Country In-Focus

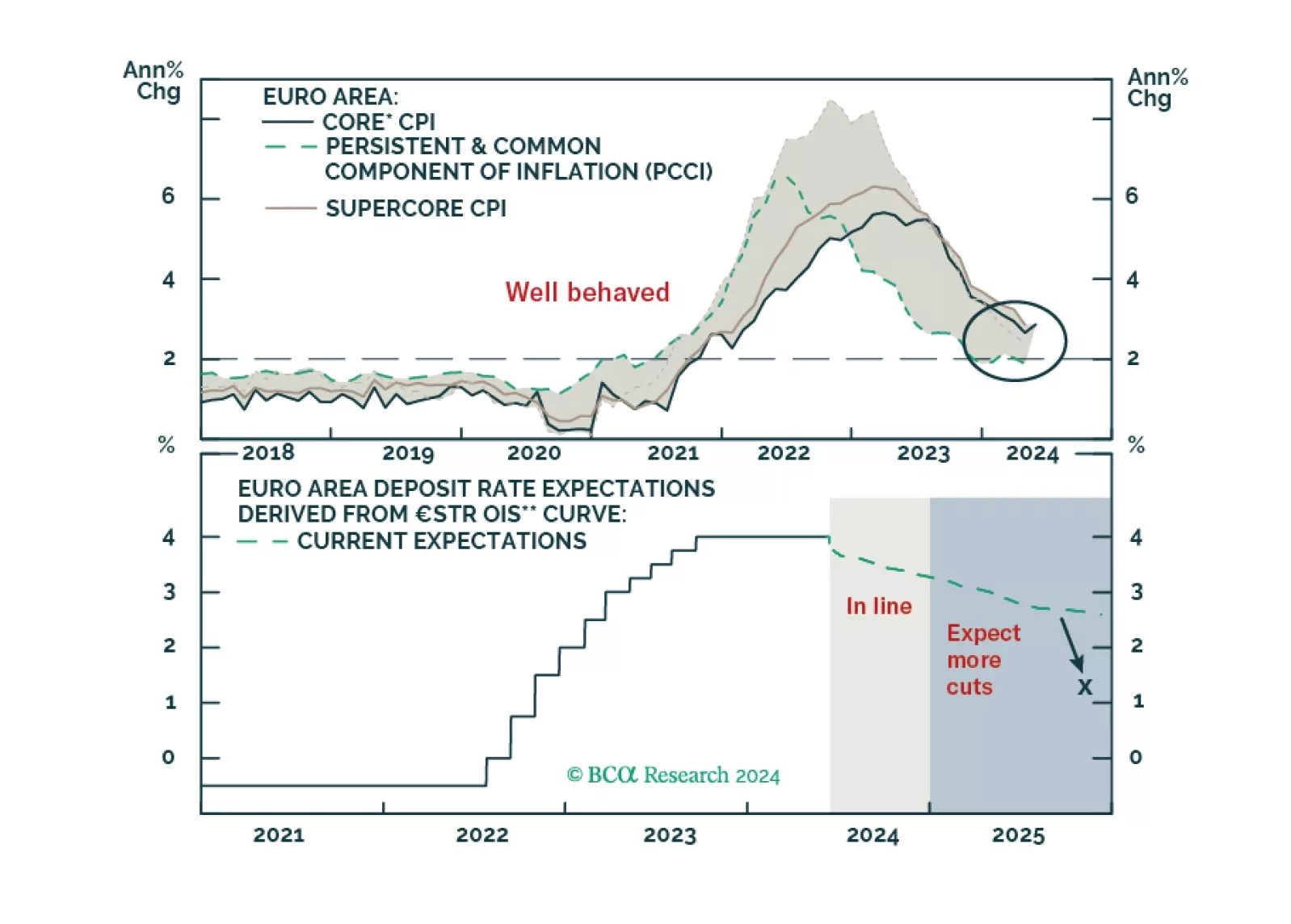

The ECB will cut rates once more this year; however, markets underprice how far it will ease next year.

