Country In-Focus

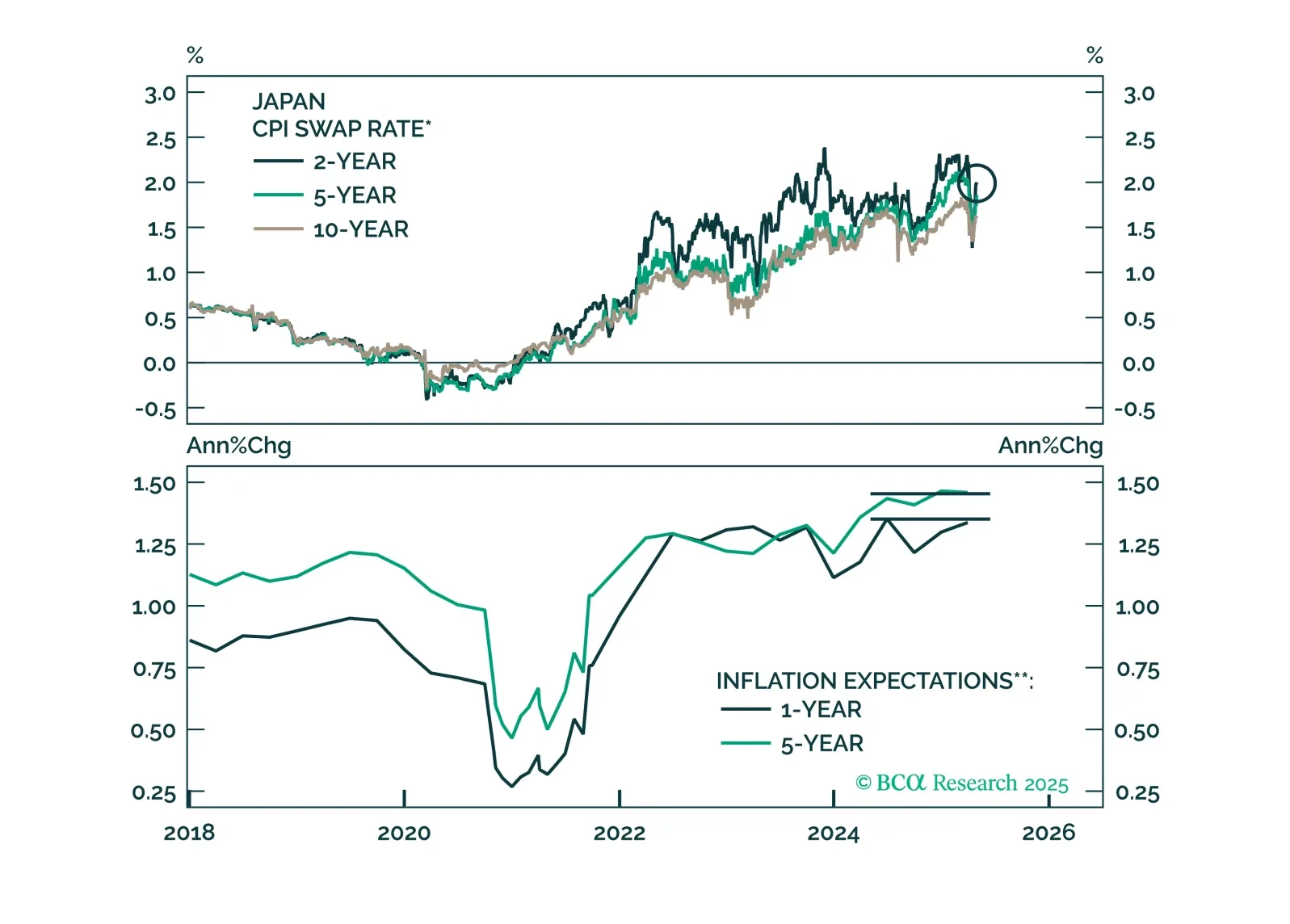

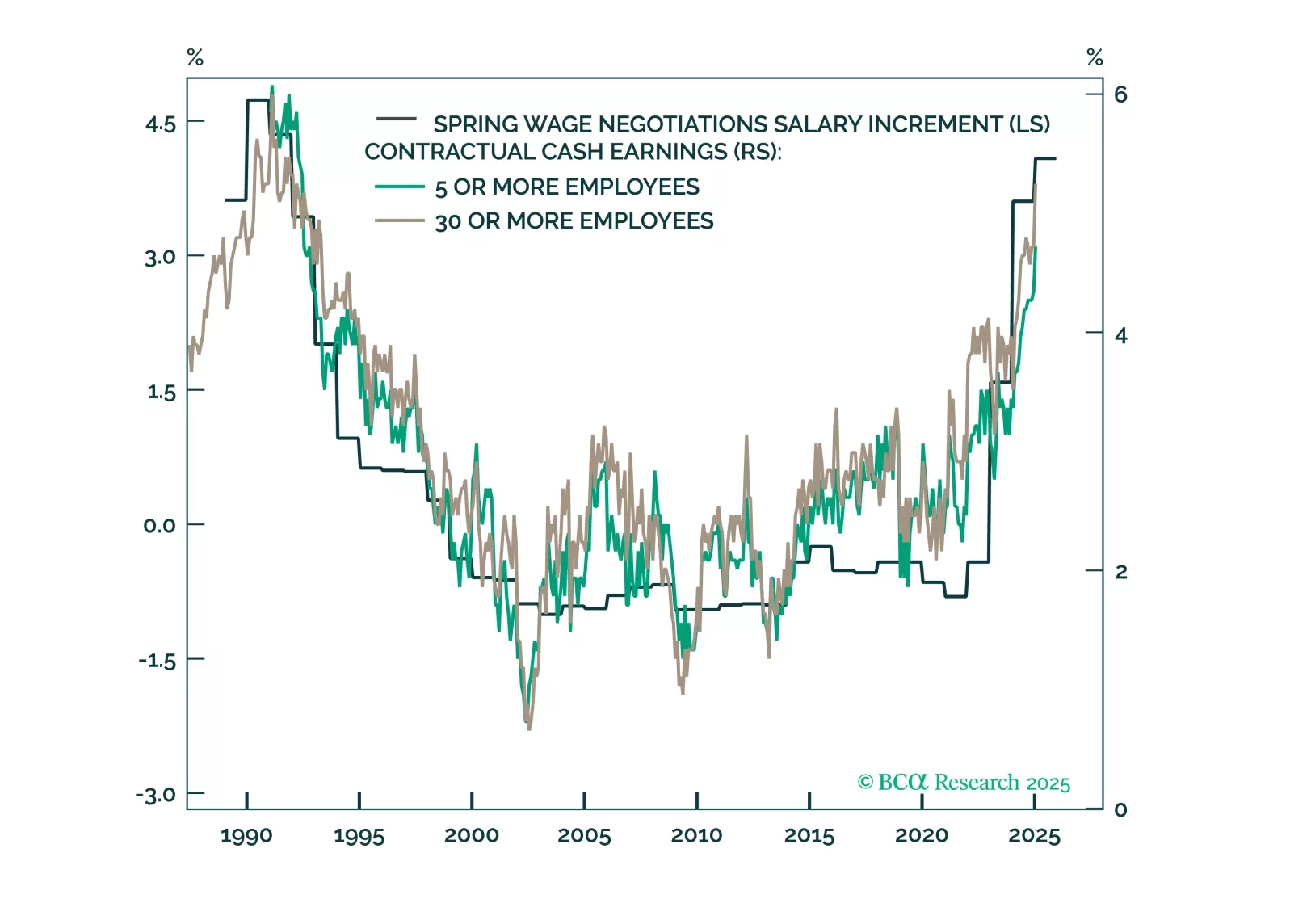

This week’s report looks at Japan, with the recent BoJ meeting. While a trade war has injected uncertainty into the Japanese economy, our conviction remains high that JGBs will underperform other government bond markets, and the yen will ultimately rally. That said, JPY is due for a tactical pullback.

