Economic Growth

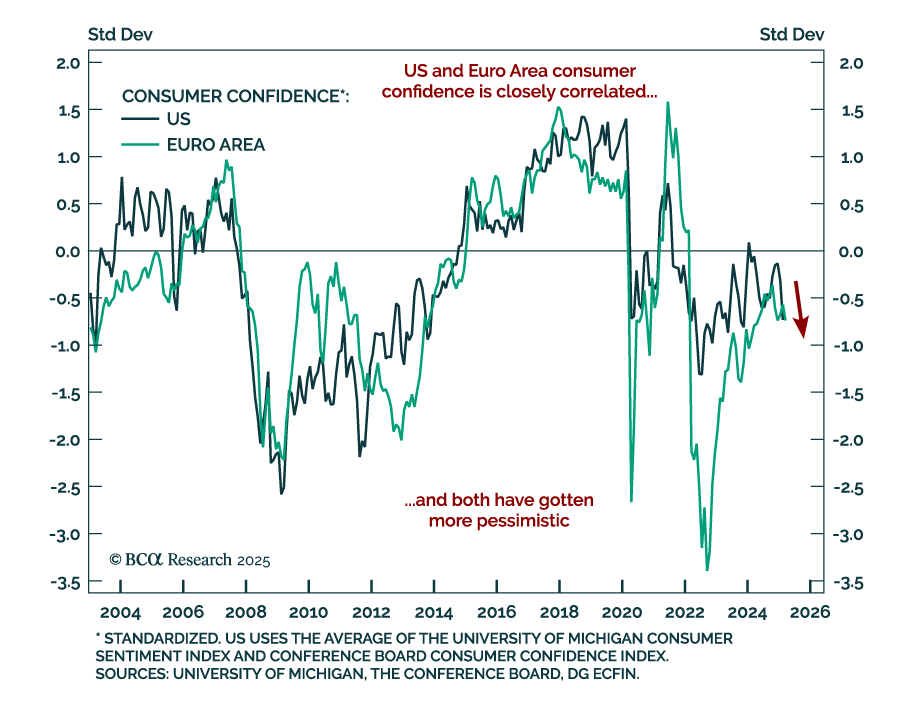

The March flash estimate for European Consumer Confidence missed estimates, and fell to -14.5 from -13.6 in February. This negative reading is the first European sentiment number missing expectations since January. The sentiment shift between the US and…

