Emerging Markets

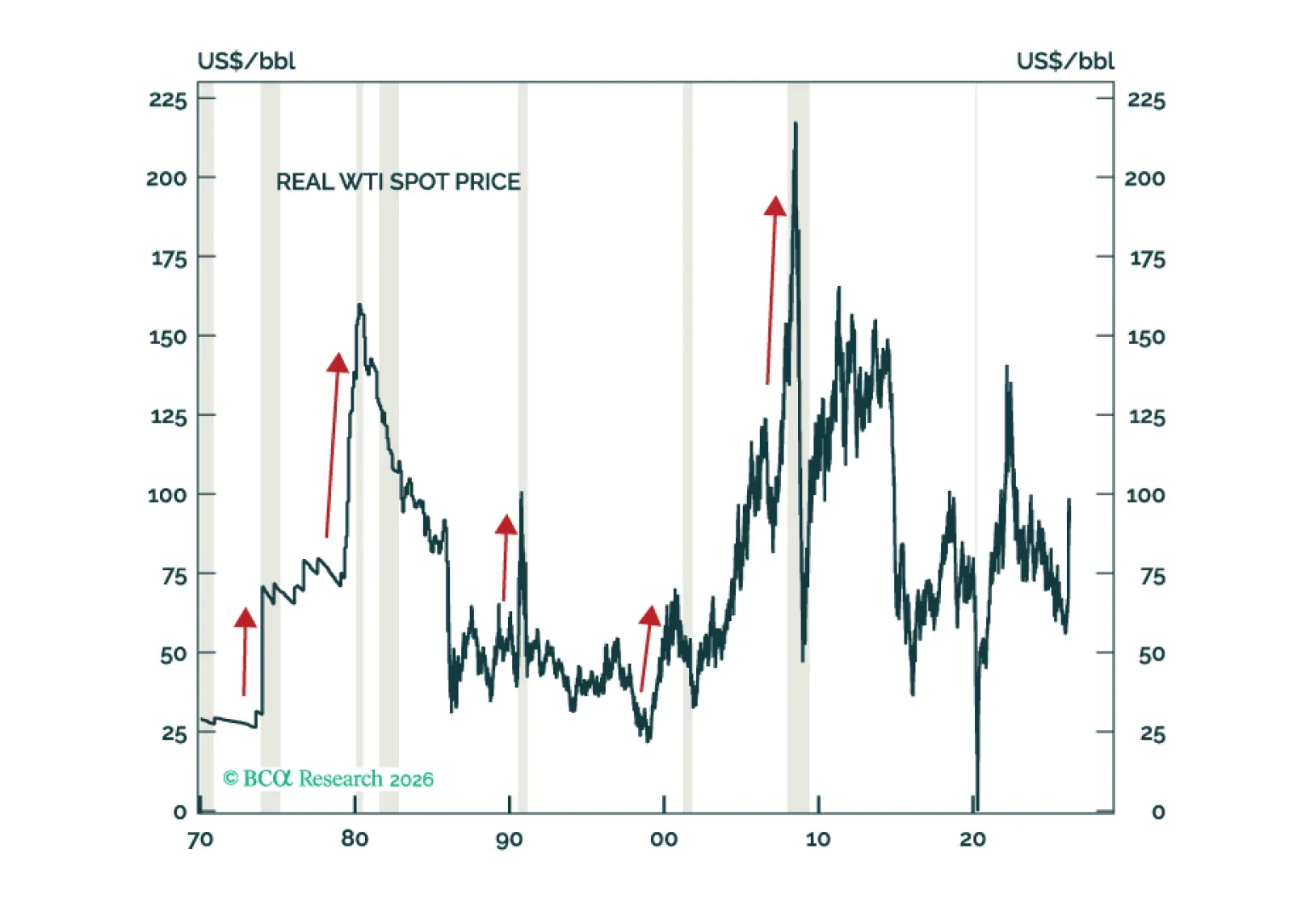

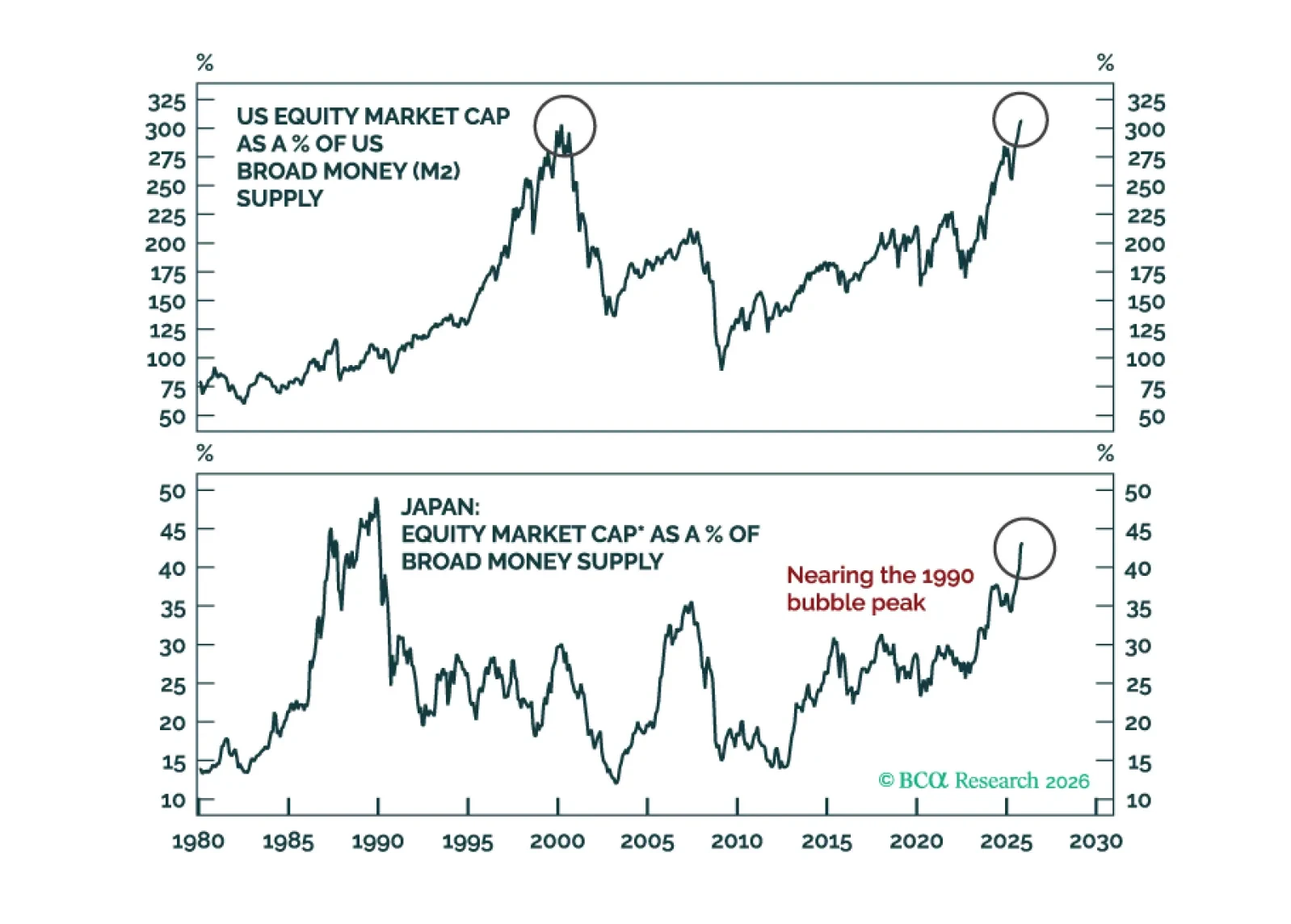

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

Indonesian rupiah will continue to plunge, and its local-currency bond yields will rise materially. Investors should short domestic bonds, currency unhedged.