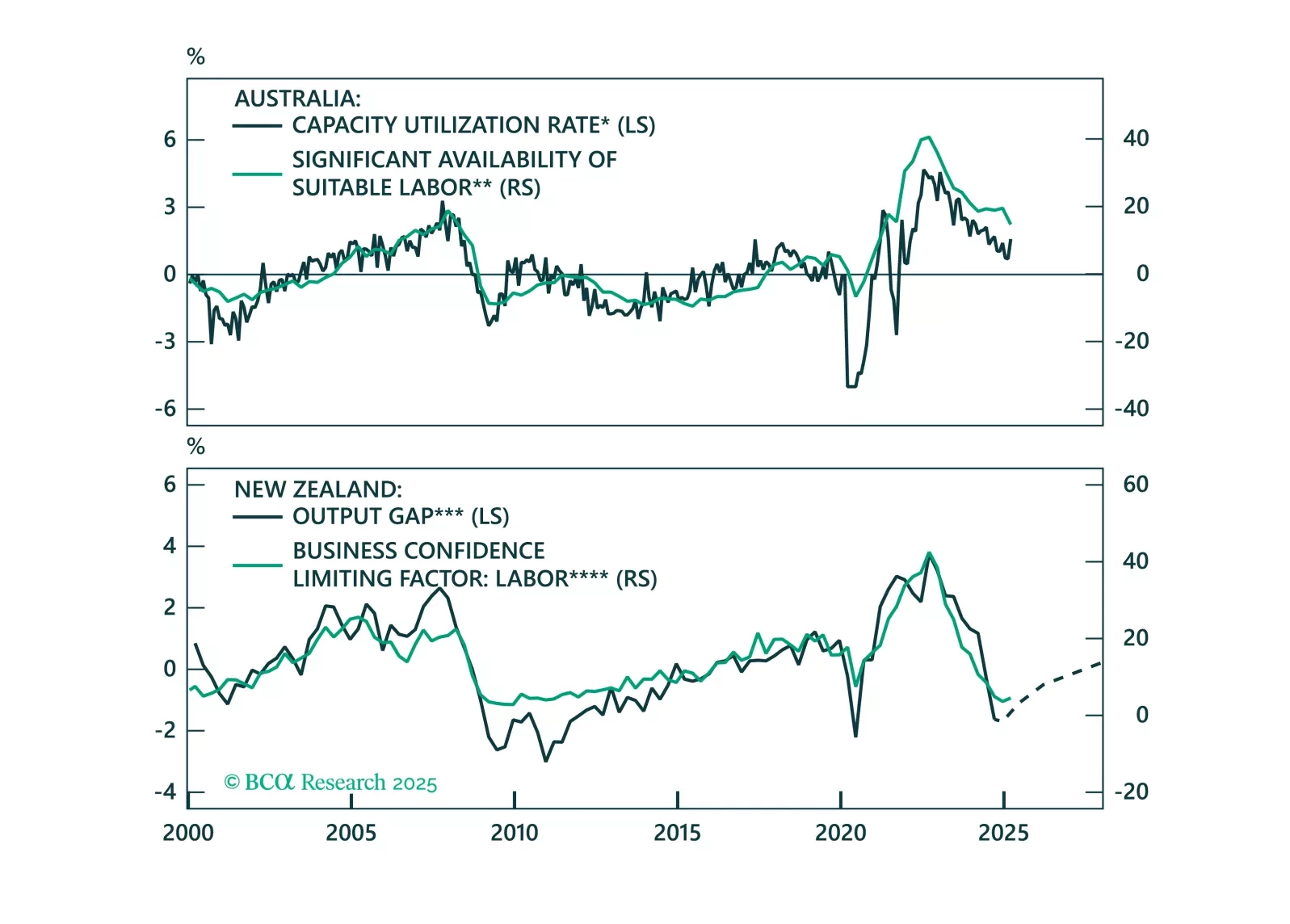

Following the escalation of the US-China trade war, the Reserve Bank of Australia is priced to cut rates most aggressively among its G10 peers. Across the Tasman Sea, the Reserve Bank of New Zealand has already cut rates aggressively, but the economy has yet to respond to this policy easing. This Special Report will examine the prospects of monetary policy for both of these central banks.

