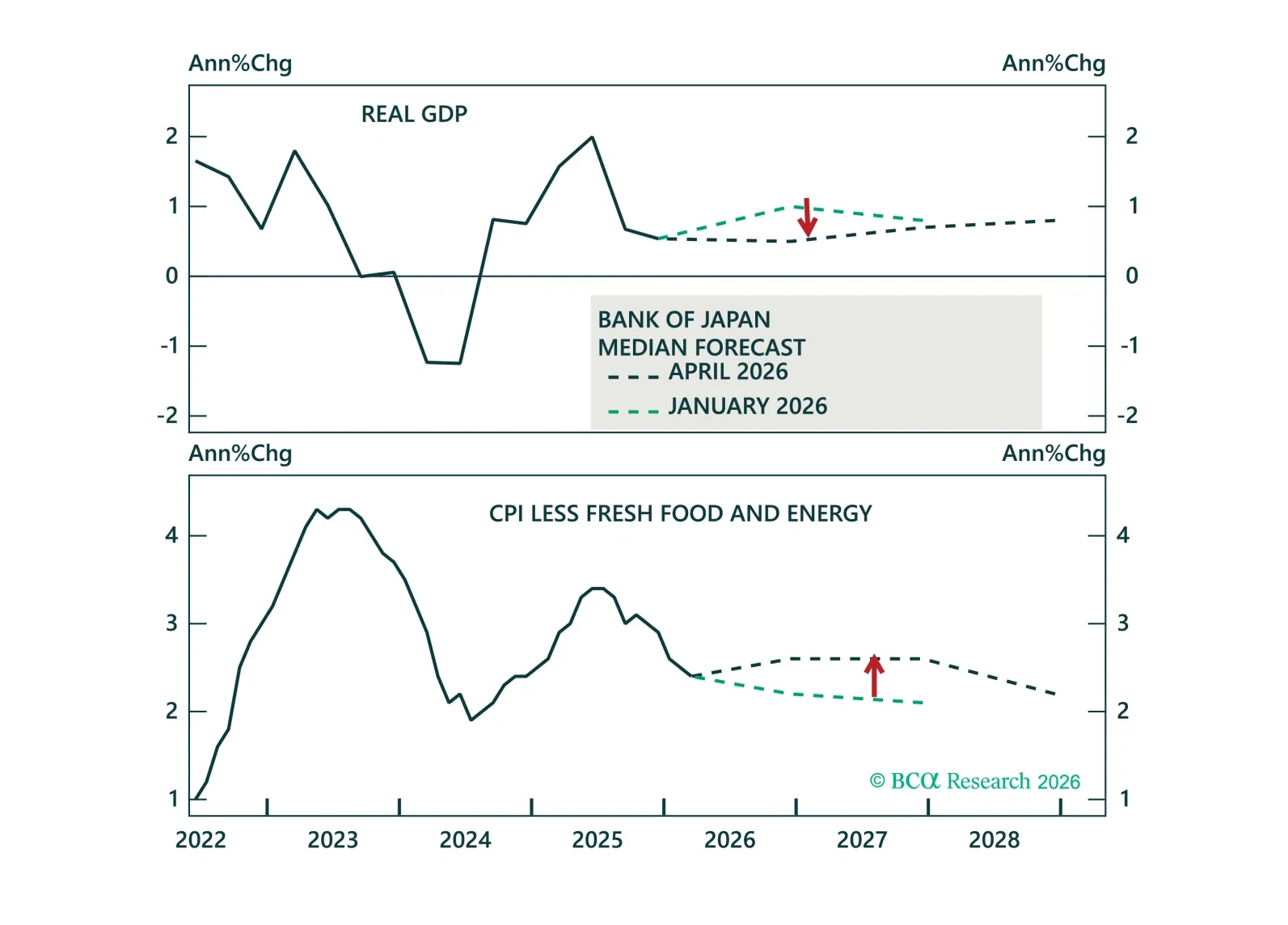

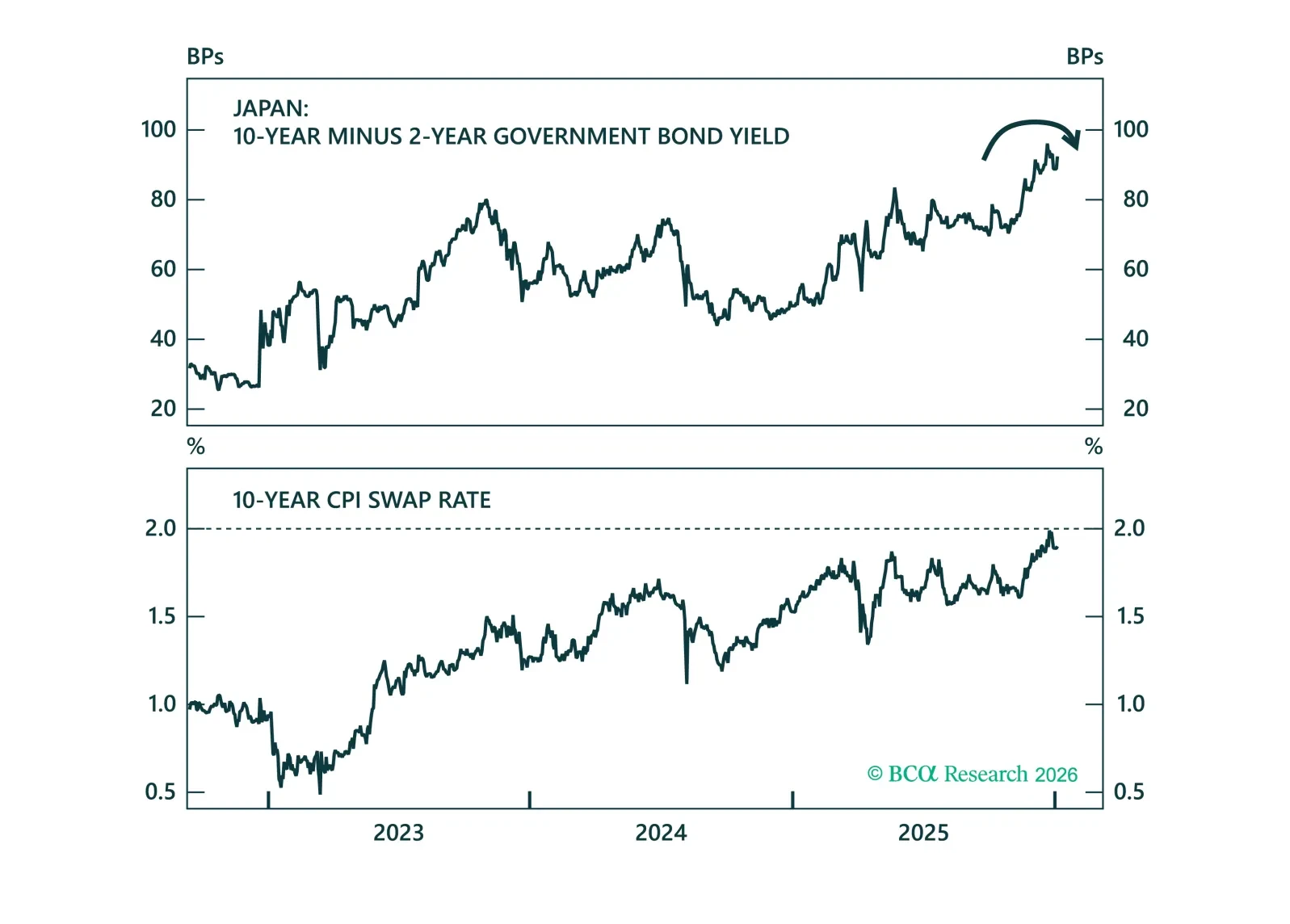

The BoJ held rates overnight, but the direction of travel hasn’t changed. We discuss how stronger wages, rising inflation, and a weak yen point to further tightening ahead.

