Developed Countries

Soaring price pressures and tight labor market conditions – characterized by the difficulty employers are facing in finding qualified workers – are a recipe for robust wage growth (see Country Focus). With labor costs accounting for over 50% of sales…

BCA Research’s European Investment Strategy service concludes that BTPs have become attractive for long-term rather than short-term investors. The differences between the neutral rates across the Eurozone are the key factor limiting how far and how fast…

Executive Summary More Tightening To Come

More Tightening To Come

More Tightening To Come

In the following report we answer the most asked questions from our recent “Bear Market 2.0” webcast. Macroeconomic backdrop and inflation: While commodity prices falling, the wage-price spiral is in full force, implying that it will take many months to reach the level of PCE inflation palatable to the Fed. The Fed will continue to tighten monetary conditions until entrenched inflation reaches its target, which may take longer than the market expects. Earnings outlook: Q2-2022 results show that an earnings slowdown has already commenced and is bound to get worse over the next couple of quarters. However, earnings forecasts are still too optimistic and a slowdown in earnings growth is not yet priced in. Investment themes: We recommend topping up allocation to Tech as it benefits from rate stabilization. However, be judicious in your choices, staying away from the more cyclical areas, such as Hardware and Equipment, and Semiconductors. We are overweight Software and Services, which is dominated by profitable and stable growth companies. Bottom Line: We continue to recommend that investors remain patient and prudent in range-bound markets. Earnings growth is likely to deteriorate into the year end. Feature Last Monday, July 18, I hosted a webcast called “Bear Market 2.0.” A total of 675 people dialed in, and I was honored. The webcast generated a significant number of client questions which I aim to address in this weekly publication. Broadly speaking, questions fell under each of the three rubrics of the webcast: Macroeconomic backdrop, earnings outlook, and investment themes, with the latter generating the lion’s share of questions. In today’s report, we will discuss inflation and rates, earnings season results, potential S&P 500 targets, whether the S&P 500 rally is sustainable, and if it is a good idea to top up Tech. We will address remaining questions on Energy and Materials, and Semiconductor in the near future. And as always, we are looking forward to more questions! Macroeconomic Backdrop How do you reconcile your inflation outlook with an assumption that long yields may have peaked? In the “Fat and Flat” and “Adaptive Expectations” reports, we outline our view that the market’s focus is shifting away from concerns about inflation and the hawkish Fed toward worries about growth. Indeed, the 10-year rate has stabilized at 2.78% on fears of impending slowdown (Chart 1). How does this reconcile with our view that inflation is entrenched and broadening (Chart 2), especially in light of the recent pullback in energy and commodities prices? Chart 1Yields Are Stabilizing

Yields Are Stabilizing

Yields Are Stabilizing

Chart 2Inflation Is Entrenched

Inflation Is Entrenched

Inflation Is Entrenched

Even if energy and commodities prices are falling, the latest wage survey from the Atlanta Fed demonstrates wage growth is not letting up, and labor costs, at over 50% of sales as per NIPA accounts, are a more important component of the US corporate cost structure than the cost of energy. Inflation is embedded as, companies pass on wage increases to customers by increasing prices – and, voilà, the wage-price spiral is becoming pervasive. This dynamic implies the following: Even if inflation peaks over the next several months, it will take many months to reach the level of PCE inflation palatable to the Fed. After having mismanaged inflation over the past 18 months, the Fed will err on the side of tighter policy. In fact, in its official statement, the Fed has asserted that its commitment to bringing inflation to its 2% target is unconditional. Therefore, we are still in the early innings of the monetary tightening cycle (Chart 3), where elevated inflation coexists with slowing growth and range-bound long rates. Bottom Line: The Fed will continue to tighten monetary conditions until entrenched inflation reaches its target, which may take longer than the market expects. Chart 3More Tightening To Come

More Tightening To Come

More Tightening To Come

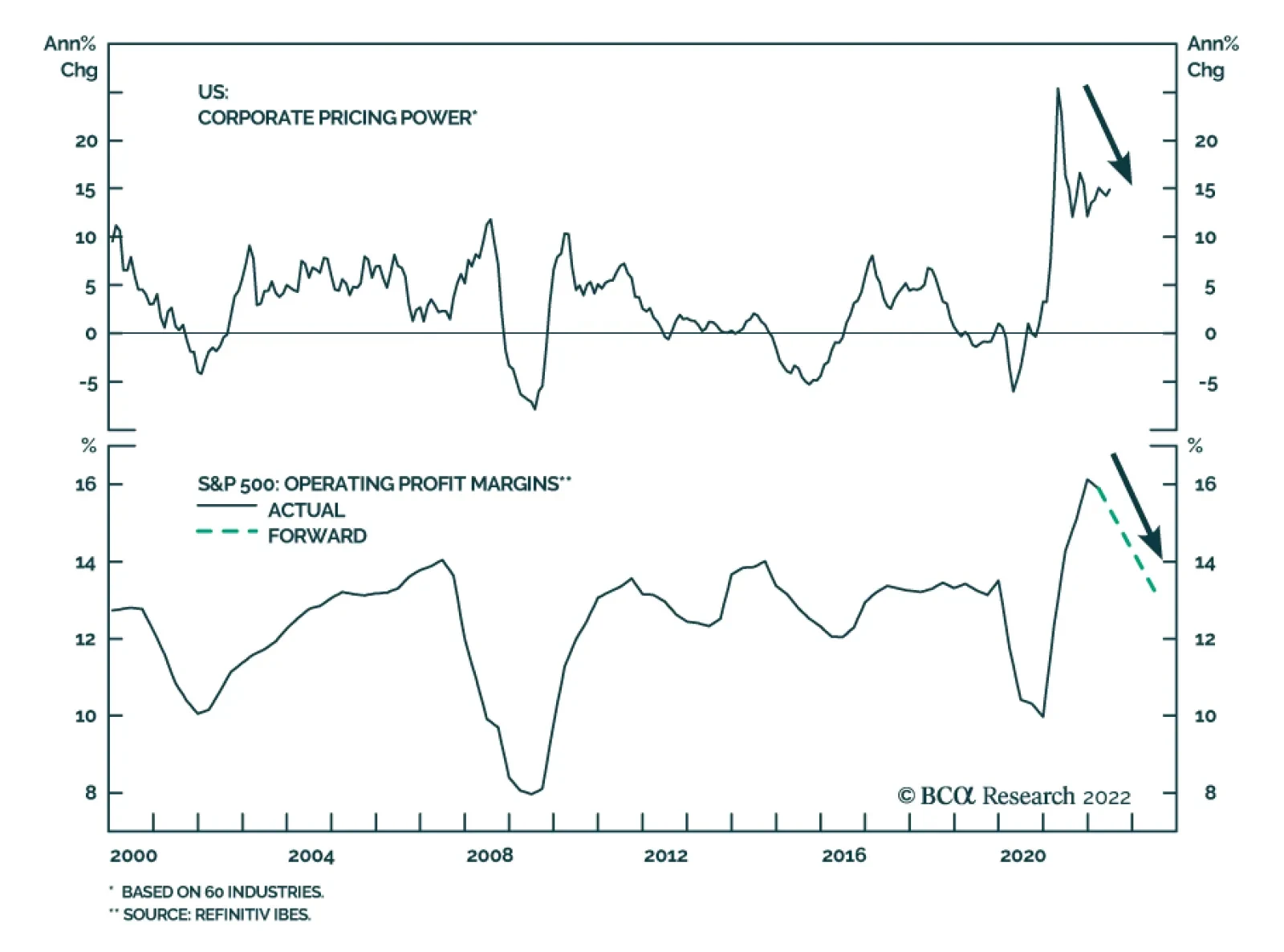

Earnings Outlook What are your takeaways from the earnings seasons so far? In the Daily Insight, which we published on July 21, we offer our initial reaction to the results. In short, so far earnings have been good, but margins are under pressure (Chart 4) from rising wages and fading pricing power (Chart 5). We have also heard quite a few negative comments from companies concerning the effects of inflation and rising costs, a strong dollar, and withdrawal from Russia. Some of the largest Technology companies announced slowdowns in hiring as they anticipate falls in demand. Forward guidance has also been concerning. Most companies talk about deteriorating economic conditions. Chart 4Margins Are Expected To Contract