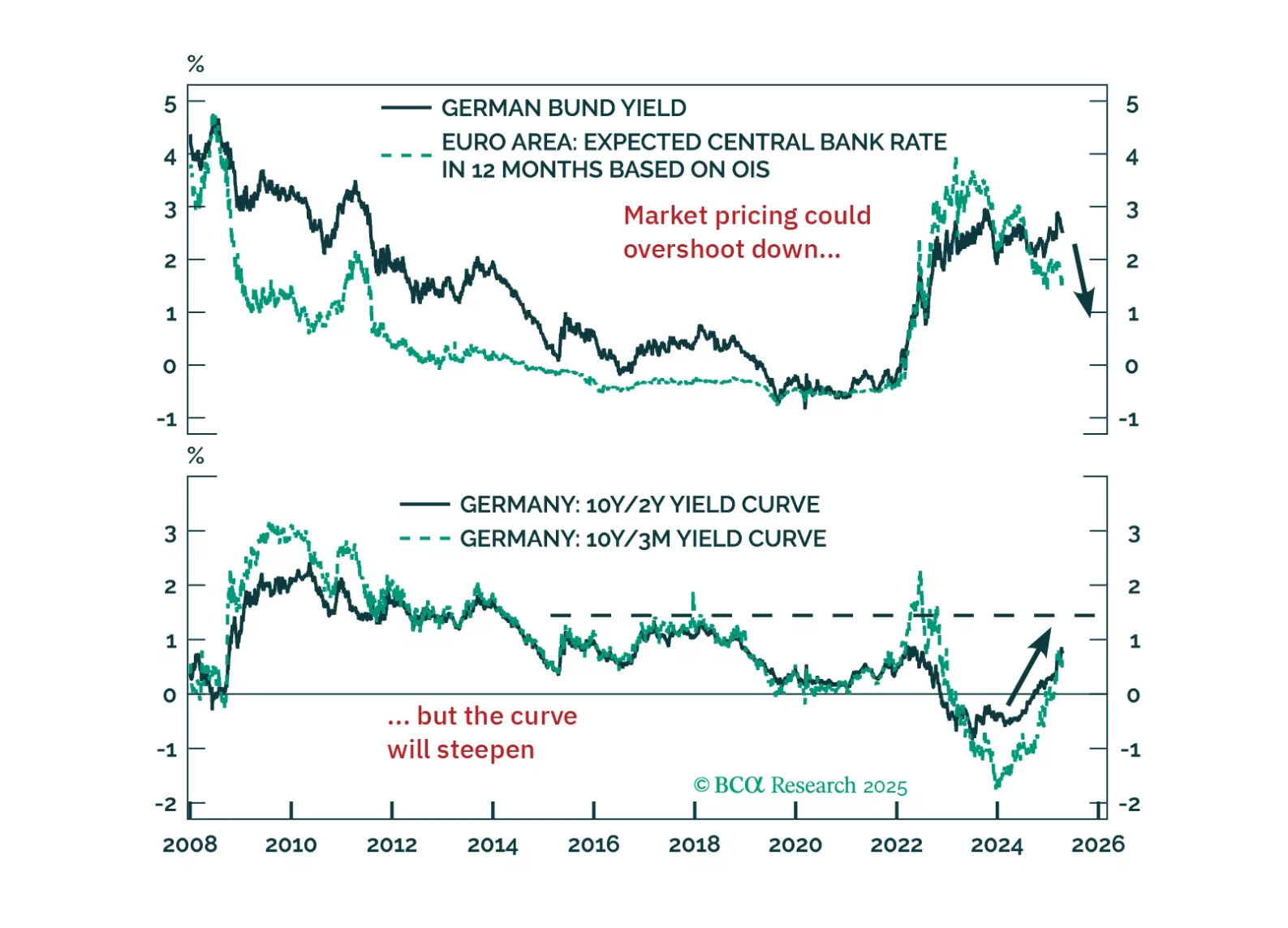

Europe’s deflation problem is getting harder to ignore. This week’s ECB cut is just the beginning — tariffs, the euro’s rally, and softening demand all point to more easing ahead. We explain what it means for yields, equities, and EUR/USD.