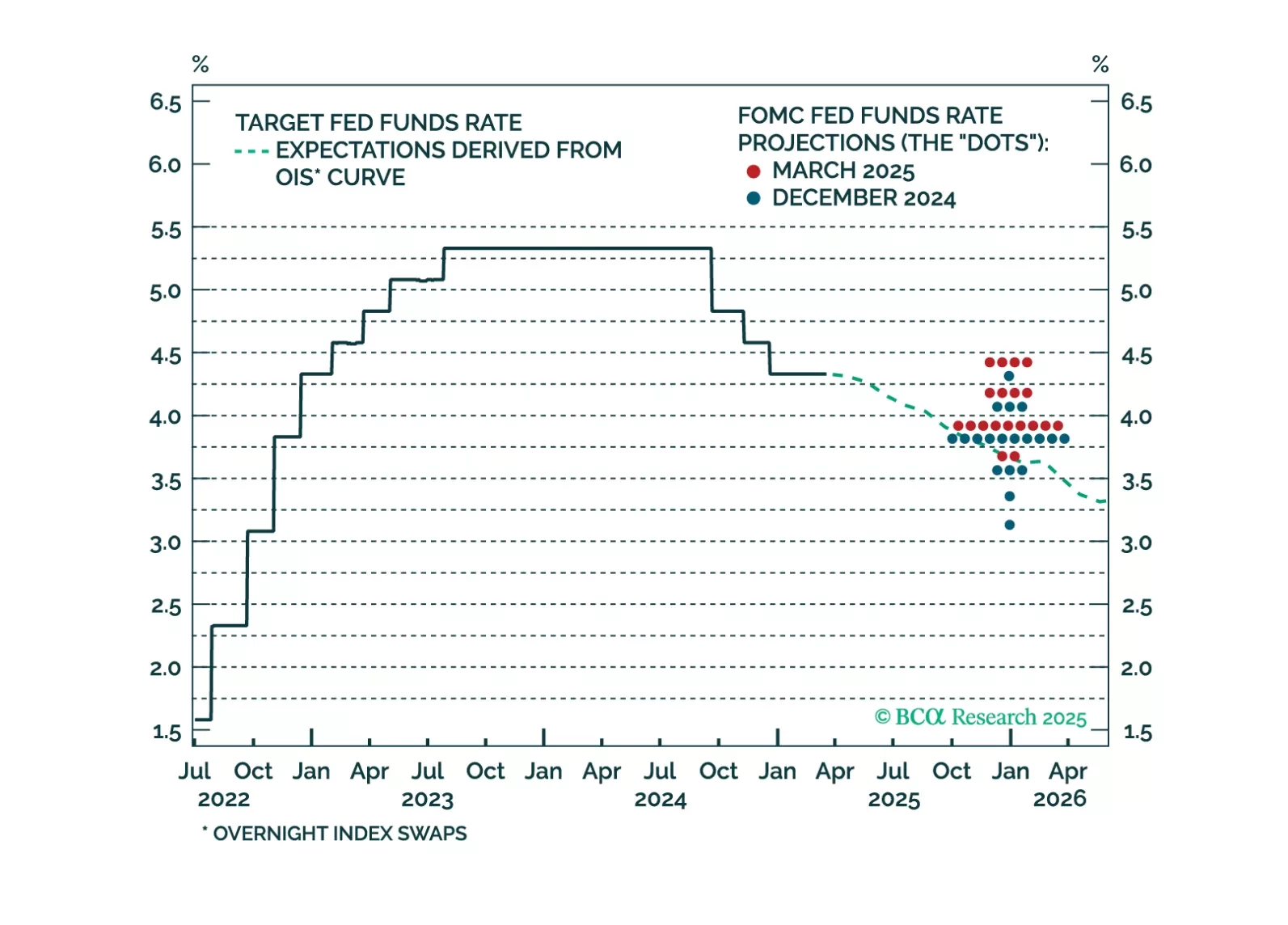

The market reaction to this afternoon’s Fed meeting looks overdone. Investors could be in for a hawkish surprise when it becomes apparent that the Fed won’t ease policy into higher tariff-driven inflation prints.