Margins Are Expected To Contract

Margins Are Expected To Contract

Chart 5Pricing Power Turning

Pricing Power Turning

Pricing Power Turning

We are still convinced that street forecasts of earnings growing at about a 10% rate over the next 12 months and 11% into year-end (Table 1), despite ubiquitous negative corporate guidance, are unrealistically high. Even in this reporting season for Q2-22, earnings growth is -3%, excluding Energy. Table 1S&P 500 EPS: Actual And Expected

What Our Clients Are Asking: The Bear Market 2.0 Webcast Follow Up

What Our Clients Are Asking: The Bear Market 2.0 Webcast Follow Up

It is unlikely that, over the next several months, macro headwinds, such as slowing growth, the hawkish Fed, stubborn inflation, and rising wages will dissipate. There is little consensus among analysts on forecasts (Chart 6) and downgrades are likely. We take it a step further, and call an earnings recession in three to six months. Chart 6Analysts Have Little Confidence In Their Forecasts

Analysts Have Little Confidence In Their Forecasts

Analysts Have Little Confidence In Their Forecasts

Bottom Line: Q2-2022 results show that an earnings slowdown has most likely already commenced and is bound to get worse over the next couple of quarters. However, earnings forecasts are still too optimistic and a slowdown in earnings growth is not yet priced in. Do you think that the slowdown in earnings might trigger multiple expansion? Earnings contraction, everything else equal, translates into multiple expansion, as the denominator of the fraction gets smaller. For example, according to our back-of-the-envelope estimates, earnings contracting by 10% will increase the forward multiple from the current 16x to 19x. Therefore, the key question here is how likely is it that everything else will indeed stay equal, as opposed to the market selling off in line with earnings? Multiples will expand if the market is able to see past negative earnings growth, identifying a catalyst for an imminent rebound. That was the case in 2020 as investors anticipated earnings bouncing back helped by easy monetary and fiscal policy, and COVID receding. What will be a catalyst for earnings rebound in, say, 2023? We can only speculate but one of the potential reasons for faster earnings growth is perhaps normalization of growth outside of the US: A weaker dollar, peace in Ukraine, resolution of the energy crisis, or ultra-loose monetary and fiscal policy in China. At home, the anticipation of a soft landing and a more dovish monetary policy coupled with a positive real wage growth boosting consumers’ spending power may be sufficient to reassure investors that earnings growth turning positive is imminent. However, all of these developments are probably months away. And we expect the market to sell off if earnings growth disappoints. Where do you see the S&P 500 by the end of the year? Broadly speaking, BCA Research does not provide targets but rather aims to offer insights into market trends. However, in the “Is Earnings Recession In The Cards?” report, we presented a matrix outlining different scenarios of earnings growth vs. forward multiples to arrive at a potential range of the outcomes for the index. We assume that the forward multiple stays at 16x, as the multiple contraction stage of the bear market is likely completed, but there is still no clear catalyst for earnings rebound. We will approximate CY 2022 results using the Next Twelve Months Matrix (Table 2). Table 2The S&P 500 Price Target Scenarios

What Our Clients Are Asking: The Bear Market 2.0 Webcast Follow Up

What Our Clients Are Asking: The Bear Market 2.0 Webcast Follow Up

We can distill the matrix into three likely scenarios: Earnings growth delivered by companies in line with analyst expectations of 11% over the six months; flat earnings (0% growth) broadly in line with the forecast based on our earnings model; and the worst-case scenario of a severe earnings contraction of -10% into year-end. We assign 25% to both extreme cases and about 50% to earnings staying flat for the next six months (earnings recession commencing in 2023). Best-case scenario: Earnings grow into year-end by 11%, and by 9.7% over the next 12 months. In that case, the S&P 500 will end the year at 3,837 or 3% off the current level. This is what is being priced in. Most likely scenario: Earnings growth trends to zero by the end of the year with the S&P 500 hitting 3500 or downshifting roughly 10% from here. Worst-case scenario: Earnings contract by 10%, and with the multiple staying at 16x, the S&P 500 price target will be 3287 or about 17% lower than today. With “E” falling so much, perhaps the multiple expands to 17x, in which case the market will fall “only” 11% from here. Bottom Line: We expect flagging earnings to cause another leg of the bear market, which is likely to be 5-10% into year-end, and perhaps another 5-10% in 2023. Equity Market Outlook And Key Investment Themes Are investors capitulating? Are we near or even past the bottom? The decline in oil and food prices and the easing of supply-side bottlenecks have alleviated market worries about US inflation. This, coupled with oversold risk assets, and apparent extreme pessimism in investor sentiment, has resulted in the S&P 500 rebounding 8% from its June lows. Sectors that have sold off the most over the past six months have bounced back the hardest (Chart 7). Naturally, the question that is top of mind for investors is whether this rebound is sustainable. Should they add beaten-down cyclicals to their portfolios to partake in the rally? Of course, no one can predict what Mr. Market will do with 100% certainty but here are some thoughts: Chart 7Sector Performance Overview

What Our Clients Are Asking: The Bear Market 2.0 Webcast Follow Up

What Our Clients Are Asking: The Bear Market 2.0 Webcast Follow Up

Positives Many risk assets are severely oversold, and for long-term investors, an entry point is attractive valuation-wise. So far, many investors find earnings season results somewhat encouraging: Netflix soared on what its CEO Hawkins called “less bad results.” Multiples have contracted and priced in most of the primary effects of high inflation and rising rates. Negatives The Fed is determined to extinguish inflation, and this hiking cycle may end up much longer and steeper than the market is pricing in. We do not anticipate monetary easing in the first half of 2023. Financial markets are currently underrating the risk of a seriously hawkish Fed. Economic growth is slowing, and consensus forecasts of earnings growth are still overly optimistic. Earnings contraction over the next several quarters is likely but is certainly not priced in, and disappointment may rock markets. The catalyst for this summer’s rebound is two-fold: The market is celebrating the end of inflation worries and is rebounding from severely oversold conditions. Black swan “generators” such as China and Russia, may have more surprises in stock (Table 3). We continue to stick to “fat and down” expectations for the equities outlined in the “Adaptive Expectations” report and anticipate a range-bound market where relief rallies are alternated with pullbacks, mostly triggered by growth disappointments and realizations that the Fed has dug in its heels and is unlikely to let up anytime soon. The “down” leg will ensue if earnings contract. Yet we recommend investors take a granular approach to industry selection and start tilting portfolios away from assets that benefit from rising inflation, such as Energy and Materials, towards the “growthy” assets that benefit from rate stabilization and falling growth. We picked up on the turning point and upgraded Growth to overweight in early July, funding it from Value. Table 3Scorecard

