Country In-Focus

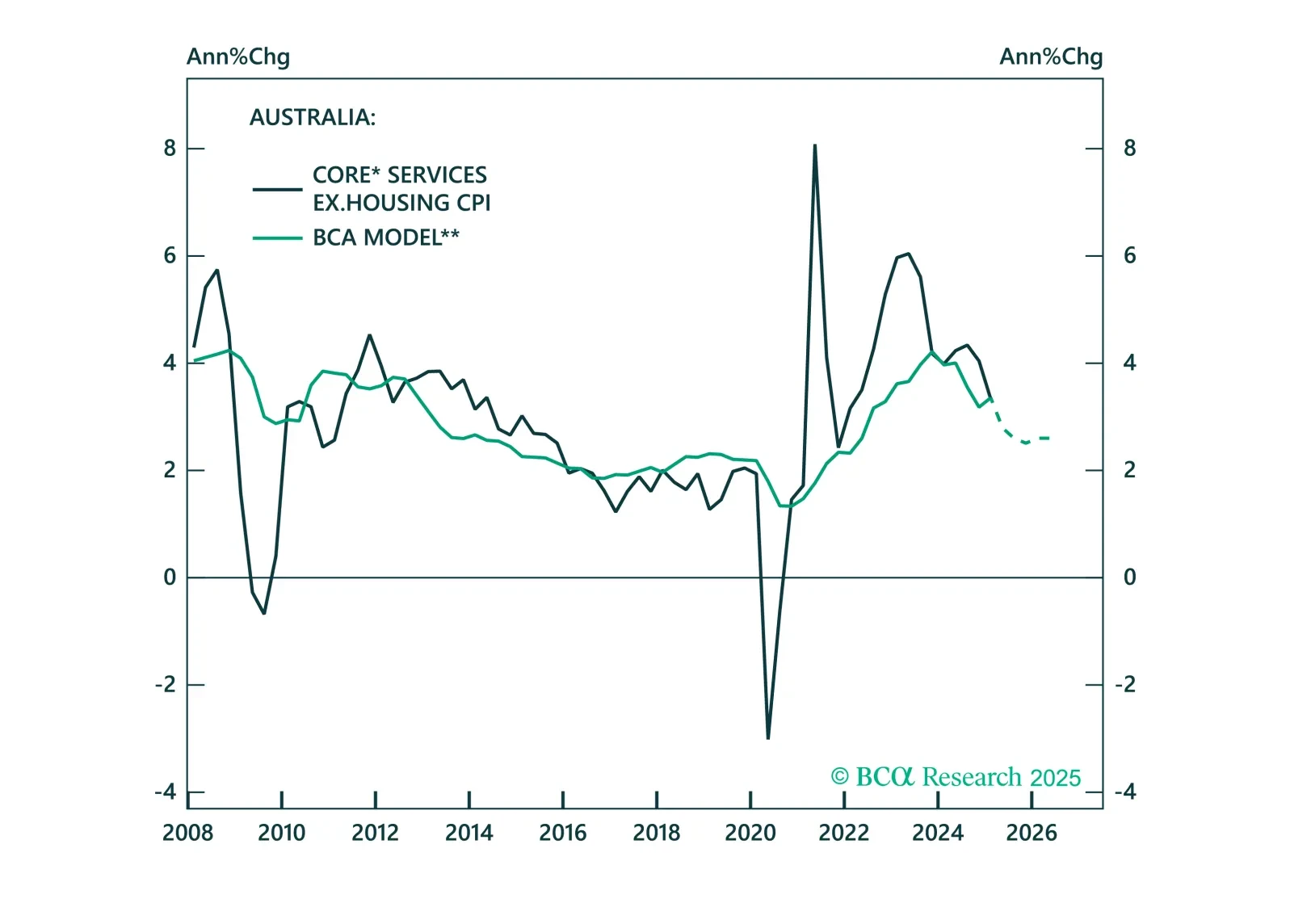

In a widely anticipated move, the RBA resumed cutting rates. However, with housing, consumption, and PMIs improving, we see little scope for the RBA to ease beyond market expectations.

