Energy

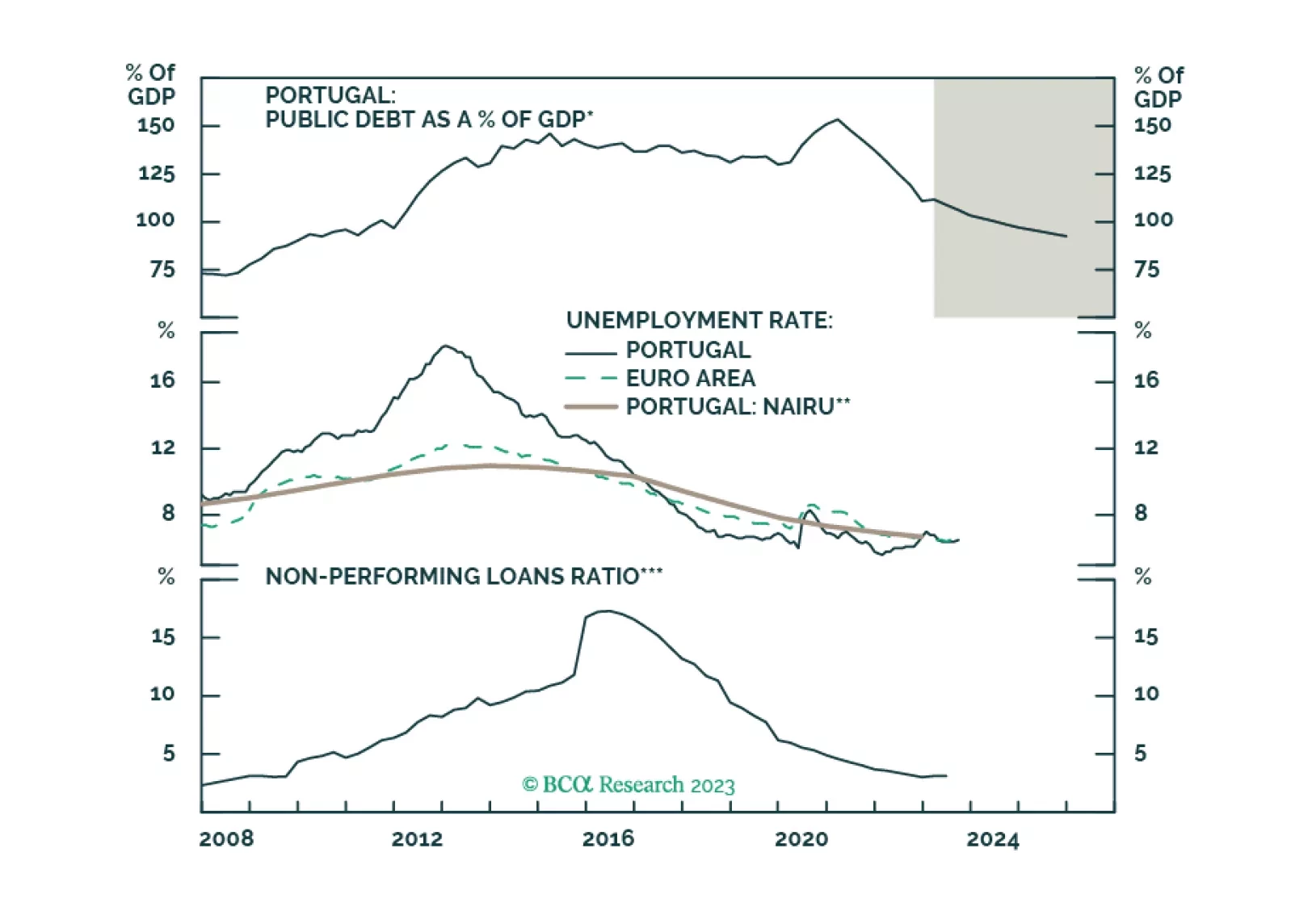

The first stop of the EIS Special Series: PIGS Have Wings takes us to Portugal.

