Energy

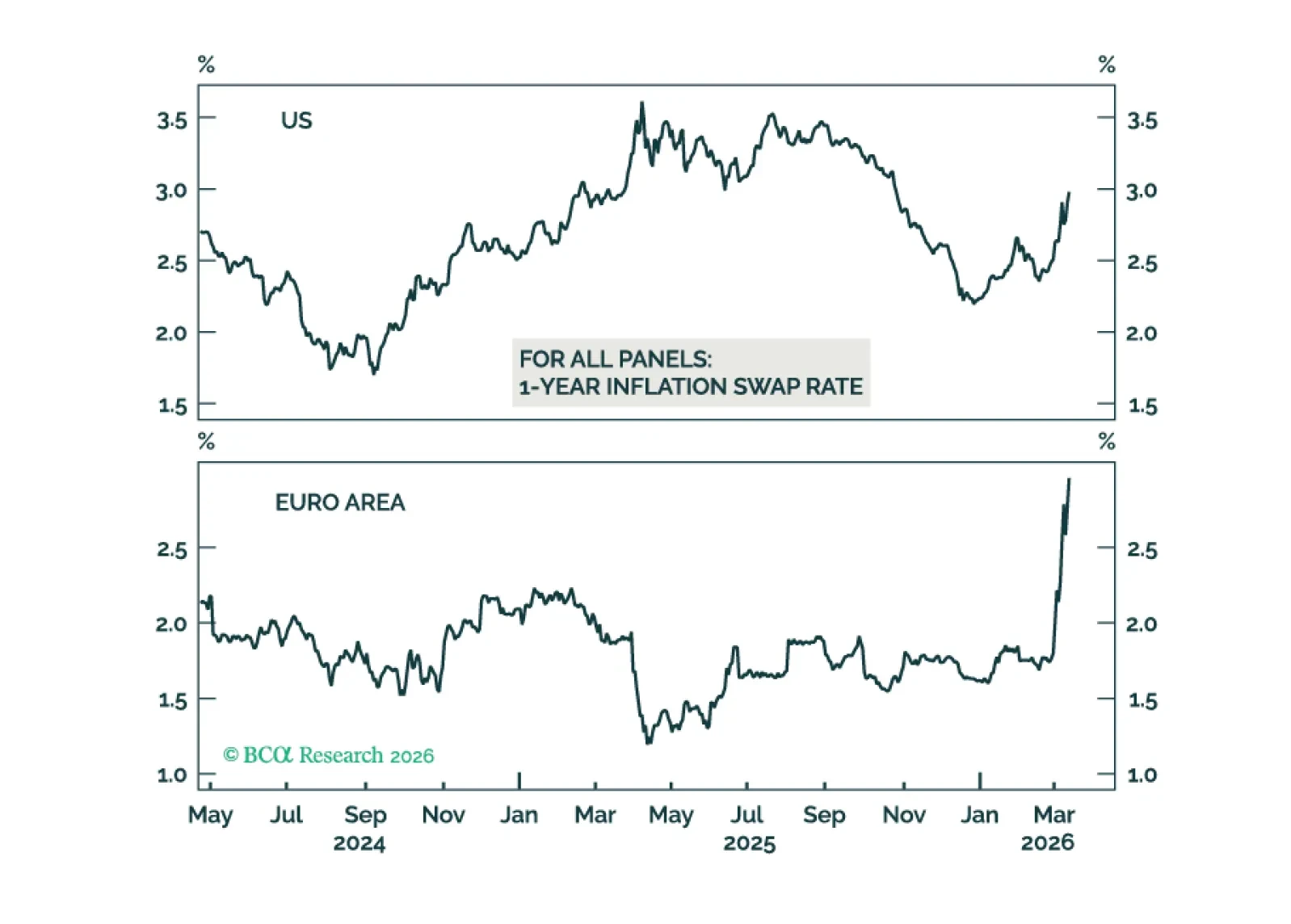

War momentum and escalating rhetoric around the Strait of Hormuz have pushed Brent above $100 and raised the risk of a broader supply shock. While parallels with 2022 offer a roadmap, today’s shock is likely shorter but more globally disruptive. Markets are repricing monetary tightening risks, though we see rate hikes as a mistake absent second-round inflation. Beyond oil, sulfur, helium, and fertilizer disruptions threaten food prices and the AI supply chain. Position defensively.