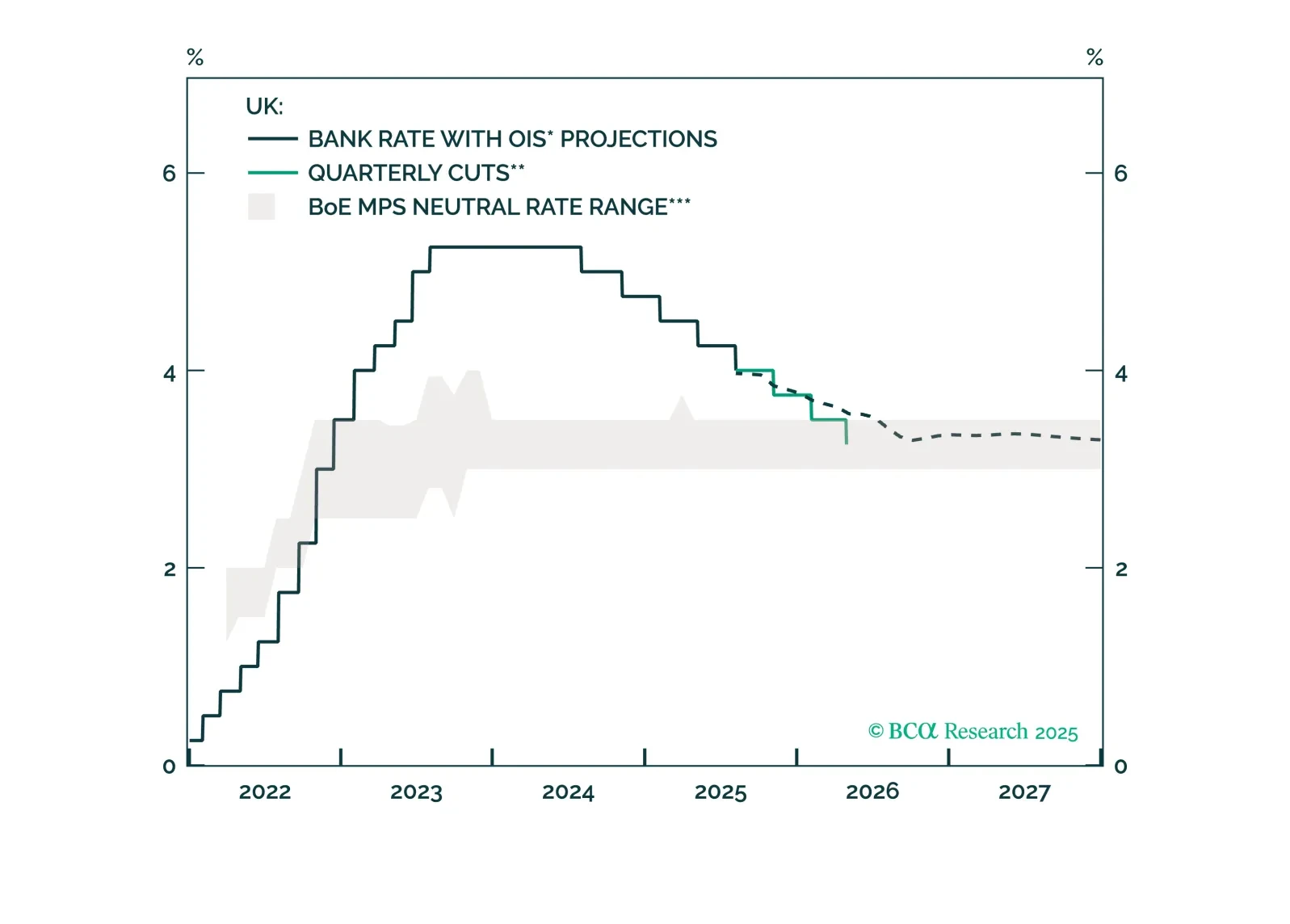

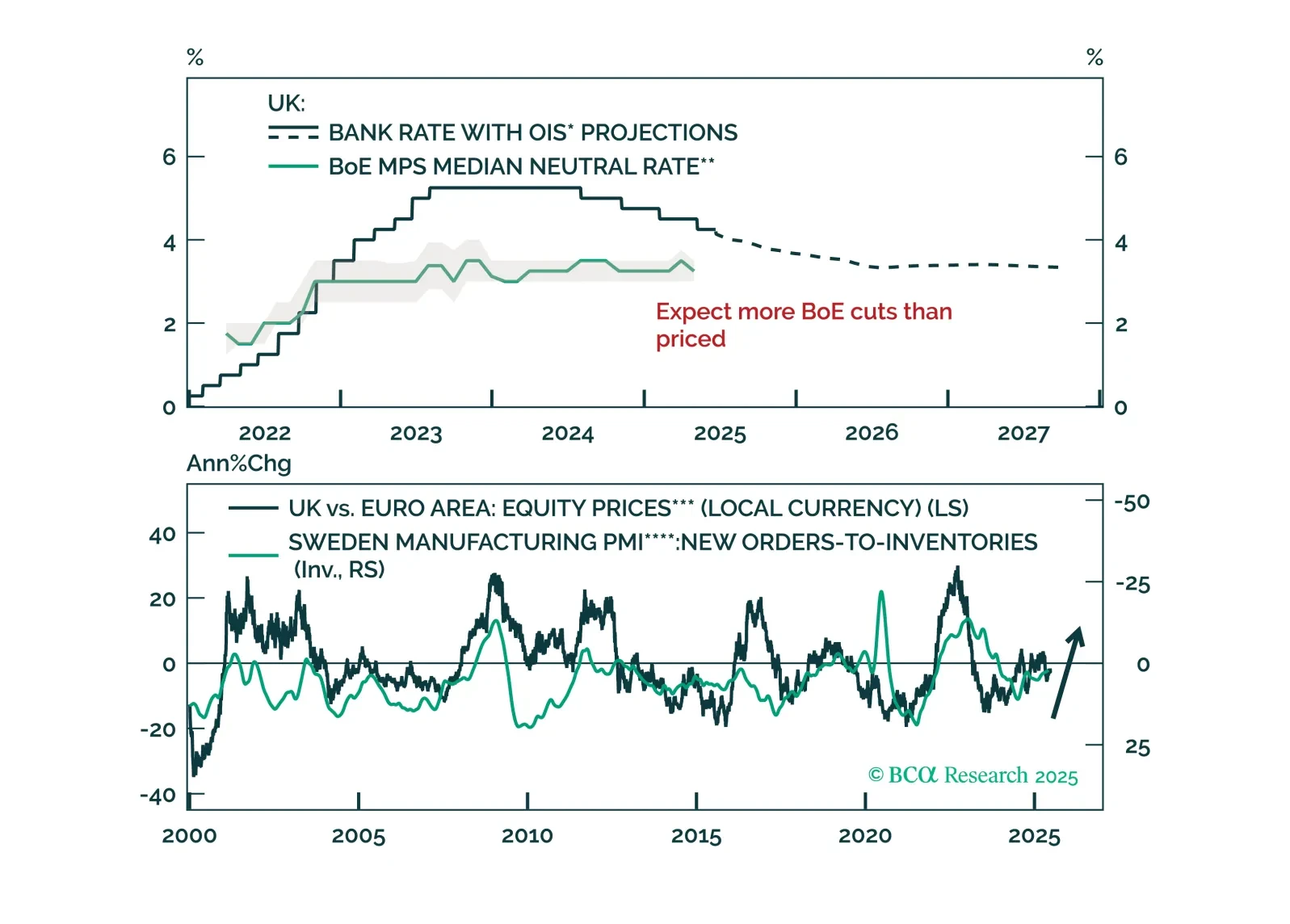

The BoE is easing, but risks falling behind. Labor and growth cracks are starting to emerge, and the Bank may soon be forced to move more decisively. This report outlines why gilts remain a buy and sterling’s path is diverging vs. USD and EUR.