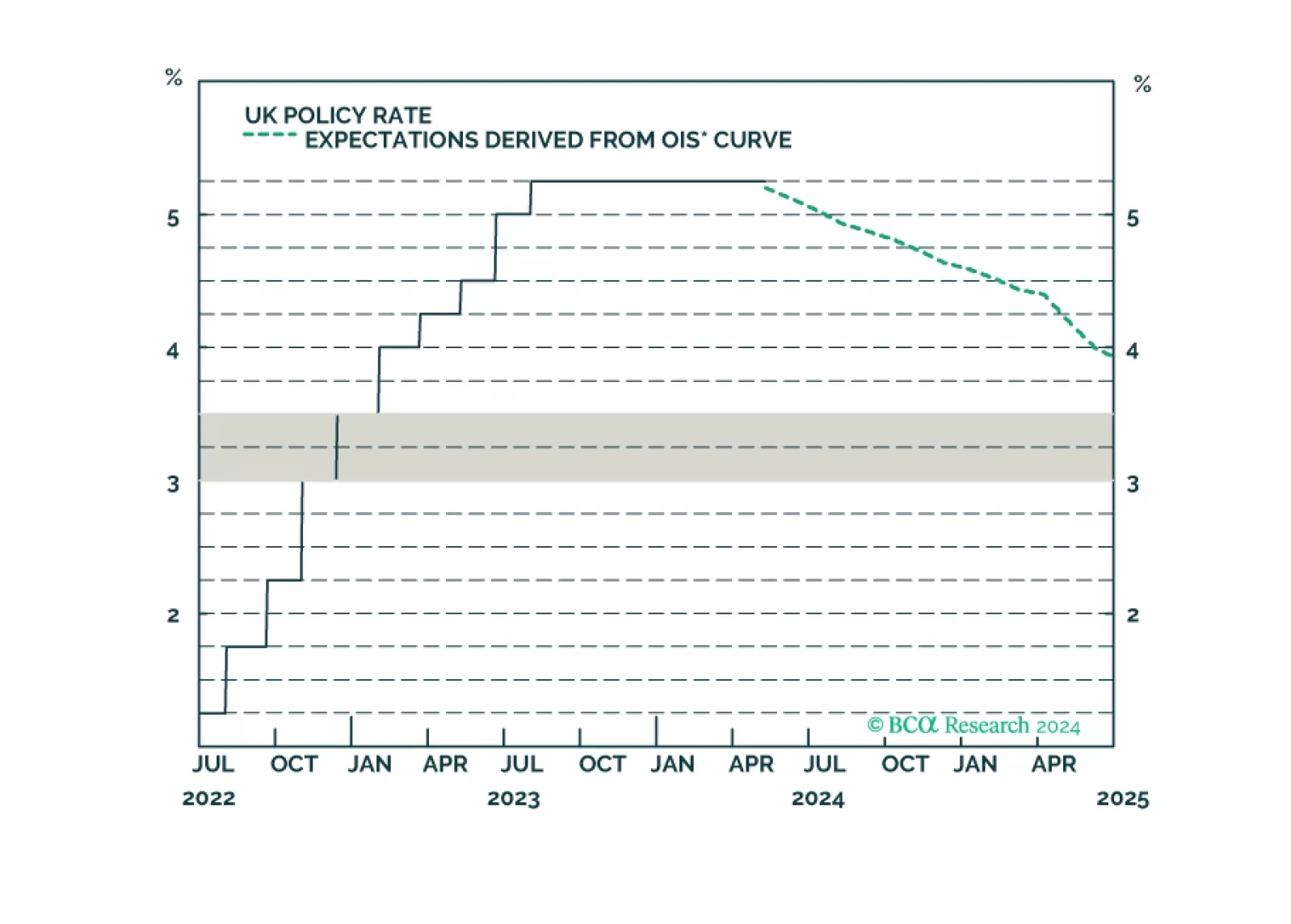

What do the mixed signals sent by the UK economy mean for the Bank of England, and what are the implications for Gilts and the British pound?