What Our Clients Are Asking: The Bear Market 2.0 Webcast Follow Up

What Our Clients Are Asking: The Bear Market 2.0 Webcast Follow Up

Bottom Line: We consider the recent rebound in US equities a bear market rally, and don’t believe that it is sustainable. The Fed and the stock market are on a collision course – easier financial conditions will make the Fed even more aggressive. Is it time to buy Tech? As we have highlighted in the “Are We There Yet?!” report back in January, Tech’s worst performance is two to three months prior to the first rate hike, and the rebound is two to three months after the beginning of the monetary cycle. The slump and a recent rally are perfectly in line with history (Chart 8). Rates have stabilized and “growthy” Tech has pounced (Chart 9). Another issue that was holding the sector back earlier in the year was a slowdown in demand for Tech investment (Chart 10). Recently, business demand for Tech has picked up. However, US consumer spending on Tech is falling, as demand for consumer goods, pulled forward by the pandemic, is fading (Chart 11). Therefore, we need to be judicious in our selection of technology stocks. Chart 8Tech Performance During A Hiking Cycle

What Our Clients Are Asking: The Bear Market 2.0 Webcast Follow Up

What Our Clients Are Asking: The Bear Market 2.0 Webcast Follow Up

Chart 9Technology Rebounded On The Back Of Yields Peaking

Technology Rebounded On The Back Of Yields Peaking

Technology Rebounded On The Back Of Yields Peaking

Chart 10Corporate Demand For Tech Has Picked Up…

Corporate Demand For Tech Has Picked Up…

Corporate Demand For Tech Has Picked Up…

We reiterate our overweight in Software and Services, which is least exposed to consumer demand. Our thesis is that this industry group represents “defensive growth” thanks to the key trends of digitization of the US economy and migration to cloud. Spending on digitization and the cloud are pervasive across non-tech companies and capture a large swath of corporate America by both size and industry. Also, software and services companies tend to have stable earnings growth throughout the cycle, as software improves productivity and cuts costs (Chart 12). Chart 11...But Consumer Spending Slowed

...But Consumer Spending Slowed

...But Consumer Spending Slowed

Chart 12Software Is Defensive Growth

Software Is Defensive Growth

Software Is Defensive Growth

We are underweight more cyclical Hardware and Equipment, and Semiconductors industry groups as they are more exposed to the slowing economy and the flagging demand for hardware and chips. We will take a close look at the Semiconductor Industry Group in the near future. Bottom Line: We recommend topping up allocation to tech as it benefits from rate stabilization. However, be judicious in your choices, staying away from the more cyclical areas, such as Hardware and Equipment, and Semiconductors. We are overweight Software and Services, which is dominated by profitable and stable growth companies. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com Recommended Allocation Recommended Allocation: Addendum

What Our Clients Are Asking: The Bear Market 2.0 Webcast Follow Up

What Our Clients Are Asking: The Bear Market 2.0 Webcast Follow Up

Executive Summary The ECB finally exited negative interest rates last week. In exchange for higher rates, the doves received an ambitious anti-fragmentation tool, the TPI. The ECB deposit rate is likely to reach between 1% and 1.5% by the summer of 2023. The ECB’s number one problem remains the widely different neutral rates across the Eurozone’s largest economies. Our r-star estimates suggest that the German neutral rate is significantly above that of Spain, Italy, and even France. This divergence in r-star means that the TPI will be activated, but its presence alone is not enough to tame the peripheral bond markets when the ECB hikes rates. While the near-term remains fraught with risks, BTPs are increasingly attractive for long-term investors. The TPI also creates a bullish long-term backdrop for the euro. Many R-Star In The European Sky

ECB Policy: One Size Doesn’t Fit All

ECB Policy: One Size Doesn’t Fit All

Bottom Line: Diverging neutral rates across the Eurozone’s main economies will impair the ECB’s ability to normalize interest rates over the next twelve months without also activating the new anti-fragmentation tool, the TPI. BTPs have become attractive for long-term rather than short-term investors. Last week, the European Central Bank (ECB) increased interest rates by 50bps, the first hike in eleven years and the third time in its history that it has tightened policy by such a large increment. In exchange for this abrupt end to negative interest rates, the doves on the Governing Council (GC) extracted the creation of the Transmission Protection Instrument (TPI), a new facility designed to limit fragmentation risk on sovereign bond yields in the Eurozone. These two moves raise three key questions: Will the ECB continue to increase rates this aggressively in the coming months? Have peripheral spreads peaked? Will the threat of TPI buying be enough to put a ceiling on spreads, or will the ECB actually need to activate the program in the coming months? To answer these questions, we evaluate where r-star (the neutral real rate of interest) stands in the four largest Euro Area economies. While there is scope for the ECB to push policy rates higher, the wide differences in r-star across European nations indicate that the TPI will need to be activated to stabilize peripheral bond markets, most importantly, Italian government debt. This makes BTPs attractive for long-term investors, although near-term volatility will remain elevated as the markets test the ECB’s resolve. What Happened? Related Report European Investment StrategyLooking Beyond Europe’s Inflation Peak In terms of interest rates, the most important conclusion from last’s week policy meeting was that forward guidance has been abandoned. The ECB is now fully data dependent, and each policy meeting will be a live one. Another rate hike is certain for the September meeting, ranging from 25bps to potentially 75bps if the ECB wishes to further “front-load” tightening. The single guiding principle will be the outlook for inflation. Chart 1Incoming Inflation Peak

Incoming Inflation Peak

Incoming Inflation Peak

We do expect inflation to peak soon in the Eurozone, mostly because of the decline in the commodity impulse and slowing food inflation (Chart 1). Additionally, the one-month impulse of our Trimmed-Mean CPI is weakening. However, as of June, headline and core inflation stand at 8.6% and 3.7%, respectively. Inflation is unlikely to slow enough by the September meeting to prompt the ECB to forecast inflation falling below its 2% target by 2024. In this context, our base case remains that the GC will opt for a 50bps hike in September. Beyond September, we expect the ECB to revert to 25bps rate hikes and the policy rate to settle between 1% and 1.5% by the summer of 2023, which is broadly in line with the current pricing of the €STR curve (Chart 2). We are somewhat less hawkish than the market for the month of October, because we expect inflation to roll over this fall. Moreover, the European economy continues to decelerate, as highlighted by the declines in the ZEW growth expectations and the PMIs (Chart 3). This deceleration will allow the ECB to revise down its inflation outlook over time. Chart 2Appropriate Pricing

Appropriate Pricing

Appropriate Pricing

Chart 3Growth Is Slowing

Growth Is Slowing

Growth Is Slowing

The announcement of the TPI was the other crucial development from the last ECB meeting. The TPI was unanimously supported. In addition, its asset purchases will be unlimited, and the GC will have much discretion with respect to its implementation. These are three important features that give it ample credibility. However, the program has yet to be activated. Chart 4PEPP Reinvestment Doing Little