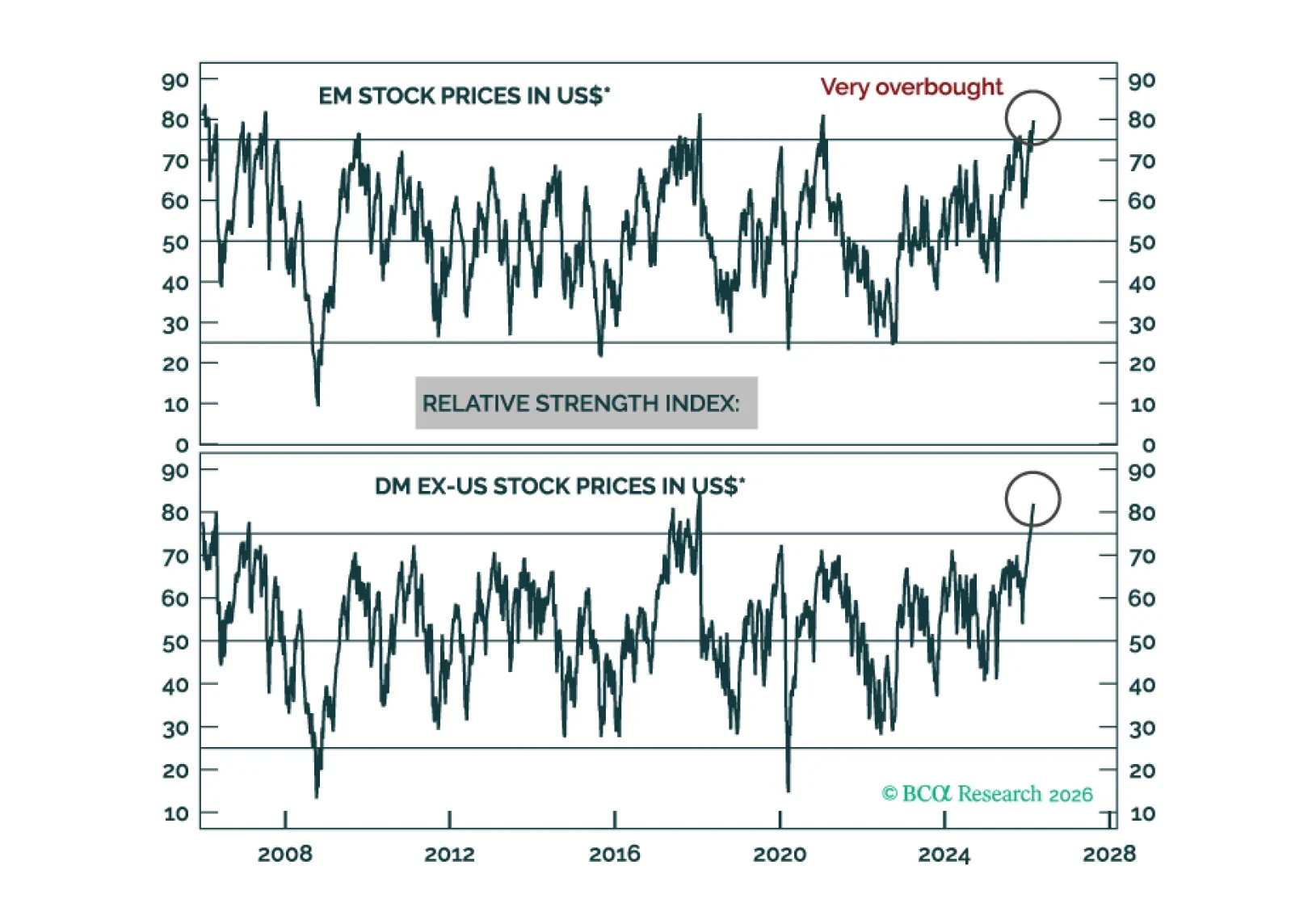

Avoid EM and DM risk assets. In the near term (one-to-three months), the odds favor US equity outperformance and a US dollar rebound. Nevertheless, the cyclical outlook (nine-to-12 months) warrants underweighting US equities and staying short the greenback.