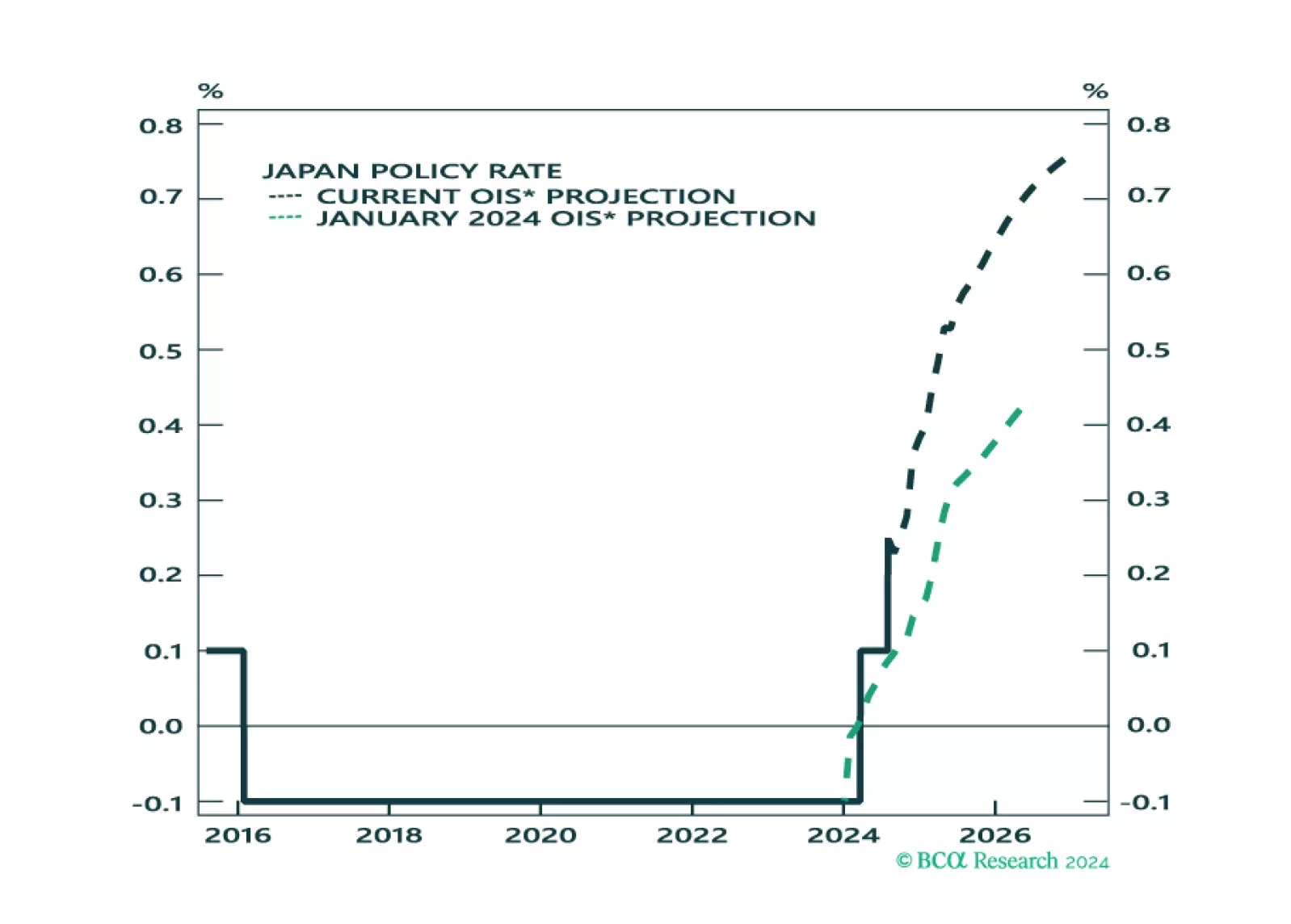

We assess the investment implications of the BoJ and Fed meetings, and give our take on the next policy moves. We also assess the impact on asset markets.