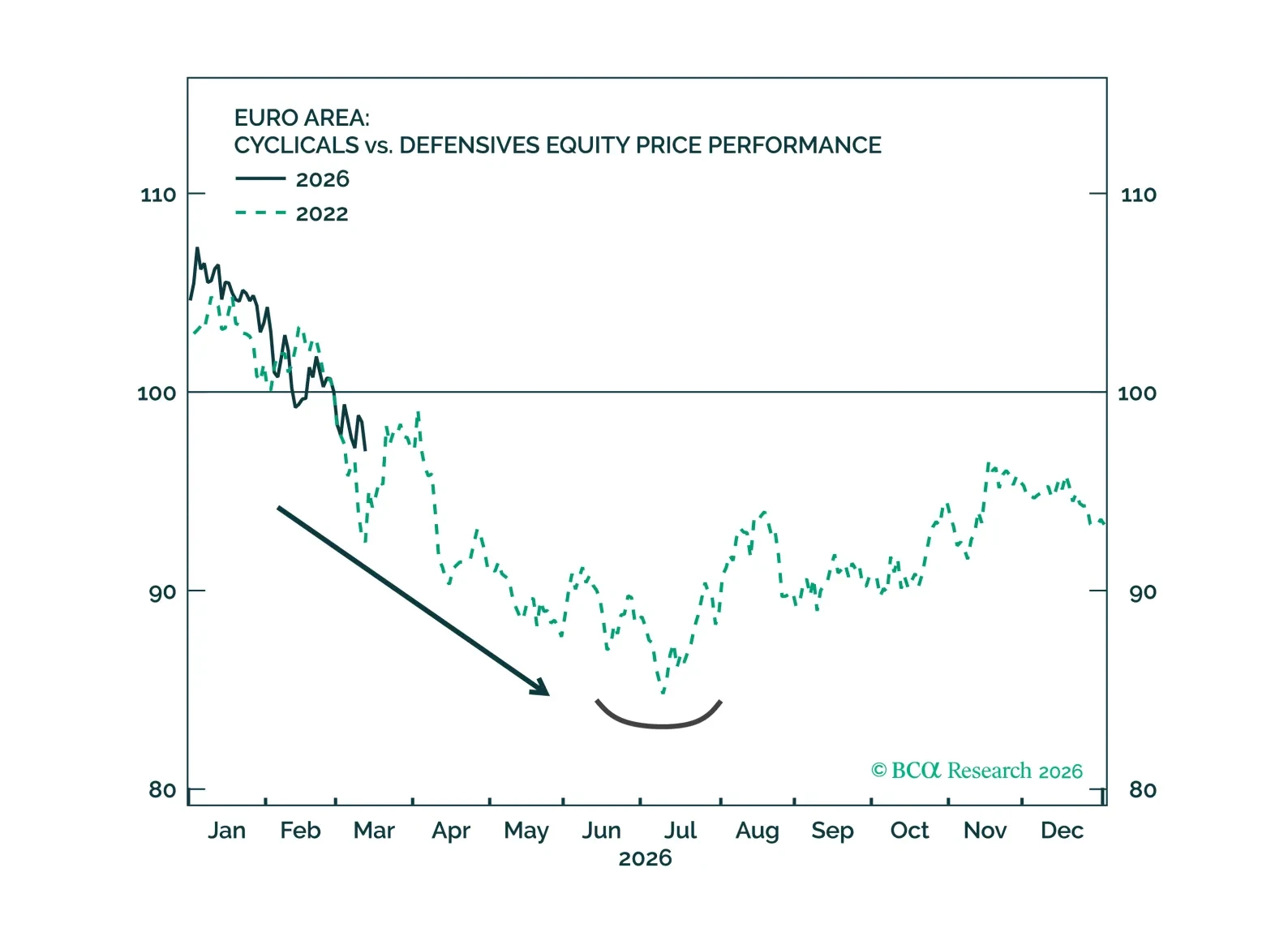

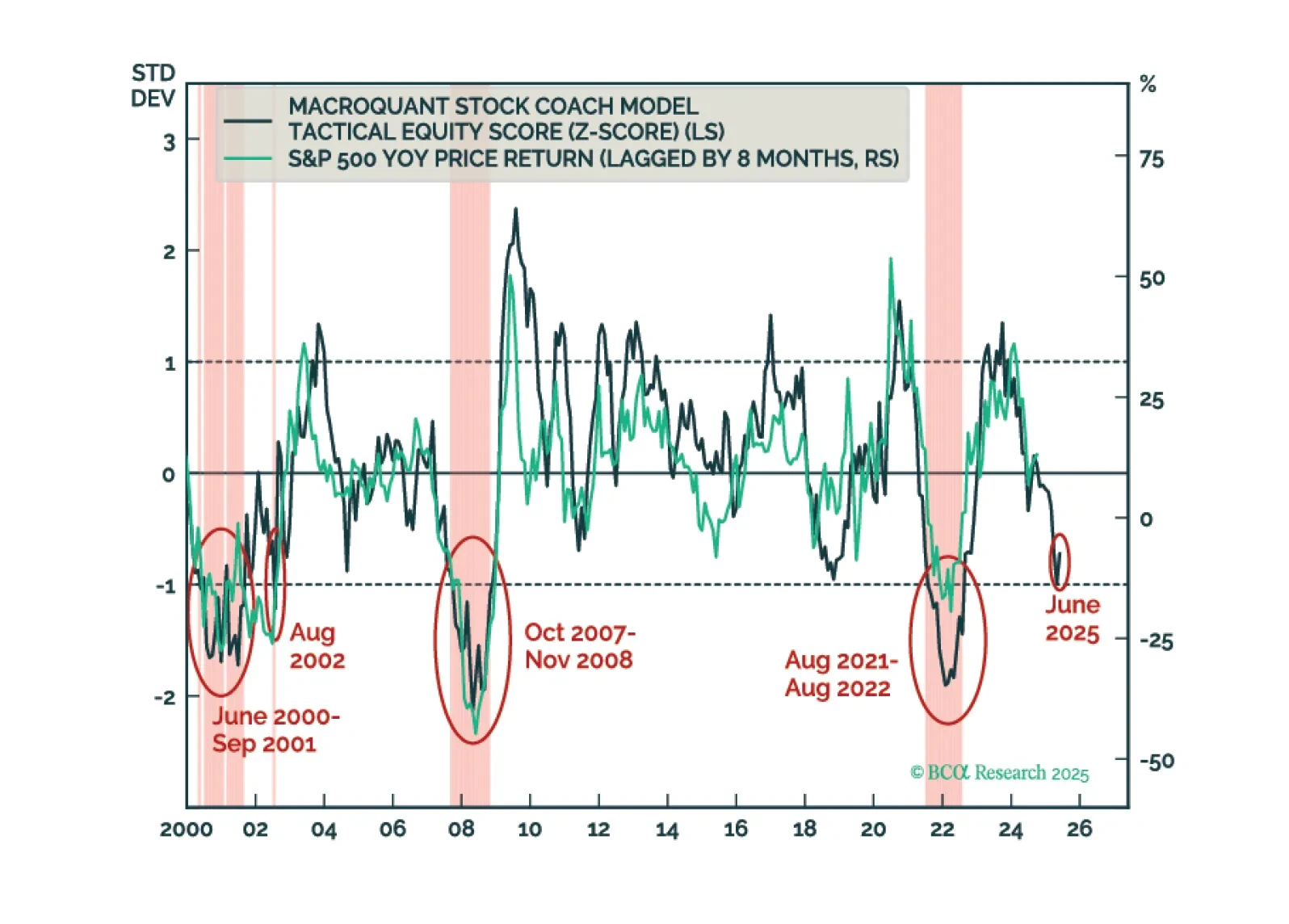

The spike in oil and gas prices has raised the odds of a global economic downturn. Combined with a more negative signal from our MacroQuant model, this warrants tactically downgrading stocks from neutral to underweight. Looking further ahead, the Iran war will lead to bigger defense budgets and a greater focus on energy self-sufficiency.

