Emerging Markets

China’s economy is cruising at a very low altitude. The odds are that China’s equity rebound is running out of time. The RMB will continue to depreciate versus the US dollar in the coming months, albeit the pace may be modest.

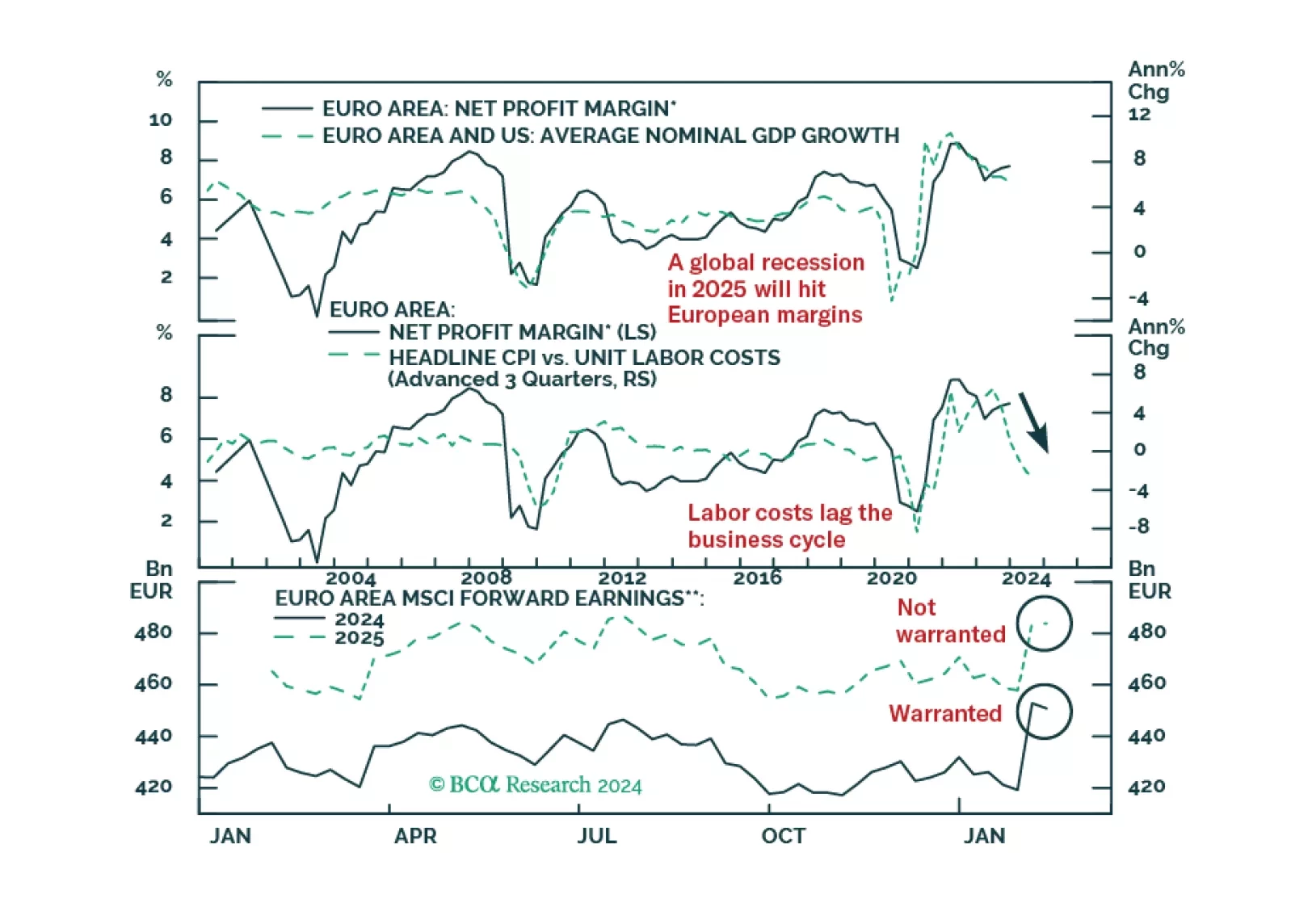

European profits margins are elevated. Will a mild recession be enough to bring them down?

The implication is that Israel chose not to escalate the risk of direct war with Iran. Hence we remain in our base-case “Minor War, Minor Oil Shock” scenario.

This year’s rise in commodity prices represents a blow-off rally rather than the start of a durable bull market. The global economy is heading for a recession. Stocks, commodities, and other risk assets are vulnerable.