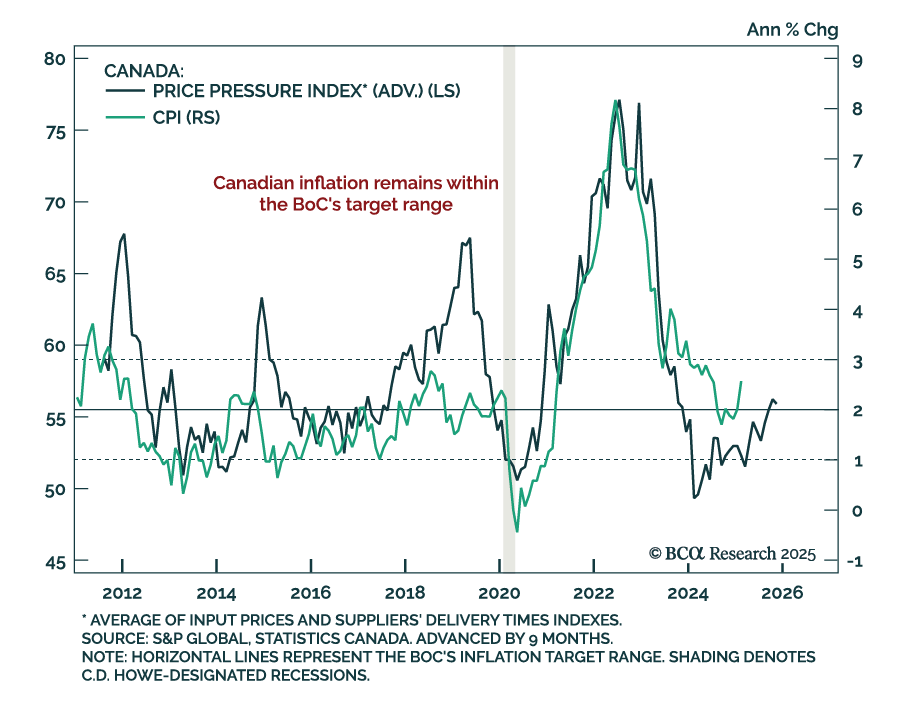

February Canadian headline inflation was stronger than expected, rising to 2.6% y/y from 1.9% in January. The Bank of Canada’s core measures were also slightly hotter than expected, both rising to 2.9% from 2.7% a month prior, near the top of the BoC’s…

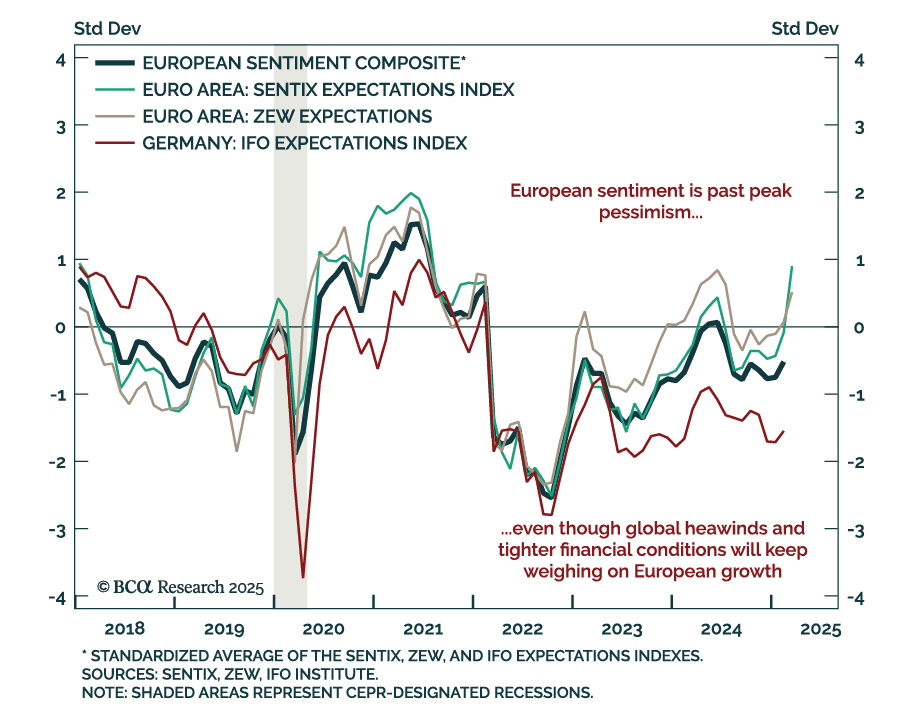

The March ZEW index for Germany and the eurozone beat estimates, with the expectations component rising to 51.6 from 26.0 in February. The current situation assessment only marginally improved yet remains deeply negative at -87.6. The March data shows…

