Economic Growth

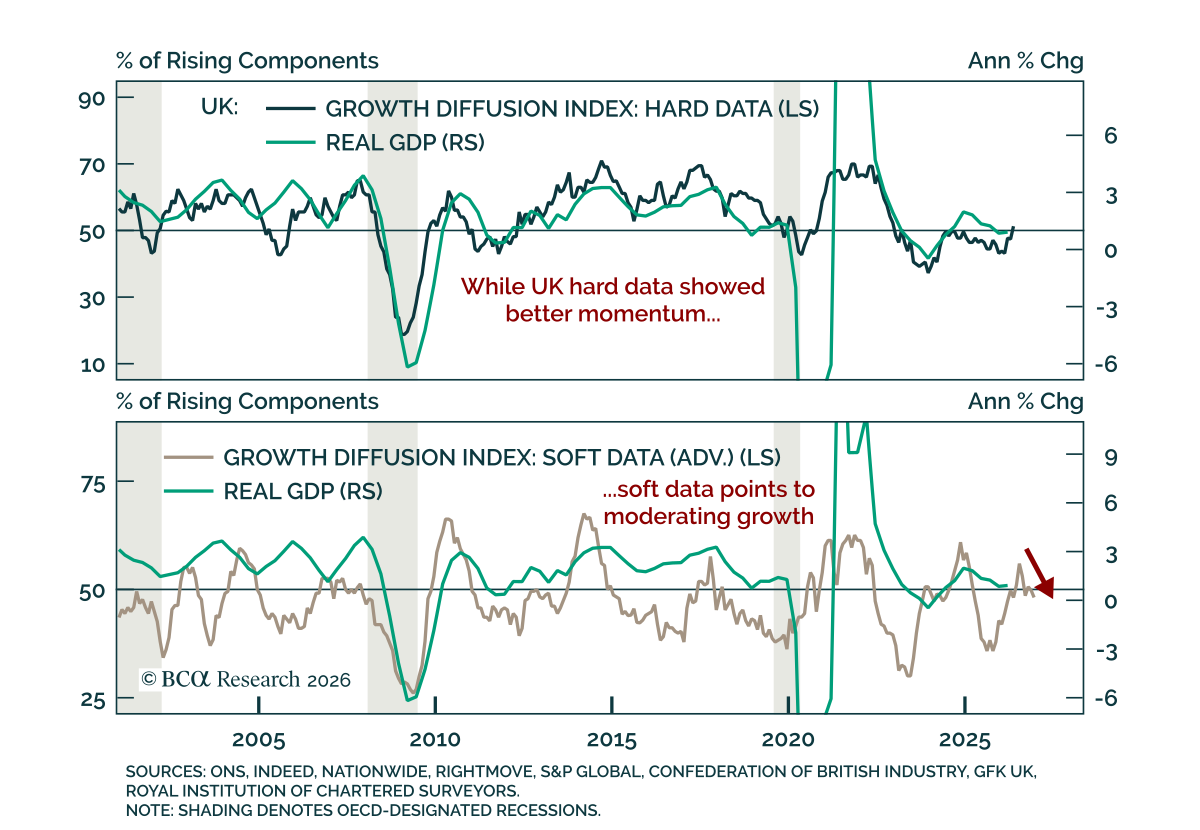

UK May hard data surprised to the upside, but still pointed to weak growth and limited scope for further BoE tightening. Hard data refers to directly measurable activity such as production, employment, and spending. Monthly GDP rose 0.1% m/m after contracting…