PEPP Reinvestment Doing Little

PEPP Reinvestment Doing Little

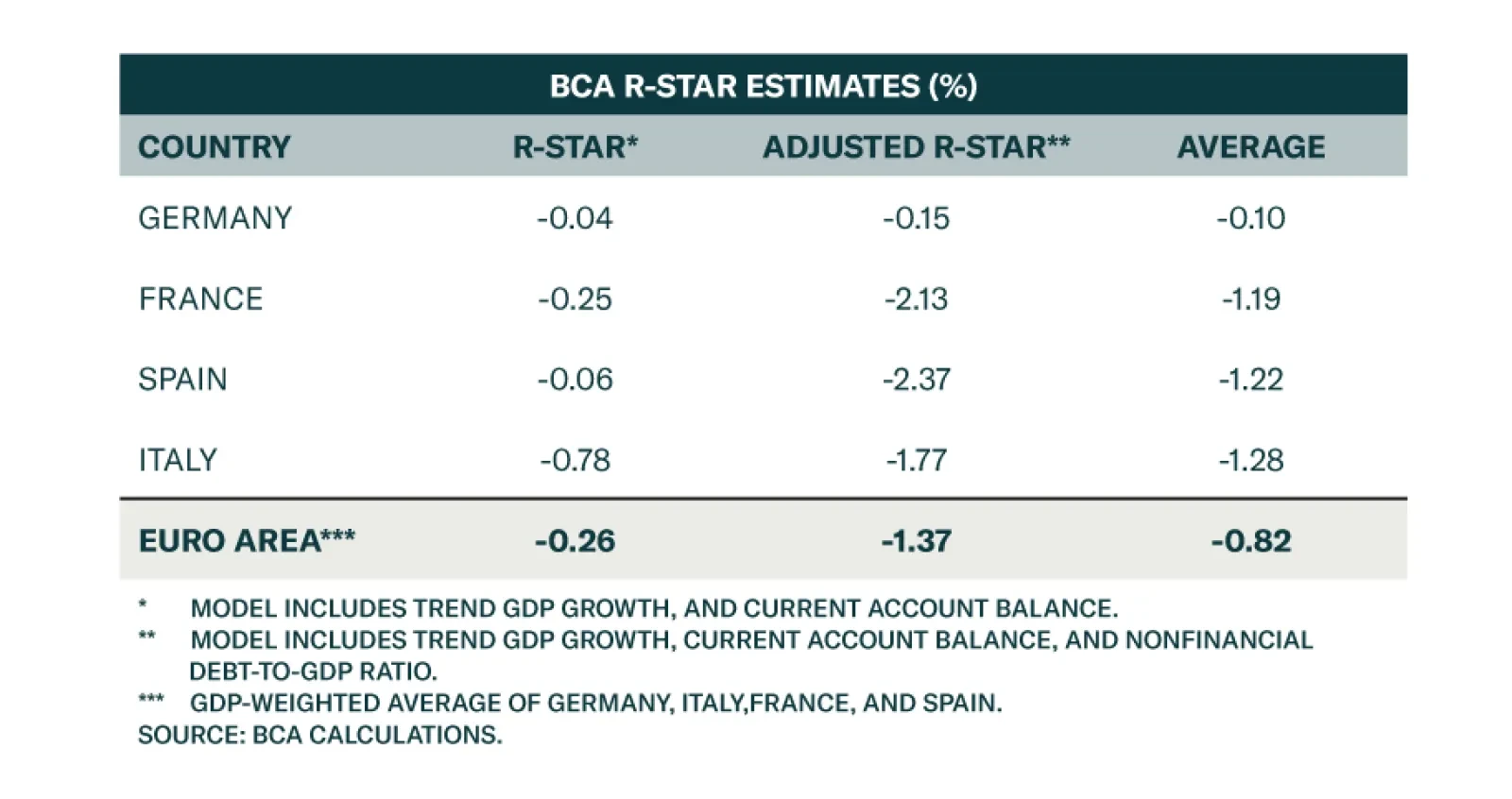

We do not share the optimism of the GC members who believe that the TPI’s existence alone will narrow peripheral spreads without the ECB having to purchase a single bond. The market will have to figure out what the GC deems as “unwarranted” and “disorderly” moves, especially in a context in which the Draghi government has collapsed and Italy’s commitment to reform will be challenged exactly as interest rates begin to rise. Moreover, the flexible re-investment of PEPP redemptions has not prevented BTP/Bund spreads from widening (Chart 4). As a result, we expect the market to test the ECB’s resolve over the coming weeks, which is likely to result in volatility and wider spreads until the TPI is activated. Bottom Line: Last week’s ECB meeting was a seminal moment. The ECB not only abandoned eight years of negative rates in one go, but it also implemented an ambitious program that aims to restrict peripheral spreads, albeit with some near-term volatility. European policy rates are set to rise to between 1% and 1.5% by the summer of 2023. In Search Of A Neutral Rate During Thursday’s press conference, President Christine Lagarde refused to respond to a question about the neutral rate of interest in Europe. We have sympathy for her predicament. The ECB’s biggest problem is that there is not one neutral interest rate for the entire euro area, but nineteen individual neutral rates for each Eurozone country, with wild differences among them.1 The differences between the neutral rates across the Eurozone are the key factor limiting how far and how fast the ECB may increase rates. It is also the main reason why the ECB resorts to an alphabet soup of non-interest rate policy measures (APP, PEPP, LTRO and, now, TPI) to maintain appropriate monetary conditions across the bloc. But exactly how wide are the differences between the neutral rates? To answer this question, we expand on the methodology developed by Holston, Laubach and Williams (HLW) from the San Francisco Fed to estimate the neutral real interest rate – or “r-star” - in Germany, France, Italy, and Spain. These are the four largest economies in the Euro Area, accounting for 70% of its GDP. Specifically, we run regressions between the real interest rates in those countries versus trend GDP growth and current account balances, which approximates the savings-investment balance. Mimicking the HLW methodology, the inflation expectations used to extract real interest rates from nominal short rates reflect an adaptative framework whereby inflation expectations are a function of the ten-year moving average core CPI. Our methodology produces estimates of r-star that range from 0% in Germany, to -0.8% in Italy, or a GDP-weighted average of -0.3% for the Eurozone (Table 1). When incorporating last week’s ECB rate hike, Europe’s real deposit rate falls to -1.2% if we use the smoothing procedure from HLW to compute inflation expectations, or -3.7% if we use current core CPI. In either case, policy remains accommodative for everyone. Table 1Many R-Star In The European Sky

ECB Policy: One Size Doesn’t Fit All

ECB Policy: One Size Doesn’t Fit All

We also ran a second set of estimates for r-star, which includes total nonfinancial debt-to-GDP. The logic reflects the notion that adverse debt dynamics was a key force behind the 2011/12 European sovereign debt crisis, which obligated the ECB to reverse course after pushing up the repo rate twice in 2011. Moreover, heavy debt loads not only constrain the ability of various countries to withstand higher rates, but they are also linked to misallocated capital and are therefore likely to depress trend GDP growth over time compared to countries with lighter debt loads. This adjustment changes the picture considerably. While Germany’s real neutral rate of interest remains around 0%, those of Italy and Spain plunge to -1.8% and -2.4%, respectively. France has also experienced a large decline in its r-star to -2.1% in response to the heavy debt load carried by its private and public sectors. Using this method, the GDP-weighted Euro Area r-star falls to -1.4% (Table 1). So which version of the model is more accurate? We believe the most realistic estimate for r-star in each of the four countries is the simple average of both the unadjusted and the debt-adjusted r-star. This implies that the inflation-adjusted neutral rate is close 0% in Germany, -1.2% in France, -1.2% in Spain and -1.3% in Italy (Table 1). Are those results consistent with reality? A country-by-country evaluation suggests that this ranking is correct. To arrive at this judgment, we evaluated each country based on the following four dimensions: Private sector debt accumulation since 2010. If policy is particularly easy for one country, the private sector will be incentivized to take on debt at a more rapid pace than if monetary conditions were tighter. House price appreciation since 2010. Housing is the part of the economy most sensitive to monetary conditions. Larger real estate price gains will materialize in economies where monetary policy is particularly loose. Profit growth since 2010. Easy monetary policy will subsidize corporate profitability, either through faster domestic activity or a cheaper exchange rate (or both). Unemployment rate. The unemployment rate is a crude measure of slack in the economy. An easier policy setting in one country will reduce the unemployment rate compared to a country where policy rates are high relative to r-star. Germany Chart 5Loosest Monetary Conditions In Germany