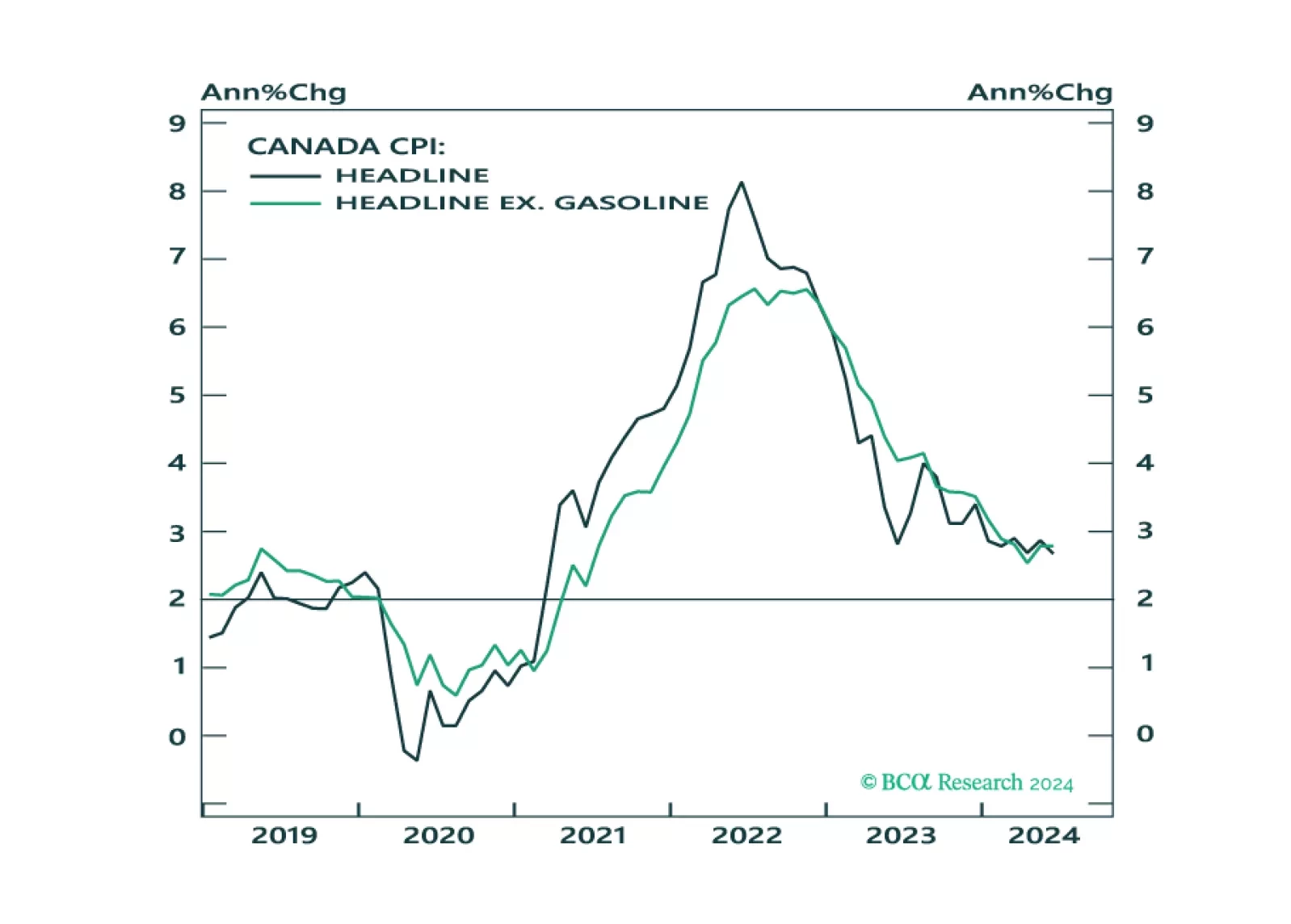

In this Insight, we look into the recent CPI release in Canada, and the possible implications for fixed-income market trades.