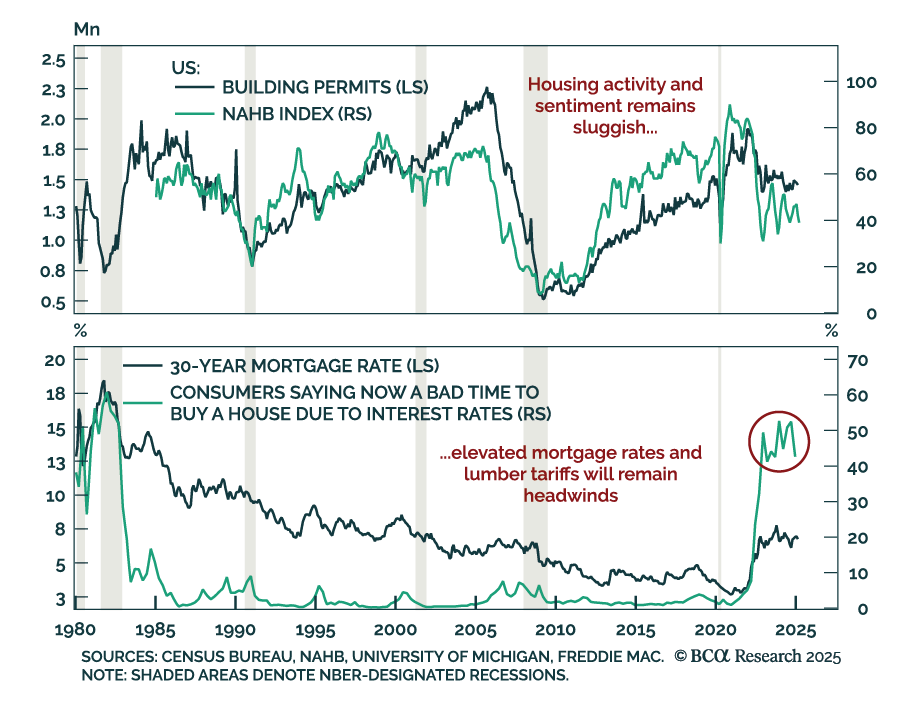

US February housing data was relatively strong, with housing starts rising 11.2% m/m after falling 9.8% in January. While they fell less than expected, building permits still declined at a faster pace than in January. The March NAHB Housing Market Index also…

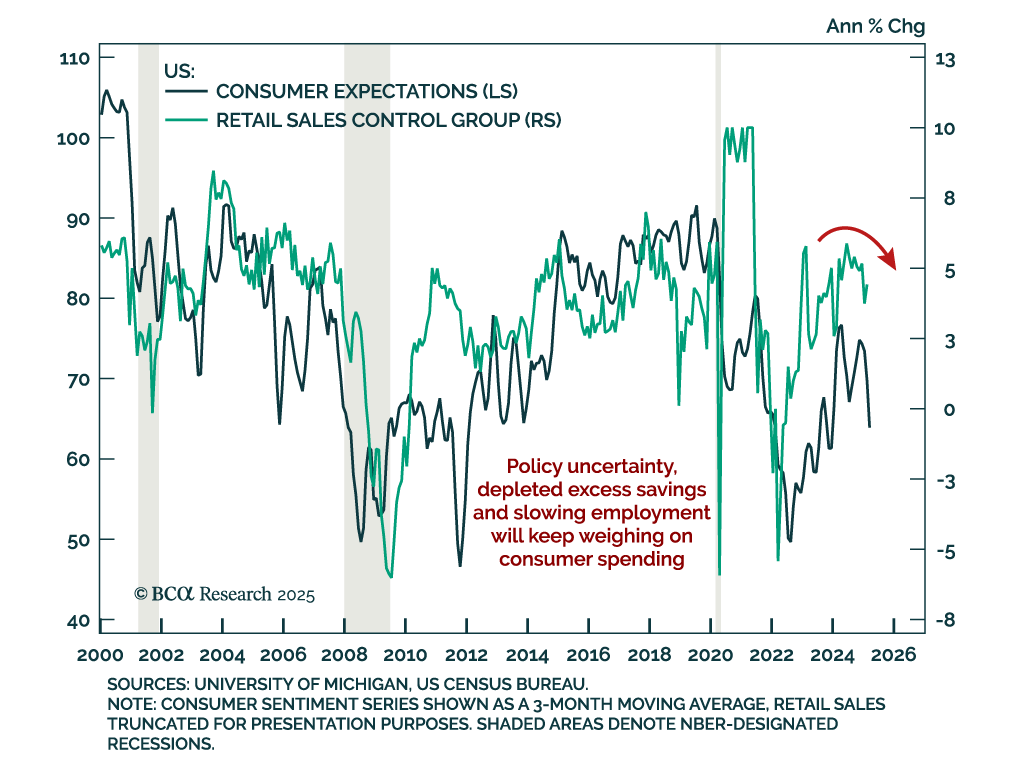

February US retail sales were mixed, with the headline number missing expectations at only 0.2% m/m. January’s reading was revised down to -1.2%. Core measures (excluding gas & autos) were roughly in line with estimates, but the control group saw a 1.0%…

