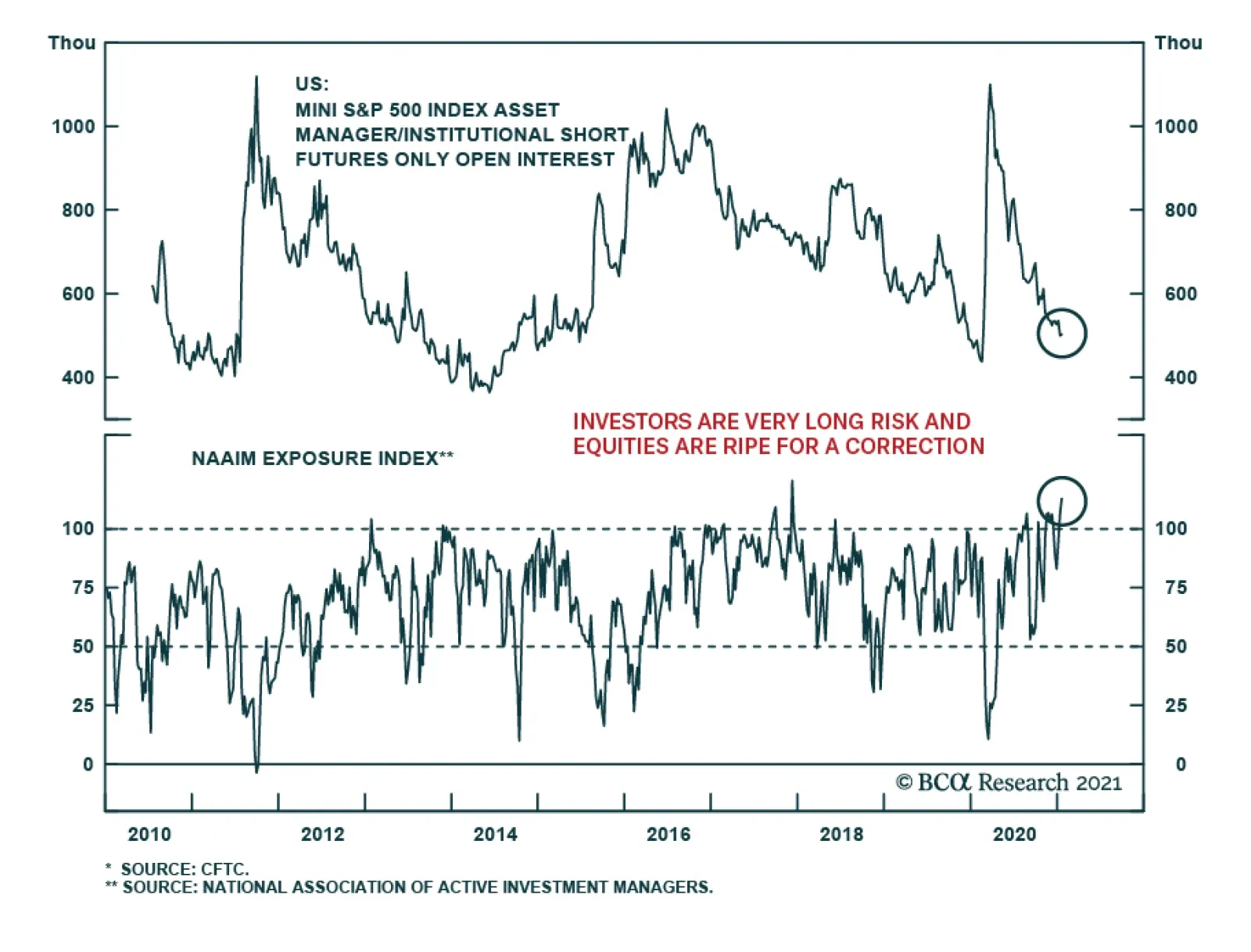

Equities

The dizzying gains attained over the past few days by the likes of GME, AMC and NAKD on the back of Reddit-engineered short squeezes have raised hopes of similar gains elsewhere. Instead, the message from market sentiment and positioning indicators is that…