Loosest Monetary Conditions In Germany

Loosest Monetary Conditions In Germany

Germany exhibits all the evidence of monetary policy being much more accommodative for that country than the other four countries, for the following reasons: Since 2010, German private debt has been expanding much faster than the average of the four countries (Chart 5, top panel). Germany is experiencing the fastest house price appreciation (Chart 5, second panel). Germany’s profits have grown much faster (Chart 5, third panel). Germany’s unemployment rate stands at only 3%, compared to an average rate of 8% for the four nations together (Chart 5, bottom panel). France Chart 6French Monetary Conditions Are Tighter

French Monetary Conditions Are Tighter

French Monetary Conditions Are Tighter

France is a mixed bag. Monetary policy has been easy for France, but the French economy lags Germany on three of the four aforementioned dimensions: Since 2010, French private debt is growing at the fastest pace of the four economies studied, outpacing even that of Germany (Chart 6, top panel). While French house prices have grown slightly faster than the average of the four nations, they lagged German real estate prices (Chart 6, second panel). While French profits have also bested the average of the four nations, they nonetheless trail German profits (Chart 6, third panel). France’s unemployment rate is in line with the average of the four countries under observation (Chart 6, bottom panel). Spain For most of the period following 2010, Spain has suffered from the scars of the disastrous deleveraging that was required in the wake of the sovereign debt crisis. Its trend growth collapsed, and the ECB’s common policy was never as accommodative as it was for its northern neighbors. However, in recent years, the Spanish economy seems to be catching up, a result of the impact of previous structural reforms and the improved competitiveness brought about by collapsing real unit labor costs: Chart 7Spain Still Grapples With Problems

Spain Still Grapples With Problems

Spain Still Grapples With Problems

Since 2010, Spanish private debt has contracted by 20% compared to a 33% expansion for the European average (Chart 7, top panel). Spanish real estate prices have also lagged far behind those of the other countries put together (Chart 7, second panel). However, since 2015, Spanish house prices have begun to recover, and they are now moving at the same pace as the Euro Area average. Spanish profit growth remains weak compared to the average of the four countries studied in this report (Chart 7, third panel). The Spanish unemployment continues to tower at 13%, well above the average of the four largest Euro Area economies (Chart 7, bottom panel). Italy Italy has a similar profile to that of Spain. While its worst performance is solidly in the rear-view mirror, the recent period of easy monetary policy has allowed for some recovery. Nonetheless, Italy still lags far behind other Eurozone countries, which suggests that policy in Italy is not nearly as accommodative as in the rest of the Eurozone. Chart 8Italy Shows Little Improvements

Italy Shows Little Improvements

Italy Shows Little Improvements

Burdened by very large nonperforming loans, the Italian banking sector has been unable to provide adequate credit to the Italian private sector, which already had a limited appetite for debt. As a result, since 2010, Italian private credit has lagged far behind the European average (Chart 8, top panel). Italian real estate prices have not recovered meaningfully from their contraction between 2011 and 2019. Consequently, Italian housing prices lag substantially behind the average of the largest Euro Area countries (Chart 8, second panel). Italian profits remain weak (Chart 8, third panel). While not as elevated as the Spanish unemployment rate, at 8%, Italy’s rate is comparable to the four-country average (Chart 8, bottom panel). Generalizations These observations about individual countries confirm that Germany’s r-star is significantly higher than those of Spain and Italy. When compared to France, the German r-star is also higher, but the gap is much narrower than that between Germany and the two southern nations. The recent ECB Euro Area Bank Lending Survey confirms that France’s r-star is well below that of Germany. French lending standards are tightening as fast as those in Italy (Chart 9). In effect, France’s heavy private sector debt load is proving to be a burden as the ECB begins to tighten policy, which implies a lower French r-star. Chart 9Lending Standard Are Tightening Most In France And Italy

ECB Policy: One Size Doesn’t Fit All

ECB Policy: One Size Doesn’t Fit All

Bottom Line: Among the four largest economies in the Eurozone, a modeling exercise based on the HWL approach reveals that there is a large gap in neutral real interest rates, with Germany on one side around 0%, and Italy, Spain, and even France on the other side with r-star estimates ranging between -1.2% and -1.3%. A survey of current economic activity in these four nations confirms the results from the modeling exercise. Investment Implications The main consequence of the differing r-star across the Eurozone is that the ECB will need to remain an active player in the sovereign bond market. The German, Dutch, and Baltic economies are overheating, and policy needs to be tightened. This means that the ECB will continue to hike rates over the coming months. However, it cannot raise rates much more before they become problematic in Italy, Spain, and even France. Thus, the ECB will activate the TPI in the coming months in order to ease monetary conditions in those economies relative to the stronger group by limiting policy-induced increases in bond yields. In fact, using the r-star estimates adjusted for the debt-to-GDP ratios, the ECB would need to absorb roughly 30% of the Italian total debt to bring Italy’s r-star closer to Germany’s levels. This will not happen, which means that in the foreseeable future, Italy will not be able to withstand the levels of interest rate needed to cool down the German economy. Nonetheless, the TPI can help the ECB in fine-tuning monetary conditions across the Eurozone as it hikes policy rates. For now, Italian bonds are likely to remain volatile until the TPI is activated, especially considering the political situation in Italy, where the outlook for structural reform seems compromised by political uncertainty. This volatility will result in the activation of the TPI before year-end. Once the TPI is activated, BTP/Bund spreads are likely to move back toward 100bps, the level historically consistent with the ECB’s involvement in the sovereign debt market during the APP/PEPP era. The activation of the TPI will also be a positive development for the European corporate bond market, especially investment grade bonds. In last week’s post-conference press release, the ECB revealed that the TPI will also be able to buy private issuer securities. Thus, the ECB is likely to return as a potential buyer in this market. Moreover, investment grade bonds already price in a European recession and therefore offer a large value cushion with 12-month breakeven spreads trading in their 79th historical percentile (Chart 10). We especially like European investment grade corporate bonds relative to US ones on a USD-hedged basis. Relative valuations are in favor of Europe, and the ECB is not tightening policy as much as the Fed. Related Report European Investment StrategyTo Parity And Beyond The euro will ultimately benefit from the activation of the TPI. The narrowing of both sovereign and corporate spreads resulting from the program represents a very bullish development for EUR/USD (Chart 11), especially because the ECB will likely sterilize the bonds purchased under the program (i.e. the ECB’s balance sheet will not expand because of the TPI). The TPI will also allow the ECB to deliver higher interest rates, which further supports the euro. Nonetheless, we continue to see substantial (roughly 20%) odds of a break below parity in the near-term, especially if wider BTP-Bund spreads in the coming three months are the key catalyst behind the TPI’s activation. Chart 10Eurozone IG Debt Is Attractive

Eurozone IG Debt Is Attractive

Eurozone IG Debt Is Attractive

Chart 11The TPI Will Help The Euro, Eventually

The TPI Will Help The Euro, Eventually

The TPI Will Help The Euro, Eventually

Finally, last week’s policy development is unlikely to affect the absolute performance of European stocks. European equities remain mostly impacted by the fluctuations in global stock prices and the shifting probability of a recession in Europe this winter in response to the evolving energy crisis on the continent. European equities are inexpensive, and the probability of a recession is declining as a result of the resumption of natural gas flows from Russia. Crucially, the broadening trend toward coal utilization this winter and the growing list of deals that Europe is striking to secure non-Russian gas supplies suggest the impact of Russian cutoffs this winter could be more limited than once feared. Moreover, we expect European governments to hose their economies with stimulus if a crisis does emerge, which would both limit the depth of the crisis and prompt a rapid rebound in activity once winter ends. However, the inattention of the ECB to recession risks suggests that European equities could lag US equities in the near term. Bottom Line: The differences in r-star across Europe mean that the ECB will be forced to activate the TPI before year-end in order to hike interest rates further. Practically, this means that medium- to long-term investors should overweight Italian bonds at the current level of spreads. Short-term investors should remain on the sidelines; the political situation in Italy is still dangerous, and speculators are likely to test the ECB’s resolve. This also means that the euro is attractive as a long-term play, but it still carries large left-tail risk in the near term. While investors should favor European investment-grade bonds in USD-hedged terms relative to the US, European equities are likely to continue to suffer headwinds compared to US stocks. Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Footnotes 1 In fact, it will soon be 20 r-star since Croatia will join the euro on January 1, 2023.