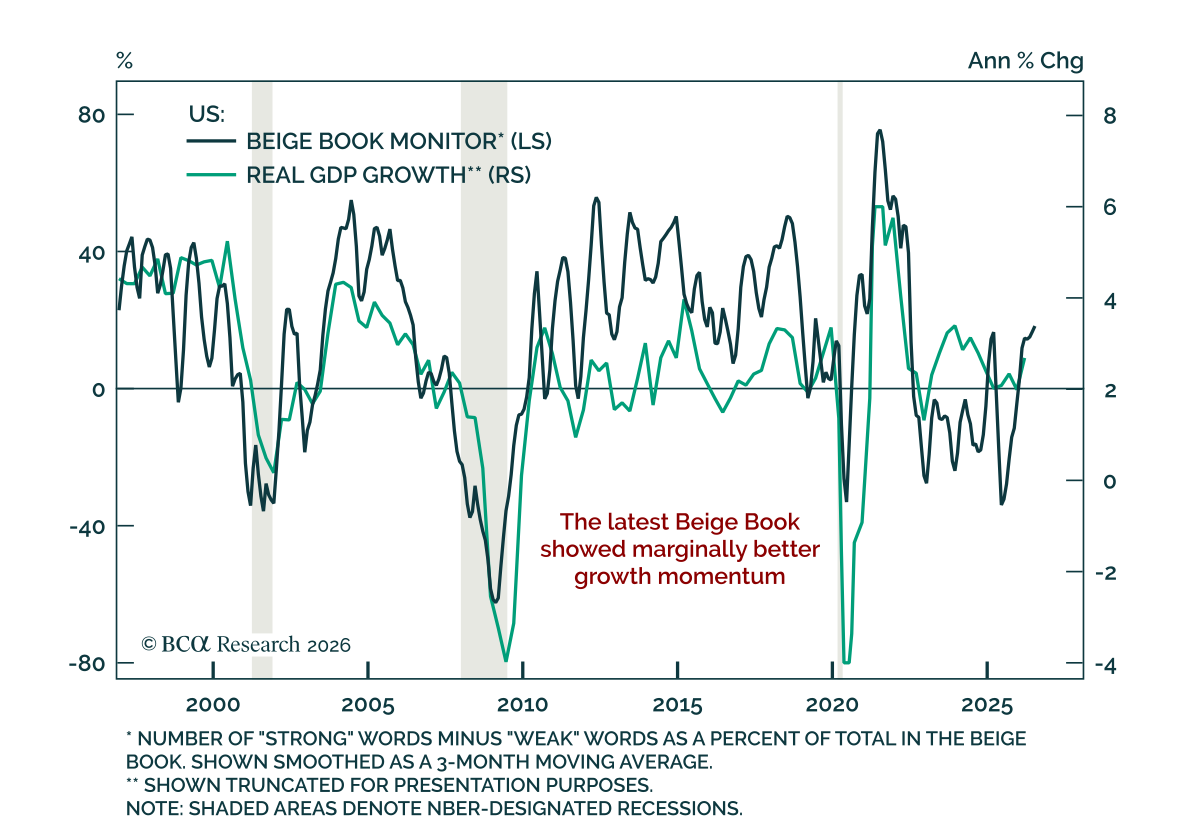

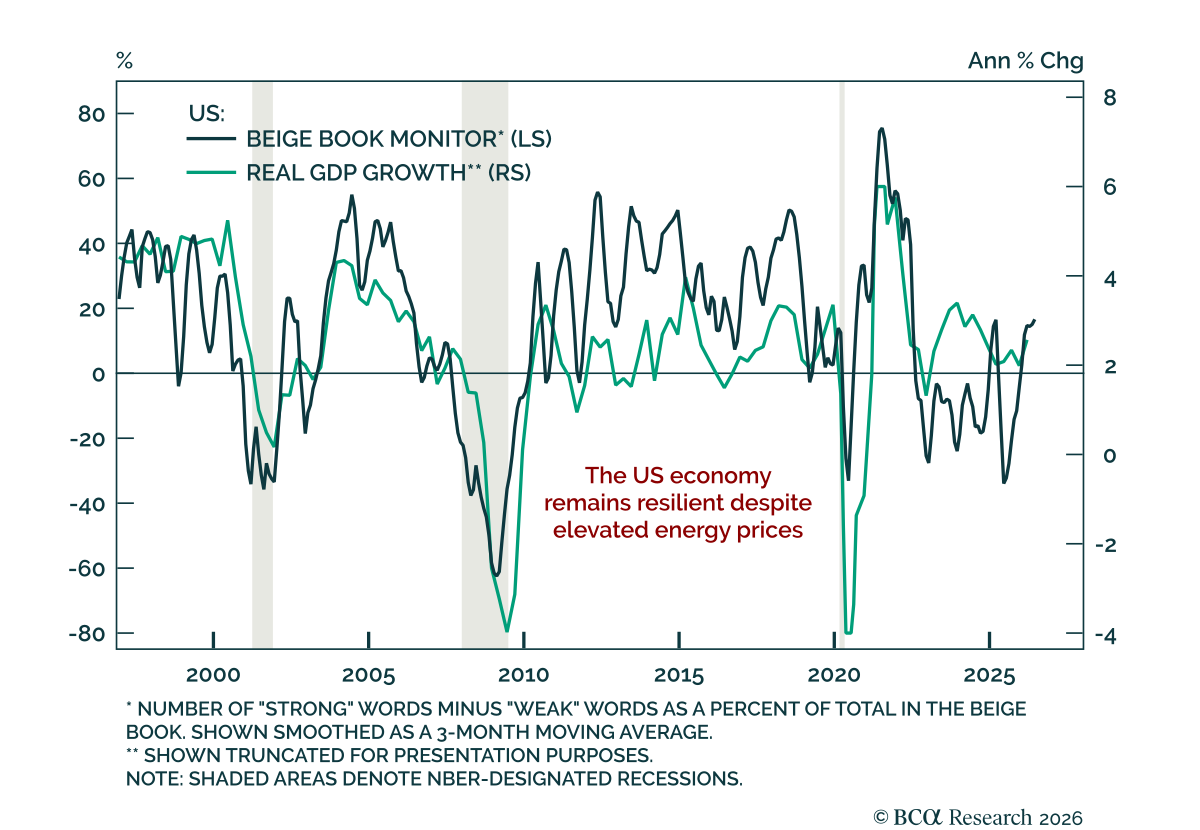

The Fed’s Beige Book pointed to slightly better growth momentum, while confirming that wage growth is normalizing and AI’s inflationary effects remain demand-driven for now. An increasing share of Fed districts reported growth at a slight-to-modest pace,…