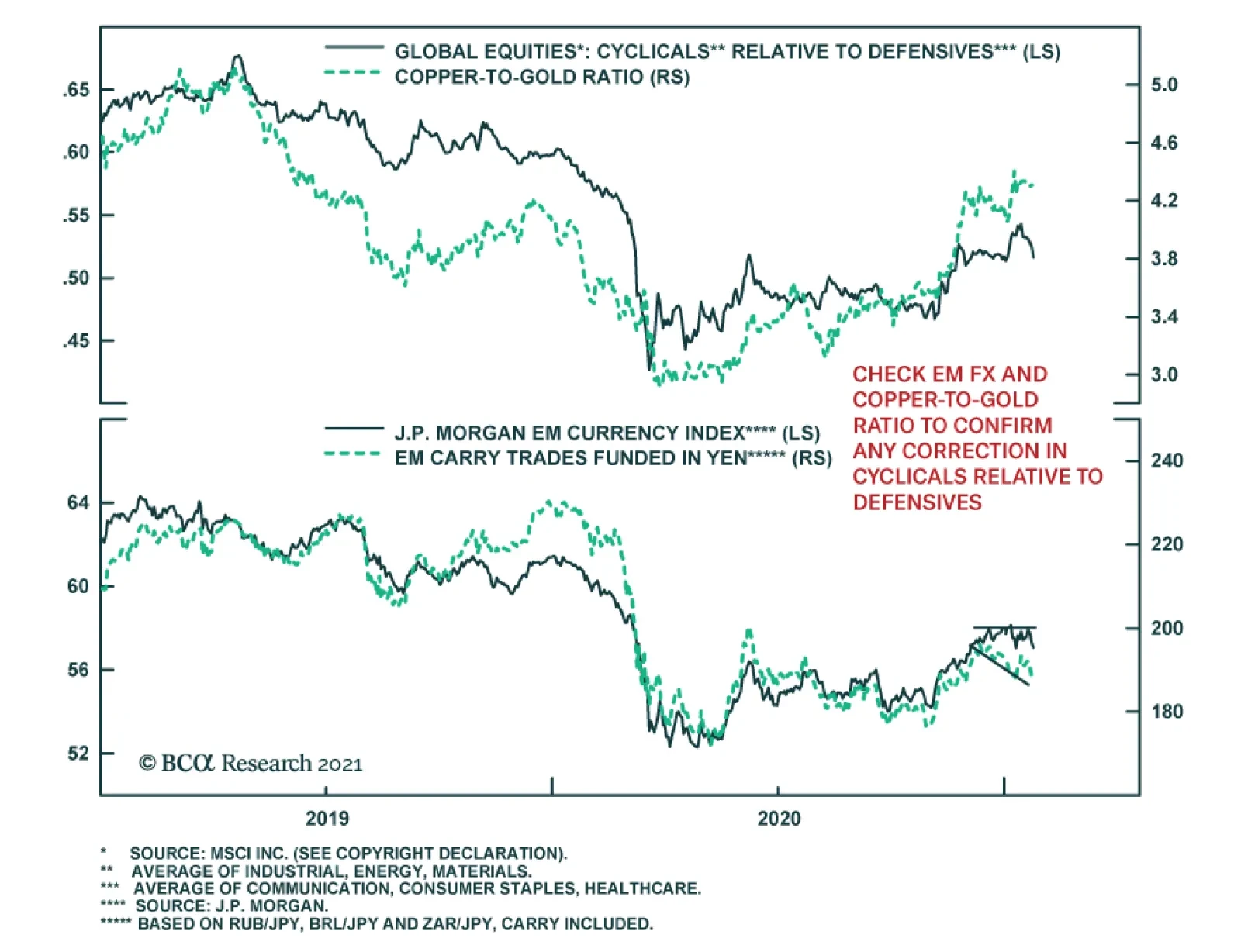

BCA Research’s Emerging Markets Strategy service concludes that the enormous size of US stimulus and overflow of liquidity is creating a thrill akin to riding a tiger. Remarkably, this kind of jubilation is very similar to what EM experienced in 2009-10. That…

Highlights The enormous size of US stimulus and overflow of liquidity is creating a thrill akin to riding a tiger. Remarkably, this kind of jubilation is very similar to what EM experienced in 2009-10. That was followed by a lost decade for EM. The US equity and bond markets as well as the economy have grown accustomed to constant stimulus – an addiction that will be very hard to wean off. Due to recurring stimulus, the US will experience asset bubbles and inflation in the real economy. The Fed will fall behind the inflation curve. The resulting downward pressure on the US dollar in the coming years favors EM stocks and fixed-income markets over their US counterparts. Feature Policymakers worldwide and in the US in particular “are riding a tiger”. Congress is authorizing unlimited spending and the government is on a borrowing and spending spree. So far there are no constraints on the ballooning budget deficit. Government bond yields are well behaved. In turn, the Fed is printing limitless money to finance the Treasury and there have been no market or economic constrictions. Share prices are at a record high and credit spreads are very tight. The US dollar is depreciating but it is a benign adjustment for the US because the greenback had been too strong for too long. Chart 1EM's Soft-Budget Constraints In 2009-10 Were Followed By A Decade-Long Hangover

EM's Soft-Budget Constraints In 2009-10 Were Followed By A Decade-Long Hangover

EM's Soft-Budget Constraints In 2009-10 Were Followed By A Decade-Long Hangover

In brief, the enormous size of US stimulus and overflow of liquidity is creating a thrill akin to riding a tiger. Remarkably, this kind of jubilation is very similar to what EM experienced in 2009-10. At the BCA annual conference in New York in 2016, one of the invited speakers – a hedge fund manager – recounted that in 2010, in a private conversation with an investor, Brazilian President Lula da Silva likened ruling Brazil to driving a sports car at high speed in the city with no police around. These were prescient words to describe the situation in Brazil’s economy and financial markets in 2009-10. In 2009-10, Brazil – like many other developing countries – benefited from both the impact of China’s enormous stimulus on commodities prices as well as from foreign capital inflows in part triggered by the Fed’s QE program. In addition, its own government provided sizeable monetary and fiscal stimulus. This stimulus trifecta – emanating from China, the US and local authorities – produced a one-off economic boom and a cyclical bull market in Brazil and other EM countries. Yet, the exuberance was followed by a stagflationary period in Brazil, and later a depression and associated rolling bear markets. Brazil was a poster child for that EM era. The experience of other EM economies was similar and the performance of their financial markets was equally underwhelming. These economies, their leaders, and financial markets wholly enjoyed the stimulus of that period. What followed, however, was a drawn-out hangover that lasted many years: EM ex-China, Korea and Taiwan share prices have been flat for the past 10 years and their currencies were depreciating till last spring (Chart 1). China, the epicenter of epic stimulus in 2009-10, had a similar experience. Its investable ex-TMT stocks, i.e., excluding Alibaba, Tencent and Meituan, are presently at the same level as they were in 2010 (Chart 2). The underlying cause has been a collapse in listed companies’ return on assets (Chart 2, bottom panel). It is essential to emphasize that such poor Chinese equity market performance occurred despite recurring fiscal and credit stimulus from Chinese authorities since 2009 (Chart 2, top panel). As we discussed in detail in a previous report, soft-budget constraints – unlimited stimulus and liquidity overflow – led to complacency, inefficiencies and falling return on capital in EM/China. Chart 3 demonstrates that EM EPS (including China, Korea and Taiwan and their TMT companies) has been flat for 10 years and non-financial companies’ return on assets plunged during the past decade. Chart 2China: "Free Money" Undermined Corporate Efficiency And Profitability