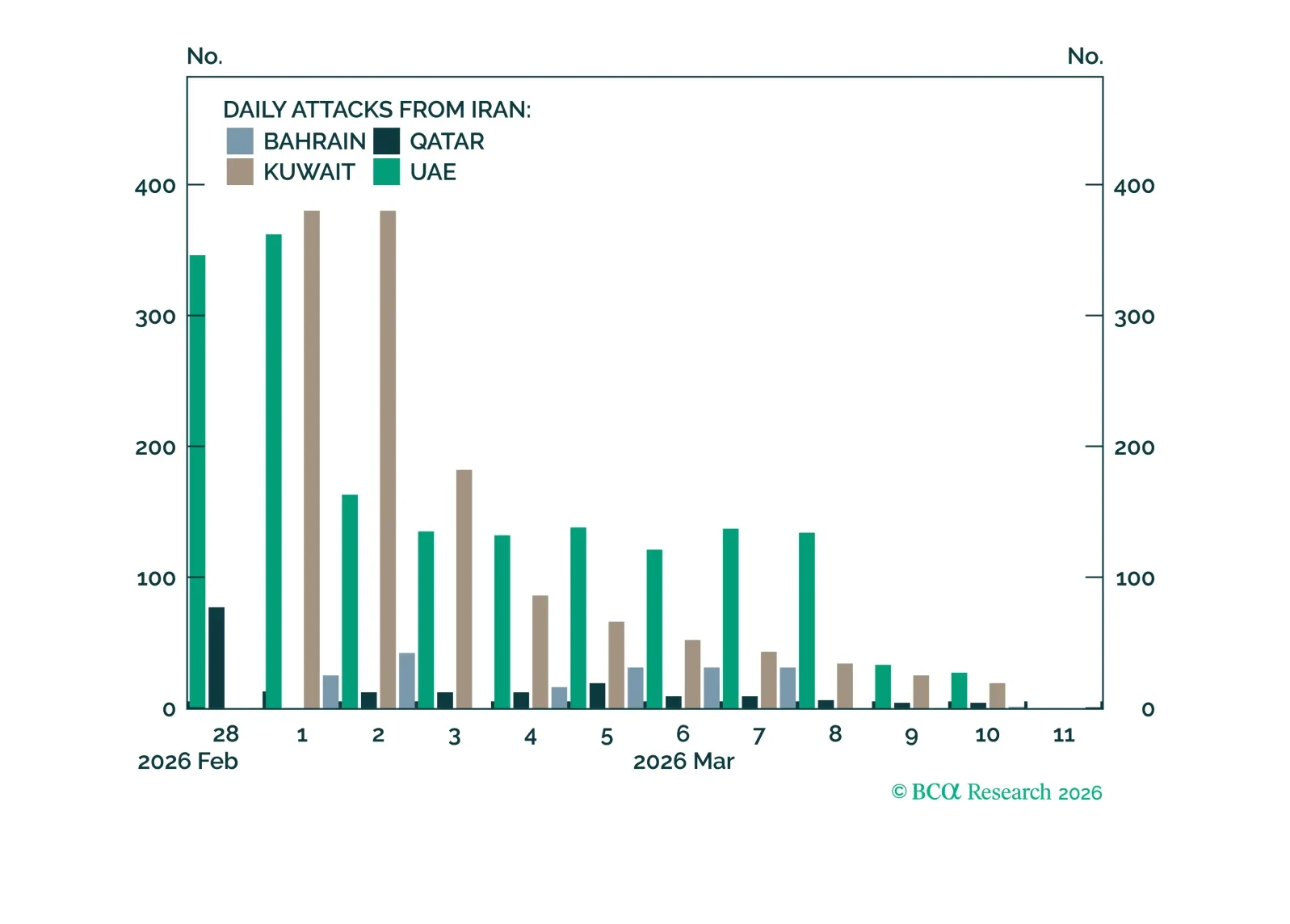

With all eyes on the Strait of Hormuz, BCA Research has created a dashboard of data for your convenience.

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.