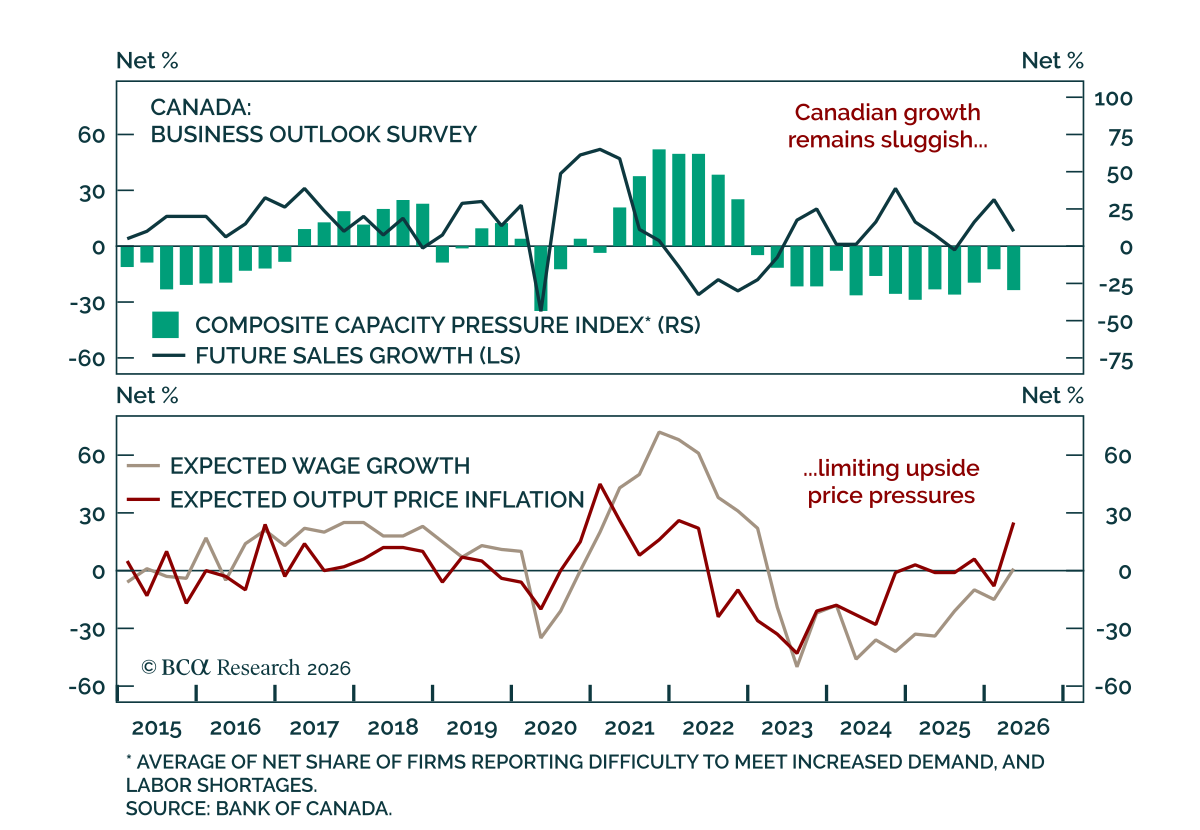

The Bank of Canada’s Q2 Business Outlook Survey pointed to a fragile economy, supporting the case for fading hikes priced into the CORRA curve. While the BOS indicator was roughly unchanged at -0.4, the report’s underlying details showed broad deterioration…

