Currencies

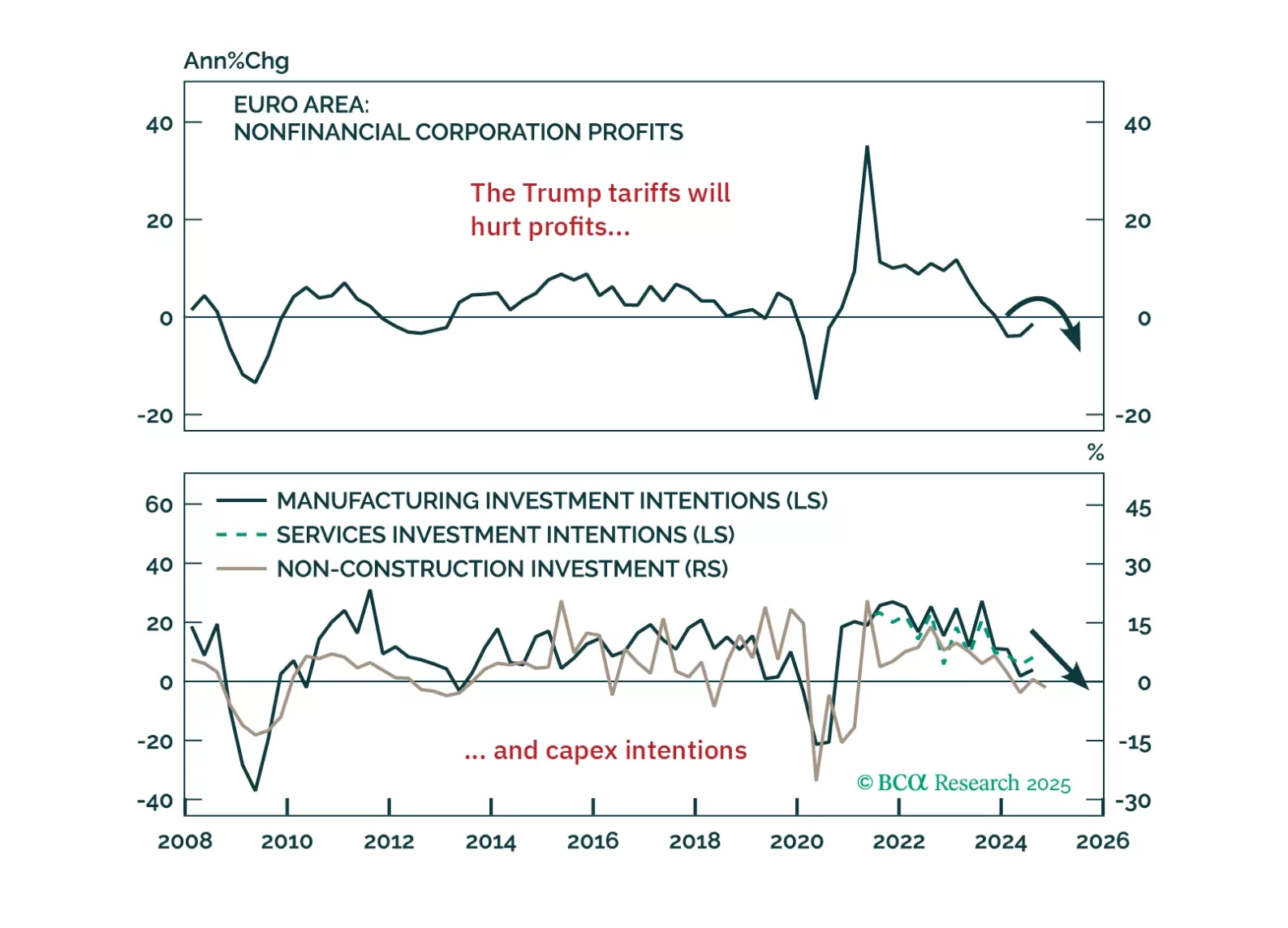

Trump’s tariff shock will push Europe into recession — but it’s also triggering a powerful integration response. In this report, we lay out the tactical case for staying defensive and the structural case for going long European assets when the dust settles.

This report looks at the FX implications of the Trump tariffs, and the review of our Q1 trades.