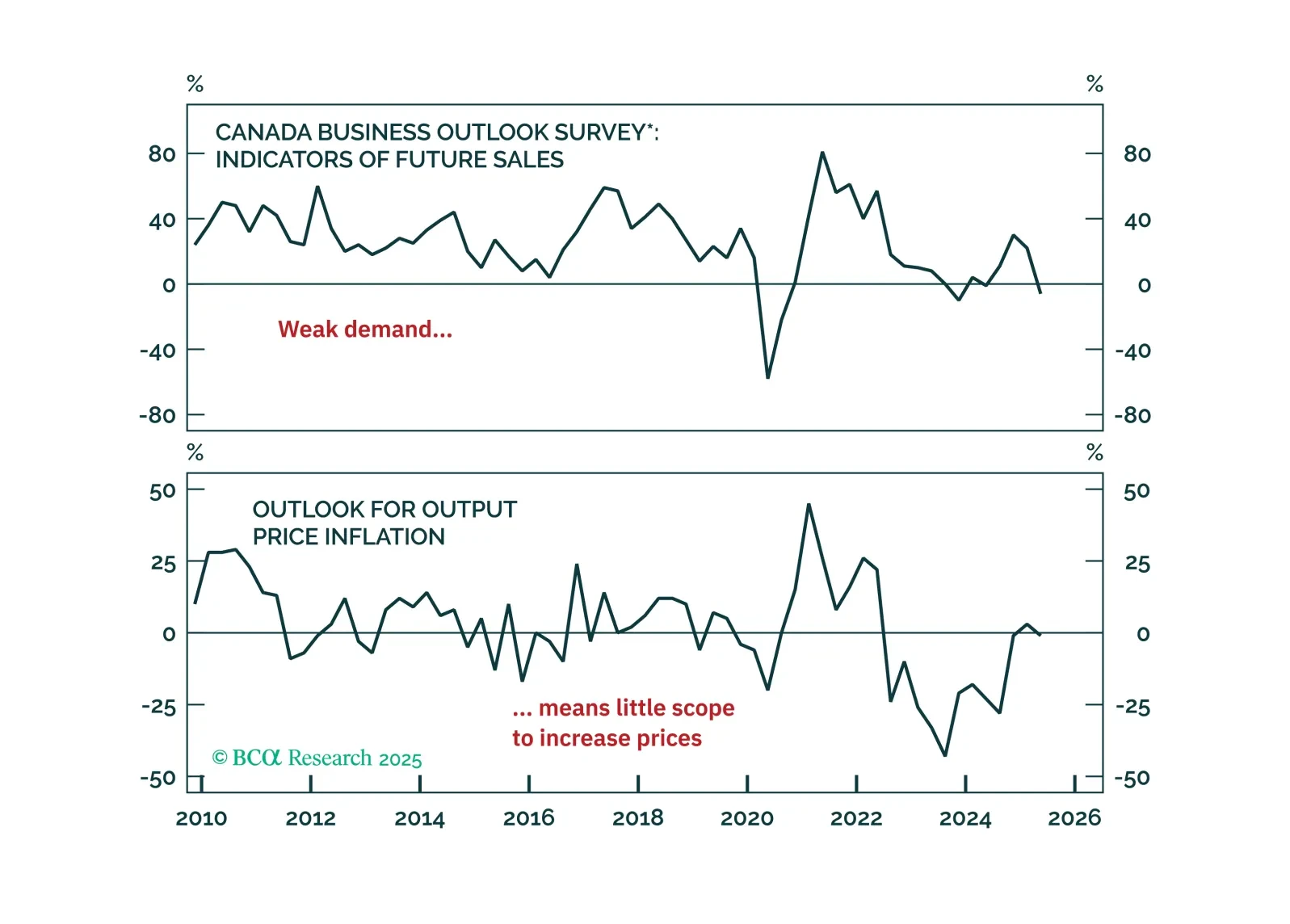

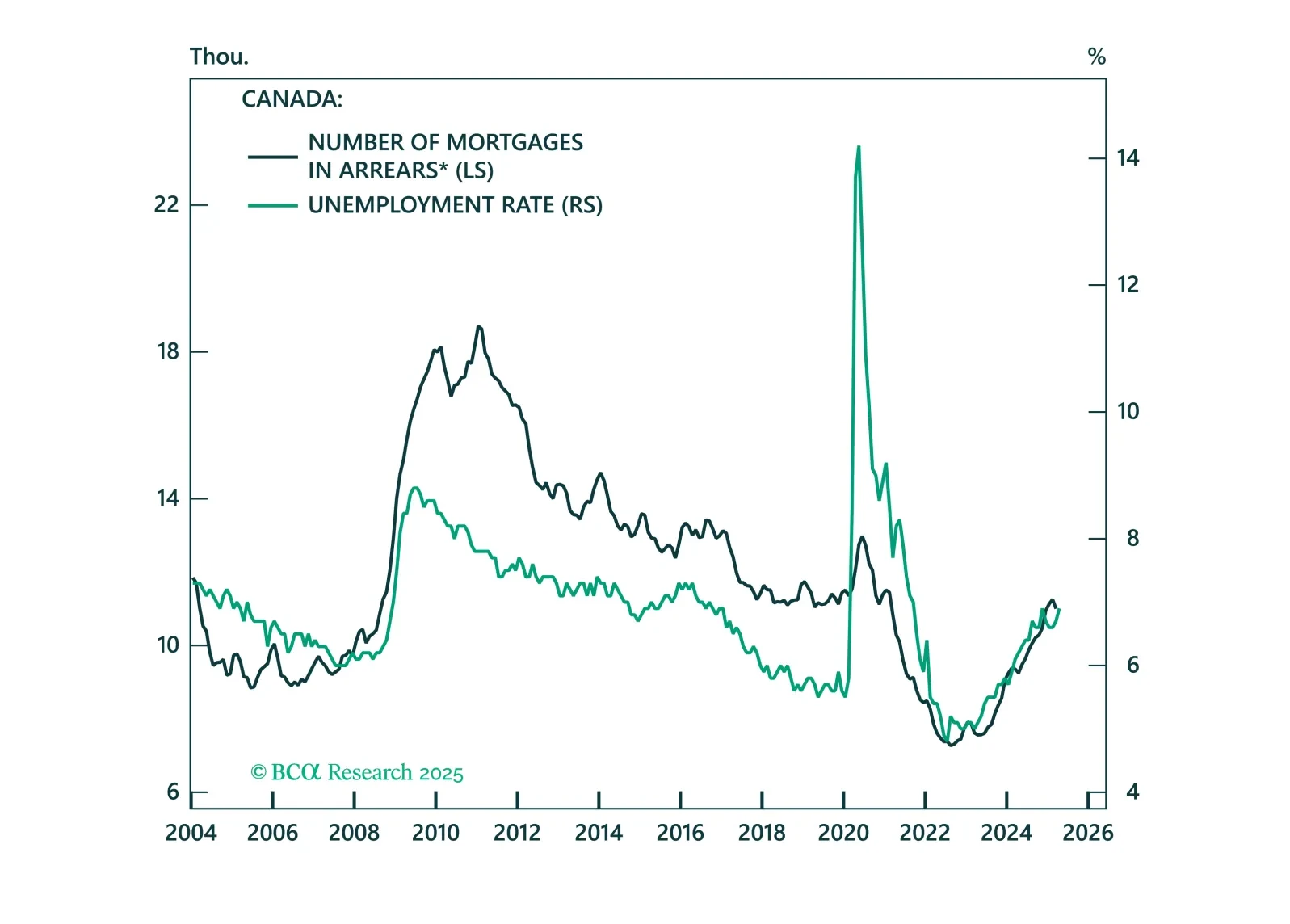

The Bank of Canada continues to hold its policy rate amid trade uncertainty and shows little concern about the potential economic damage from tariffs. We judge the risks differently and view a bet on more rate cuts this year as attractive.