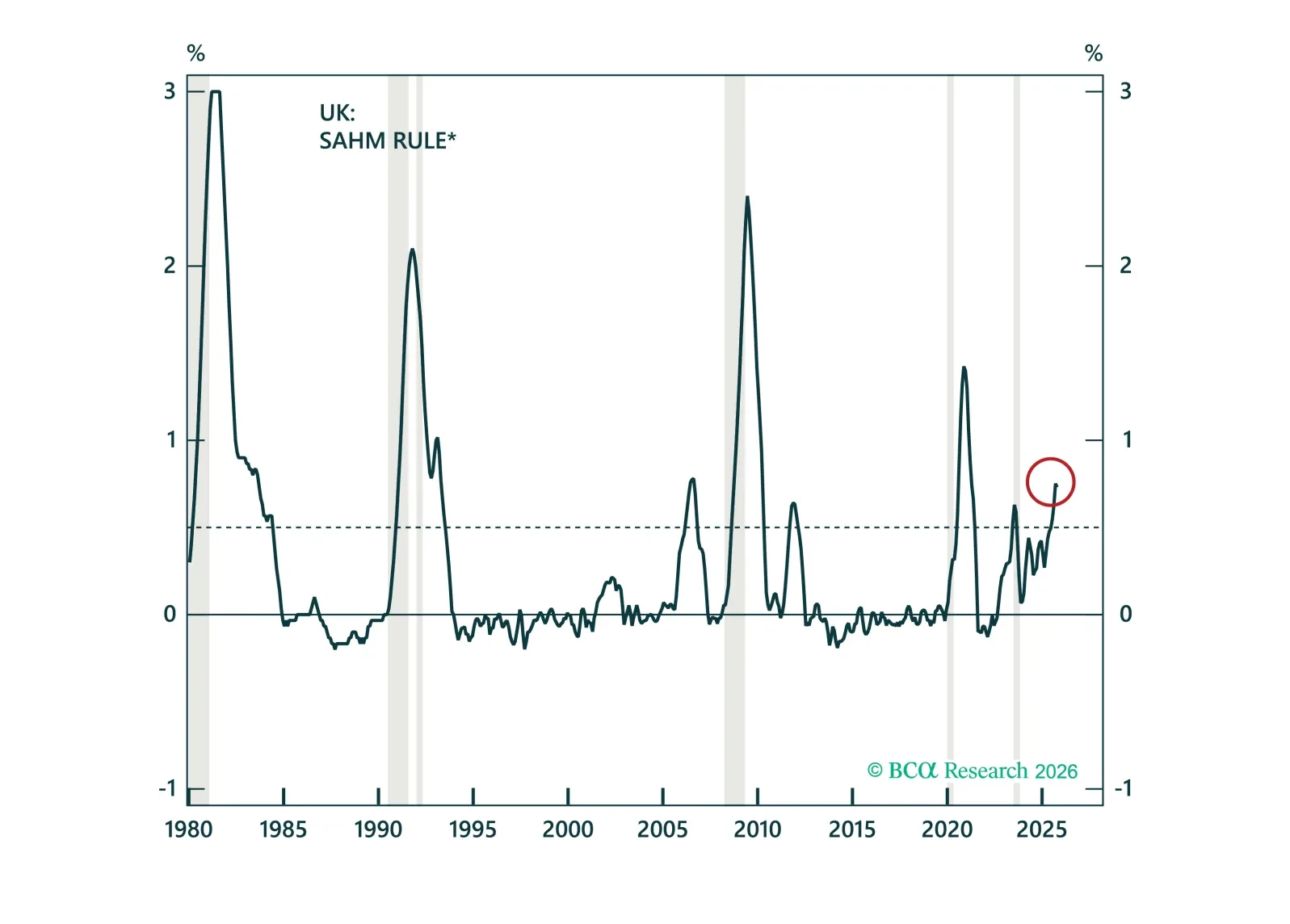

Recession risks in the UK are clearly rising. In this Special Report, we unpack why labor market deterioration, falling wage growth, and normalizing inflation support deeper BoE cuts ahead. We then discuss how to position across gilts, the pound, and UK equities.

From steepening to flattening. As the BoJ continues to tighten in 2026, we show why curve flatteners are finally the right trade.