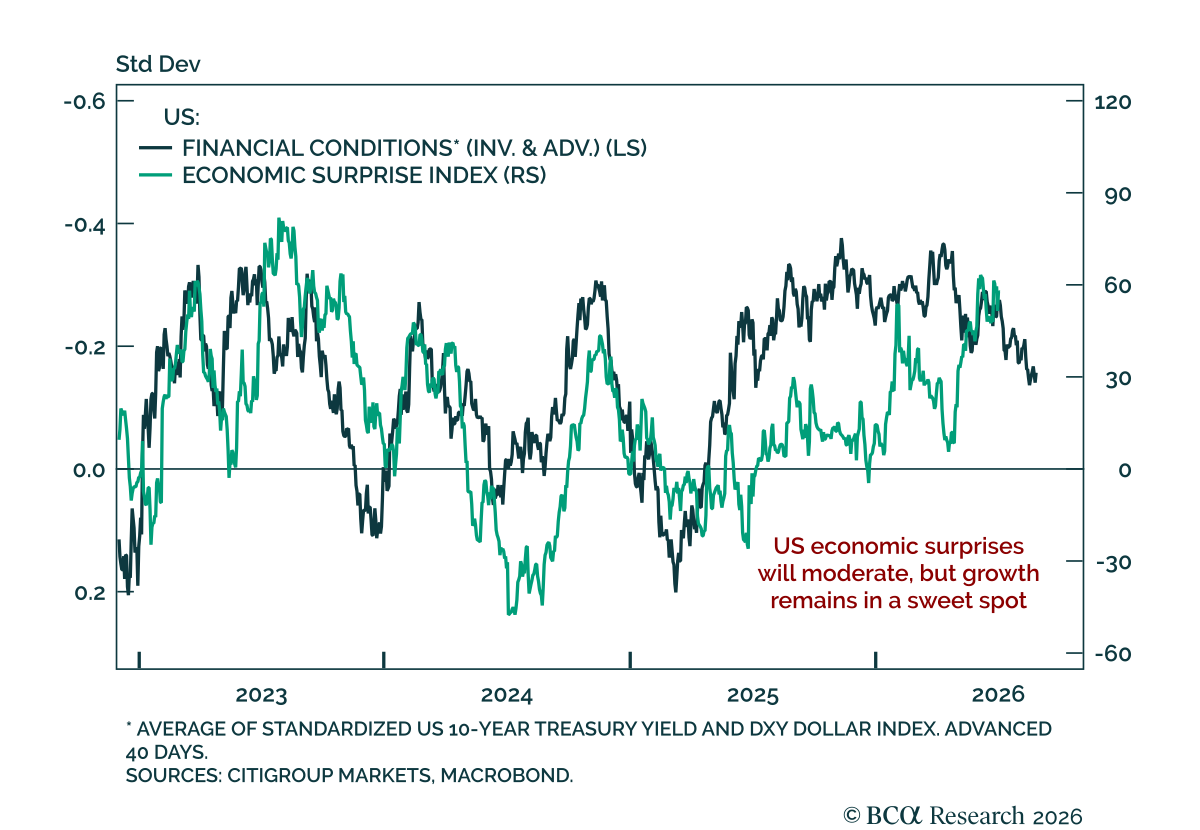

Marginally tighter US financial conditions point to some moderation in economic surprises. Despite a disappointing employment report, US economic data remains positive. But while the US economy has so far beaten forecasts this year, the Iran war has tightened…