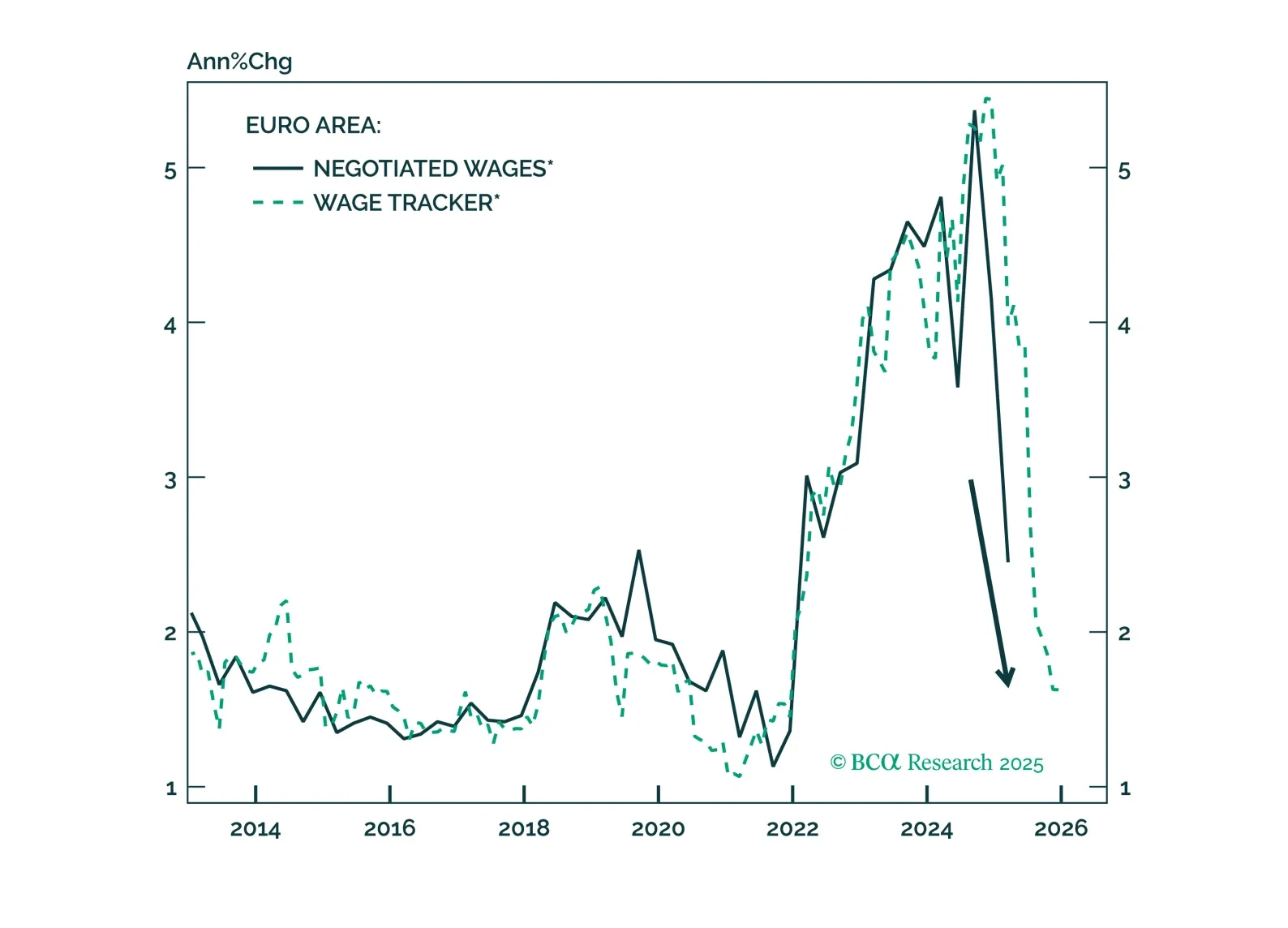

Consensus sees one final ECB cut; we argue two are coming as deflationary forces are building in Europe. Dive in for the trade map: falling Bund yields, tighter peripheral spreads, and a euro primed for a 2026 rebound.