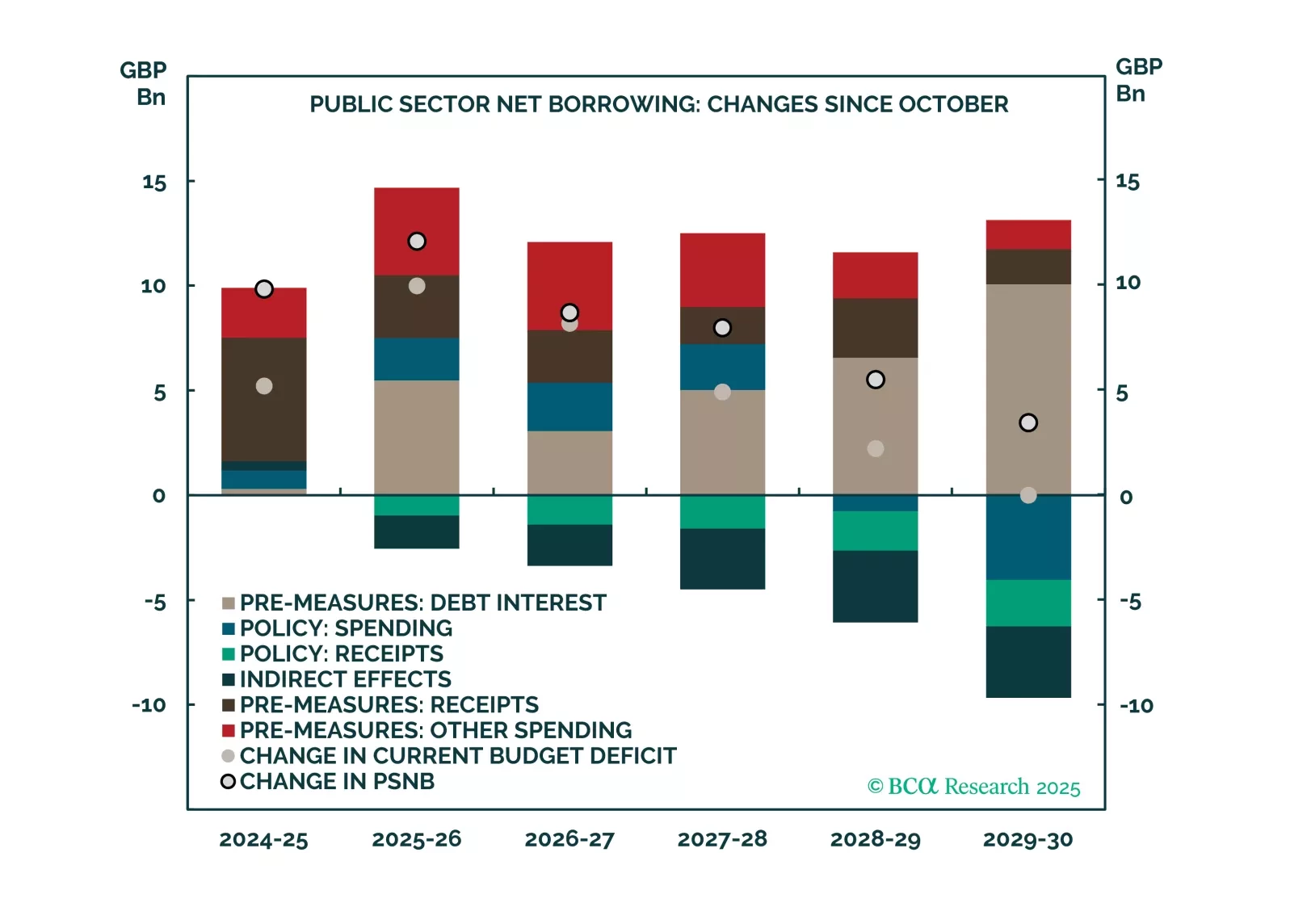

This report is a quick take on our views on UK bonds and FX, given the recent budget.

Given the meetings between the Bank of Japan, the Bank of England, and the Swiss National Bank, our highest convictions views are:

Overweight UK Gilts. It is also time to sell sterling. We are short sterling, as of 1.30.

Underweight JGBs. Correspondingly, be long the yen.

A short CHF/JPY position remains a core holding. Selling GBP/JPY is also a great trade.