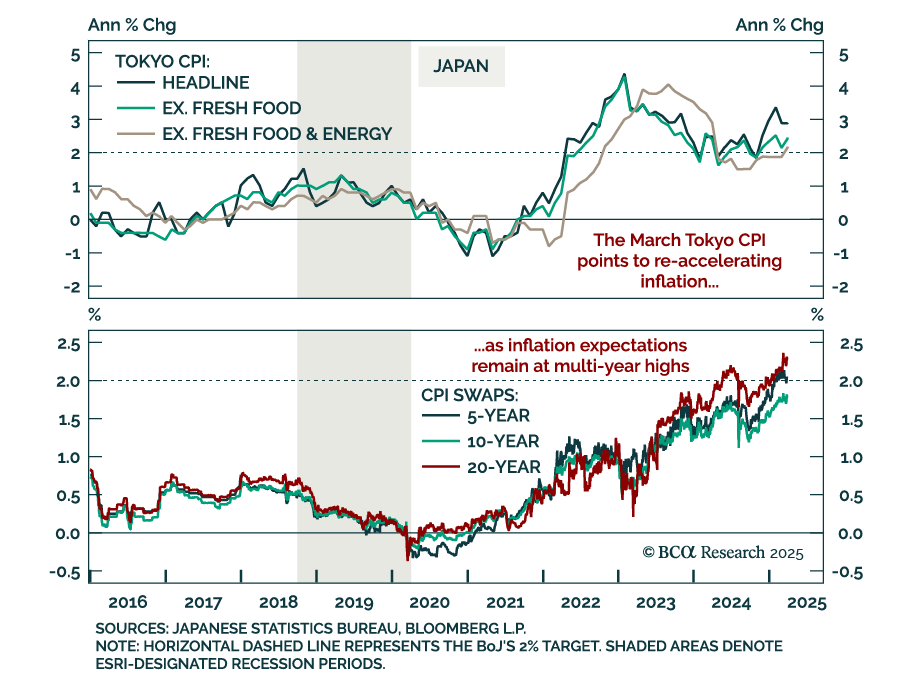

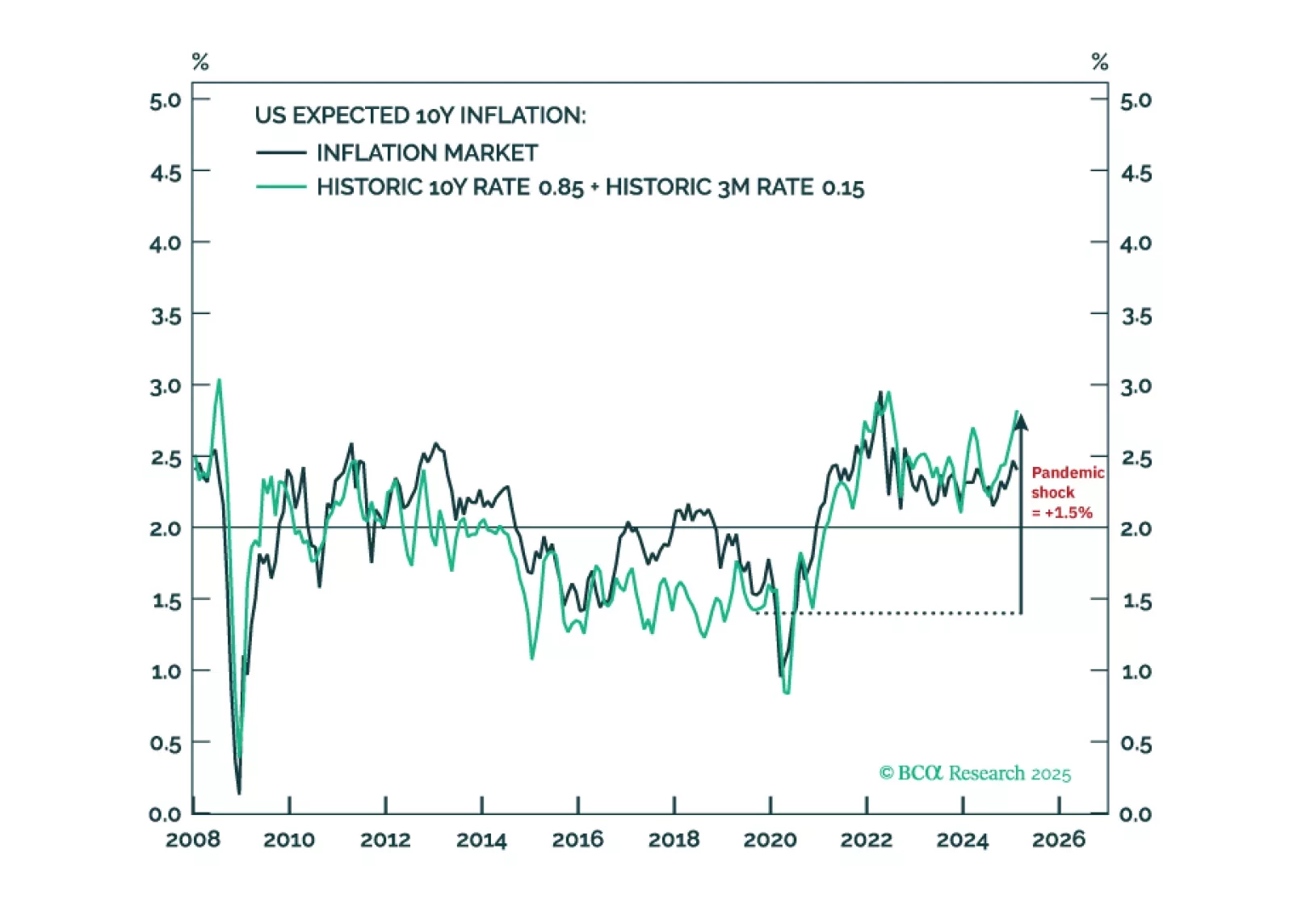

Tariffs will make a difficult job almost impossible. Hitting and sustaining a precise 2 percent inflation target is more about luck than judgement. It requires both the starting point for inflation expectations and any inflation/deflation shock to combine perfectly to 2 percent. While structural inflation expectations in the euro area and Japan could be close to 2 percent, those in