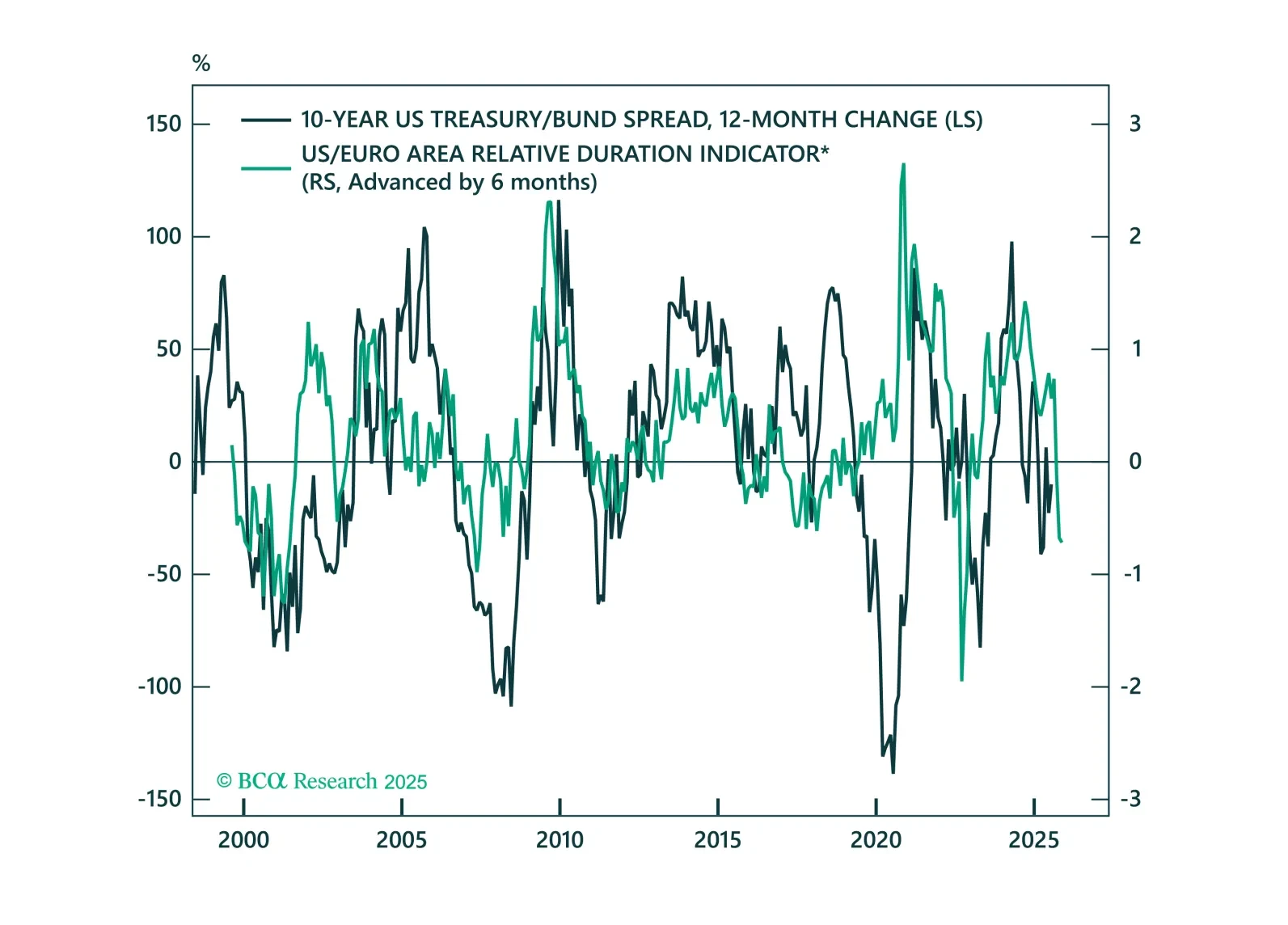

Volatility is back in UST/Bund spreads. We unpack what’s driving the moves and explain what we are watching for tactical opportunities in the UST/Bund spread.

UK inflation risks are falling on the back of a weakening labor market. Read why Gilts and UK stocks are poised to outperform as BoE easing resumes.