China: "Free Money" Undermined Corporate Efficiency And Profitability

China: "Free Money" Undermined Corporate Efficiency And Profitability

Chart 3EM EPS And Return On Assets: The Lost Decade

EM EPS And Return On Assets: The Lost Decade

EM EPS And Return On Assets: The Lost Decade

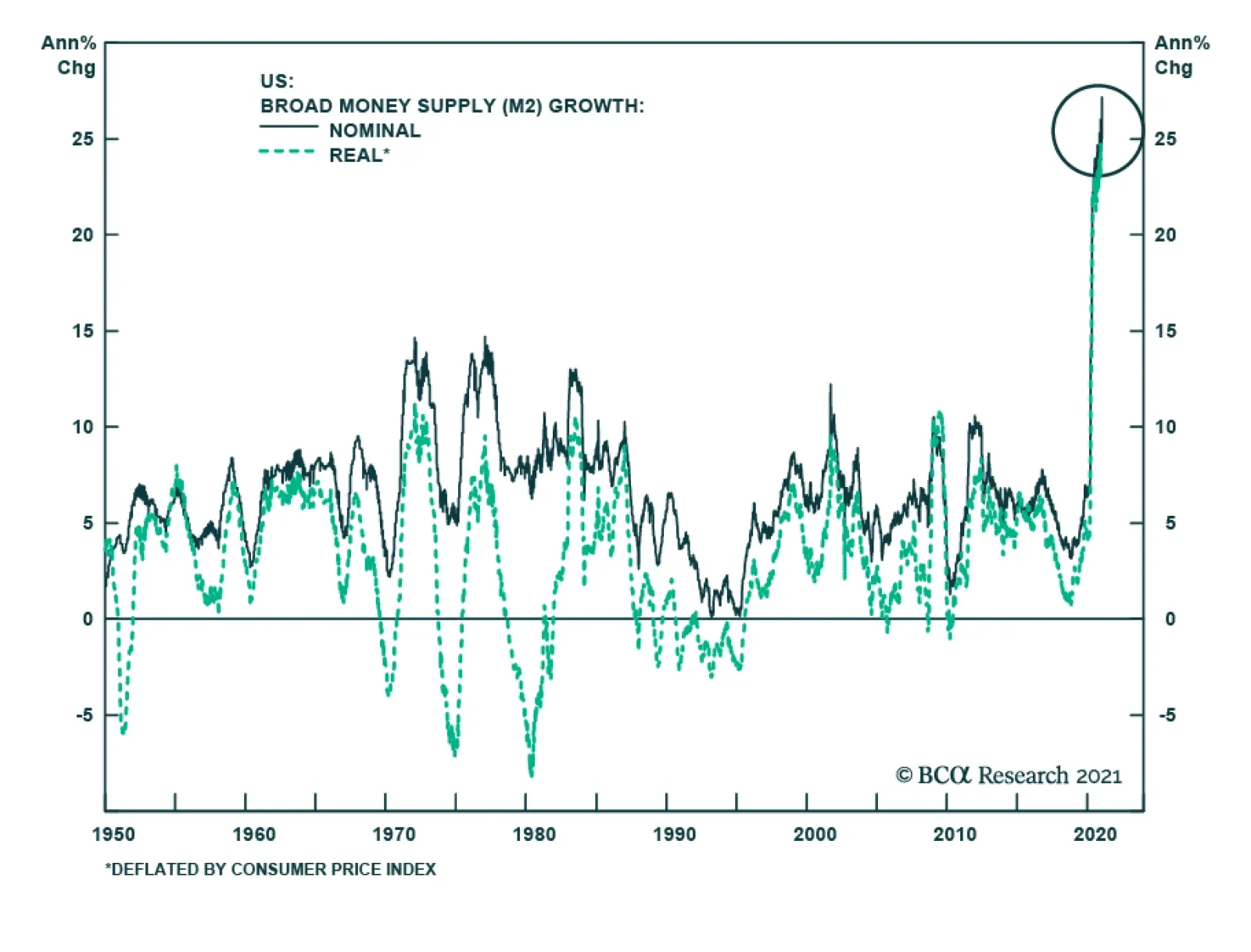

Can The US Dismount The Tiger? The US is currently experiencing no budget constraints. US broad money (M2) growth is at a record high both in nominal and real terms (Chart 4). In turn, the fiscal thrust was 11.4% of GDP last year and will remain substantial this year as most of Biden’s stimulus plan is likely to gain approval from Congress. Chart 4Helicopter Money In The US

Helicopter Money In The US

Helicopter Money In The US

Chart 5China Has Not Been Able To Wean Off Stimulus

China Has Not Been Able To Wean Off Stimulus

China Has Not Been Able To Wean Off Stimulus

Such an explosive boom in US money supply and fiscal largess will continue. Even after the pandemic is under control, it will be hard for policymakers to withdraw stimulus. China is a case in point. In the past 10 years, any time Beijing attempted to reduce the stimulus, China’s economic growth downshifted considerably and financial markets sold off (Chart 5, top panel). This forced Chinese policymakers to continuously enact new rounds of stimulus measures. As a result, they have not been able to achieve their goal of stabilizing the credit-to-GDP ratio (Chart 5, bottom panel). Similar dynamics will likely transpire in the US. Having been inflated enormously, US equity and corporate credit markets will be exceptionally sensitive to any policy shifts. US financial markets will riot at any attempt to withdraw monetary or fiscal stimulus. Given how sensitive US policymakers are to selloffs in financial markets, authorities will be extremely reluctant to exit these stimulative policies. Overall, the US equity and bond markets as well as the economy have grown accustomed to constant stimulus – an addiction that will be very hard to wean off. Bottom Line: Riding a tiger is fun. The hitch is that no one can safely get off a tiger. Similarly, US authorities are currently enjoying the exuberance from stimulus, but they will not be able to safely and smoothly dismount. Inflation, Asset Bubbles Or Capital Misallocation? In any system where an explosive money/credit boom persists, the outcome will be one or a combination of the following: inflation, asset bubbles or capital misallocation. Charts 6 and 7 illustrate that rampant money/credit growth in Japan and Korea in the second half of the 1980s produced property and equity market bubbles. Chart 6Japan: Money And Asset Prices

Japan: Money And Asset Prices

Japan: Money And Asset Prices

Chart 7Korea: Money And Asset Prices

Korea: Money And Asset Prices

Korea: Money And Asset Prices

Chart 8Deploying Credit To Capital Spending Could Lead To Deflation

Deploying Credit To Capital Spending Could Lead To Deflation

Deploying Credit To Capital Spending Could Lead To Deflation

In China’s case, the 2009-10 stimulus resulted in a property bubble as well as capital misallocation. Over the years, we have discussed these outcomes in China in detail and will not elaborate on them in this report. The pertinent question is why inflation has remained depressed in China. In fact, bouts of deflation occurred in various industries in China in the past 10 years. One usually associates a money/credit boom with demand exceeding supply resulting in higher inflation. That is correct if money/credit origination finances consumption with little capital expenditures taking place. However, the credit outburst in China enabled a capital spending boom. This led to a greater supply of goods and services, which in many cases exceeded underlying demand. The upshot has been deflation in various goods prices (Chart 8). History does not repeat but it rhymes. Open-ended stimulus in the US will eventually lead to years of economic and financial malaise. The nature of the challenges that the US will face matters not only to US financial markets but also to EM. Odds are that the US will experience asset bubbles and inflation in the real economy. We will not debate whether the US equity market is already in a bubble or not. Suffice it to say that in our opinion, parts of the market are already in a bubble. The main observation we will make in that regard is as follows: the sole way to justify the current broad US equity valuations is to assume that US Treasurys yields will not rise from the current levels. If US bond yields do not rise much, equity prices could hover at a high altitude. However, any mean reversion in US bond yields will deflate American share prices considerably. In turn, the outlook for US bond yields is contingent on the Fed’s willingness to continue with QE. We do not doubt the Fed will continue buying government securities until it faces a significant inflationary threat. Hence, the primary threat to US and global equity prices is inflation. Fertile Grounds For Inflation In The US Odds of inflation rising meaningfully above 2% in the US economy in the next 12-24 months have increased substantially:1 1. A combination of surging money supply and a potential revival in the velocity of money herald higher nominal GDP growth and inflation. It is critical to realize that in contrast to the last decade when the Fed was also undertaking QE programs, US money supply is now skyrocketing, as shown in Chart 4. In the Special Report from October 22 we discussed in depth why US money growth is currently substantially stronger than the post-GFC period. With household income and deposits (money supply) booming due to fiscal transfers funded by the Fed, the only missing ingredient for inflation to transpire is a pickup in the velocity of money. Lets’ recall: Nominal GDP = Price Level x Output Volume = Velocity of Money x Money Supply Solving the above equation for inflation, we get: Price Level = (Velocity of Money x Money Supply) / (Output Volume) Going forward, the velocity of US money will likely recover, for it is closely associated with consumer and businesses’ willingness to spend. At that point, a rising velocity of money and greater money supply will work together to exert upward pressure on nominal GDP and inflation (Chart 9). Chart 9The US: The Velocity Of Money Correlates With Inflation Momentum