Our quant models suggest Democrats are still slightly favored for the White House. Our Senate model favors Republican control, though Montana and Ohio are the weak links that could deliver Democrats a de facto Senate majority in the event they keep the White House. But there are still six months before the vote. An oil shock from the Middle East or other negative economic news would force a major change to these models.

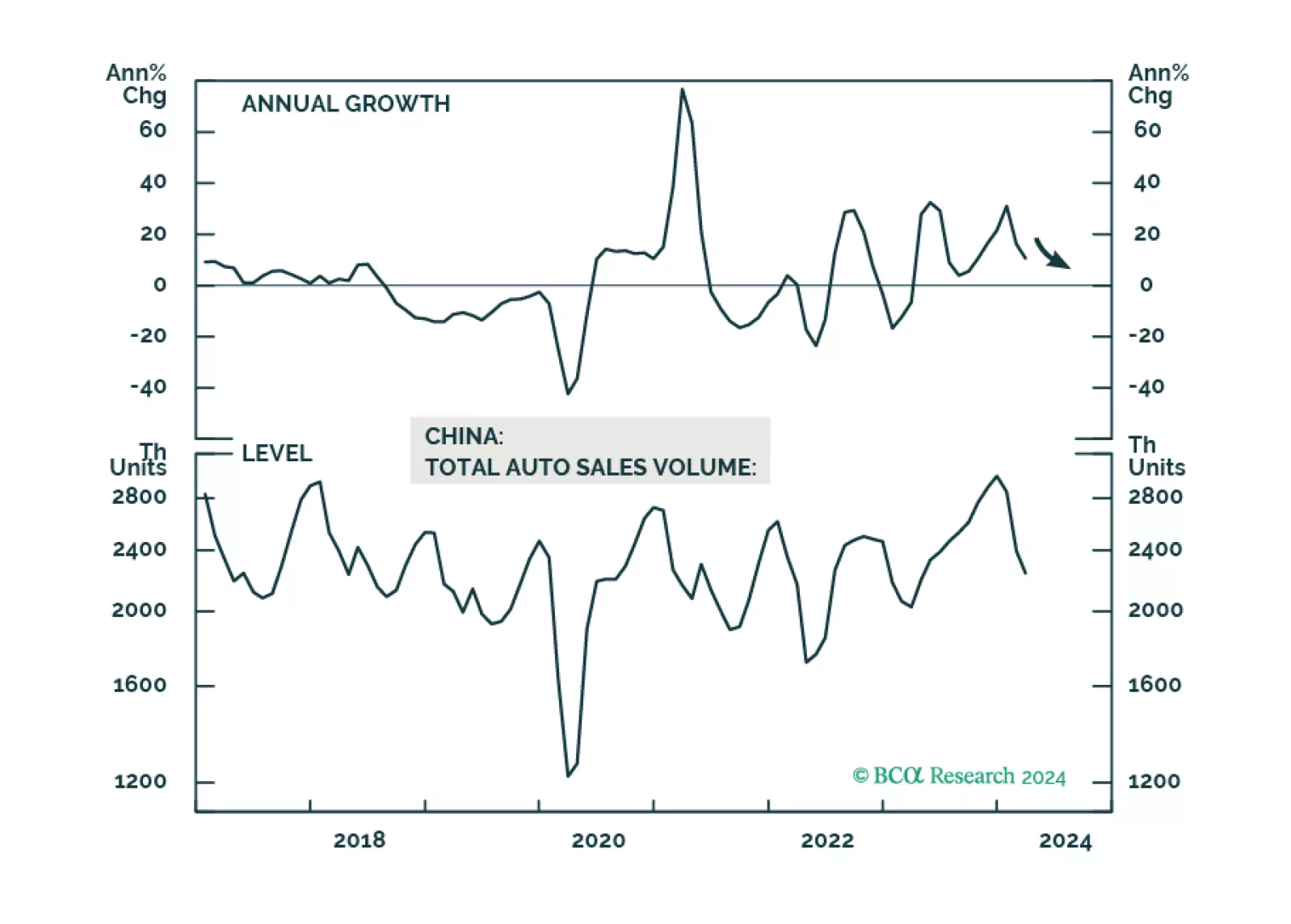

This year’s cash for clunkers program will have only a mildly positive impact on domestic demand for automobiles and home appliances in China. In the meantime, the equipment renewal program will prop up domestic manufacturing moderately as well as help the country reduce its reliance on high-end equipment imports. We recommend continuing to overweight onshore auto stocks relative to the A-Share Index.