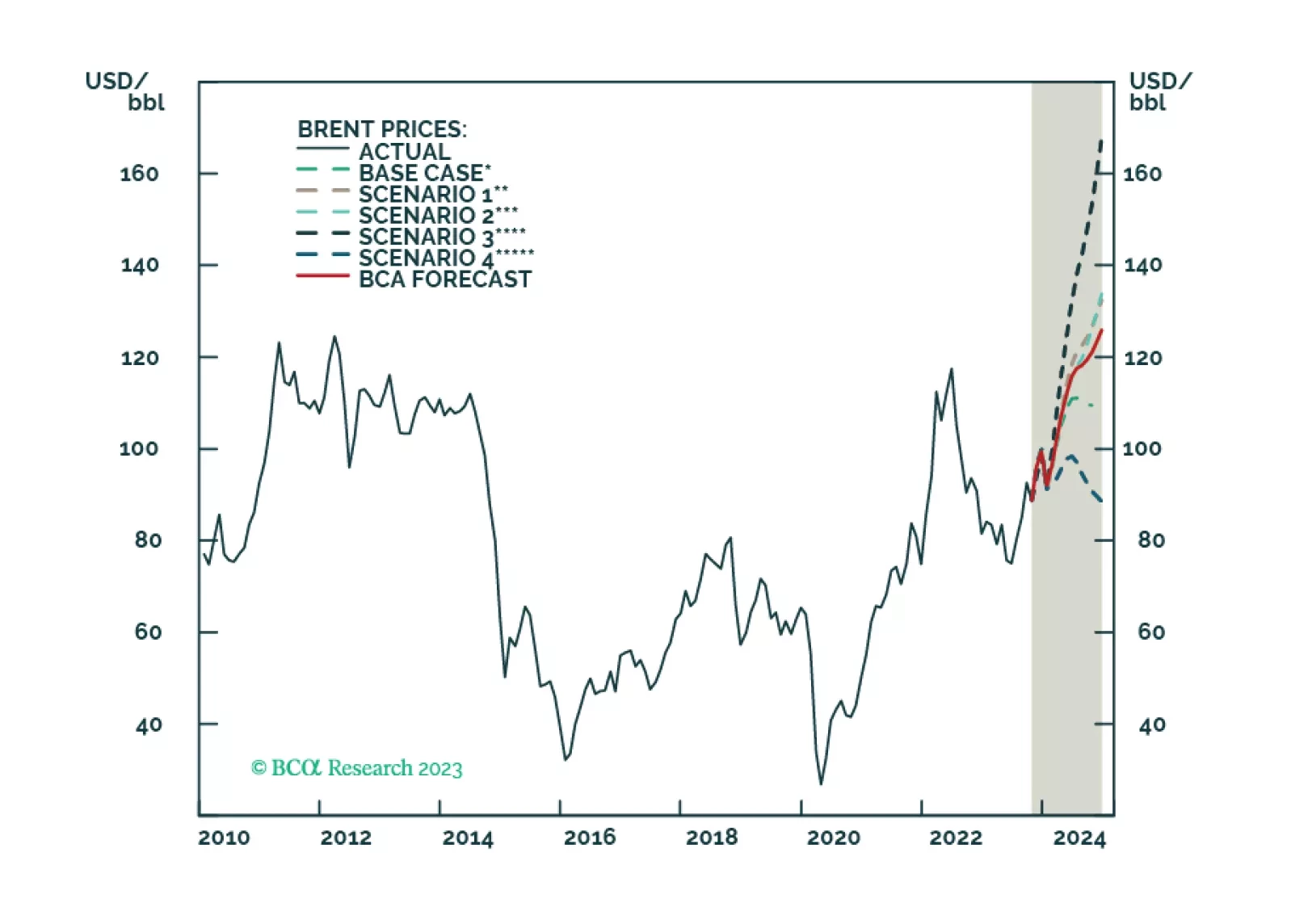

US and Chinese oil-demand strength will offset EU weakness next year. Incremental supply growth from non-OPEC 2.0 producers, coupled with a lower risk of the US enforcing its sanctions on Iranian oil exports, reduces our 2024 Brent price forecast by $6/bbl, and takes it to $112/bbl.