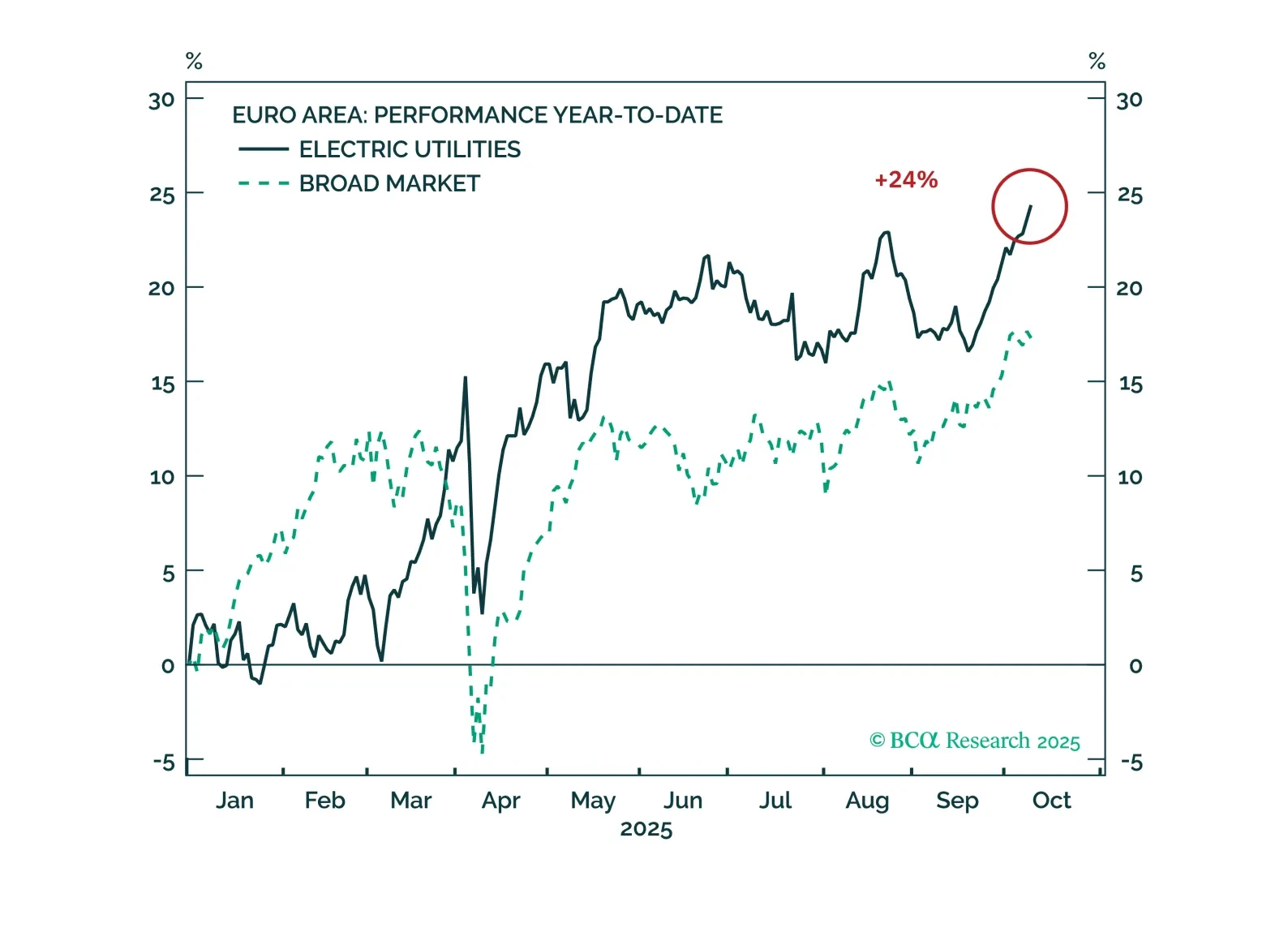

The structural demand base for electricity is expanding, requiring massive investment in grid capacity, storage solutions, and renewable generation. For investors, this trend highlights long-duration opportunities in utilities as electricity responds to the ever-growing needs of data centers and becomes the backbone of Europe’s decarbonized growth model.