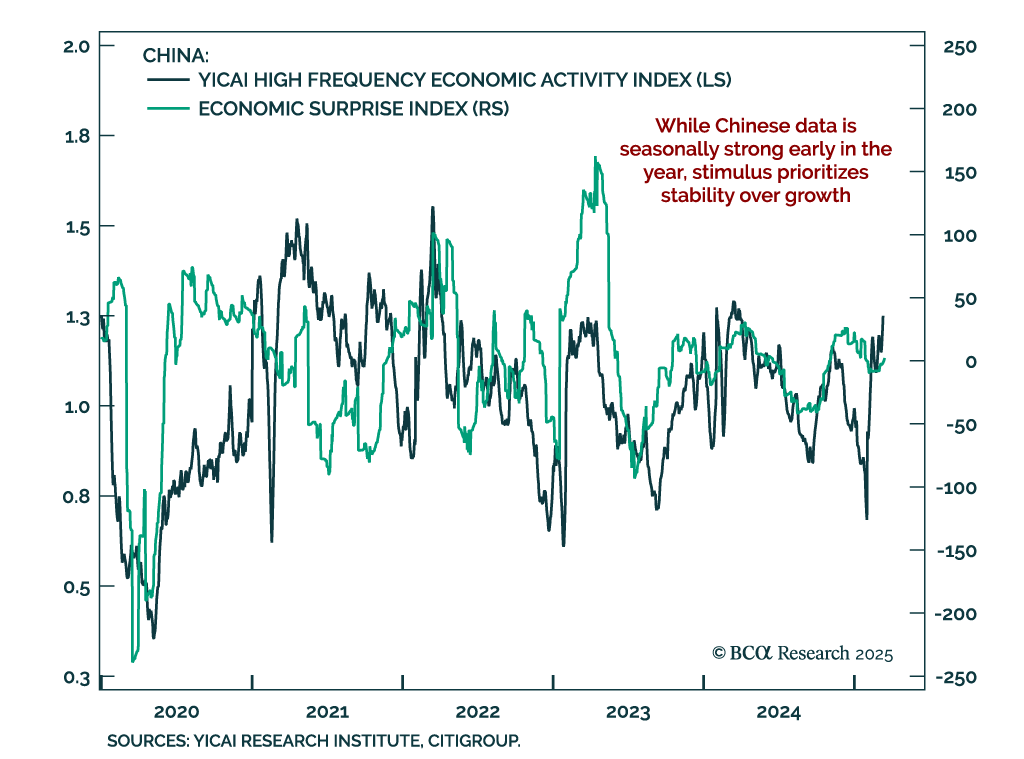

Outside of the real estate sector, Chinese activity was decent in January and February. Both industrial production and retail sales were slightly stronger than expected. The jobless rate ticked up to 5.4% while property investment was down -9.8%…