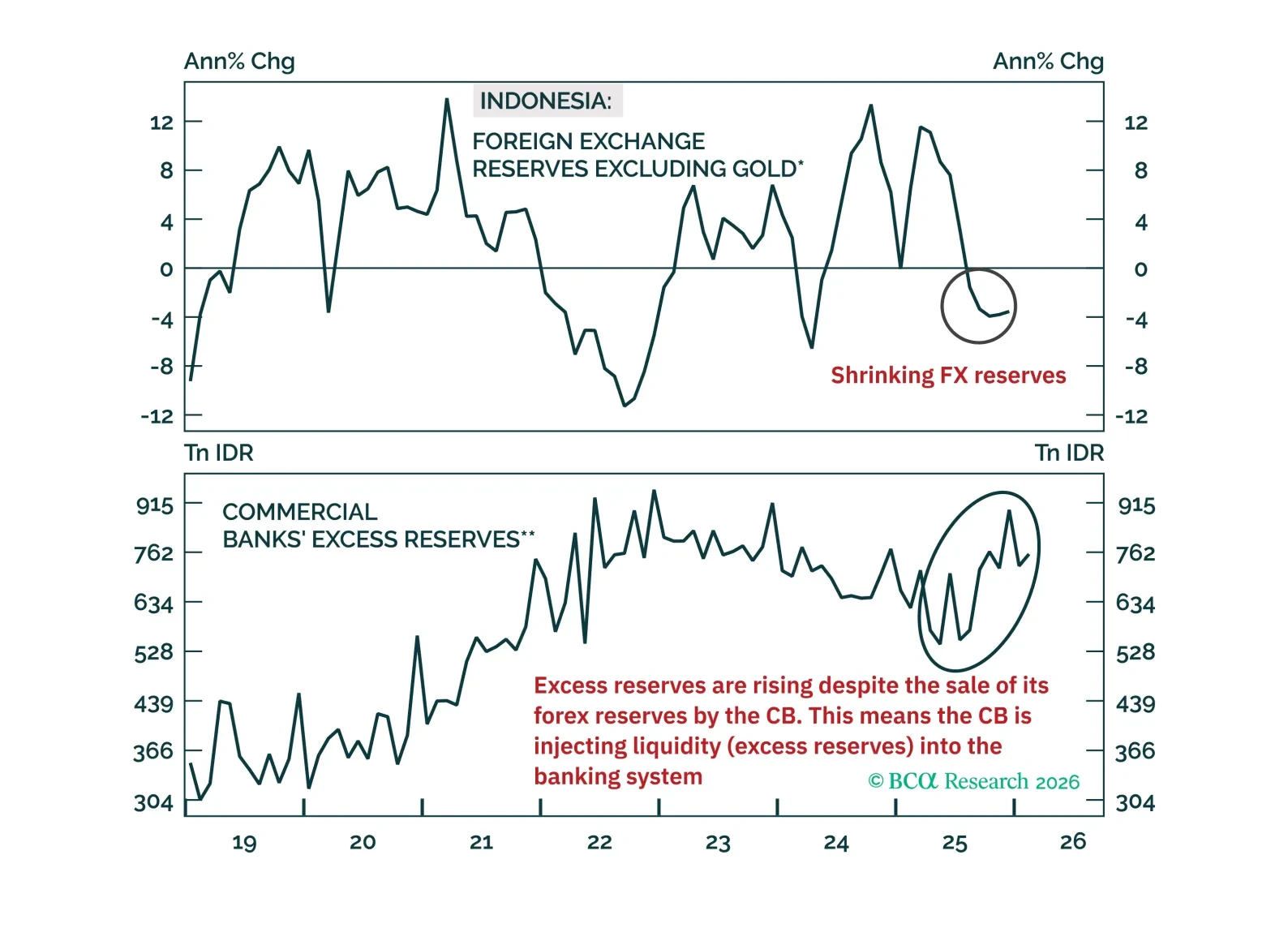

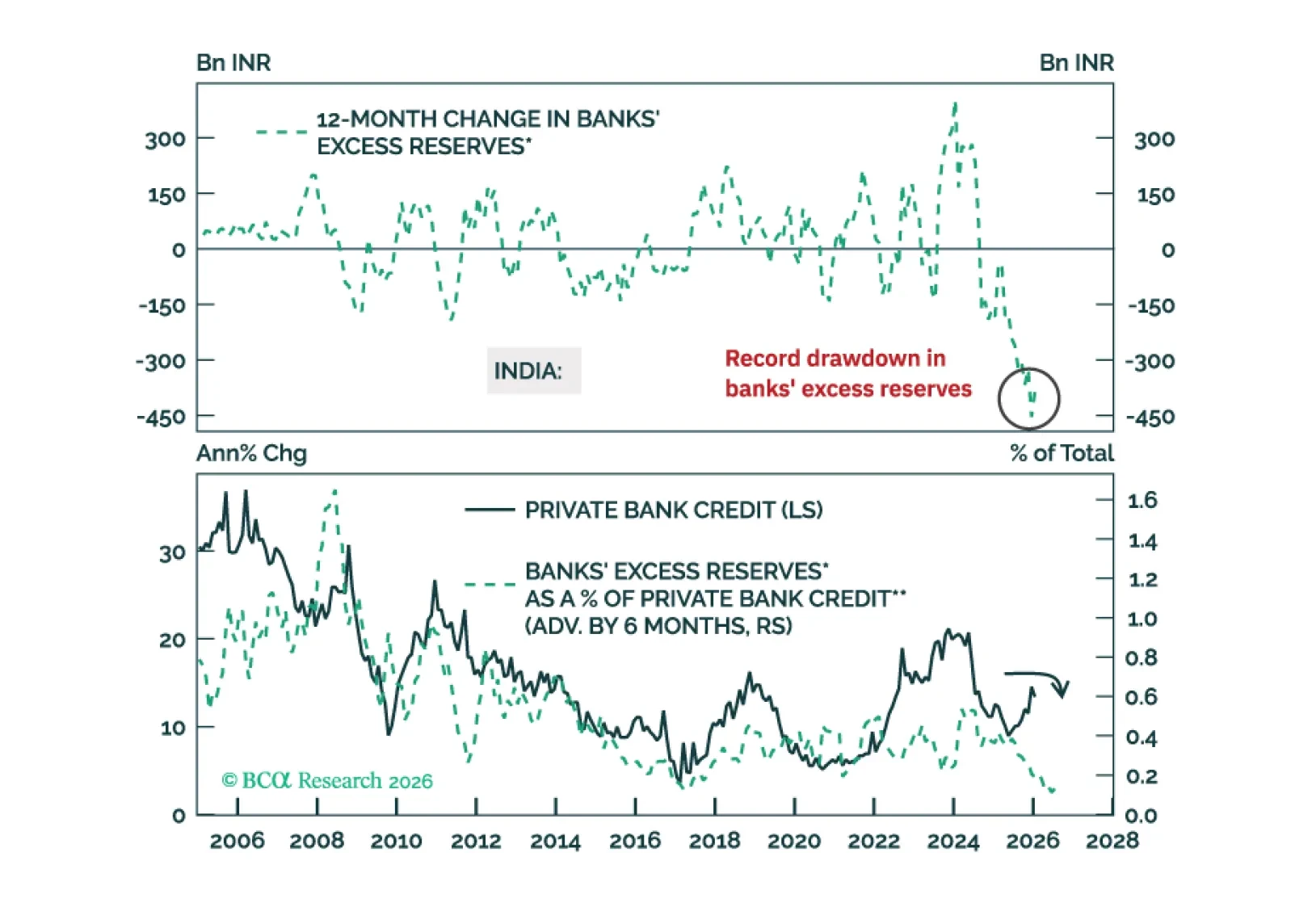

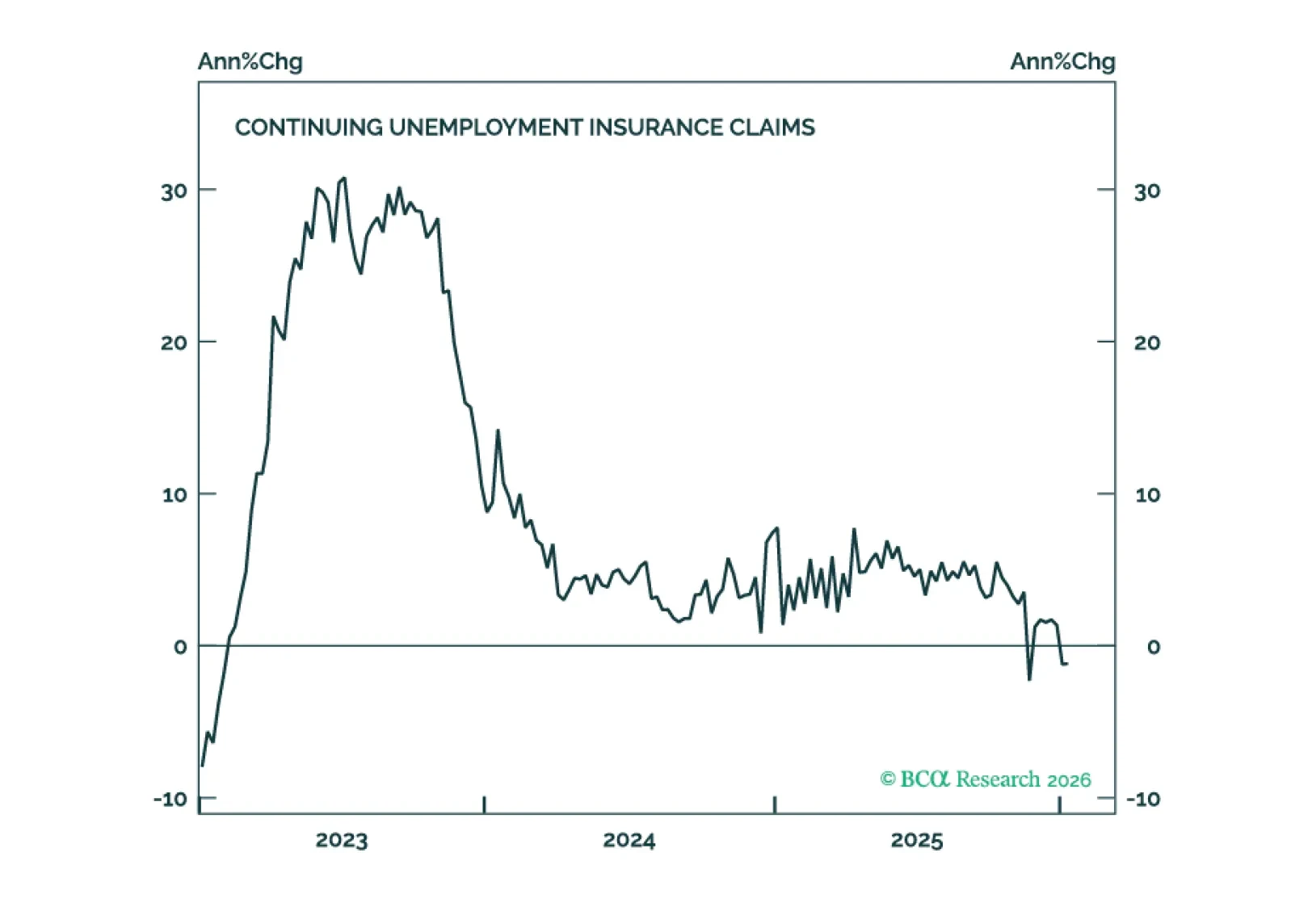

India is seeing net capital outflows for the first time in a generation. The central bank is selling foreign reserves to defend the rupee, which is draining banking system liquidity. The latter risks derailing the nascent credit revival. Indian stock prices remain vulnerable.

Our Portfolio Allocation Summary for February 2026.