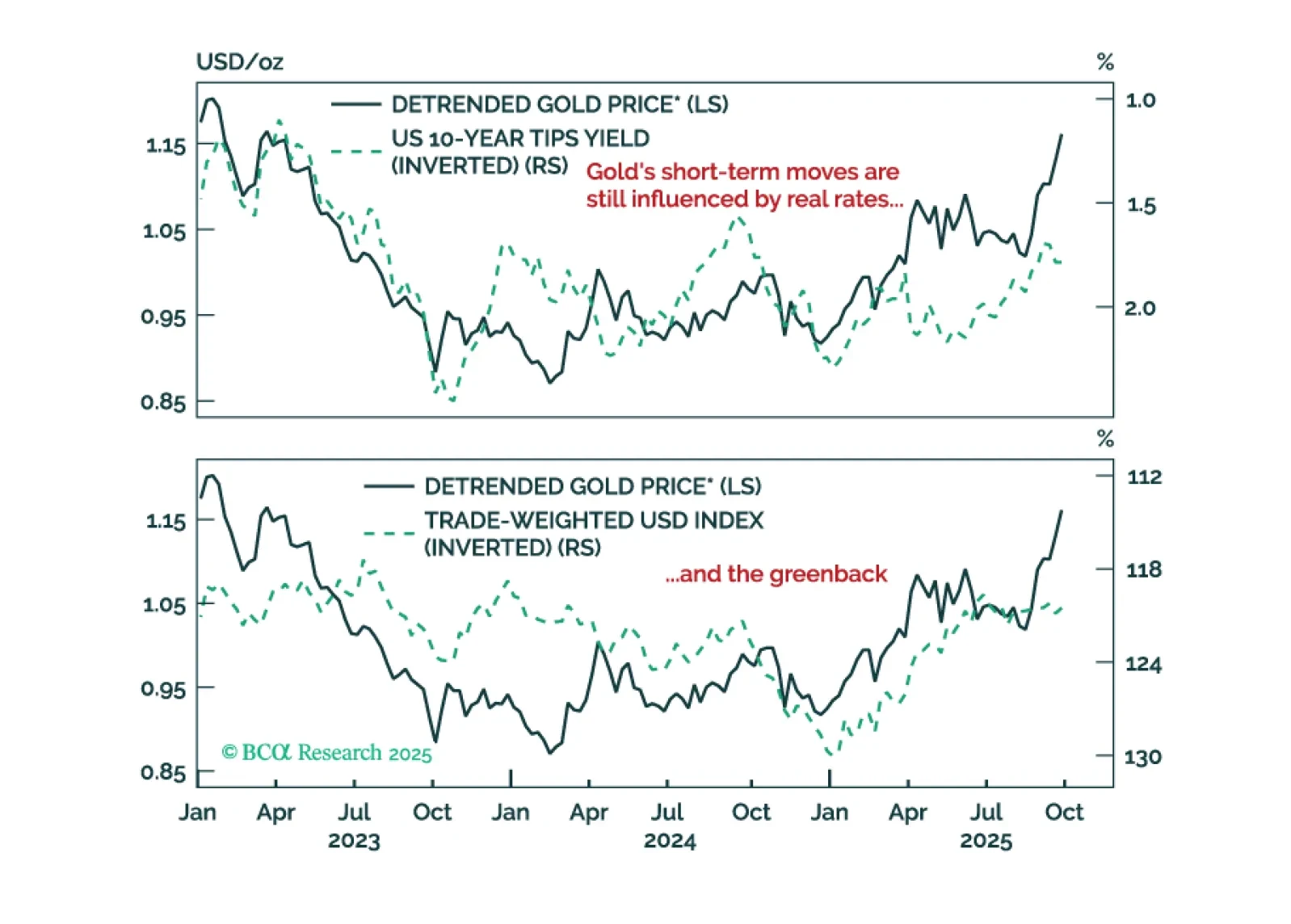

Commodity market breadth would need to improve for it to signal bullish conditions for the aggregate commodity complex. We maintain a defensive tilt within commodities, favoring precious metals over the more cyclically sensitive energy and industrial metals.

The Norges Bank will cut rates only once until year-end as the NOK weakens and inflation hovers around 3%. Expect aggressive easing next year as the economic recovery is delayed by weakness in the energy sector and the labor market deteriorates.