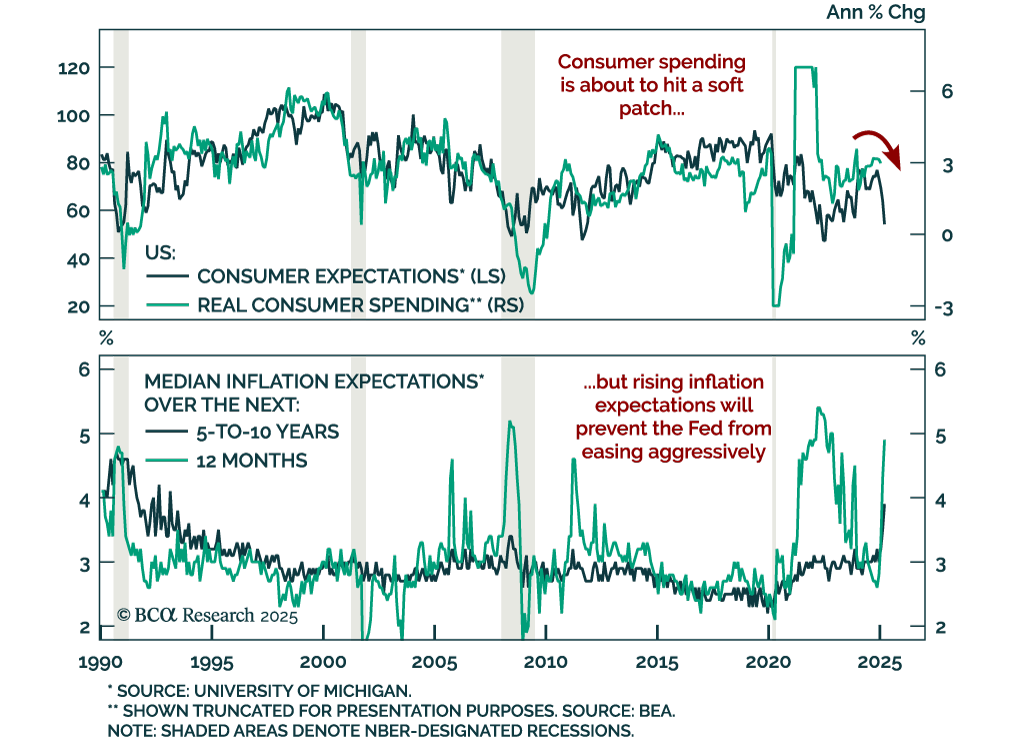

The preliminary March University of Michigan Consumer Sentiment Index missed estimates, falling to 57.9 from 64.7. The decrease came from both the assessment of current conditions and expectations, with the latter falling almost 10 points. Measures of 1-year…