The ECB is in somewhat of a pickle. Prices are surging, which has prompted the central bank to start its rate hike cycle with a bang on Thursday – raising rates by an outsized 50bps. However, these price pressures ultimately reflect the ramifications of the…

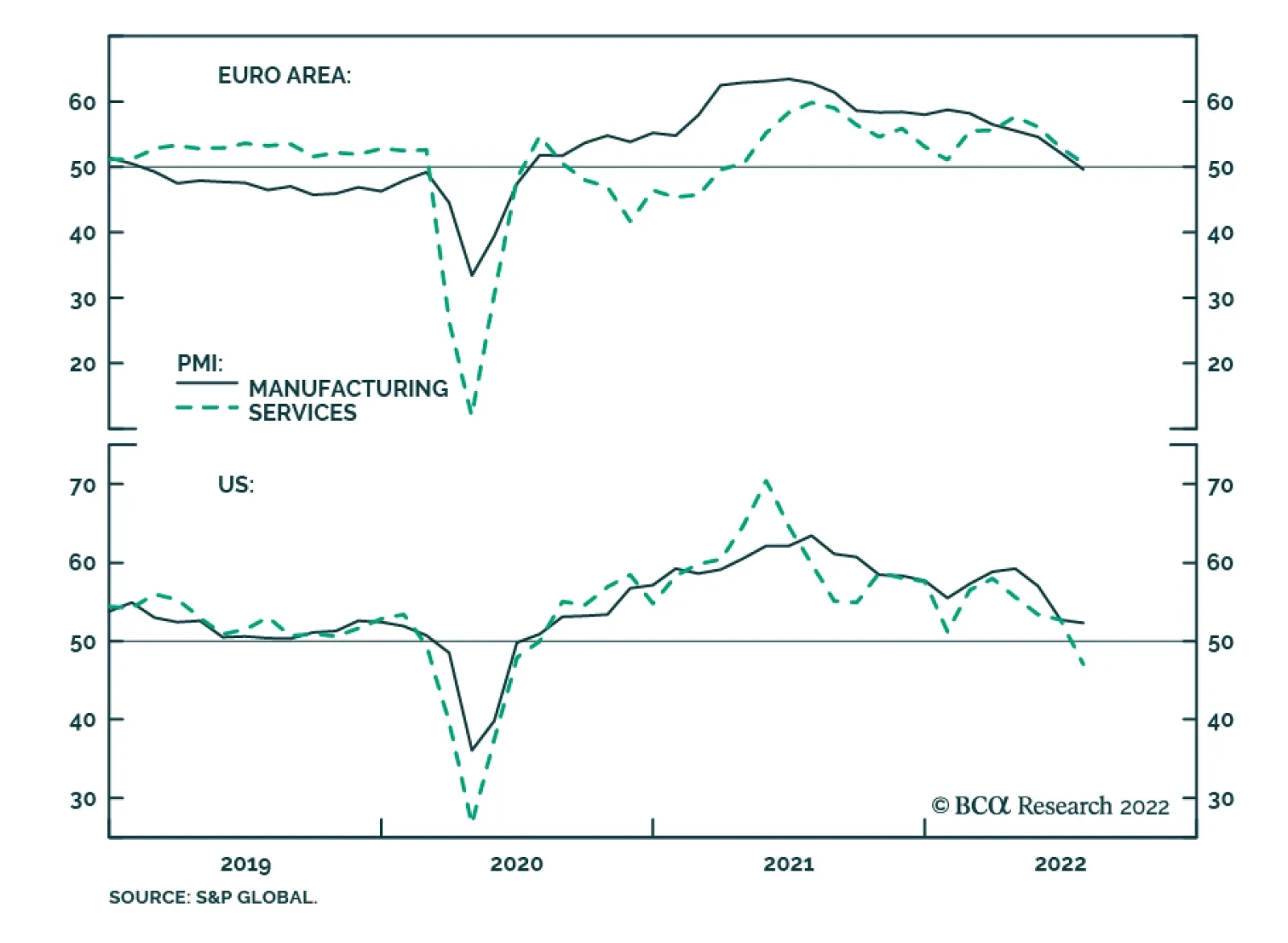

Flash PMIs sent an ominous signal about economic activity in July. The Eurozone composite index dropped to contractionary territory of 49.4 from 52.0, disappointing expectations of a slowdown to 51.0. In particular, the manufacturing index dropped below…

On Friday, Russia and Ukraine signed UN-backed agreements in Turkey that will enable Ukraine to restart exports of grains that have been blocked by Russian forces in Black Sea ports since the start of the conflict earlier this year. The agreement will also…

BCA Research’s Global Asset Allocation & Foreign Exchange Strategy services conclude that the deployment of CBDCs will be transformative for monetary policy, fiscal policy, and the banking system. Some tentative long term investment conclusions…

Listen to a short summary of this report. Executive Summary The odds of a recession in the US are lower than widely perceived. The probability of a recession is higher in Europe, although this week’s partial resumption of gas flows through the Nord Stream 1 pipeline, along with increased use of coal-fired power plants, should soften the blow. Chinese growth should rebound in the second half of the year. However, the specter of future lockdowns, the shift in global spending away from manufactured goods towards services, and the weakening property sector will continue to weigh on activity. With the Twentieth Party Congress slated for later this year, it is increasingly likely that the authorities will open up a firehose of stimulus. Fading recession risks will buoy stocks in the near term. However, a brighter economic outlook also means that the Fed, and several other central banks, may see little need to cut policy rates in 2023, as the markets are currently discounting. The end result is that government bond yields will rise from current levels, implying that stock valuations will not return to last year’s levels even if a recession is averted. After Rapidly Raising Rates, Markets Expect Some DM Central Banks To Start Easing Next Year

The Downside Of A Soft Landing

The Downside Of A Soft Landing

Bottom Line: We recommend a modest overweight on global equities for now but would turn neutral if the S&P 500 were to rise above 4,050. Dear Client, I am delighted to announce that Ritika Mankar, CFA, has joined the Global Investment Strategy team. Ritika will be writing occasional special reports on a variety of topical issues. Next week, she will make the case that the US economy’s ability to spawn mega-sized companies may become increasingly compromised over the next decade. Best regards, Peter Berezin, Chief Global Strategist The Case for a Soft Landing in the US Chart 1Cyclicals Underperformed Defensives As Recession Risks Intensified

Cyclicals Underperformed Defensives As Recession Risks Intensified

Cyclicals Underperformed Defensives As Recession Risks Intensified

Over the last few months, investors have become concerned that the Fed and many other central banks will need to engineer a recession in order to bring inflation down to more comfortable levels. While these fears have abated over the past trading week, they still continue to dominate market action (Chart 1). We place the odds of a US recession at about 40%. This is arguably more optimistic than the consensus view. According to Bank of America, the majority of fund managers saw recession as likely in this month’s survey. Not surprisingly, investors consider recession to be a major risk for equities over the next 12 months (Chart 2). Chart 2Many Investors Now See Recession As Baked In The Cake