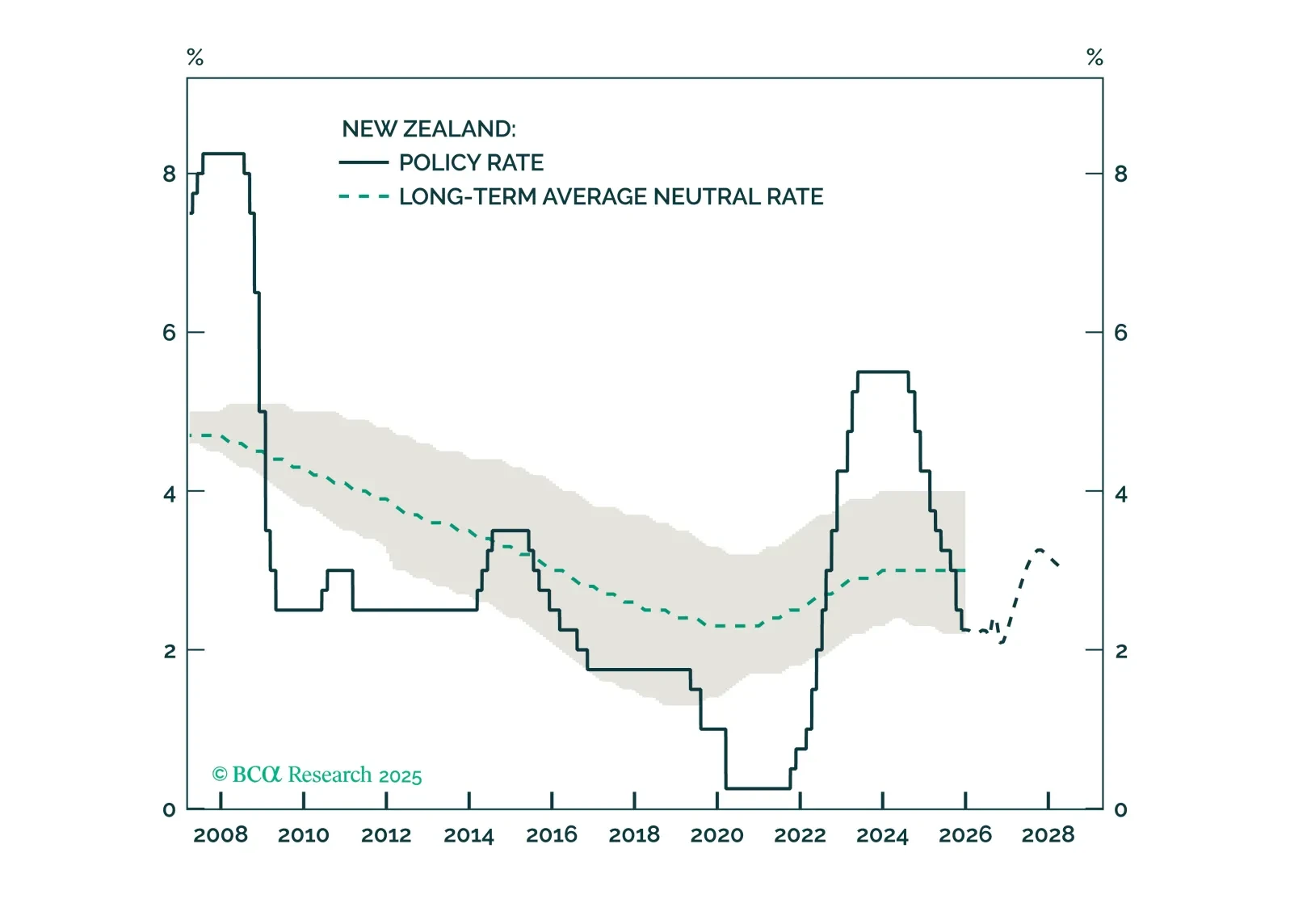

The RBNZ has concluded its aggressive easing blitz. With New Zealand economy finally showing signs of life, both the kiwi and local rates now look ripe for a reversal.