The US: The Velocity Of Money Correlates With Inflation Momentum

The US: The Velocity Of Money Correlates With Inflation Momentum

2. Government policies targeting faster growth in employee compensation are conducive to higher inflation. One of the Biden administration’s key priorities is to boost wages and reduce income inequality. Unless productivity growth accelerates considerably in the coming years, odds are that labor’s share in national income will rise and companies’ profit margins will shrink (Chart 10). Businesses will attempt to raise prices to restore their profit margins. Provided income and spending will be strong, companies could succeed in raising their prices. In the US, a modest wage-inflation spiral is probable in the coming years. Chart 10The US: Faster Wage Growth Will Likely Undermine Corporate Profit Margins

The US: Faster Wage Growth Will Likely Undermine Corporate Profit Margins

The US: Faster Wage Growth Will Likely Undermine Corporate Profit Margins

Chart 11US Core Goods Price Inflation Is Accelerating

US Core Goods Price Inflation Is Accelerating

US Core Goods Price Inflation Is Accelerating

3. Demand-supply distortions and shortages will lead to higher prices. The pandemic has distorted supply chains while the overwhelming demand for manufacturing goods has produced shortages of manufacturing goods. US household spending on goods is booming and US core goods prices as well as import prices from emerging Asia and China are rising (Chart 11). In the service sector, lockdowns will permanently curtail capacity in some sectors. Meanwhile, the reopening of the economy will likely release pent-up demand for services, leading to shortages in certain segments. 4. De-globalization – the ongoing shift away from the lowest price producer – entails higher costs of production and, ultimately, higher prices. 5. Higher industry concentration and less competition create fertile grounds for inflation. Over the past two decades, the competitive structure of many US industries has changed – it has become oligopolistic. Due to cheap financing and weak enforcement of anti-trust regulation, large companies have acquired smaller competitors. In many industries, several dominant players now have a substantial market share. Such a high concentration across many industries raises odds of collusion and price increases when the macro backdrop permits. In sum, US inflation will rise well above 2% in the coming years. Inflationary pressures will become evident later this year when the economy opens up. The main and overarching risk to this view is that technology and automation will boost productivity and allow companies to cut or maintain prices despite cost pressures. Conclusions And Investment Strategy As America’s economy normalizes in the second half of this year, US inflationary pressures will begin rising. However, the Fed will fall behind the inflation curve – it will be late to acknowledge the potency of the inflationary pressures and act on it. It is typical for policymakers to downplay a budding new economic or financial tendency when they have long been pre-occupied with the opposite. Policymakers often fight past wars and are slow to calibrate their policy when the setting changes. The Fed falling behind the inflation curve is bearish for the US dollar in the medium and long-term. Share prices will be caught between rising inflationary pressures and the Fed’s continuous dovishness. This could create large swings in share prices: the market will sell off in response to evidence of rising inflation but will rebound after being calmed by the Fed. Eventually, fundamentals will prevail and the next US equity bear market will be due to higher inflation and rising bond yields. Over the coming several years, US share prices and bond yields will be negatively correlated as they were in the second half of the 1960s (Chart 12). Chart 12The 1960-70s: US Treasury Yields And The S&P 500 Were Negatively Correlated

The 1960-70s: US Treasury Yields And The S&P 500 Were Negatively Correlated

The 1960-70s: US Treasury Yields And The S&P 500 Were Negatively Correlated

Chart 13Will Gold Outperform Global Equities?

Will Gold Outperform Global Equities?

Will Gold Outperform Global Equities?

This is not imminent, but it is not several years away either. Inflation could become the market’s focus later this year. Such a backdrop of heightening inflation risks and the Fed falling behind the curve will favor gold over equities – this ratio might be making a major bottom (Chart 13). In this context, we reiterate our trade of being long gold/short EM stocks. For now, global risk assets are extremely overbought and many of them are expensive. In short, they are overdue for a correction. During this setback, EM equities and credit markets will suffer and in the near term could even underperform their respective global benchmarks. In anticipation of such a setback, we have not upgraded EM to overweight. We continue to recommend maintaining a neutral allocation to EM in global equity and credit portfolios. Consistently, the US dollar will rebound because it is very oversold. We continue shorting a basket of EM currencies versus the euro, CHF and JPY. High-risk currencies will underperform low-beta currencies. The EM/China backdrop remains disinflationary. Therefore, fixed-income investors should continue receiving 10-year swap rates in the following EM countries: Mexico, Colombia, Russia, China, Korea, India, and Malaysia. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Footnotes 1 This is the view of BCA’s Emerging Markets team and is different from BCA’s house view. The latter is more benign on the US inflation outlook in the coming years. Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

Highlights Increased fiscal assistance in the US and other advanced economies will support economic activity until the practice of social distancing durably ends later this year. The US is not yet vaccinating at a pace that is consistent with herd immunity, but that pace is likely to quicken over the coming weeks. A September herd immunity milestone should allow for a significant increase in public “contacts” over the summer and for a substantial closure of the output gap in the second half of the year. The spending of accumulated household savings in the US would rapidly push the output gap into positive territory if those savings were fully deployed upon reopening. But expectations of eventual tax increases and some permanent reduction in services spending suggests that some of those savings will not be spent, and that major economic overheating this year is not likely. The market has largely priced in the most likely economic outcome over the coming year, suggesting that investors should not expect outsized returns in 2021. But our base case view still favors equities relative to bonds, and implies mid-to-high single-digit returns from stocks in absolute terms. An aggressively hawkish deviation in monetary policy later this year is unlikely, barring a sharp and sustained rise in inflation back to target levels. Still, a closure of the output gap this year will push long-dated bond yields higher, suggesting that fixed-income investors should be short duration. Investors should favor global over US and value over growth stocks over the coming year. The US dollar will continue to trend lower, albeit at a slower pace. Feature Chart I-1The Near-Term Outlook For Economic Growth Is Poor