The Downside Of A Soft Landing

The Downside Of A Soft Landing

Even if a recession does occur, we have contended that it will likely be a mild one, perhaps so mild that it will be difficult to distinguish it from a soft landing. A number of things make a soft landing in the US more probable than in the past: Labor supply has scope to increase. The labor participation rate is still 1.2 percentage points below its pre-pandemic level, two-thirds of which is due to decreased participation among workers under the age of 55 (Chart 3). The share of workers holding multiple jobs is also below its pre-pandemic level (Chart 4). The number of multiple job holders has been rising briskly lately. That is one reason why job growth in the payroll survey – which double counts workers if they hold more than one job – has been stronger than job growth in the household survey. Increased labor supply would obviate the need for the Fed to take drastic actions to curtail labor demand in its effort to restore balance to the labor market. Chart 3Labor Supply Has Scope To Rise

Labor Supply Has Scope To Rise

Labor Supply Has Scope To Rise

Chart 4The Number Of Multiple Job Holders Is Still Below Pre-Pandemic Levels

The Number Of Multiple Job Holders Is Still Below Pre-Pandemic Levels

The Number Of Multiple Job Holders Is Still Below Pre-Pandemic Levels

A high level of job openings creates a moat around the labor market. There are almost two times as many job openings as there are unemployed workers in the US (Chart 5). Many firms are likely to pull job openings before they cut jobs in response to a slowing economy. A high level of job openings will also allow workers who lose their jobs to find employment more quickly than usual, thus limiting the rise in so-called frictional unemployment. It is worth noting that the job openings rate has declined from a record 7.3% in March to a still-high 6.9% in May, with no change in the unemployment rate over this period. Chart 5A High Level Of Job Openings Creates A Moat Around The Labor Market

A High Level Of Job Openings Creates A Moat Around The Labor Market

A High Level Of Job Openings Creates A Moat Around The Labor Market

A steep Phillips curve implies that only a modest increase in unemployment may be necessary to knock down inflation towards the Fed’s target. Just as was the case in the 1960s, the Phillips curve has proven to be kinked near full employment (Chart 6). Unlike in the late 1960s, however, when rising realized inflation caused long-term inflation expectations to reset higher, expectations have remained well anchored this time around (Chart 7). Chart 6The Phillips Curve Is Kinked At Very Low Levels Of Unemployment

The Downside Of A Soft Landing

The Downside Of A Soft Landing

Chart 7Long-Term Inflation Expectations Are Well Anchored

Long-Term Inflation Expectations Are Well Anchored

Long-Term Inflation Expectations Are Well Anchored

The unwinding of pandemic and war-related dislocations should push down inflation. A recent study by the San Francisco Fed estimates that about half of May’s PCE inflation print was the result of supply-side disturbances (Chart 8). While the ongoing war in Ukraine and the threat of another Covid wave in China will continue to unsettle global supply chains, these problems should fade over time. Falling inflation would allow real wages to start rising again. This would bolster confidence, making a soft landing more likely (Chart 9). Chart 8Supply Factors Explain Half Of The Increase In Prices Over The Past Year

The Downside Of A Soft Landing

The Downside Of A Soft Landing

Chart 9Positive Real Wage Growth Will Bolster Consumer Confidence

Positive Real Wage Growth Will Bolster Consumer Confidence

Positive Real Wage Growth Will Bolster Consumer Confidence

A lack of major financial imbalances makes the US economy more resilient to economic shocks. As a share of disposable income, US household debt is 34 percentage points below its 2008 peak (Chart 10). Relative to net worth, household debt is at multi-decade lows. About two-thirds of mortgages carry a FICO score above 760 compared to only one-third during the housing bubble (Chart 11). Non-mortgage consumer credit also remains in good shape, as my colleague Doug Peta elaborated in this week’s US Investment Strategy report. While corporate debt has risen over the past decade, the ratio of corporate debt-to-assets today is still below where it was during the 1990s. Moreover, thanks to stronger corporate profitability, the interest coverage ratio is near an all-time high (Chart 12). Chart 10AUS Household Debt Is Not Especially High Anymore (I)

US Household Debt Is Not Especially High Anymore (I)

US Household Debt Is Not Especially High Anymore (I)

Chart 10BUS Household Debt Is Not Especially High Anymore (II)

US Household Debt Is Not Especially High Anymore (II)

US Household Debt Is Not Especially High Anymore (II)

Chart 11FICO Scores For Residential Mortgages Have Improved Considerably Since The Pre-GFC Housing Bubble

The Downside Of A Soft Landing

The Downside Of A Soft Landing

Chart 12Corporate Balance Sheets Are In Decent Shape

Corporate Balance Sheets Are In Decent Shape

Corporate Balance Sheets Are In Decent Shape

Chart 13Tight Supply Limits The Downside Risks To Housing

Tight Supply Limits The Downside Risks To Housing

Tight Supply Limits The Downside Risks To Housing

Just like the US does not suffer from major financial imbalances, it does not suffer from any major economic imbalances either. The homeowner vacancy rate is near a record low, which should put a floor under residential investment (Chart 13). Outside of investment in intellectual property, which is not especially sensitive to the business cycle, nonresidential investment is still below pre-pandemic levels and not much above where it was as a share of GDP during the Great Recession (Chart 14). Spending on consumer durable goods has retraced four-fifths of its pandemic surge, with little ill-effect on aggregate employment (Chart 15). Chart 14Outside Of IP, Nonresidential Investment Is Still Low

Outside Of IP, Nonresidential Investment Is Still Low

Outside Of IP, Nonresidential Investment Is Still Low

Chart 15Spending On Durable Goods Has Been Normalizing Without Derailing The Economy

Spending On Durable Goods Has Been Normalizing Without Derailing The Economy

Spending On Durable Goods Has Been Normalizing Without Derailing The Economy

Europe: A Deep Freeze Will Likely Be Avoided Chart 16Russia Can Potentially Cause Significant Economic Damage In The EU If It Closes The Taps

The Downside Of A Soft Landing

The Downside Of A Soft Landing

The macroeconomic picture is less benign outside the US. Four years ago, German diplomats laughed off warnings that their country had become dangerously dependent on Russian energy. They are not laughing anymore. German industry, just like industry across much of Europe, is facing a major energy crunch. The IMF estimates that output losses associated with a full Russian gas shutoff over the next 12 months could amount to as much as 2.7% of GDP in the EU (Chart 16). In Central and Eastern Europe, output could shrink by 6%. Among the major economies, Germany and Italy are the most at risk. Fortunately, Europe is finally stepping up to the challenge. The highly ambitious REPowerEU plan seeks to displace two-thirds of Russian gas by the end of 2022. The plan does not include any additional energy that could be generated by increased usage of coal-fired power plants, a strategy that the European political establishment (including the German Green Party!) has only recently begun to champion. It is possible that EU leaders felt the need to generate a crisis mentality to justify the decision to burn more coal. Dire warnings about how Europe is prepared to ration gas also send a message to Russia that the EU is ready to suffer in order to thwart Putin’s despotic regime. Whether Europe actually follows through is a different story. It is worth noting that the Nord Stream 1 pipeline resumed operations this week after Germany received, over Ukrainian objections, a repaired turbine from Canada. The resumption of partial flows through the pipeline, along with increased fiscal support for households and firms, reduces the risks of a “deep freeze” recession in Europe. The unveiling of the ECB’s new Transmission Protection Instrument (TPI) this week should also help anchor sovereign credit spreads across the euro area. While the exact conditions under which the TPI will be engaged have yet to be fleshed out, we expect the terms to be fairly liberal, reflecting not only the lessons learned from last decade’s euro debt crisis, but also to serve as a powerful bulwark against Putin’s efforts to destabilize the EU economy. China: Government’s Growth Target Looks Increasingly Unrealistic Stronger growth in China would help European exporters (Chart 17). Chinese real GDP grew by just 0.4% in the second quarter from a year earlier as the economy was battered by Covid lockdowns. Activity should pick up in the second half of the year, but at this point, the government’s 5.5% growth target looks completely unachievable. The specter of future lockdowns, the shift in global spending away from manufactured goods towards services, and the weakening Chinese property sector are all weighing on the economy (Chart 18). Chart 17European Exporters Would Welcome A Stronger Chinese Economy