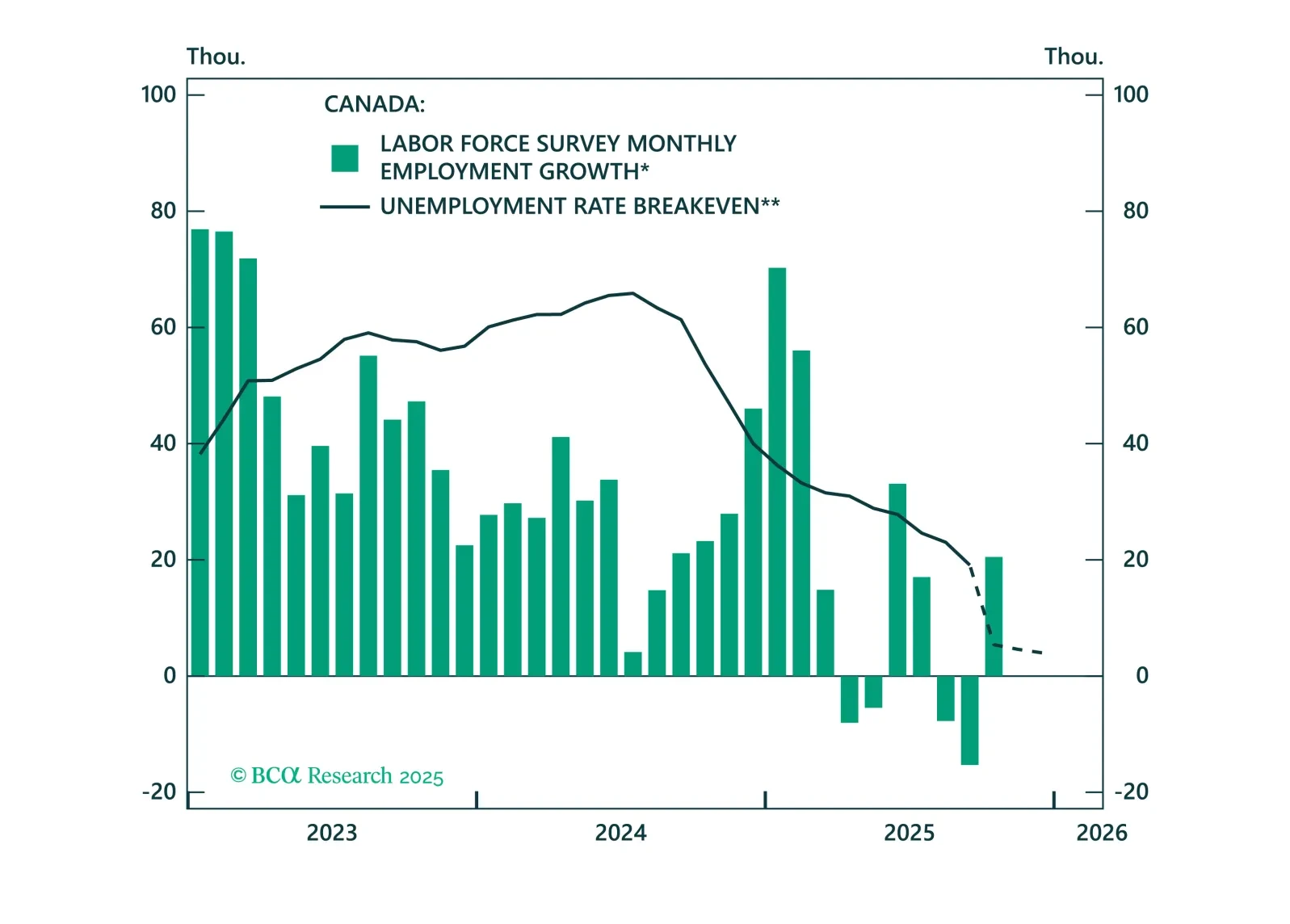

The trade war hit Canada’s economy hard, but the worst is over. In our latest update on Canada, we assess the aftermath of the trade shock, the new budget, and the effects of BoC easing. We outline what this means for duration, the Loonie, and Canadian stocks heading into 2026.

The Bank of England will resume rate cuts in December after the autumn budget is passed. Today’s Strategy Insight discusses what this means for UK gilts and the pound.