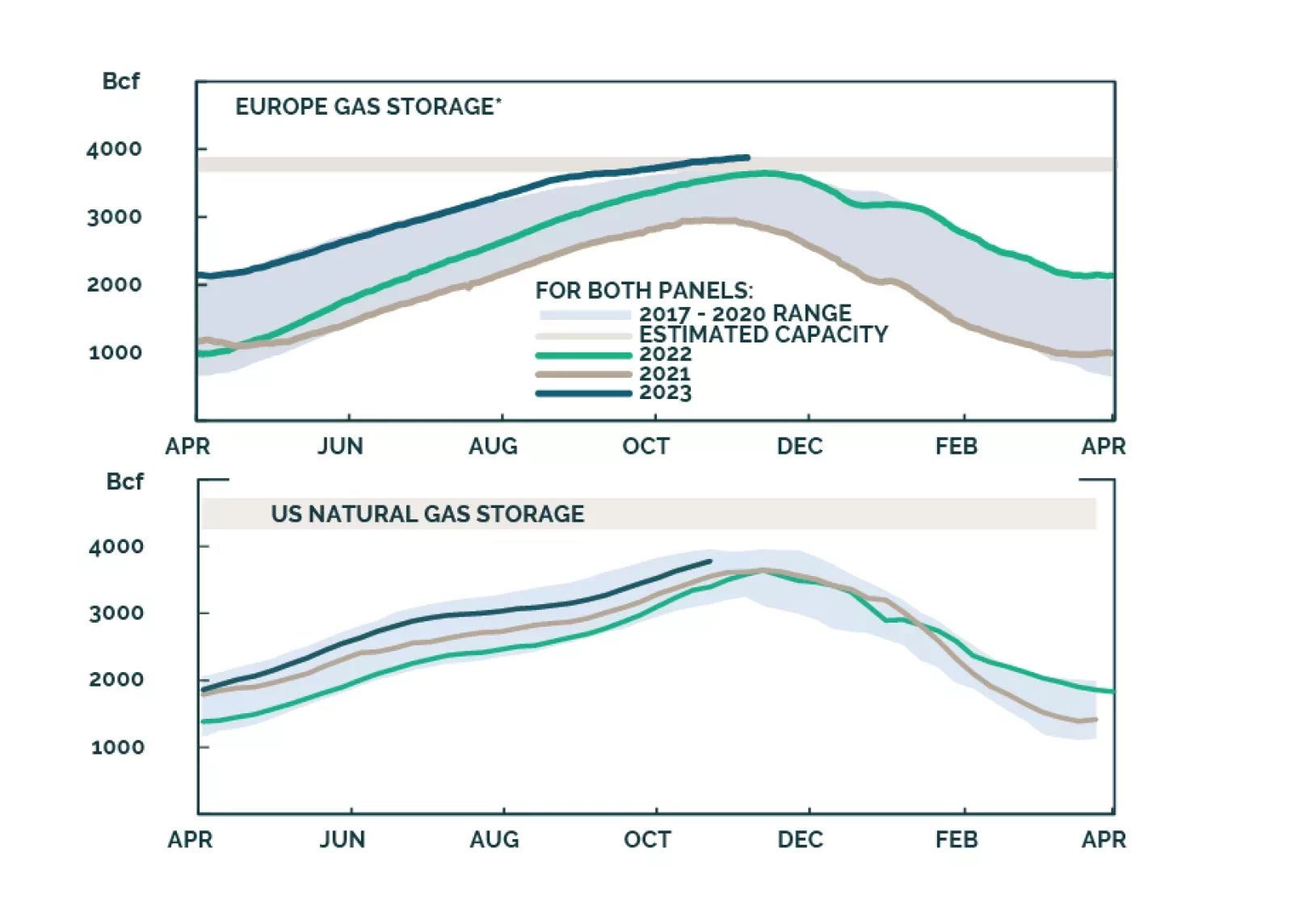

Natural gas storage levels in the US and EU are sufficient to balance flowing supply and demand this winter, assuming normal weather. China continues to invest in domestic production, and to diversify supply sources to compensate for a lack of storage. Longer-term Qatari contracts are giving higher weight to natgas trading hub prices. We remain long the XOP ETF to retain exposure to fossil-fuel producers supplying DM and EM economies with natgas beyond the 2050 net-zero-emissions goals advanced by the IEA.