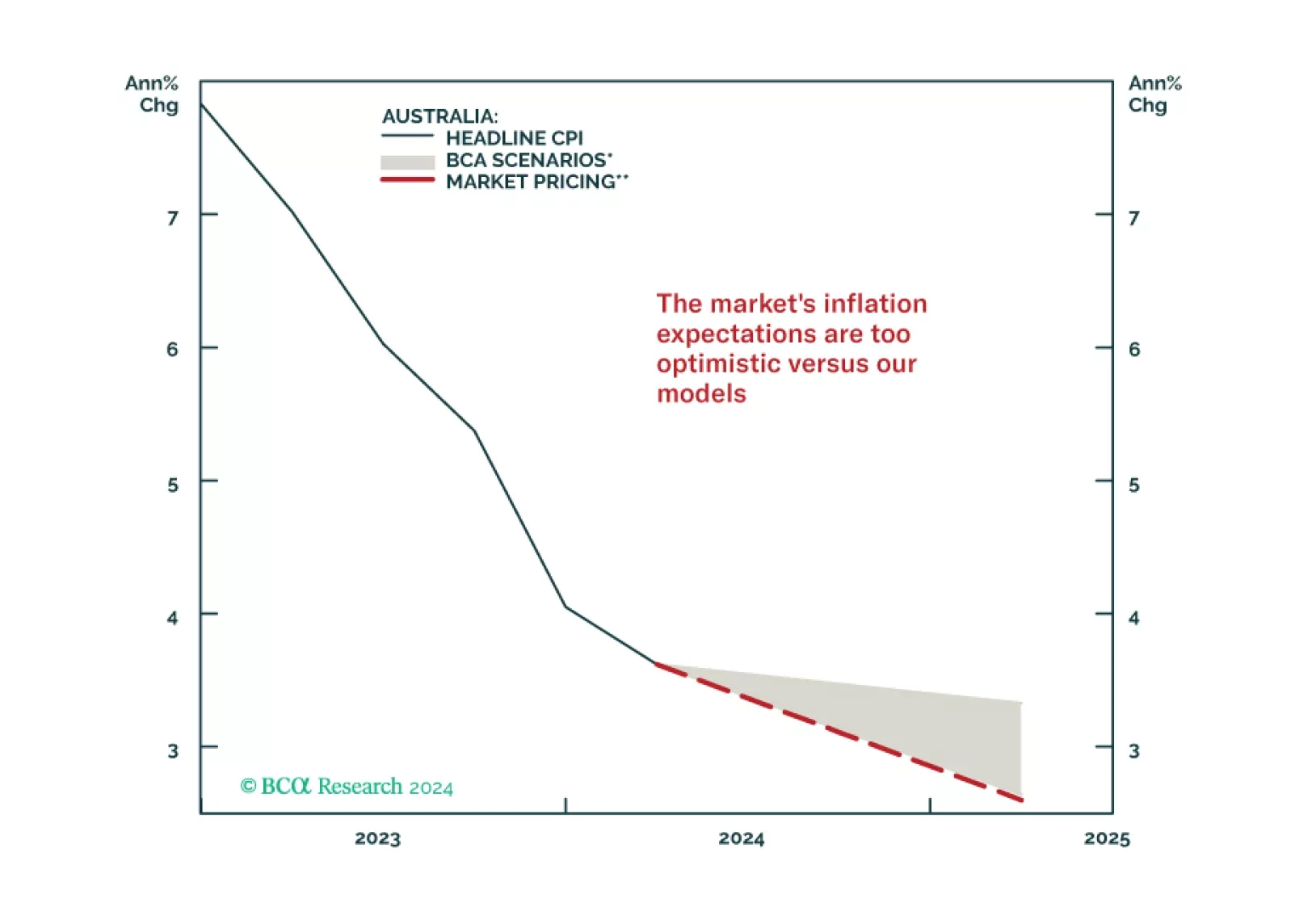

In light of this week’s RBA decision to keep policy on hold, we look at the best possible trades in fixed income markets. In our view, inflation-linked bonds, relative to nominals remain a good bet.

In this insight, we update our thinking on the recent BoJ move in terms of positioning for the yen and JGB yields.