the US and the UK will be stuck uncomfortably above 2 percent. We discuss the investment implications for rates and FX. Plus: gold is vulnerable to a tactical reversal.

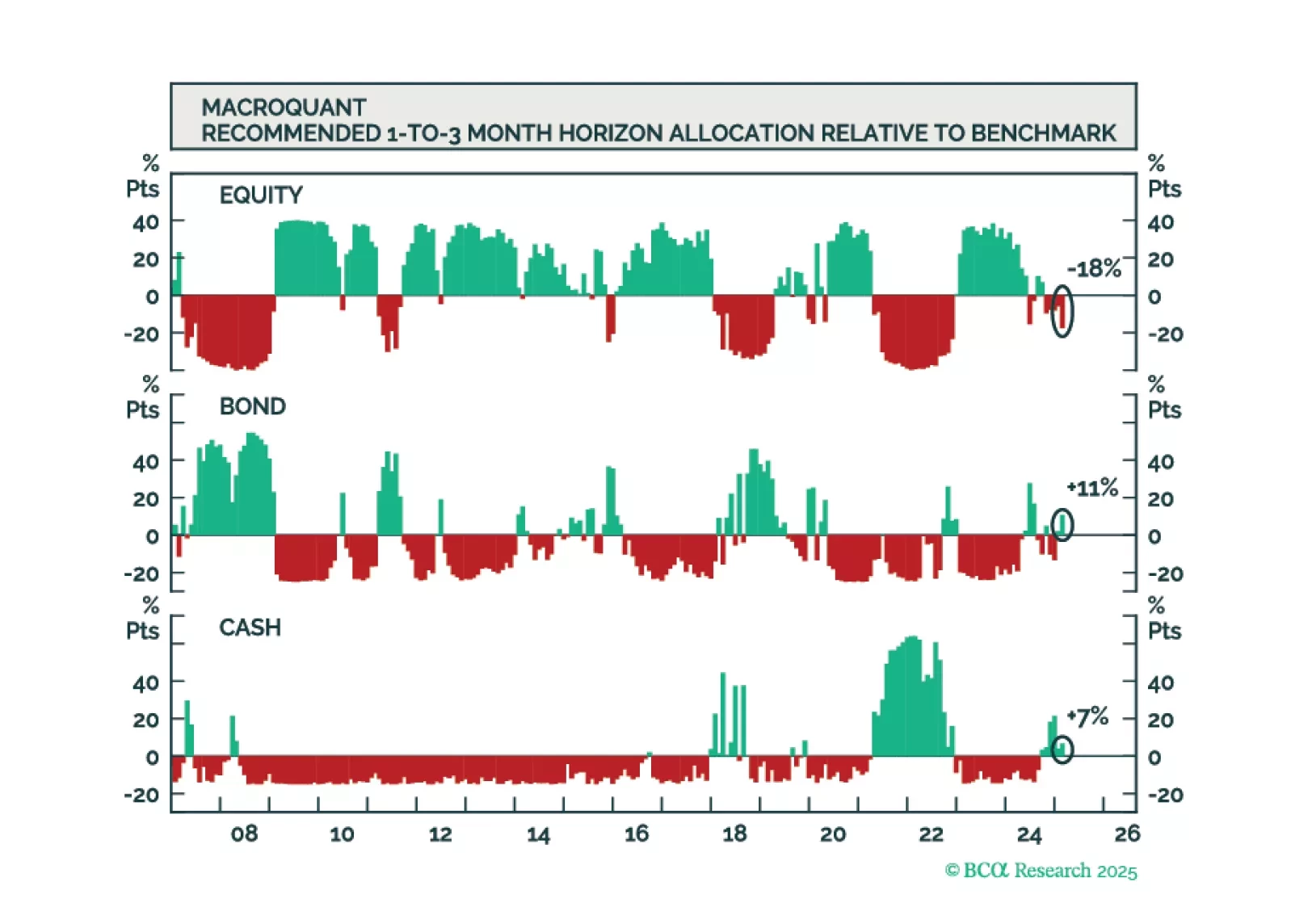

Going into April, MacroQuant recommends a modest underweight on stocks, offset by an overweight on bonds and cash. While MacroQuant is modestly bearish on stocks, we suspect that the downside risks to equities may be greater than what the model assumes.