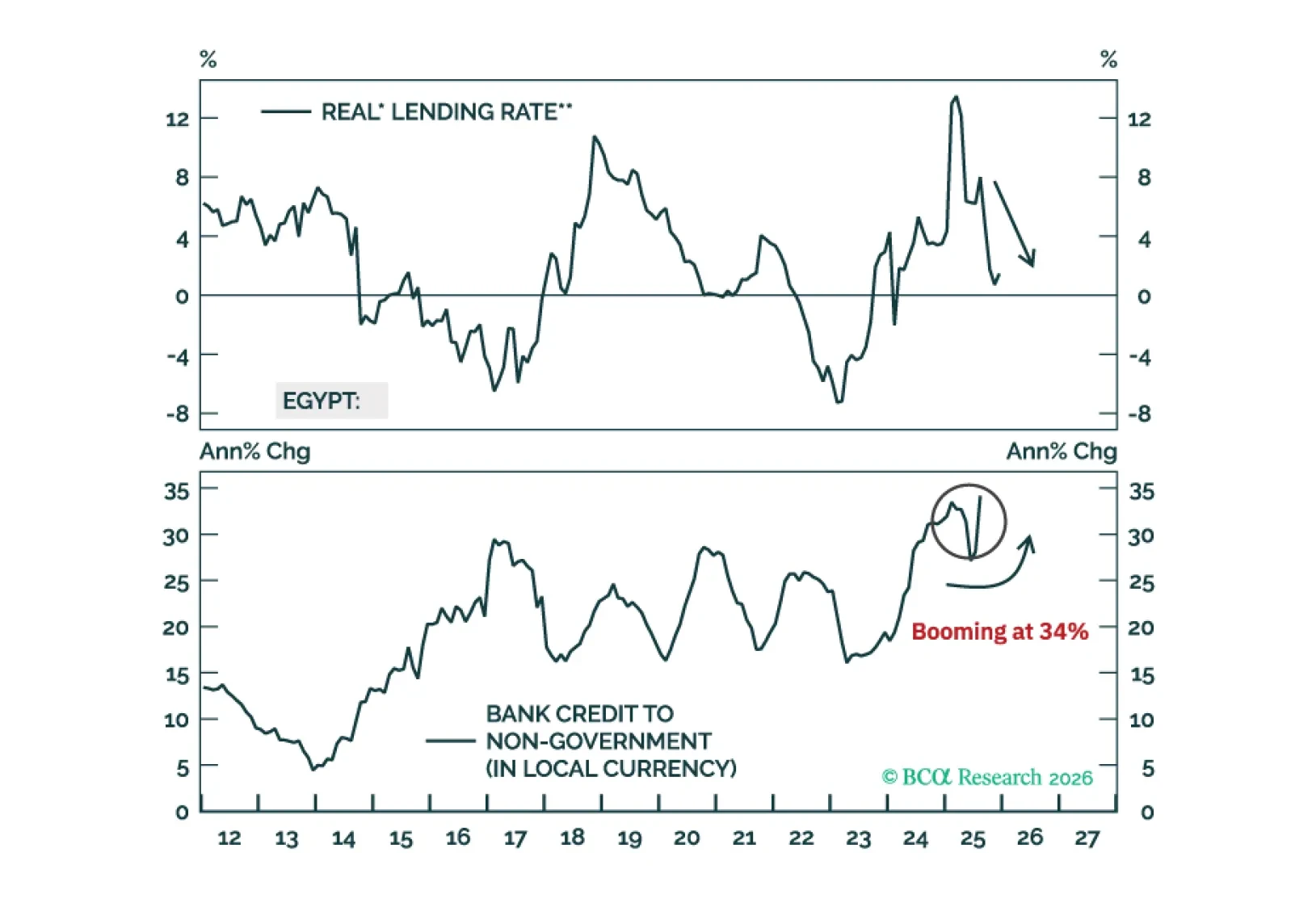

Egypt’s underlying inflation pressures are much higher than the headline CPI numbers imply. Real interest rates have plunged. As such, domestic bond yields have stayed high for a reason. Steer clear.