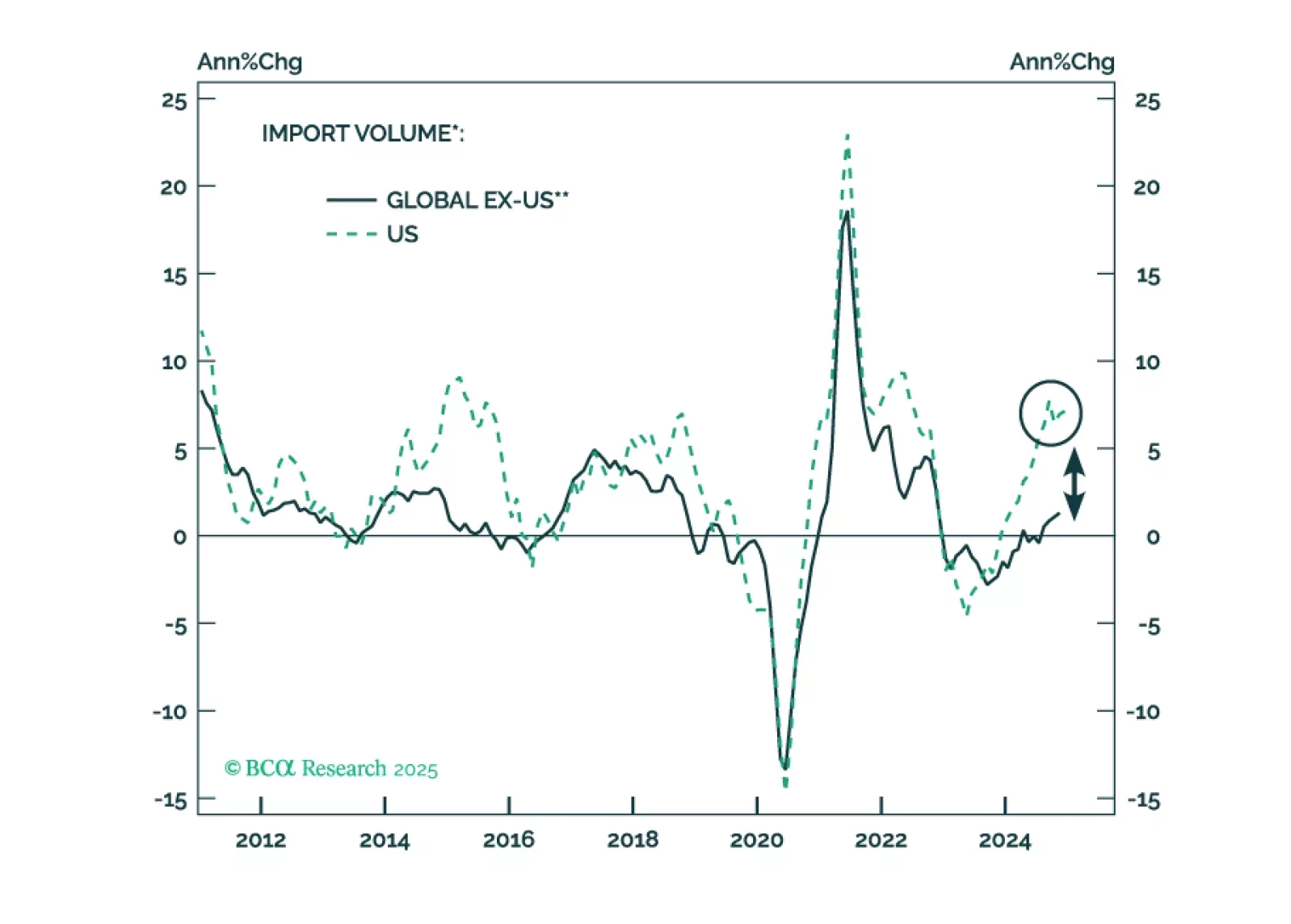

Notwithstanding periodic short-term rebounds, the path of least resistance for global share prices remains down. The resilience of European and Chinese stocks in the face of the US equity selloff is unsustainable. These economies will deteriorate as US demand – the sole pillar of global growth in the past two years – vanishes and tariffs bite. A new currency trade: go long MXN / short an equal-weighted basket of CAD and the euro.

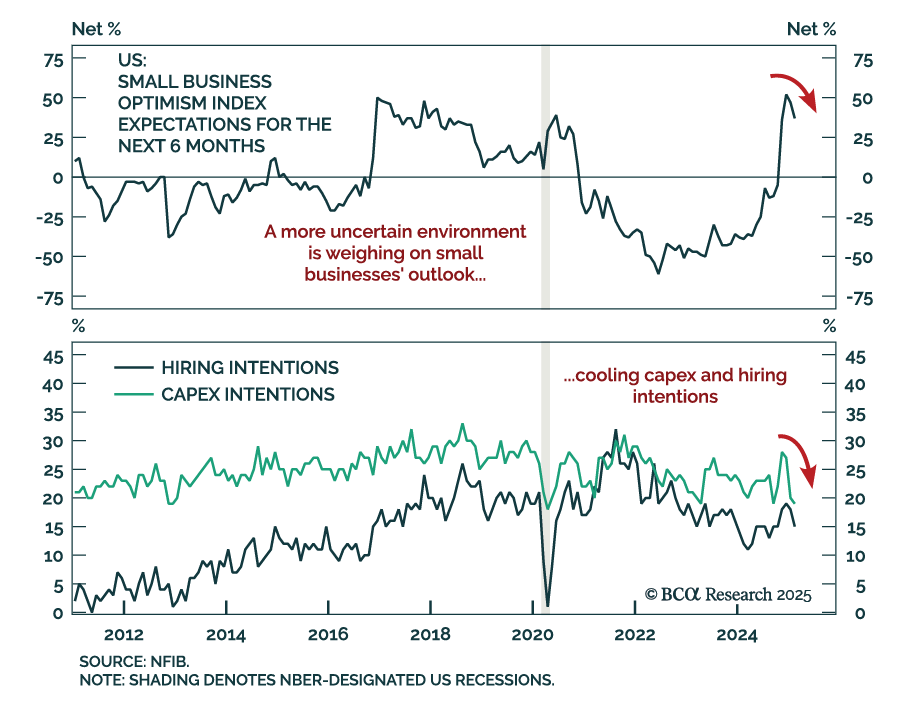

The February NFIB Small Business Optimism index decreased more than expected to 100.7 from 102.8. The decline extends the reversal seen since the November US election as policy optimism yields to uncertainty. The signal from the report was stagflationary…