European Exporters Would Welcome A Stronger Chinese Economy

European Exporters Would Welcome A Stronger Chinese Economy

The authorities will likely seek to stimulate the economy by allowing local governments to bring forward $220 billion in bond issuance that had been originally slated for 2023. The problem is that land sales – the main source of local government revenue – have collapsed. Worried about the ability of local governments to service their obligations, both retail investors and banks have shied away from buying local government debt. Chart 18A Slowing Property Market And Covid Lockdowns Have Been Weighing On The Chinese Economy

A Slowing Property Market And Covid Lockdowns Have Been Weighing On The Chinese Economy

A Slowing Property Market And Covid Lockdowns Have Been Weighing On The Chinese Economy

Meanwhile, the inability of property developers to secure adequate financing to complete construction projects has left a growing number of home buyers in the lurch. In most cases, these properties were purchased off-the-plan. Understandably, home buyers have balked at the prospect of having to make mortgage payments on properties that they do not possess. With the Twentieth Party Congress slated for later this year, it is increasingly likely that the authorities will open up a firehose of stimulus, including increased assistance for property developers and banks, as well as income-support measures for households. While such measures will not address China’s myriad structural problems, they will help keep the economy afloat. Equity Valuations in a Soft-Landing Scenario A few weeks ago, the consensus view was that stocks would tumble in the second half of the year as the global economy fell into recession but would then rally in 2023 as central banks began lowering rates. We argued the opposite, namely that stocks would likely rebound in the second half of the year as the economy outperformed expectations but would then face renewed pressure in 2023 as it became clear that the Fed and several other central banks had no reason to cut rates (Chart 19). Chart 19After Rapidly Raising Rates, Markets Expect Some DM Central Banks To Start Easing Next Year

The Downside Of A Soft Landing

The Downside Of A Soft Landing

Chart 20Real Rates Have Jumped This Year

Real Rates Have Jumped This Year

Real Rates Have Jumped This Year

In a baseline scenario where a recession is averted, we argued that the S&P 500 could rise to 4,500 (60% odds). In contrast, we noted that the S&P 500 could fall to 3,500 in a mild recession scenario (30% odds) and to 2,900 in a deep recession scenario (10% odds). It is worth stressing that even at 4,500, the S&P 500 would still be 11% lower in real terms than it was on January 4th. At the stock market’s peak in January, the 10-year TIPS yield stood at -0.91%, while the 30-year TIPS yield stood at -0.27%. Today, they stand at 0.58% and 0.93%, respectively (Chart 20). If real rates do not return to their prior lows, it is unlikely that equity valuations will return to their prior highs. This limits the upside for stocks, even in a soft-landing scenario. The sharp rally in stocks over the past week has priced out some of this recession risk, moving equity valuations closer towards what we regard as fair value. As we noted last week, we will turn neutral on equities if the S&P 500 were to rise above 4,050. As we go to press, we are only 1.3% from that level. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Follow me on LinkedIn & Twitter Global Investment Strategy View Matrix

The Downside Of A Soft Landing

The Downside Of A Soft Landing

Special Trade Recommendations Current MacroQuant Model Scores

The Downside Of A Soft Landing

The Downside Of A Soft Landing

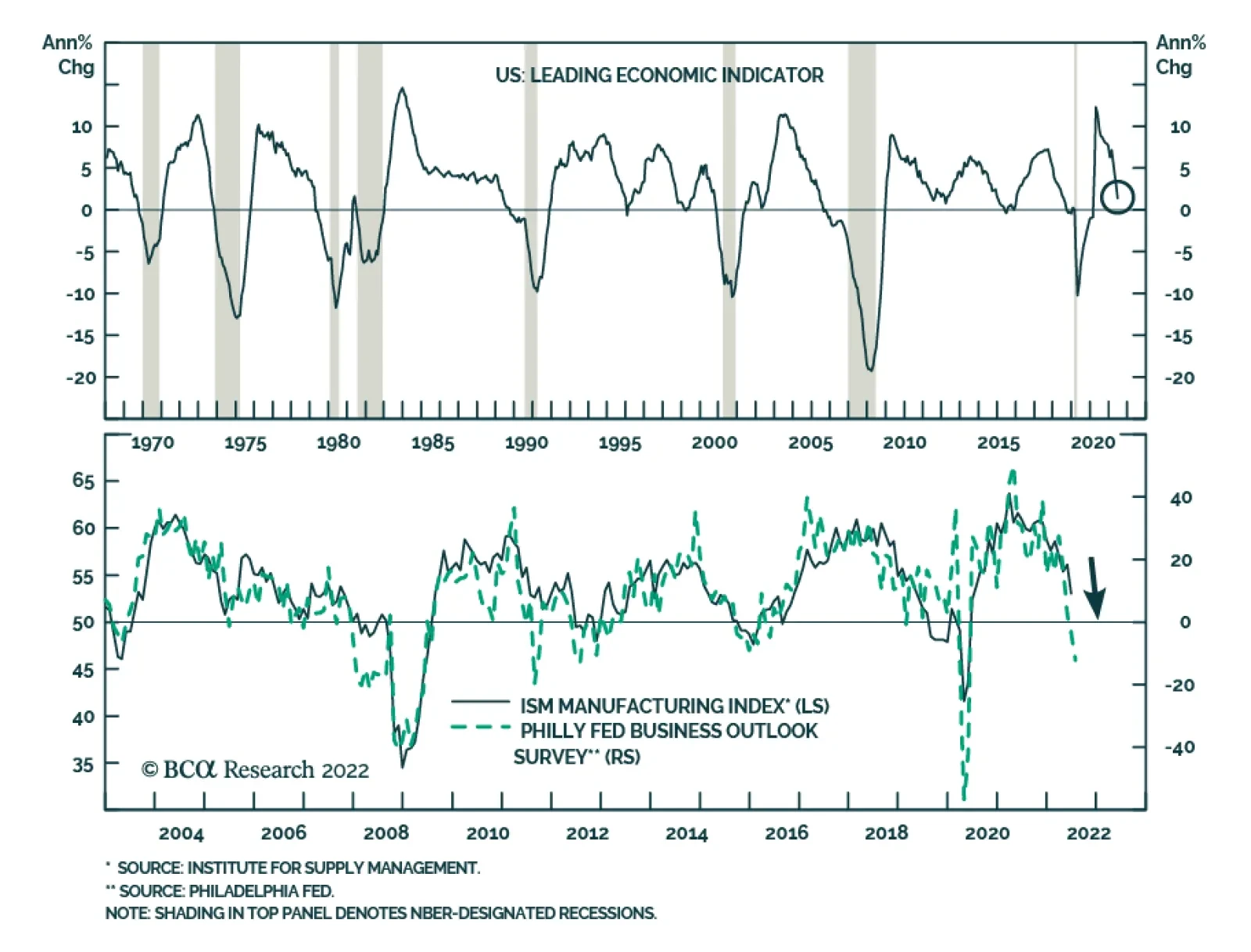

The Conference Board US Leading Economic Index (LEI) deteriorated further in June, contracting by a larger-than-expected 0.8% following a 0.4% decline in May. Consumer sentiment, labor market conditions, stock prices and manufacturing new orders were the main…