The Near-Term Outlook For Economic Growth Is Poor

The Near-Term Outlook For Economic Growth Is Poor

The outlook for growth in the US and other developed economies remains poor over the very near term. The combination of another major wave of the COVID-19 pandemic, at least partially driven by more transmissable variants of the virus, as well as the lagged effects of diminished US fiscal support in the second half of last year have led to a slowdown in economic activity that is likely to linger for the coming several weeks (Chart I-1). Outside of the US, the pressure on the medical system has led to the re-imposition of heavy control measures that mechanically weigh on consumer spending. Within the US, some restrictions have been re-imposed, but spending has also slowed due to the exhaustion of the stimulative benefits of last year’s CARES act for a sizeable portion of recipients. There are early signs suggesting that the second wave is cresting in advanced economies: hospitalizations appear to have peaked in the US and a few major European economies, and the number of new cases is either trending lower or has plateaued (Chart I-2). However, even if this is the beginning of the end of the latest wave, the gains in the war against COVID-19 have clearly been won through changes in policy and human behavior, not through inoculation. Chart I-2Infections Are Slowing Because Of Policy And Behavior (Not Vaccinations)

Infections Are Slowing Because Of Policy And Behavior (Not Vaccinations)

Infections Are Slowing Because Of Policy And Behavior (Not Vaccinations)

For example, in the US, some market commentators have highlighted the fact that hotbed midwestern states such as North and South Dakota have administered more doses of the vaccine and that the Midwest is experiencing the largest decline in new cases in the country, inferring a causal relationship. This ignores the fact that new confirmed cases peaked in the Midwest almost a month before the Pfizer/BioNTech vaccine was approved by the CDC. This suggests that a decline in cases there, which led the overall US trend, much more likely occurred in response to an exponential rise in hospitalizations in October and early November. We cannot identify a specific policy change in Midwestern states that catalyzed a peak in cases, but we hypothesize that residents of these states took it upon themselves to reduce their contacts as the threat of medical system collapse and health care rationing increased sharply. A cresting second wave is certainly positive from a health perspective, and should reduce the pressure on the medical system. But the fact that additional restrictions and/or growth-negative consumer behavior were required yet again to “flatten the curve” underscores that many of these measures will likely remain in place for the coming few weeks to durably end the wave, and thus will weigh on Q1 growth. They will also likely remain the only viable response to combat future outbreaks until vaccination reaches levels that are sufficient to reduce the impact of the pandemic on economic activity. More Fiscal Support On The Way In Europe and Canada, the fiscal response to the second wave has generally been to extend wage subsidy and income support programs. In the US, after having let unemployment benefit payments lapse in the second half of 2020, the US congress passed a US$900 billion aid bill in late December that provides US$300 per week in supplemental unemployment benefit payments and US$600 in direct checks to most Americans. Chart I-3 highlights that these payments have already begun to reach US households. In addition, following the Democratic Senate wins in Georgia earlier this month, President Biden announced a $1.9 trillion emergency relief package that topped up individual direct payments to US$2,000, assistance to small businesses, aid to state & local governments, and funding for pandemic-related expenses such as testing and the rollout of vaccines. While the size and contents of Biden’s proposal may get scaled down, our geopolitical strategists expect most of the plan to gain approval in Congress early this year. That implies that the federal deficit is on track to fall somewhere between the “Democratic Status Quo” and “Democratic High” scenarios shown in Chart I-4, meaning that the deficit will peak at between 22% and 25% of GDP in fiscal year 2021. Chart I-3Unemployment Benefit Payments Are Rising Again

Unemployment Benefit Payments Are Rising Again

Unemployment Benefit Payments Are Rising Again

Chart I-4A Very Significant Amount Of Stimulus Is Still To Come

February 2021

February 2021

This is a very significant amount of stimulus, and will provide a substantial reflationary bridge to help counter the negative impact on Q1 growth from the pandemic. But in the aggregate, some portion of the fiscal stimulus is unlikely to be spent by households until there is no longer a need for social distancing and the economy fully reopens. How long it takes to arrive at that moment depends enormously on the US’ progress at vaccinating its population. Vaccines, Herd Immunity, And Reopening For now, the news on the vaccine front is mixed. Israel, which has vaccinated over 40% of its population with at least one dose (Chart I-5), has demonstrated that it is technically possible to deploy the vaccine at an extremely rapid pace. But it is not clear that Israel’s experience is applicable to other countries, given aggressive efforts by the Israeli government to obtain early access to vaccine doses (which cannot, by definition, be achieved by everyone). While Chart I-5 shows that the US currently ranks highly among other countries at administering vaccines, Chart I-6 highlights that the pace must quicken for herd immunity to be reached later this year. The chart shows the number of actual US doses administered per 100 people, alongside the range that would need to be followed for 50-80% of the US population to be fully immunized by the end of September. Note that more than 100 doses per 100 people will be required in order to vaccinate most of the US population, given that two vaccine doses will need to be administered per person. Chart I-5Israel Is Winning The Vaccine Race Because Of Preferential Access

February 2021

February 2021

Chart I-6Although It Likely Will, The Pace Of US Vaccinations Must Quicken

Although It Likely Will, The Pace Of US Vaccinations Must Quicken

Although It Likely Will, The Pace Of US Vaccinations Must Quicken

The “X” on the chart highlights the Biden administration’s previous goal of 100 million doses administered in the first 100 days following inauguration, which was too timid of an objective to be on any of the herd immunity paths shown in the chart. The administration’s new goal of 1.5 million injections administered per day starting by the middle of February is more promising and suggests that the US will be within the herd immunity range by late April. Chart I-6 is somewhat daunting, in that it highlights the risk that the US may not actually achieve herd immunity this year, and that investors are overestimating the odds of true economic reopening. However, that would be an overly pessimistic assessment, for three reasons: Due to the scaling up of vaccine production, the pace of vaccine dose deliveries will likely soon grow at an exponential rather than linear rate. This implies that the “underperformance” of actual vaccine doses administered versus the herd immunity paths shown in Chart I-6 is temporary. Private industry is likely to help the government meet its new vaccination goals. Amazon has recently offered the federal government assistance at distributing vaccine doses, and CVS, the retail pharmacy chain, has recently suggested that its stores could provide 1 million injections per day. These estimates do not include the likely establishment of large-scale, federally-funded vaccination sites. Despite what health professionals may advise, wide-ranging re-opening of economic activity and the end of social distancing policies will likely occur before herd immunity is technically reached. From the perspective of a health care professional, case minimization should be the objective of policy as it stands to minimize the number of deaths linked to the pandemic. But given the tremendous economic, emotional, and mental health toll inflicted by social distancing, from the perspective of politicians and many members of the public, the objective of policy should instead be to ensure that the medical system remains functional and that rationing of critical care is not required. The fact that vaccines are being administered to those most likely to become hospitalized suggests that the peak impact on the health care system will occur before herd immunity is achieved, which should allow for an increase in public “contacts” over the summer. What Happens When The Economy Re-Opens? In the US and in most advanced countries, the gap in spending is focused entirely on the services side of the economy. Table I-1 presents a simple estimate of the US spending gap for real personal consumption expenditures, broken down by type. The table highlights that goods spending is currently above not just pre-pandemic levels, but also above what would have been expected if the pandemic had not occurred. The only exceptions to this are nondurable goods categories that have been highly impacted by working-from-home policies, such as clothing and footwear and gasoline and other energy goods. The household services consumption gap, on the other hand, was deeply negative in Q3, concentrated within transportation, recreation, and food/accommodation services. Table I-1The Spending Gap Is Almost Entirely On The Services Side