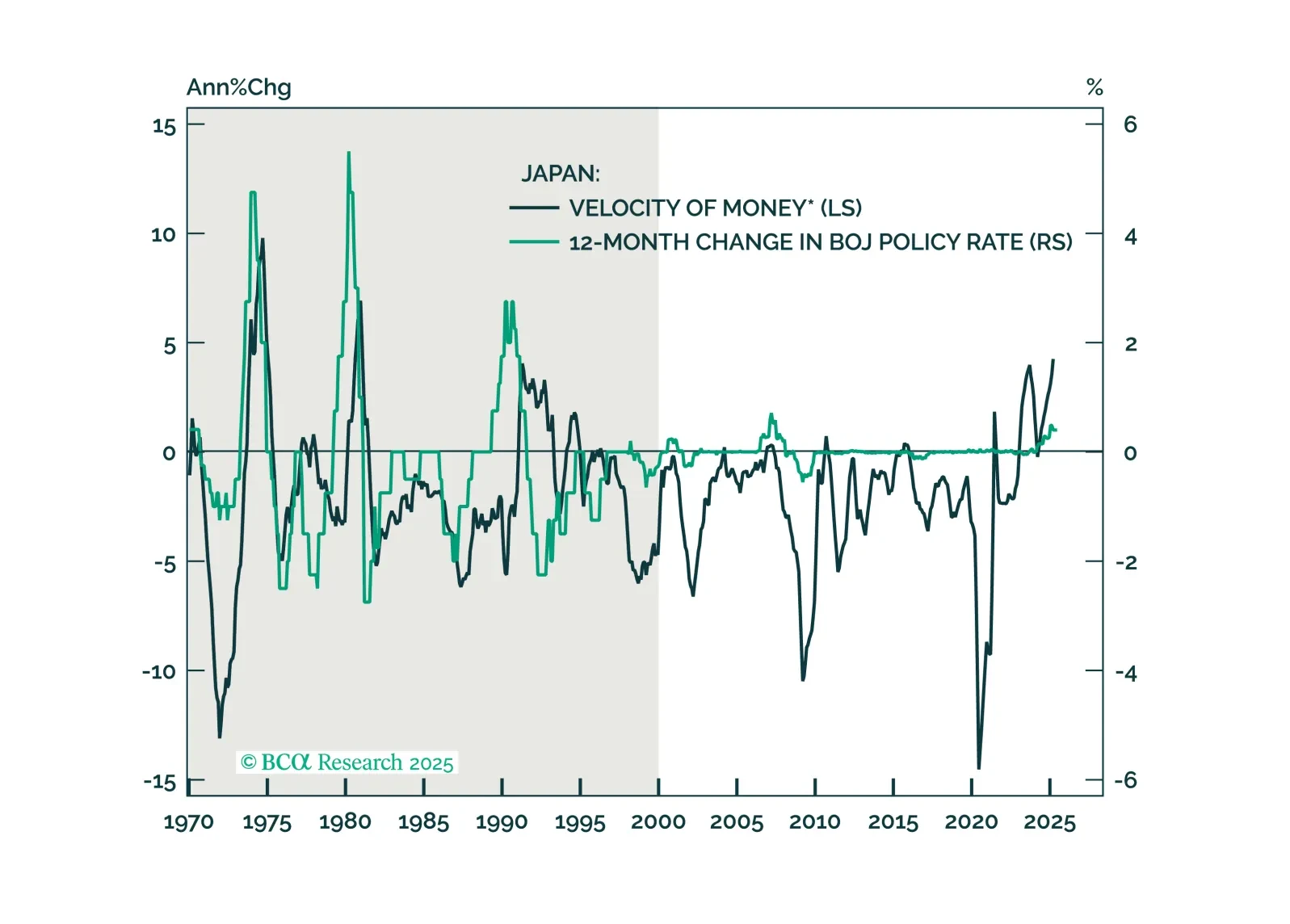

In this note, we reaffirm our underweight position in JGBs and long yen positions given the BoJ’s meeting overnight.

The Bank of Canada may be on hold for now, but deflationary risks are rising fast. Find out why rate cuts may come sooner than markets expect.