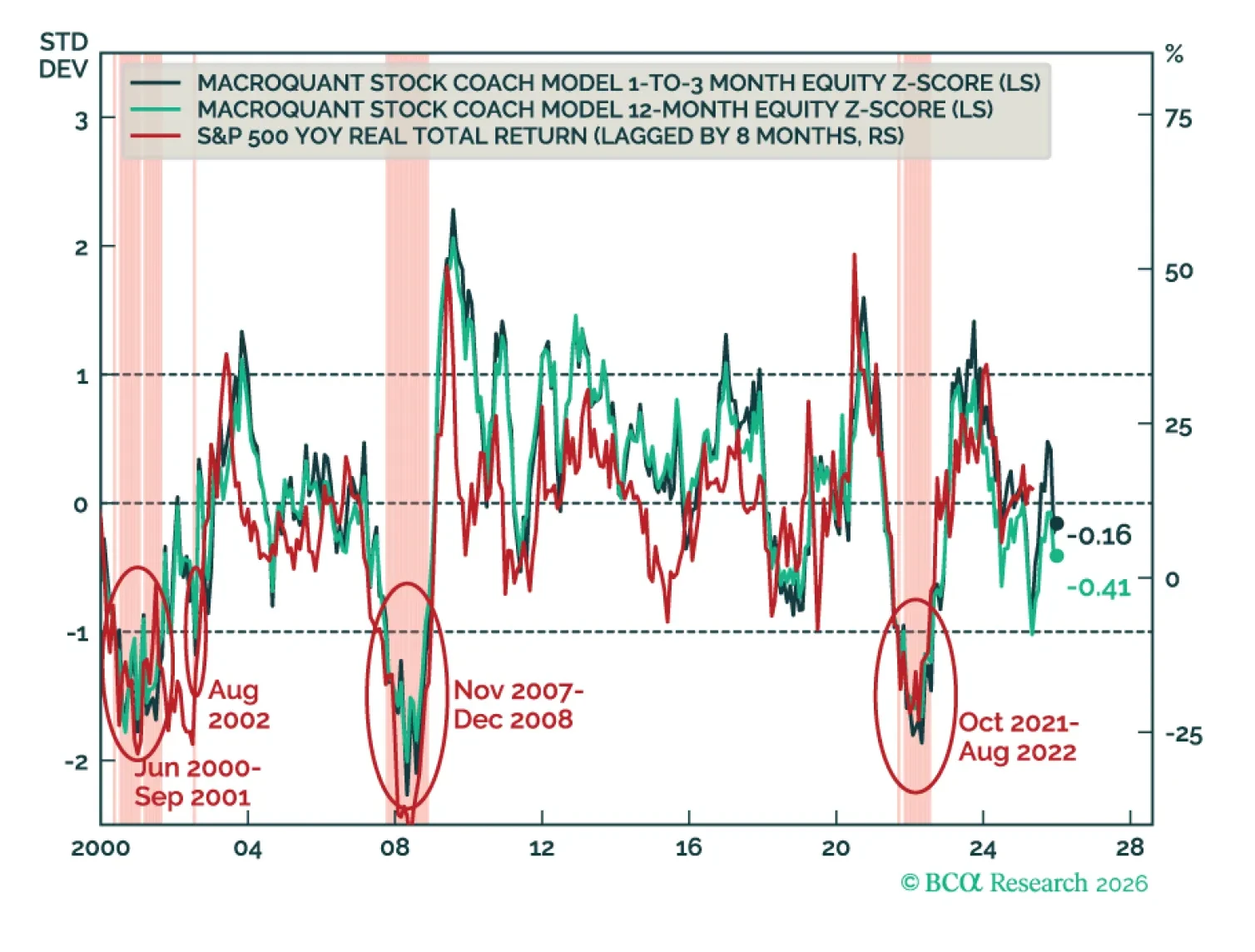

MacroQuant recommends a slight underweight in equities, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has upgraded oil and copper to overweight, and is bullish on gold.