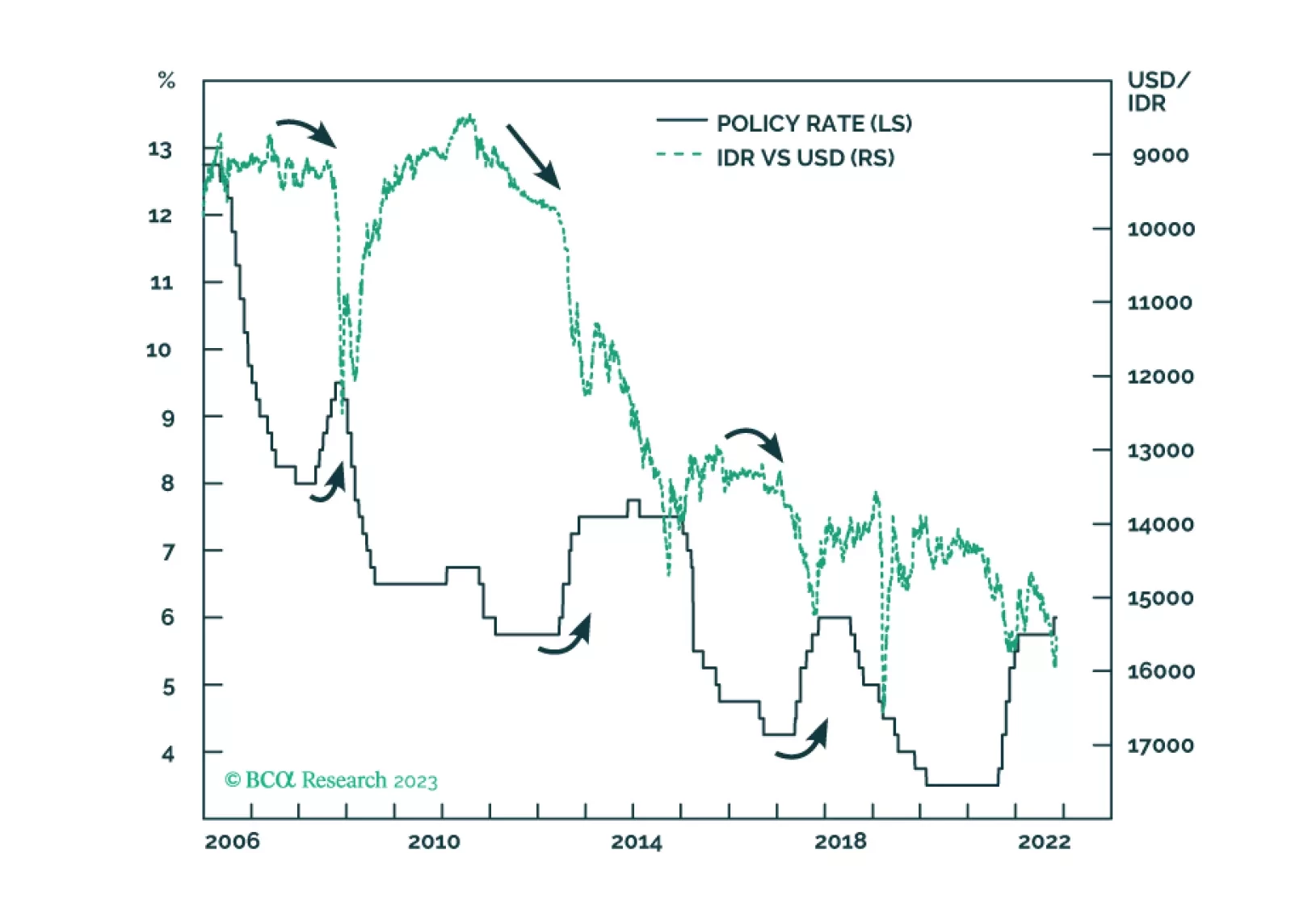

Despite very low inflation, Bank Indonesia raised its policy rates last month to support the currency. The strategy did not work before and will not work now. Stay short the rupiah.

