Emerging Markets

China has notably diversified its export markets over the past two decades, reducing its dependence on the US and other DM economies and strengthening trade ties with EM nations. Since 2000, shipments to the US have halved (from 30% to 16% of total…

The Asian currency index (ADXY index) rose nearly 3% from its late-July lows. While CNY/USD accounted for a large share of these gains, an equal-weighted basket of non-CNY Asian currencies surged by an even larger margin (5%) indicating that Asian currencies’…

According to BCA Research’s Commodity & Energy Strategy service, oil markets are caught in a tug-of-war that has kept oil prices in a trading range since H2 2023. Bearish demand concerns are enforcing an upper limit on the price of crude while bullish…

Chinese industrial profits rose by 4.1% y/y (3.6% YTD y/y) in July, from 3.6% (3.5%) in June. Upstream mining industries’ profits contracted 9.5% from January to July 2024, whereas downstream manufacturing sectors’ profits rose 5.0%. The NBS reported that…

Brazilian equities have largely underperformed their EM peers in USD terms since the beginning of the year. Rising public debt and inflation are the two main forces weighing on the Brazilian bourse. Our Emerging Market strategists expect public debt-to-GDP…

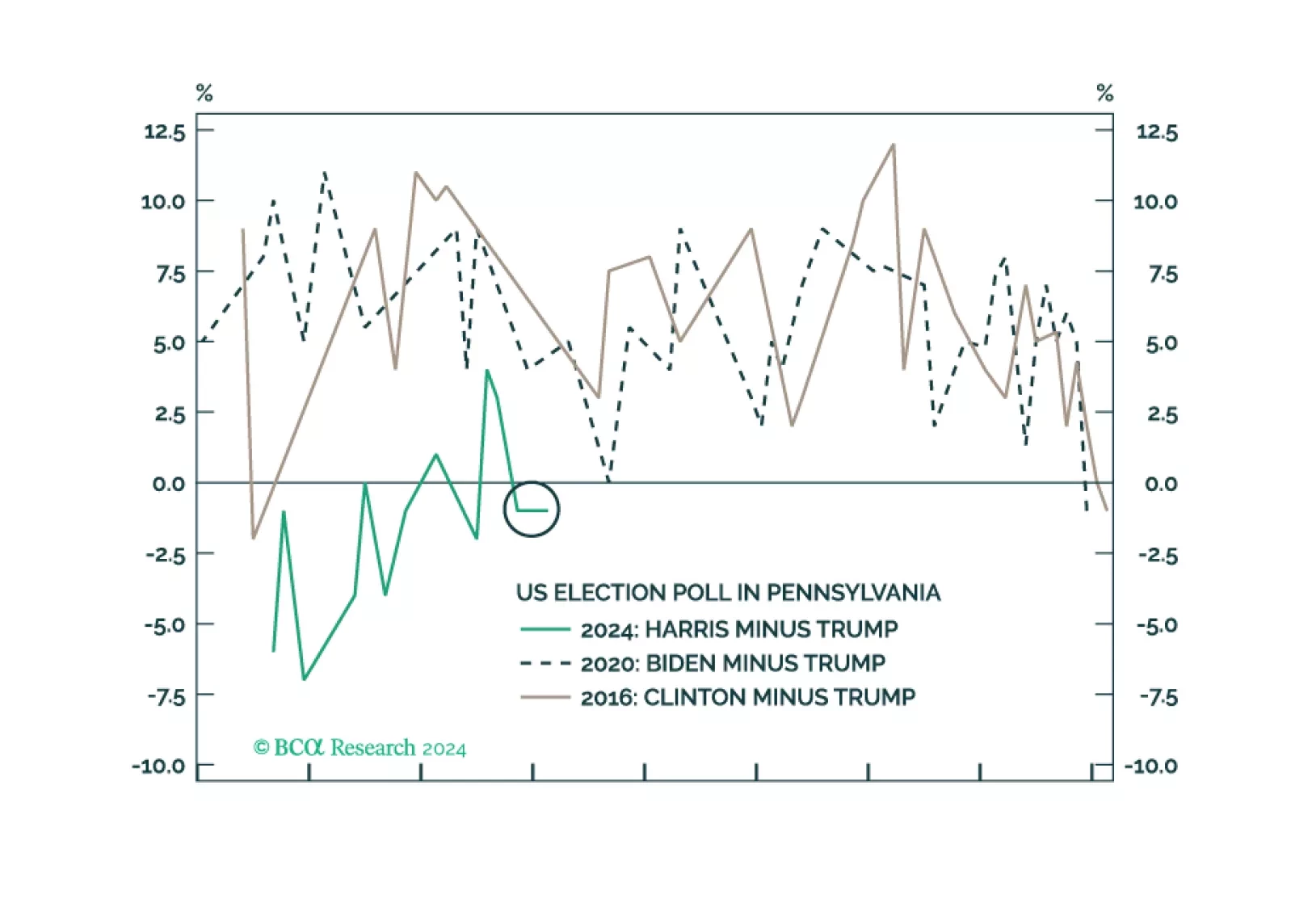

According to BCA Research’s Geopolitical Strategy service, the logic of pursuing one’s interest against US interests in the final hours of the election mostly applies to states that will suffer a significant loss to their strategic security if the…

Investors should buy protection against further volatility. The shakeup in early August was a taste of things to come. The US election is a pivotal moment in modern history that will drive up uncertainty, while other countries take advantage of US division and distraction.

EM equities have dramatically underperformed their US and Eurozone peers in USD terms over the past 15 years. The inability of EM and EM Asia companies to grow their EPS largely explains EM equities “lost decade” (and a half). Since 2010, US EPS have grown…

According to BCA Research’s Commodity and Energy Strategy service, soft oil demand growth raises the likelihood that OPEC+ will back down from its plan to begin unwinding some of its production cuts later this year. However, investors should not read this as…