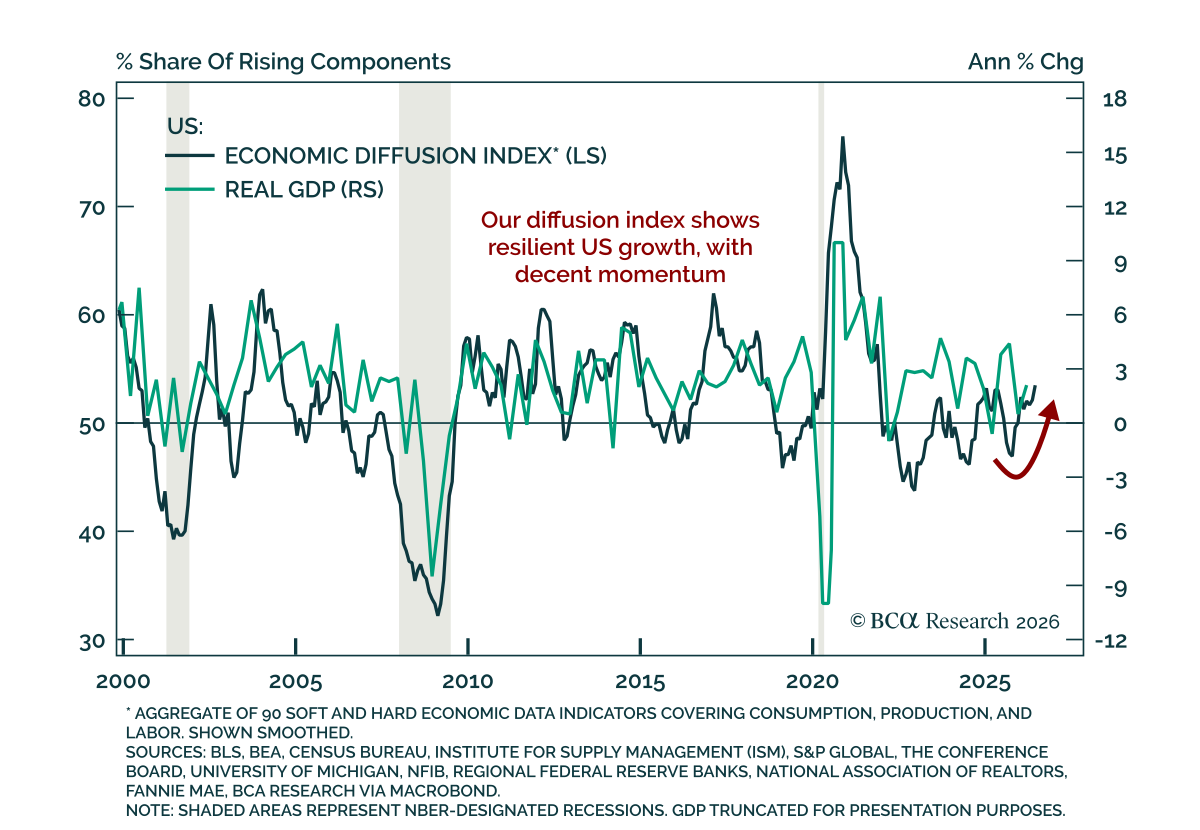

The US economy has remained resilient this year despite slowdown fears tied to geopolitical tensions. US economic data has surprised positively since the start of the year. The Iran war has weighed on business and consumer confidence, but has had little…