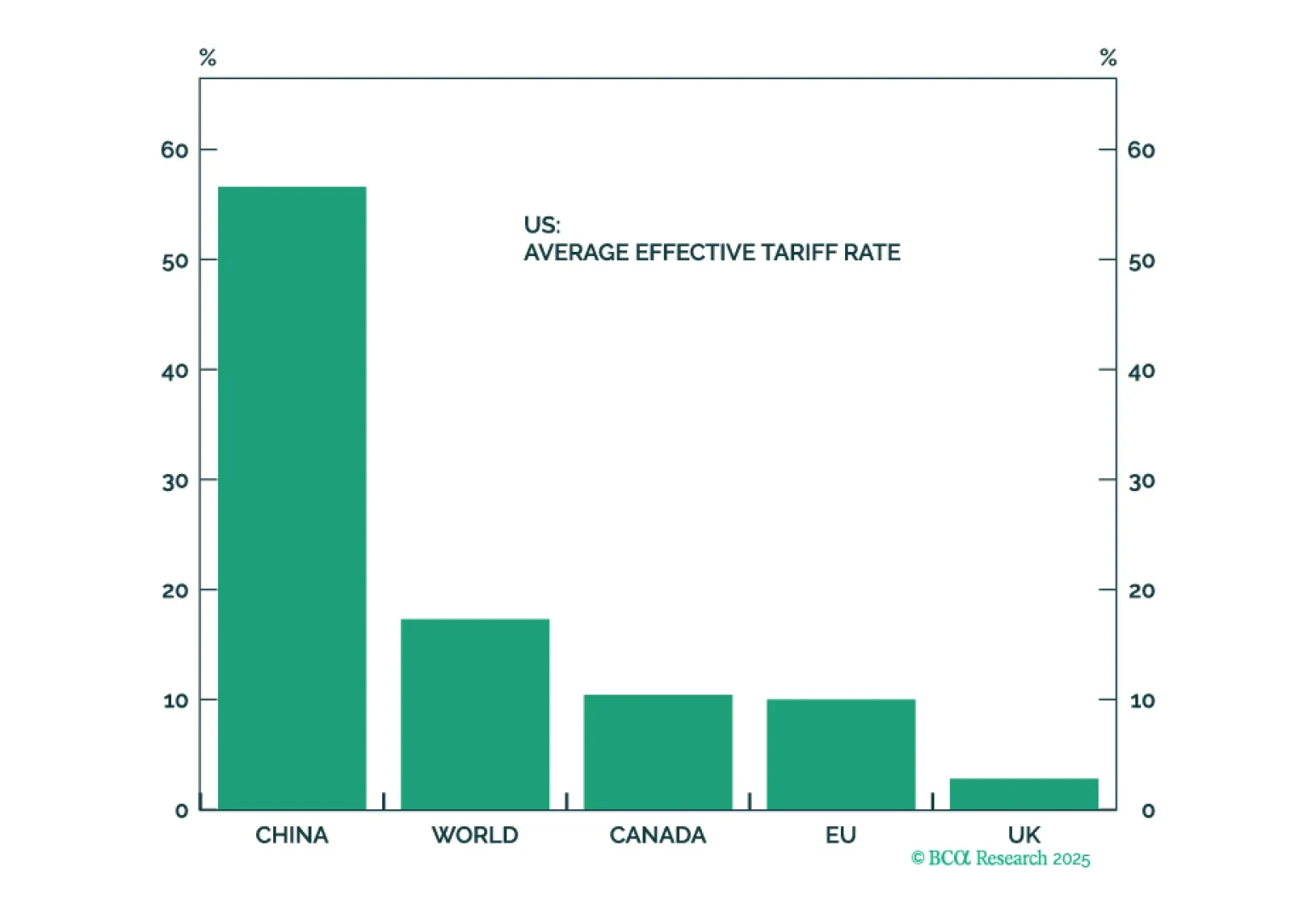

Acute geopolitical risks, like a massive oil shock, may be abating. But structural geopolitical risk remains high and could upset a blithe market. Cyclical economic risks are underrated as the US slows down and China continues to stumble. Investors should book some profits in anticipation of tariff implementation and a downturn in hard economic data.

MacroQuant’s US equity z-score is dangerously close to the -1 threshold. Moves below that threshold have reliably coincided with equity bear markets in the past. As such, MacroQuant recommends an underweight on stocks, offset by an overweight on bonds and cash.