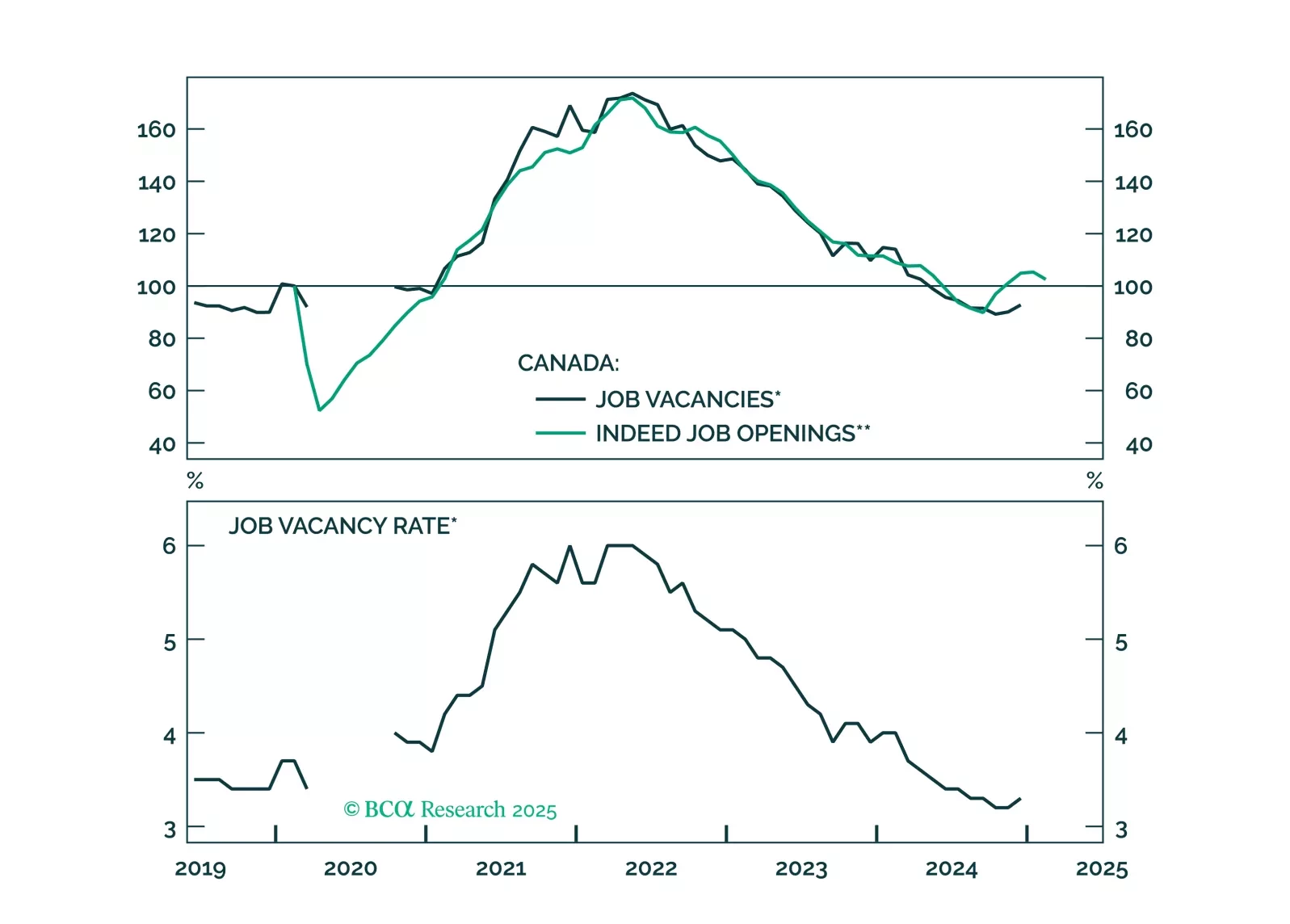

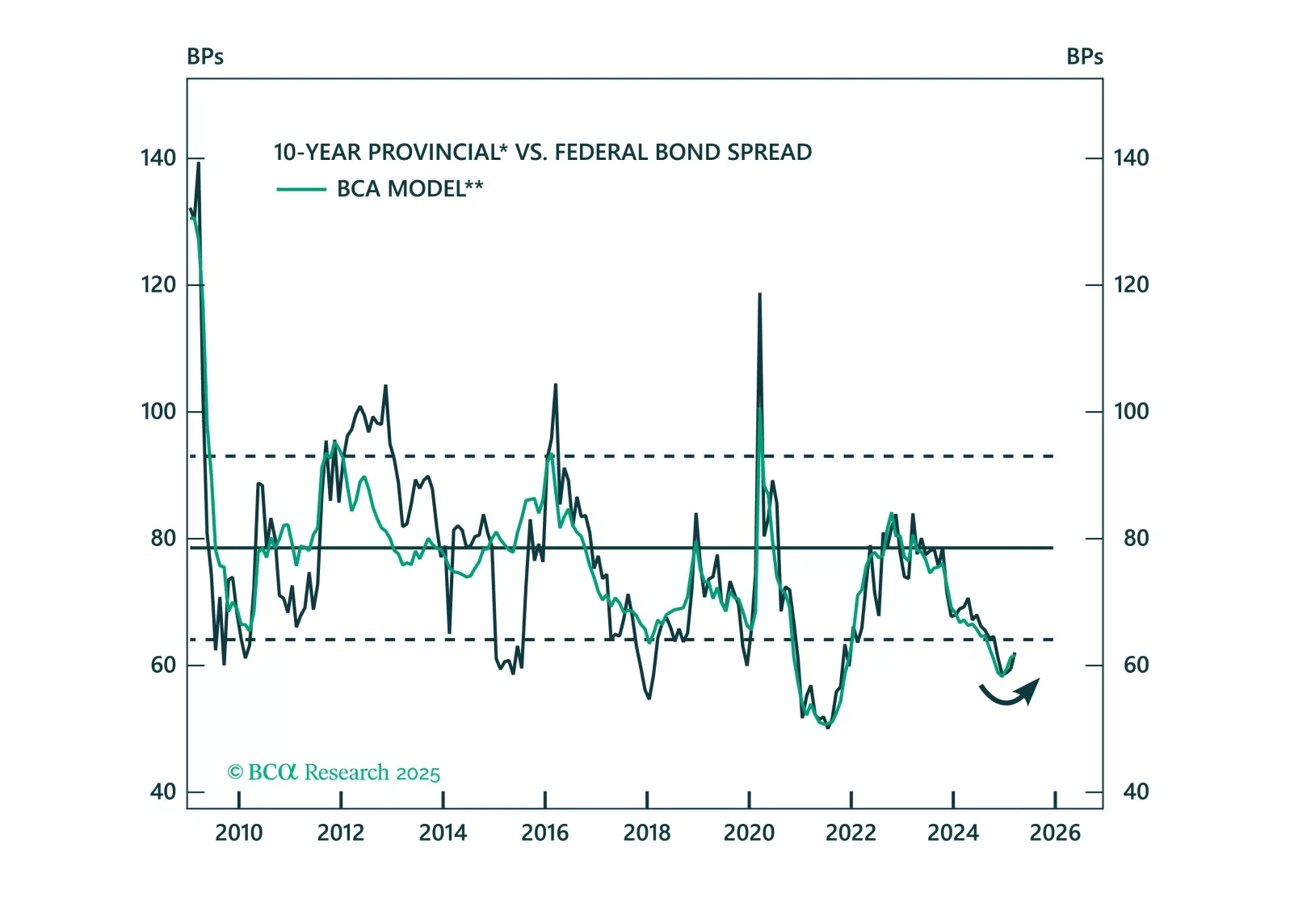

The trade war complicates the Bank of Canada’s task to achieve stable inflation. But the bottom line is that rising uncertainty, which will dampen business sentiment, will cause the BoC to cut rates by at least what is priced in the CORRA curve, and likely to 2%. The CAD, which is very oversold, might not depreciate much. The big trade is a bet on a spread widening for Canadian provincial bonds.