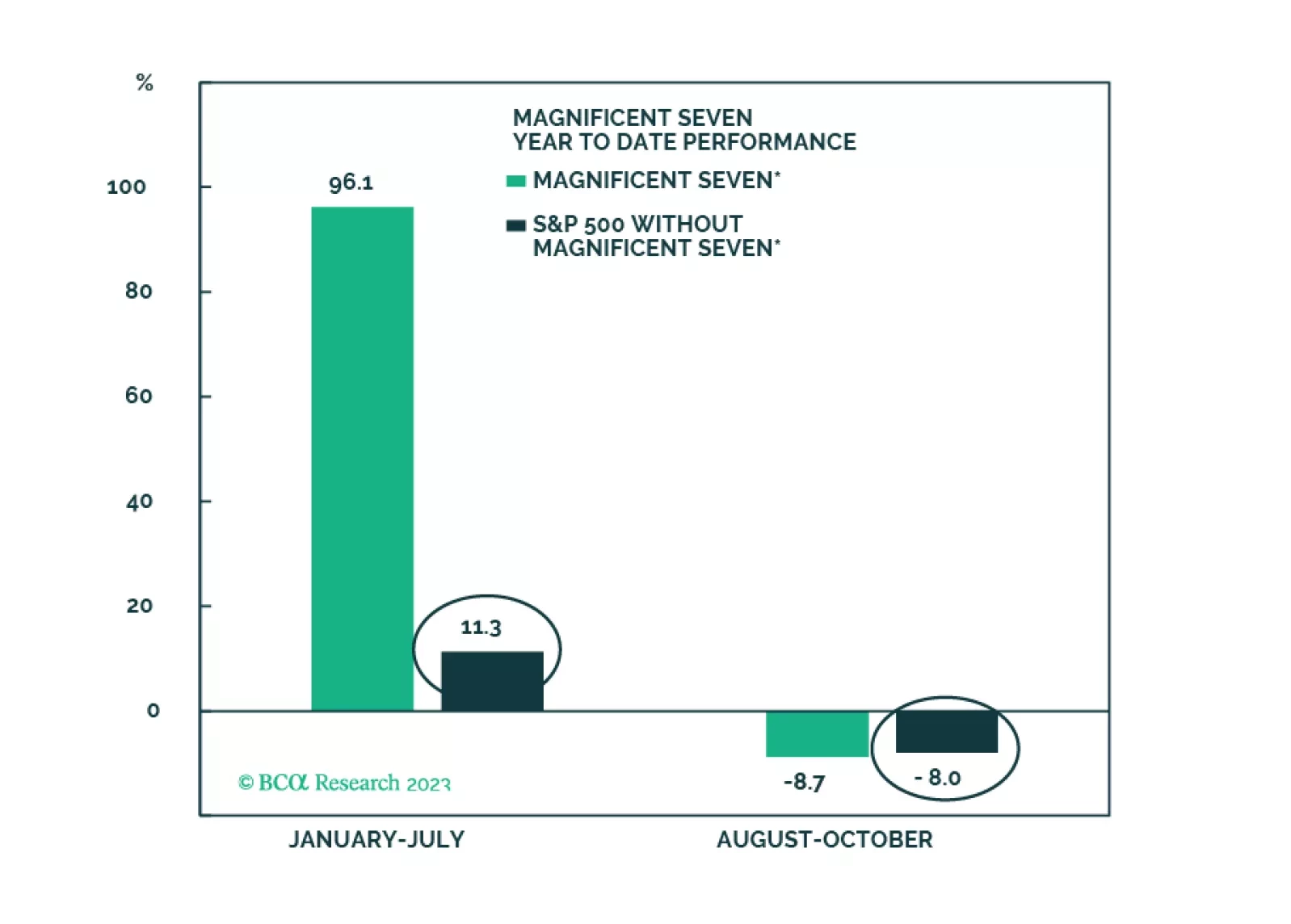

The Vicious Troika remains a long-term threat, but over the short term, rates will likely have another leg down on growth concerns, offering support to equities, which are now fairly valued and are no longer overbought. Longer-term outlook remains negative. The Magnificent Seven will likely lead a tactical rebound. Overweight Growth vs Value and FSemis.