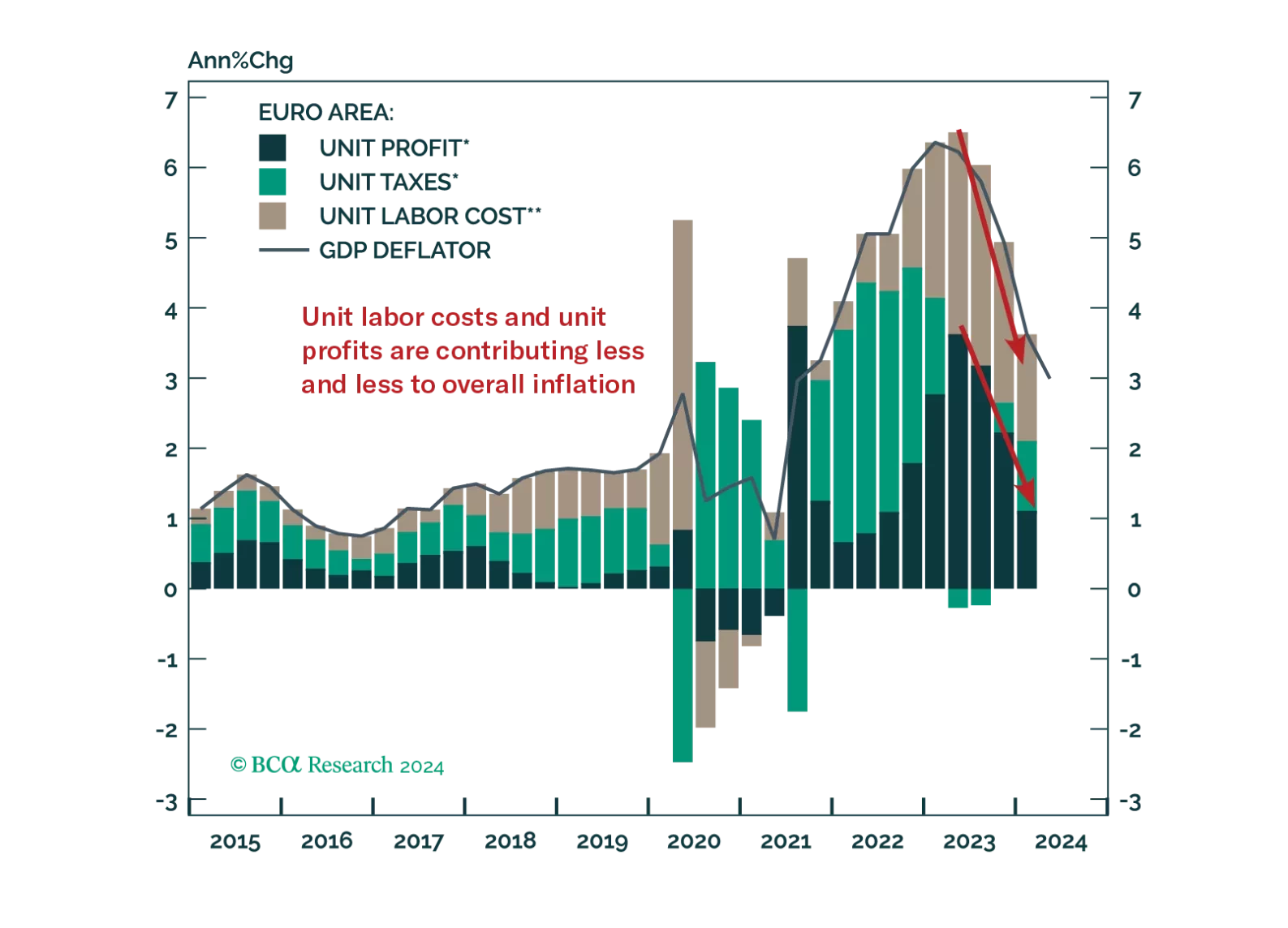

The ECB is now firmly in easing mode, even if it refuses to pre-commit to a specific rate path. What does this data dependency mean for the euro and European yields?

In this Insight, we revisit our "higher for longer" theme for the Reserve Bank of New Zealand, in light of the latest central bank meeting. In conclusion, we are inching towards a more dovish RBNZ ahead. Ergo, we recommend some fixed income and currency trades.