February 2021

February 2021

My colleagues Peter Berezin and Doug Peta have recently estimated that US households are sitting on roughly $1.4-1.5 trillion in excess savings as a combined result of the CARES act and the massive services spending gap noted above (Chart I-7). That amounts to approximately 7% of GDP, which significantly exceeds an estimated output gap of roughly 3% at the end of Q4 (Chart I-8). Chart I-7A Massive Horde Of Excess Savings Has Been Accumulated

A Massive Horde Of Excess Savings Has Been Accumulated

A Massive Horde Of Excess Savings Has Been Accumulated

Chart I-8Excess Savings Of 7% Of GDP Dwarf A -3% Output Gap

Excess Savings Of 7% Of GDP Dwarf A -3% Output Gap

Excess Savings Of 7% Of GDP Dwarf A -3% Output Gap

At first blush, this suggests that the deployment of those savings, which seems likely once the pandemic is over and the need for social distancing measures are no longer required, could rapidly push the output gap into positive territory. But that calculation assumes that all excess savings will be spent, which will probably not occur given that some holders of those savings will expect future tax increases. An enormous budget deficit combined with Democratic control of government means that individual and corporate tax increases are highly likely over the coming 12-24 months, suggesting that higher-income individuals will expect some of those excess savings to ultimately be taxed away. In addition, even once social distancing is no longer required, it seems likely that some small portion of the spending on services that has been “missing” over the past year will never return. While it seems reasonable to expect that the gap in spending on hospitality and travel will close quickly and even potentially exceed pre-pandemic levels once the health situation allows, it also seems reasonable to expect that some service areas, particularly retail, will experience a permanent loss in demand owing to durable shifts in consumer behavior that occurred during the pandemic (greater familiarity and use of online shopping, a permanent reduction of some magnitude in commuting, etc). Chart I-9So Far, There Is Little Evidence Of Major Permanent Labor Market Damage

So Far, There Is Little Evidence Of Major Permanent Labor Market Damage

So Far, There Is Little Evidence Of Major Permanent Labor Market Damage

It remains unclear how much of a permanent decline will occur, and it is very difficult to forecast because of its dependency on the pace at which vaccination occurs. The faster that economic circumstances return to normal, the less permanent changes are likely to occur. For now, evidence from the labor market remains encouraging, in that permanent job loss has not surged beyond that experienced during a typical income-statement recession (Chart I-9). But the bottom line is that some of the mountain of savings that has been accumulated over the past year has occurred due to a reduction in spending on certain services that may not return once the pandemic is over, meaning that those funds may be permanently saved. This suggests that meaningful output gap closure, rather than major overheating of the economy, is the more likely scenario later this year. Is Re-Opening Priced In? Charts I-10 and I-11 highlight market expectations for growth and earnings over the next 12 months. The charts highlight that expectations are already in line with a meaningful closure of the output gap later this year: consensus growth expectations suggest that real GDP will only be about half a percentage point below potential output by the end of 2021, and bottom-up analysts expect that S&P 500 earnings per share will be approximately 3% higher in 12 months’ time than they were at the onset of the pandemic. Chart I-10Meaningful Output Gap Closure Is Likely This Year

Meaningful Output Gap Closure Is Likely This Year

Meaningful Output Gap Closure Is Likely This Year

Chart I-11Analysts Already Expect A Complete Earnings Recovery

Analysts Already Expect A Complete Earnings Recovery

Analysts Already Expect A Complete Earnings Recovery

Does the fact that market expectations already reflect what is likely to occur over the coming year mean that stock prices have nowhere to go? At a minimum it suggests that strong, double-digit returns are unlikely, especially given that equities are more technically stretched to the upside than they have been at any point over the past decade and that investor sentiment is very bullish (Chart I-12). However, even if earnings grow exactly in line with analyst expectations over the coming year, it is not correct to say that stocks offer no return potential. Chart I-13 illustrates this point by showing the historical relationship between earnings surprises and the price performance of the S&P 500. Chart I-12US Equities Are Extremely Overbought

US Equities Are Extremely Overbought

US Equities Are Extremely Overbought

Chart I-13Positive Stock Returns Almost Always Accompany In-Line Earnings Performance

Positive Stock Returns Almost Always Accompany In-Line Earnings Performance

Positive Stock Returns Almost Always Accompany In-Line Earnings Performance

The first point to note from the chart is that positive earnings surprises are quite rare, in that actual earnings tend to underperform expectations of earnings 12 months prior. As such, earnings performance over the coming 12 months that is exactly in line with expectations would be a better fundamental result than what investors can typically expect. The second point to note is that it is rare for stocks to fall when earnings meet or exceed prior expectations, unless faced with a significant growth shock. Earnings met or exceeded expectations in 1995, from 2004-2007, from 2010-2011, and in 2018, and in all four cases, stocks delivered either high single-digit or low double-digit price returns. Negative year-over-year returns occurred only briefly in two of these episodes and were tied to major changes to the economic outlook: the euro area sovereign debt crisis in 2011-2012, and the onset of the Sino-US trade war in 2018. Conclusions And Investment Recommendations Chart I-14Investors Should Favor Global Ex-US and Value Stocks This Year

Investors Should Favor Global Ex-US and Value Stocks This Year

Investors Should Favor Global Ex-US and Value Stocks This Year

For investors focused on the coming 6-12 months, the key conclusions of our analysis are as follows: The outlook for economic growth is negative over the very near term, but additional fiscal support will likely provide enough of a reflationary bridge to avoid a serious contraction in activity. The achievement of herd immunity and the end of social distancing must occur this year for consensus 2021 expectations for economic growth and earnings to be realized. The US is not yet vaccinating at a pace that is consistent with herd immunity later this year, but credible projections from the new administration suggest that the pace will meaningfully quicken by the end of February. Some US households have accumulated significant savings over the past year, which would rapidly push the output gap into positive territory were they to all be deployed following full economic reopening. The expectation of eventual tax increases and a permanent reduction in some services spending means that not all of these savings will be spent, suggesting that the output gap will close meaningfully this year – but not overshoot into positive territory. Consensus market expectations already reflect what is likely to occur over the coming year, but the realization of these expectations still implies mid-to-high single-digit returns from equities. Chart I-15The Dollar Is A Counter-Cyclical Currency, And Will Continue To Trend Lower