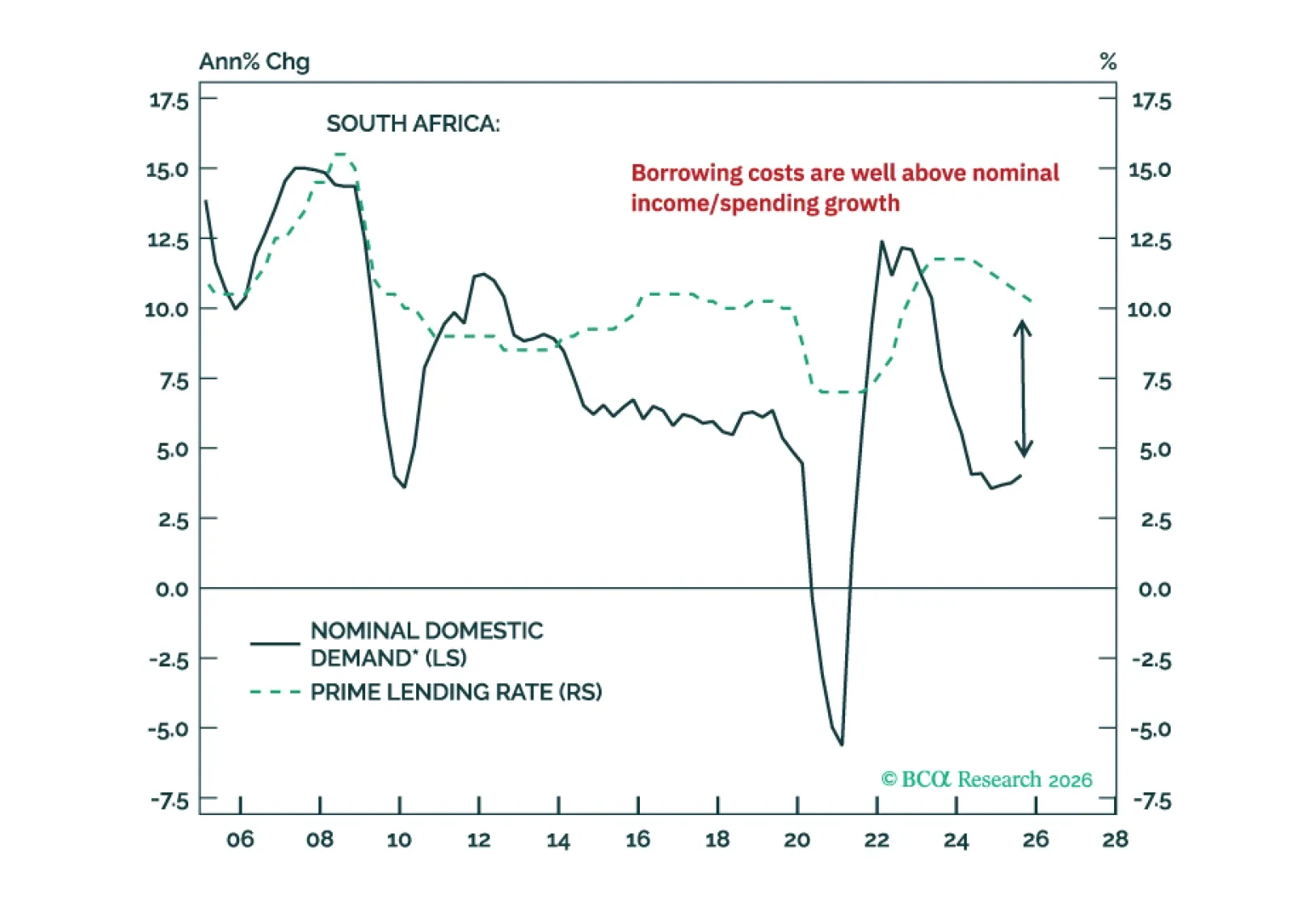

The precious metal bonanza has not resolved the South African economy’s plight. Nor did it improve its public debt sustainability issues. Investors should brace for a reversal in South African stocks, bonds, and the currency.

Our Portfolio Allocation Summary for January 2026.

At major technical crossroads, markets eitherpull back before staging a sustainable breakout, or attempt to break out only to drop considerably (i.e., a fakeout). We believe the latter dynamics are more likely to play out.