In this report, we explore the Canadian provincial bond market by developing a model to analyze its main drivers and understand the impact of a potential trade war between Canada and the US.

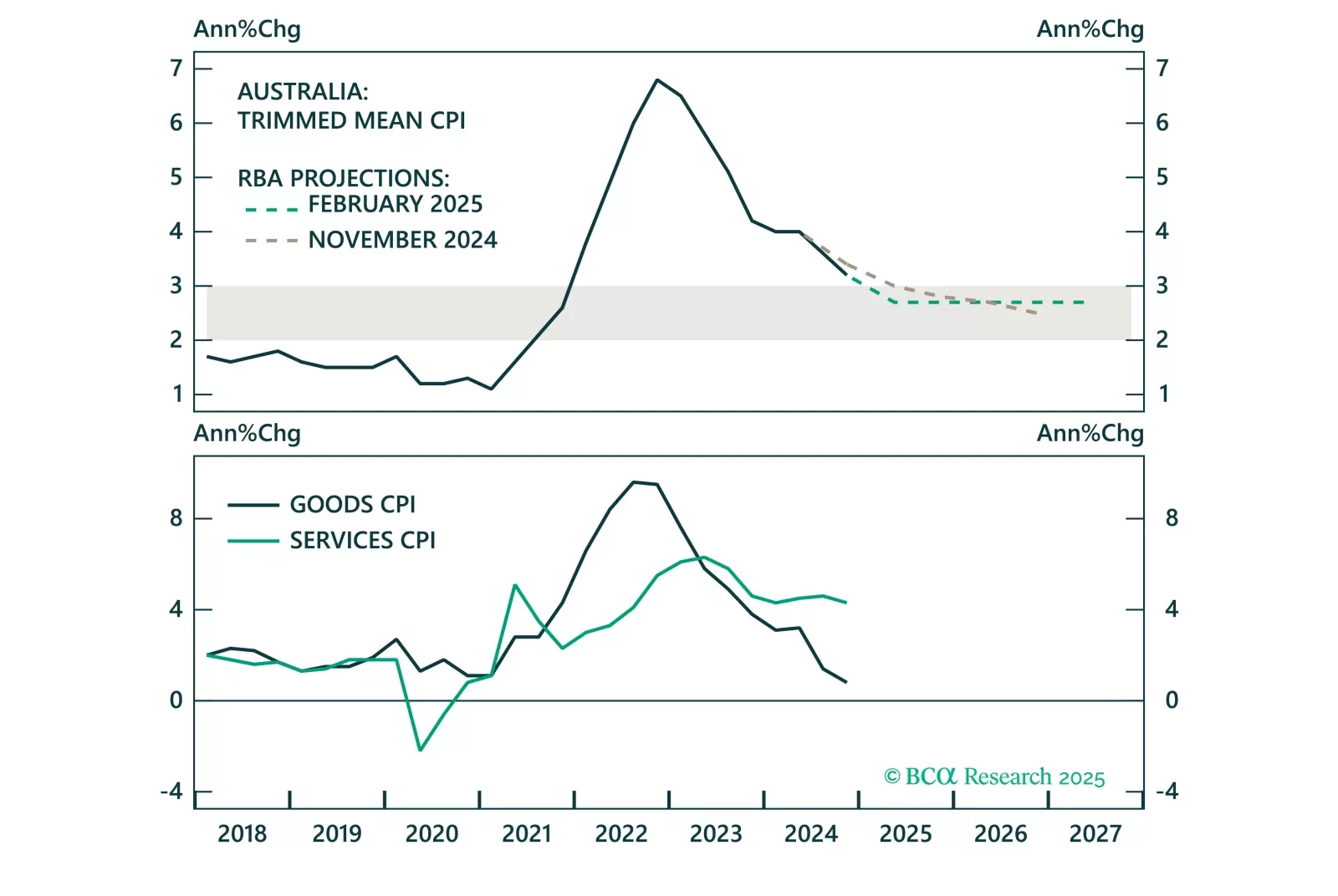

Overnight, the RBA cut the cash target rate for the first time since 2022, marking the beginning of the policy easing cycle in Australia. However, the RBA will proceed cautiously with further rate cuts, given a tight labor market and still elevated services inflation. This will keep Australian government bond yields elevated versus global yields, benefitting the Australian dollar.