The Dollar Is A Counter-Cyclical Currency, And Will Continue To Trend Lower

The Dollar Is A Counter-Cyclical Currency, And Will Continue To Trend Lower

Given these conclusions, we recommend the following investment stance over the coming 6-12 months: Stock prices are likely to rise in absolute terms despite already elevated multiples, and investors should remain overweight equities relative to government bonds. A meaningful closure of the output gap is consistent with the Fed’s economic projections, suggesting that an aggressively hawkish deviation in monetary policy later this year is unlikely, barring a sharp and sustained rise in inflation back to target levels. Still, a closure of the output gap this year will push long-dated bond yields higher, suggesting that fixed-income investors should be short duration. The “reopening trade” favors global over US stocks, and value over growth stocks. Chart I-14 highlights that global ex-US stocks are now in a clear uptrend versus their US peers, whereas value stocks have yet to decisively break out. We expect the latter will occur over the coming 6-12 months. The US dollar is a reliably counter-cyclical currency, and has behaved exactly as a counter-cyclical currency should have over the past year (Chart I-15). We thus expect a further, albeit less sharp, decline in the dollar over the coming year. Jonathan LaBerge, CFA Vice President The Bank Credit Analyst January 28, 2021 Next Report: February 25, 2021 II. Surging US Money Growth: Should Investors Be Concerned? Generally-speaking, an increase in bank deposits occurs due to either Fed asset purchases, bank asset purchases, or bank loan creation. Deposits have grown massively over the past year because the Treasury has issued an enormous amount of bonds, and these bonds have been purchased both by the Fed and US banks. Relative to the 2008-2009 period, the comparatively better health of US bank balance sheets last year has been an even more important factor than Fed asset purchases in accounting for the difference in money growth between the two periods. Money growth used to be a good predictor of economic activity, but today it makes more sense to focus on interest rates rather than monetary aggregates as a leading economic indicator. Over the past 20 years, only the collapse in velocity that occurred after 2008 is meaningful for investors, and it appears to reflect already “known” information: the persistent household deleveraging that occurred following the global financial crisis, and the effect of Fed asset purchases on the stock of money at several points over the past decade. Our base case view is that a portion of the significant amount of household savings that have accumulated will not be spent, and that the US output gap will close but not move deeply into positive territory this year. But the enormous growth in money over the past year reflects unprecedented fiscal and monetary support, which could eventually change investor expectations about long-term interest rates (even absent rapid overheating). Rising long-term rate expectations could threaten the equity bull market, given the impact the secular stagnation narrative has had in keeping long-term rate expectations low and the extent to which easy money has boosted equity valuation multiples over the past year. Broad money growth has exploded higher over the past year, to a pace that has not been seen since WWII (Chart II-1). This growth in the money supply has vastly exceeded what investors witnessed during and immediately following the global financial crisis of 2008-2009, raising concerns among many investors of the potential cyclical and structural consequences. Chart II-1A Nearly Unprecedented Surge In Money Growth

A Nearly Unprecedented Surge In Money Growth

A Nearly Unprecedented Surge In Money Growth

In this report we revisit the deposit creation process, and explain the specific factors that have led to surging money growth over the past year. We also review the usefulness of money growth as an economic indicator, and provide some perspective on the 20-year decline in money velocity. We conclude by noting that the surge in money growth is potentially concerning for investors for two reasons. First, if US households ignore likely future tax increases and decide to fully spend the vast amount of savings that have accumulated over the past year, then the US economy is likely to overheat rather quickly. The second, more likely, threat to investors is if the sharp increase in the money supply ends up changing market expectations about the neutral rate of interest. It remains too early to conclude whether investors will significantly revise up their long-term rate expectations, in large part because the scale of permanent damage in the wake of the pandemic is still unknown. But investors should remain vigilant, given the impact the secular stagnation narrative has had on keeping long-term rate expectations low and the extent to which easy money has boosted equity valuation multiples over the past year. Reviewing The Money And Bank Deposit Creation Process In order to fully understand the spectacular growth of the money supply over the past year and its potential implications for the economy and financial markets, it is important to revisit how money is created in a modern economy. My colleague Ryan Swift, BCA’s US Bond Strategist, reviewed this question in detail in a June 2020 Strategy Report and we summarize the report’s key points below.1 In the US, most of the stock of broad money aggregates is composed of bank deposits. Following the global financial crisis, the textbook view of how banks act purely as intermediaries, taking in deposits from the public and lending them out, was revealed to be a mostly inaccurate description of the financial system in the aggregate. Rather, while individual banks often compete for deposits as a source of funding, bank deposits in the aggregate are typically created by making loans. Central banks can also create money, by purchasing financial assets and crediting the banking system with reserve assets (central bank money). Table II-1 highlights the link between the Fed’s balance sheet and that of US banks in the aggregate, and highlights how changes in deposits – a liability of the banking system – must be offset by increases in bank assets or decreases in other bank liabilities. Table II-1The Link Between The Fed’s Balance Sheet And The Aggregate US Banking System

February 2021

February 2021

The typical mechanics of three money-creating operations are described below, alongside the corresponding change in balance sheet items: Fed Asset Purchases: When the Federal Reserve purchases financial assets in the secondary market, it increases securities held (Fed asset) and typically increases reserves (Fed liability). In the increase in reserves (banking system asset) matches the increase in deposits (banking system liability), as the previous holders of the assets purchased by the Fed deposit the proceeds of the sale. Bank Asset Purchases: When banks purchase government securities from non-bank holders they credit the sellers with bank deposits.2 This increases bank holdings of securities or other assets (banking system asset) and increases deposits (banking system liability). Bank Loan Creation: When banks create a loan, they increase their holdings of loans & leases (banking system asset) and deposit the loan amount into the borrowers’ account (banking system liability). At the individual bank level, if Bank A creates a loan and the borrower withdraws the funds to pay someone with an account at Bank B, there will be an asset-liability mismatch relating to that loan transaction between those two banks if no other actions are taken. The result will be that Bank A experiences an increase in equity capital and Bank B experiences a decline. But for the banking system as a whole, the increase in bank assets exactly matched the increase in bank liabilities, and Bank A created the deposits that ended up as a liability of Bank B. The issuance or retirement of long-term bank debt and equity instruments can also create or destroy deposits but, for the purpose of understanding the difference in money growth during the pandemic compared with the 2008-2009 experience, it is sufficient to focus on the three money-creating operations described above. Explaining The Recent Surge In Money Growth The prevalent view among many financial market participants is that the money supply has surged in the US due to the fiscal stimulus provided by the CARES act. But an increase in the government’s budget deficit does not in and of itself create money, because the Treasury issues bonds to finance the difference between revenue and expenditures. If those bonds are purchased entirely by the nonfinancial sector, then an increase in deposits of stimulus recipients is offset by a decrease in deposits of those who purchased the bonds. A more precise answer is that deposits have grown massively over the past year because the Treasury has issued an enormous amount of bonds and these bonds have been purchased both by the Fed and US banks. Charts II-2A and II-2B highlight this by showing the change in the main items on the aggregate banking system balance sheet since the end of 2019. The charts show that the increase in deposits on the liability side of bank balance sheets have been matched by large increases in reserves and other cash (caused by the Fed’s asset purchases) and banks’ securities holdings (caused by bank asset purchases). Chart II-2AOver The Past Year, Fed And Bank Asset Purchases…