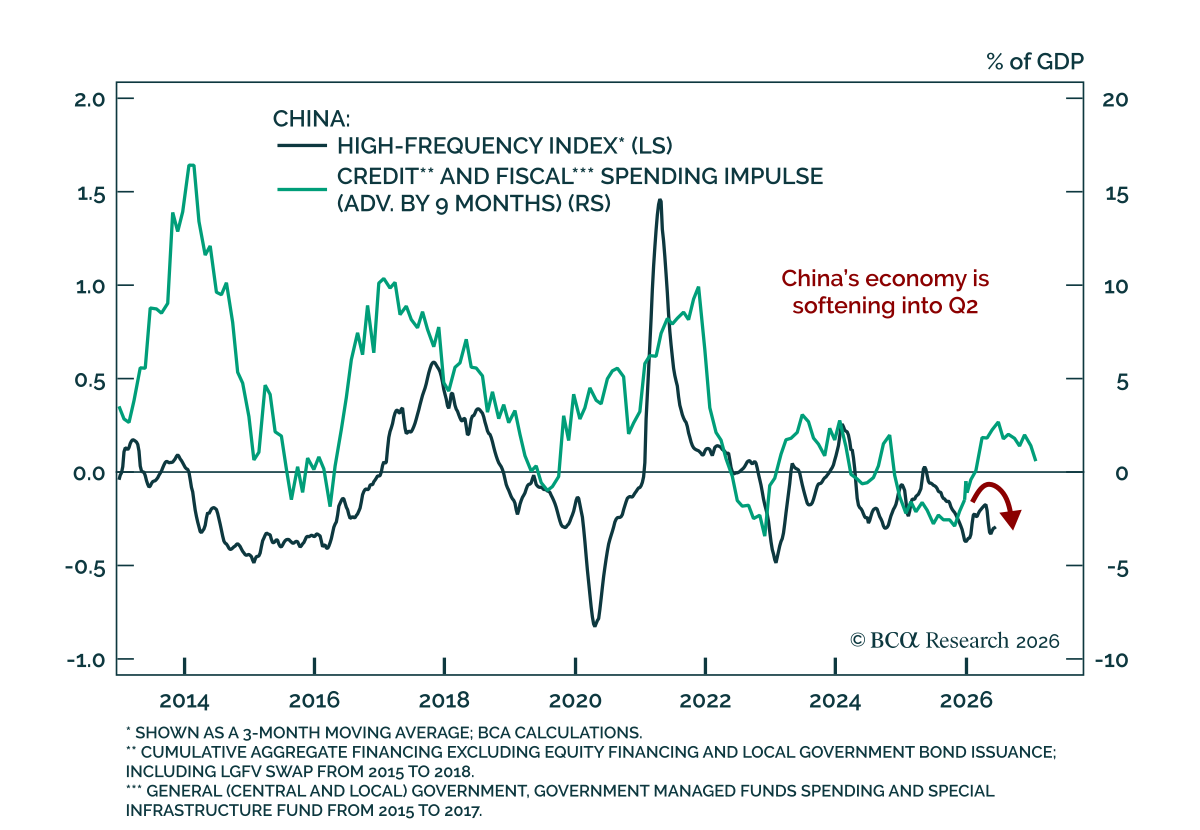

China’s weakening economy is likely to bring more fiscal support in H2, but the benefits will be concentrated and equity volatility is set to rise. Our Chart Of The Week comes from Jing Sima, Chief China Strategist. Jing looks at China’s outlook for the rest…