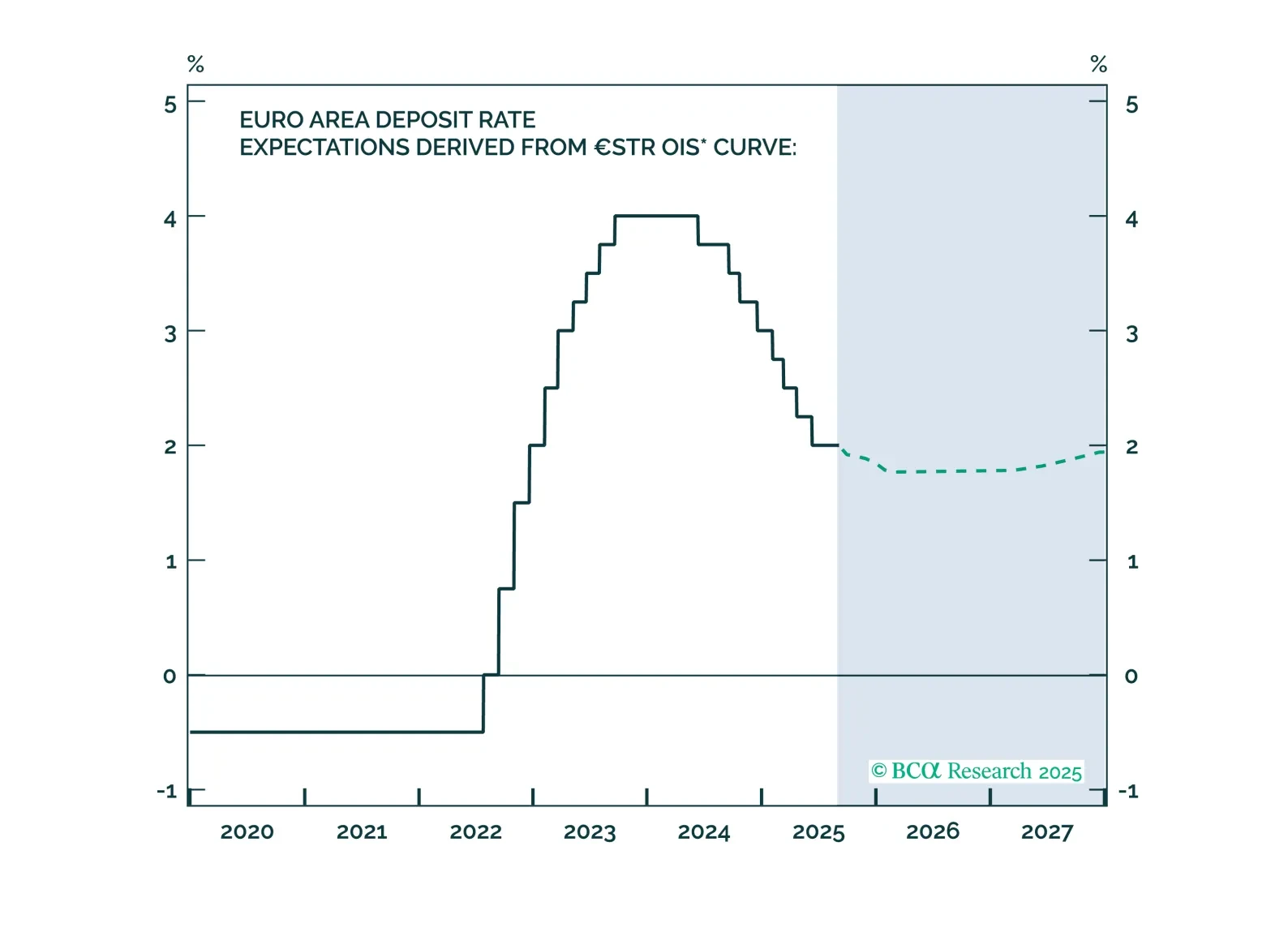

The ECB stood pat today, yet the policy path remains fraught with uncertainty as domestic resilience collides with global headwinds. This dichotomy continues to hold important implications for European assets over the coming months.

The European Central Bank has achieved a soft landing. Inflation is back to target, with well-anchored inflation expectations. The unemployment rate is historically low, and real economic growth is stable, albeit weak. Given that little to no additional easing will come from the ECB, investors should underweight government bonds relative to equities.