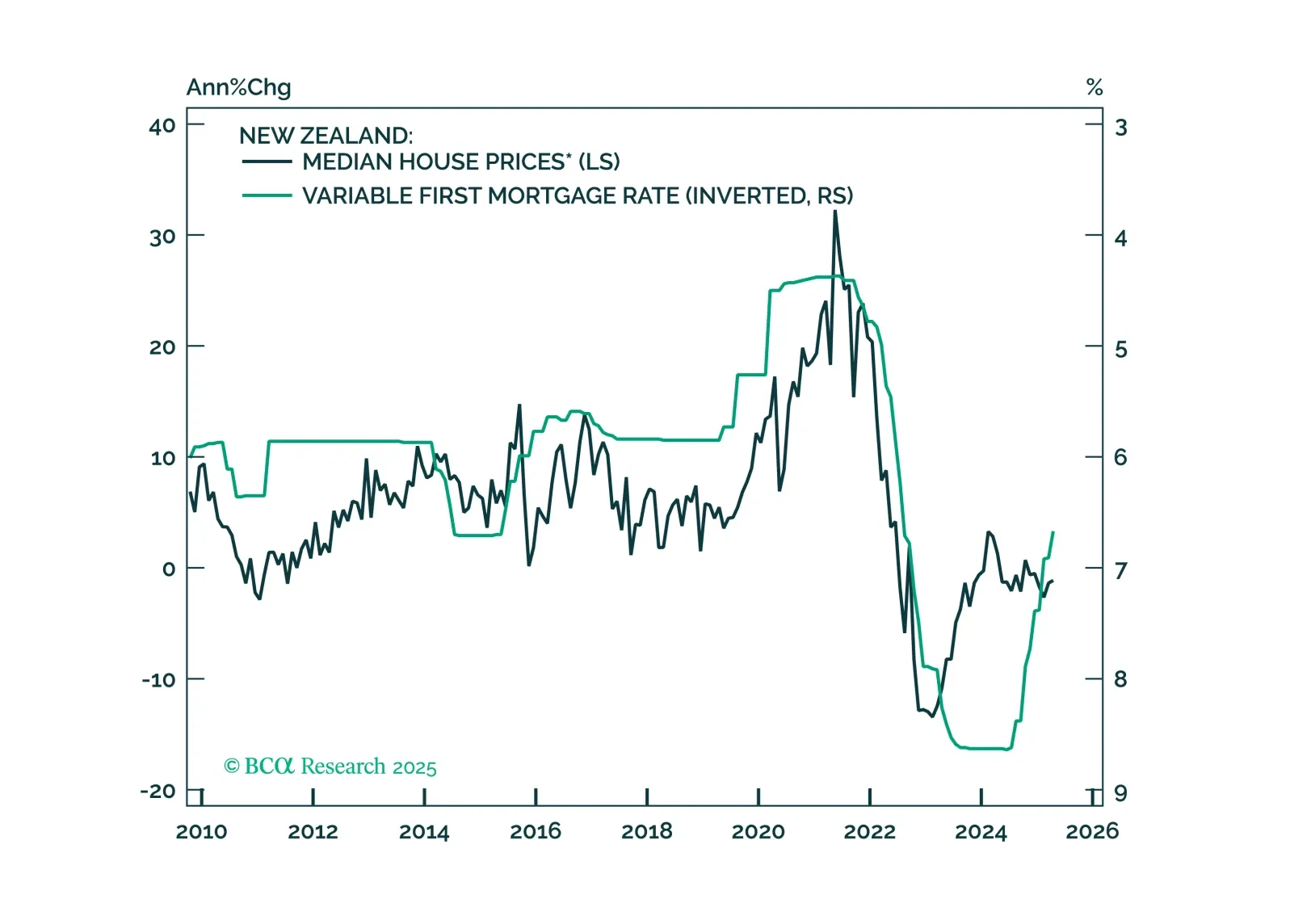

This Insight looks at the implications of the RBNZ’s rate cut on New Zealand assets.

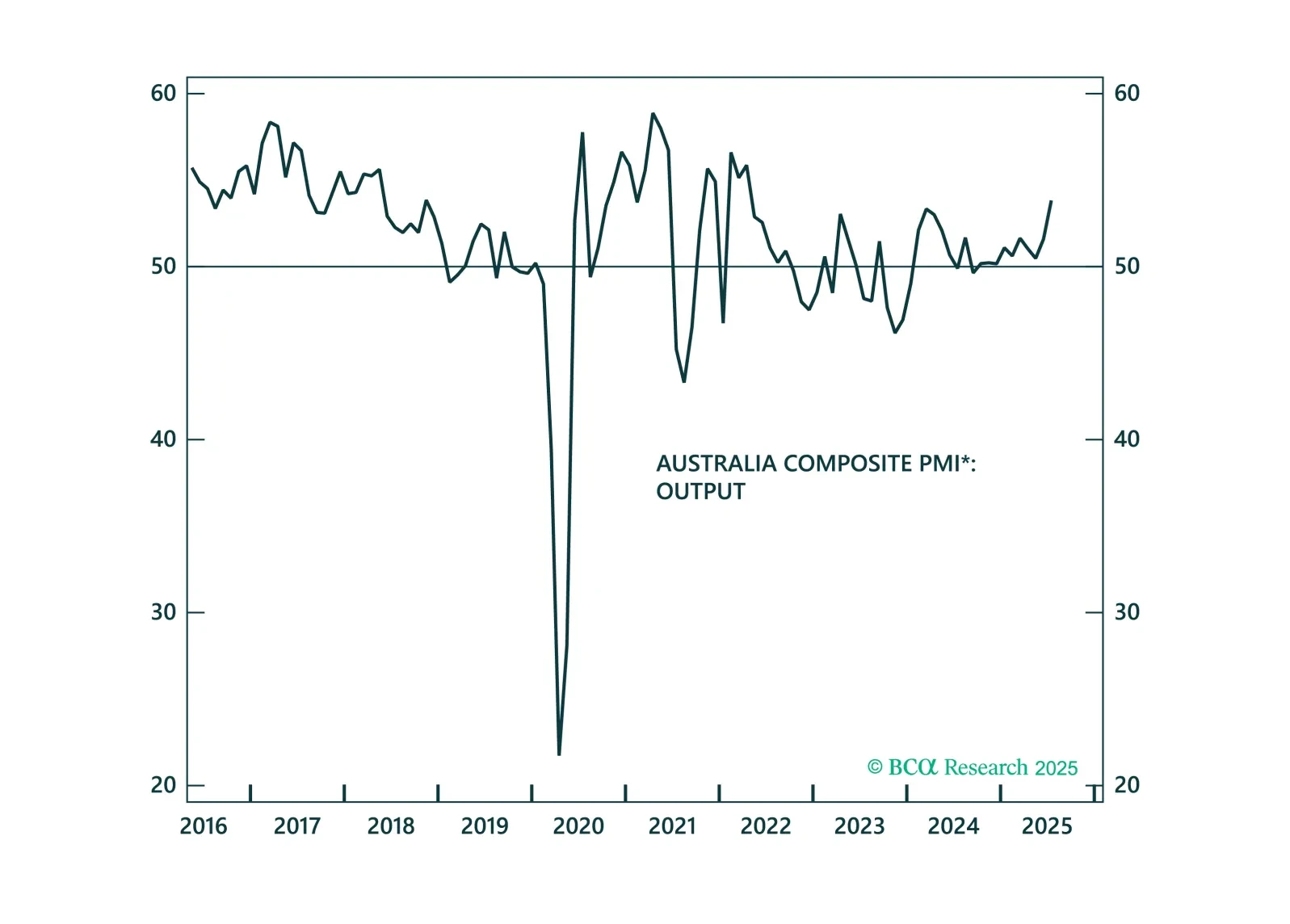

The RBA just turned dovish, but the macro data do not justify many more cuts. We unpack why Australia’s strong labor market and sticky inflation limit the scope for further easing.