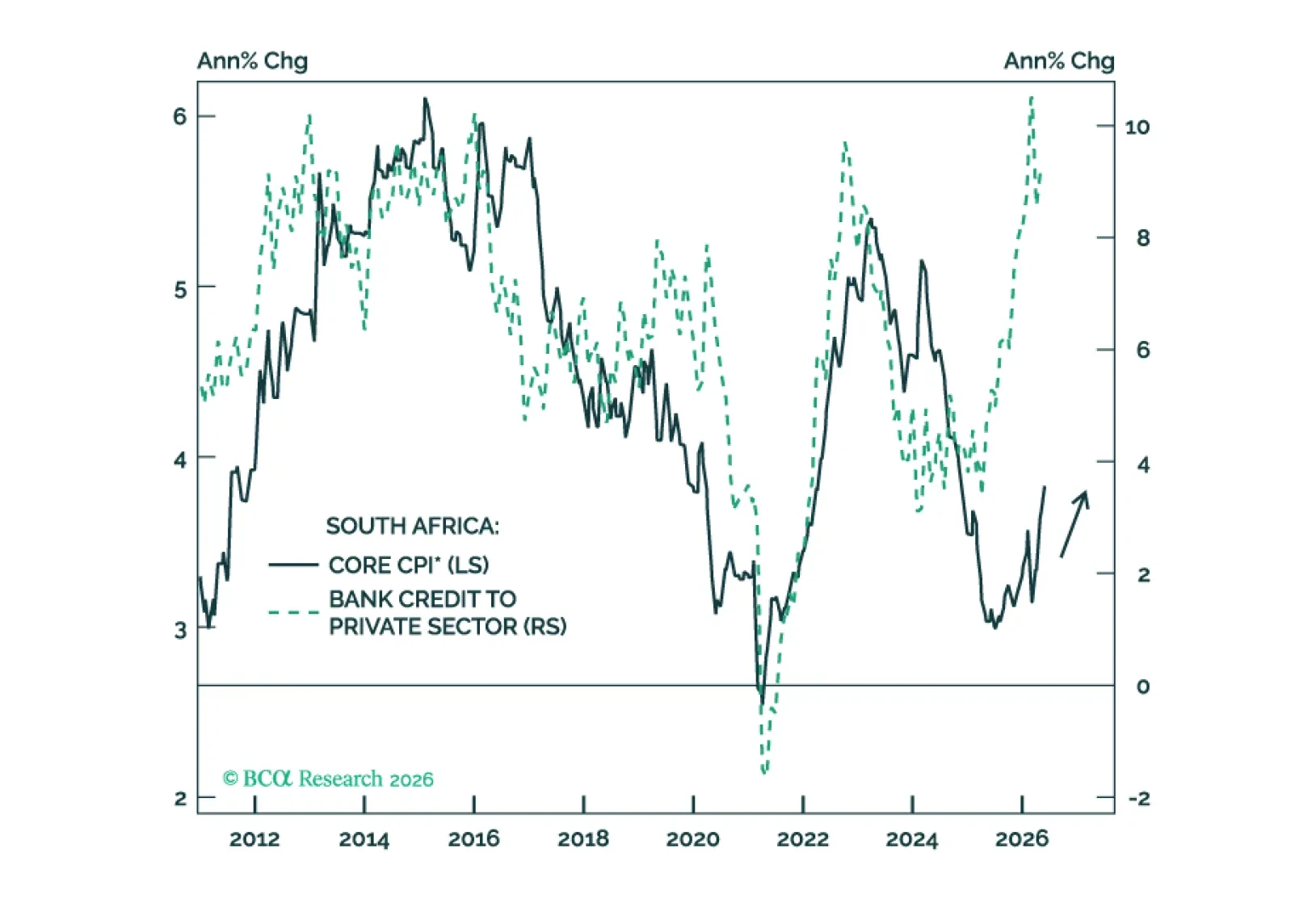

South Africa’s ambitious reform agenda will take time to bear fruit. Meanwhile, the country faces a stagflationary squeeze as inflation rises while growth slows. South African stocks, bonds, and currency are all vulnerable.