Going into April, MacroQuant recommends a modest underweight on stocks, offset by an overweight on bonds and cash. While MacroQuant is modestly bearish on stocks, we suspect that the downside risks to equities may be greater than what the model assumes.

With economic headwinds building and fiscal dynamics shifting, bond markets are at a turning point. Our latest note outlines why German bund yields are set to decline and why UK gilts are poised to outperform — and how to position accordingly.

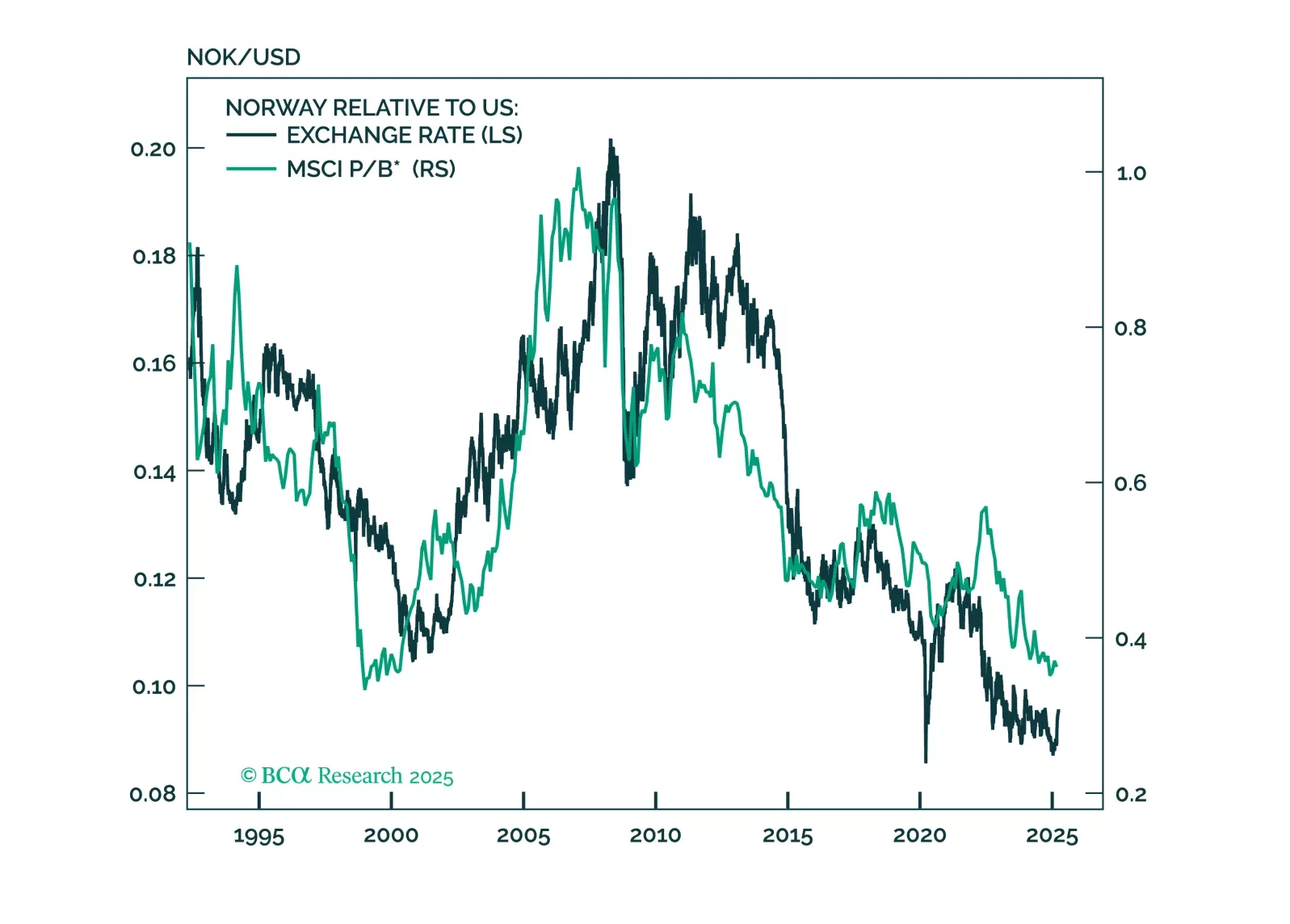

This report looks at investment implications, for Norwegian assets, given the recent meeting, from the Norges Bank.