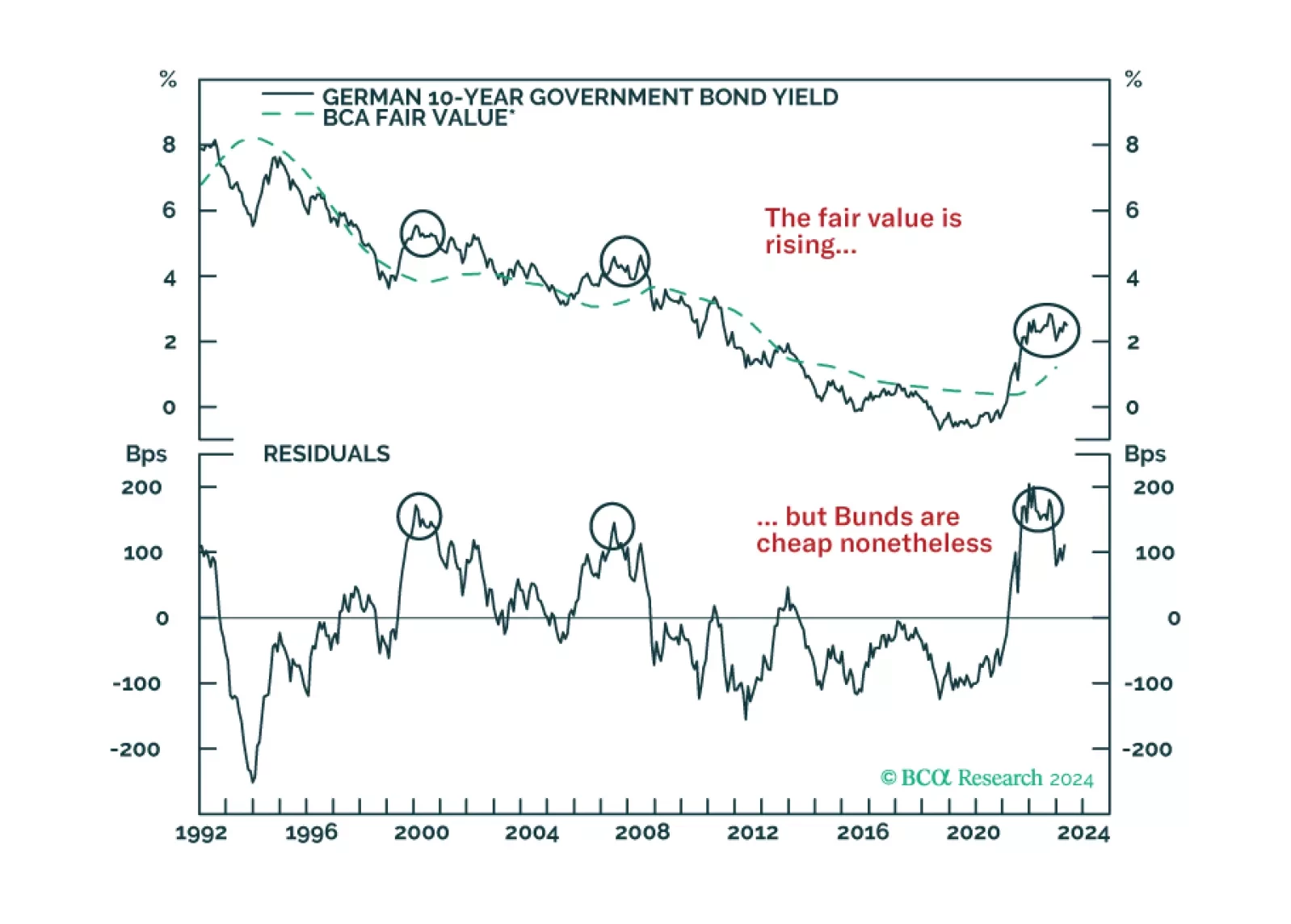

German Bunds have cheapened considerably, and the ECB is about to start cutting rates. Does this combination guarantee immediate profits from buying these bonds?

An update to our views on UK rates and currency following today’s Bank of England meeting.