Questions about fiscal risks and their impact on bond markets have become more frequent in client conversations. This Special Report provides a framework to assess a country’s fiscal sustainability and how it affects its bond market outlook. On an individual country basis, Spain has shown a remarkable turnaround in its fiscal sustainability outlook while the fiscal outlook for France continues to deteriorate.

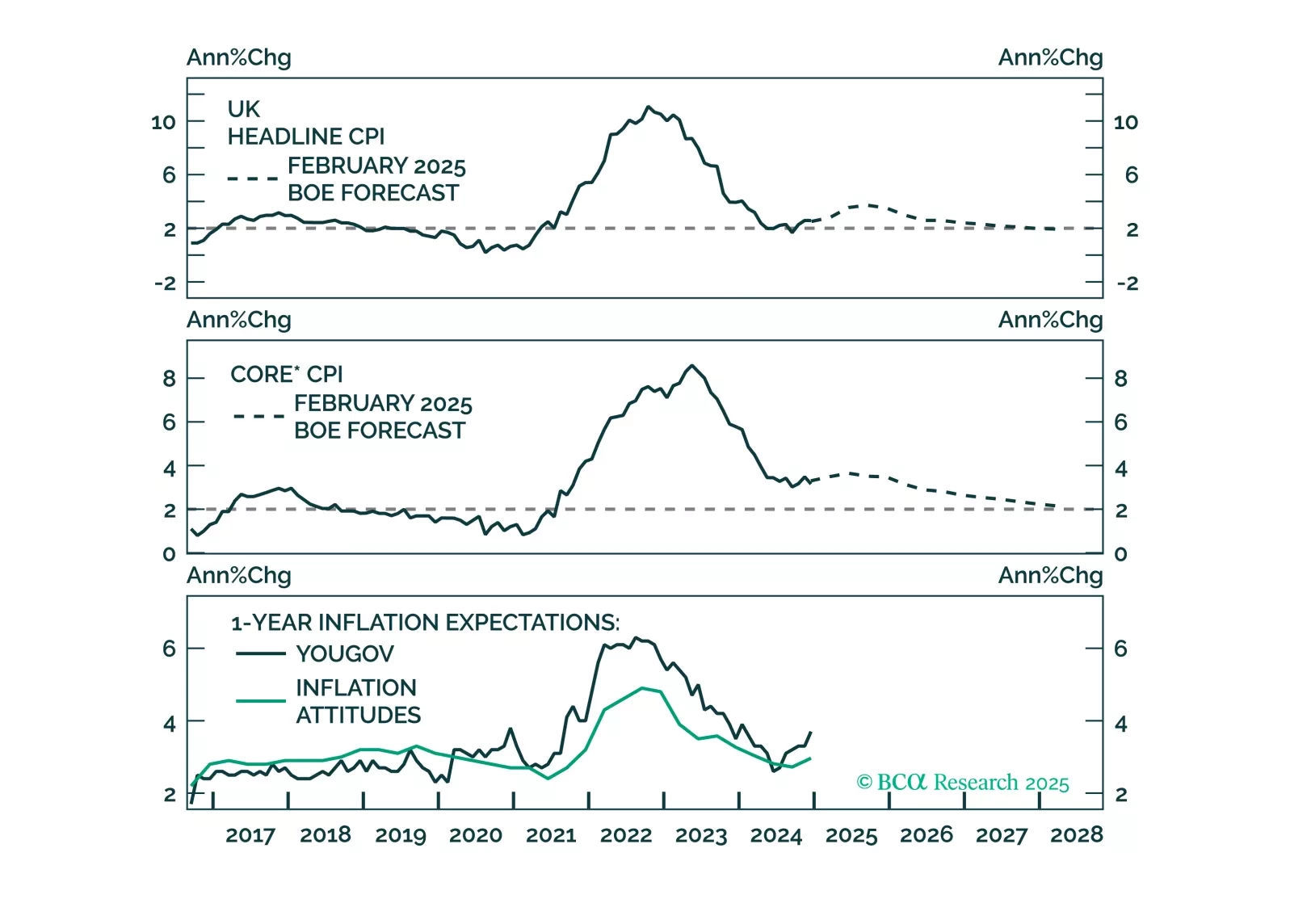

Following today’s Bank of England’s policy meeting, at which the policy rate was cut by 25 bps, we discuss our outlook for monetary policy in the UK. We expect the gradual easing to continue and discuss the investment implications for UK gilts and sterling.