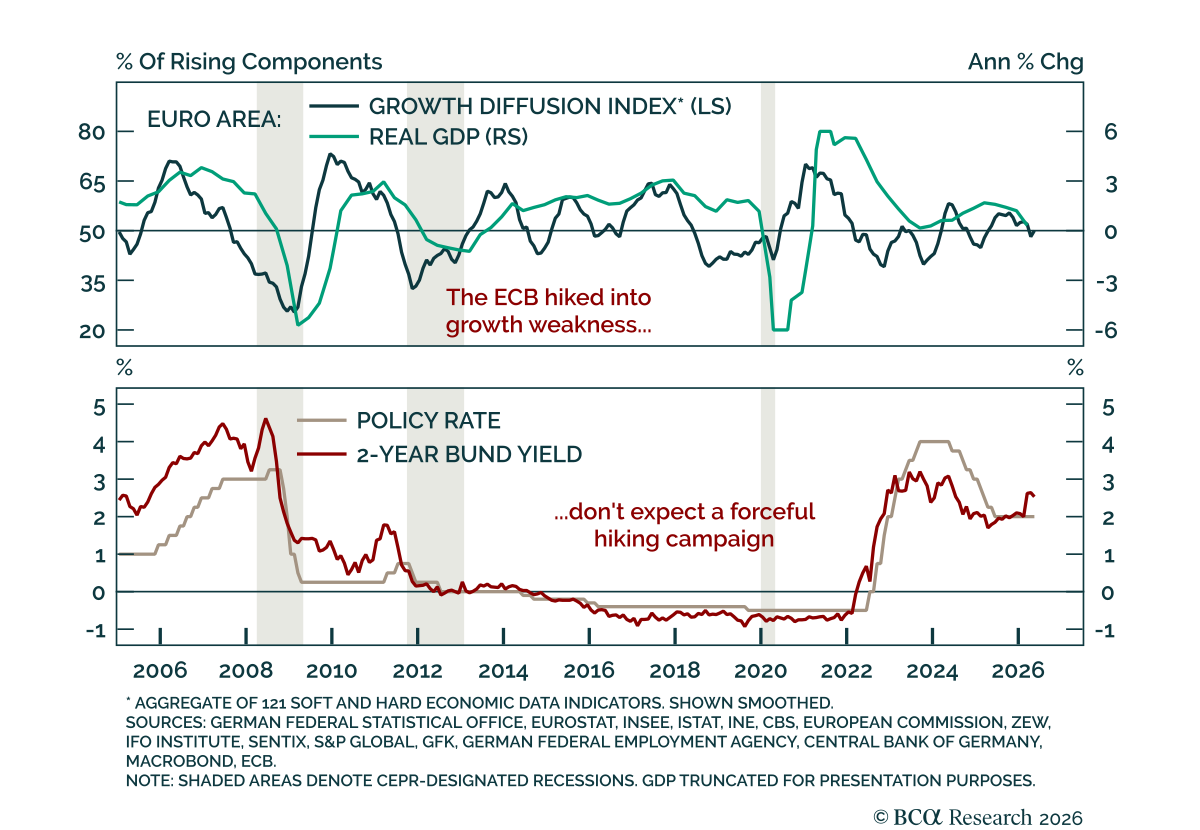

The ECB hiked as expected, but further tightening would be a mistake that ultimately supports European bonds. The policy rate was raised by 25 bps to 2.25%, as expected. The ECB also revised its inflation forecasts higher and its growth forecasts lower. It…

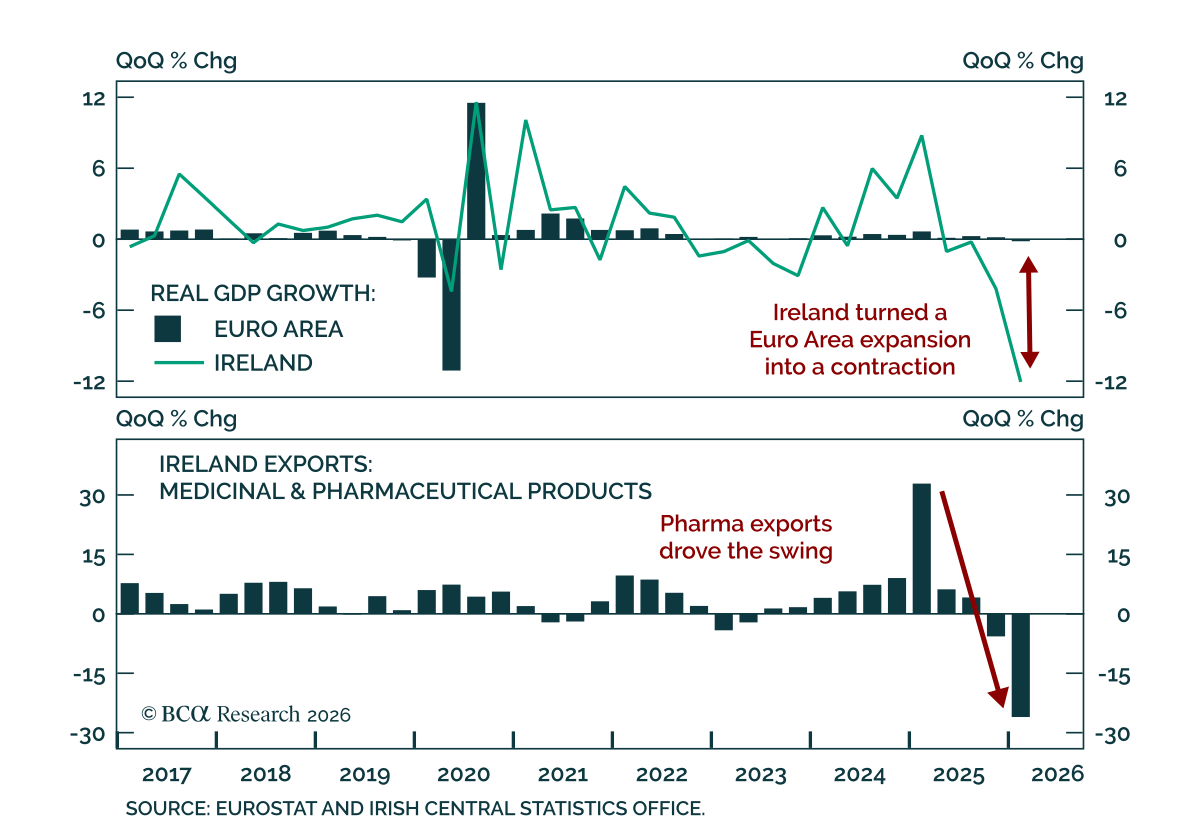

Ireland is making the Euro Area look weaker than it is. The bloc reportedly contracted 0.2% in Q1 2026, but stripping out Ireland would have shown a 0.3% expansion. That reversal can be traced back to a dramatic downward revision in Irish GDP, from -2% to…

The Beige Book reinforces a slight-to-moderate growth backdrop with widening consumer stress, stronger manufacturing, and sticky cost pressures. Latest comments provide a new angle into recent developments and the sentiment of economic agents in the face of…