February 2021

February 2021

Chart II-2B…Account For Most Of The Surge In Deposits

February 2021

February 2021

But this does not explain why money growth has been so much larger over the past year than it was in 2008-2009, when total Federal Reserve assets increased from $920 billion to $2.2 trillion. Chart II-1 on page 15 highlighted that growth in M2 has risen to a whopping 25% year-over-year growth rate, a full 15 percentage points above the strongest rate that prevailed following the global financial crisis. Charts II-3A and II-3B explain the discrepancy, by showing the change in the main items on the aggregate banking system balance sheet as a percent of the money supply during each of the two periods, as well as the difference. The charts show that while changes in bank reserves and cash assets – caused by Fed asset purchases – were significantly larger in 2020 than they were on average from 2008 to 2009, changes in loans & leases and securities in bank credit, as well as other assets were also quite significant and account for two-thirds of the difference when added together. Chart II-3ARelative To 2008/2009, The Health Of The Banking System…

February 2021

February 2021

Chart II-3B…Helped Facilitate More Money Creation Last Year

February 2021

February 2021

Thus, while it is true that the Fed’s accommodation of extraordinary fiscal easing has helped create a sizeable amount of money over the past year, relative to the 2008-2009 period the comparatively better health of US bank balance sheets has been an even more important factor – in the sense that balance sheet restrictions did not prevent US banks from facilitating the creation of money as appears to have been the case in the aftermath of the global financial crisis. Money And Growth We noted above that fiscal easing does not create money in and of itself unless the bonds issued to finance an increase in the deficit are purchased either by banks or the Fed. Yet most investors would not disagree that significant increases in budget deficits boost short-term economic growth, particularly during recessions. This implies that the link between money and economic growth may not be particularly strong over a cyclical time horizon, which is in fact what the data shows – at least over the past 30 years. Charts II-4A and II-4B illustrate the historical relationship between real GDP and real M2 growth, pre- and post-1990. The chart makes it clear that the relationship between real money and GDP growth used to be strong, with real money growth somewhat leading economic activity. This relationship completely broke down after the 1980s, and is now mostly coincident and negative. There are three reasons behind the breakdown: 1. The money supply used to be the Federal Reserve’s monetary policy target, meaning that money growth directly reflected monetary policy shifts. Today, the Fed targets interest rates, and the portion of money created through loans simply mirrors the change in interest rates as loan demand rises (falls) and interest rates fall (rise). Specifically, Chart II-4A shows that the ability of money growth to lead economic activity seems to have ended in the late 1980s, when the Fed stopped providing targets for monetary aggregates. Chart II-4AMoney Growth Used To Predict Economic Activity…

Money Growth Used To Predict Economic Activity...

Money Growth Used To Predict Economic Activity...

Chart II-4B…But Ceased To Do So Once The Fed Stopped Targeting The Money Supply

...But Ceased To Do So Once The Fed Stopped Targeting The Money Supply

...But Ceased To Do So Once The Fed Stopped Targeting The Money Supply

Chart II-5US Banks Provide Meaningfully Less Private Sector Credit Than In The Past

US Banks Provide Meaningfully Less Private Sector Credit Than In The Past

US Banks Provide Meaningfully Less Private Sector Credit Than In The Past

2. The share of total US credit provided by US banks has fallen significantly over time – especially during the early 1990s – as corporate bond issuance, securitized loans, and mortgages backed by agency bonds issued to the private sector rose as a proportion of total credit (Chart II-5). 3. Since 2000, a Chart II-4B shows that a clearly negative correlation has emerged between money growth and economic activity during recessions. In 2008-2009 and again last year, money growth reflected emergency Fed asset purchases in the face of a sharp decline in economic activity. In 2000, the Fed did not expand its balance sheet, but the economy diverged from money growth due to the lingering impact of management excesses, governance failures, and elevated debt in the corporate sector in the 1990s. The conclusion for investors is straightforward: while money growth used to be a good predictor of economic activity, today it makes more sense to use interest rates than monetary aggregates as a leading indicator for growth. Money Velocity And Its Implications When discussing the impact of money on the economy, one point often raised by investors is the fact that money velocity has declined significantly over the past two decades. This observation is frequently followed by the question of whether the absence of this decline would have caused real growth, inflation, or both to have been higher over the past 20 years than they otherwise were. It is difficult to prove or refute the point, as monetary velocity is not a well-understood concept – investors do not have a good, reliable theory upon which to predict changes in velocity or understand their economic significance. Velocity is calculated from the equation of exchange as a ratio of nominal GDP to some measure of the money supply (typically a broad measure such as M2) and theoretically represents the turnover rate of money. But long-term changes in velocity do not seem to correlate well with measures of growth or inflation. Short-term changes in velocity correlate extremely well with inflation, but this simply reflects the fact that velocity tends to be driven by the numerator (nominal GDP) over short periods of time (see Box II-1). BOX II-1 Money Velocity Over The Short-Term Some investors have pointed to the relationship shown in Chart II-B1 to argue that M2 money velocity is a significant cyclical predictor of inflation. But Chart II-B2 illustrates that nearly two-thirds of annual changes in velocity since 1990 have been accounted for by changes in the numerator – nominal GDP – rather than the denominator. This underscores that the apparent explanatory power of short-term changes in money velocity at predicting inflation is simply capturing the normal relationship between real growth and inflation, as well as the naturally positive correlation between the implicit GDP price deflator and core consumer prices. Chart Box II-1Velocity Seemingly Predicts Inflation Over The Short-Term…

Velocity Seemingly Predicts Inflation Over The Short-Term...

Velocity Seemingly Predicts Inflation Over The Short-Term...

Chart Box II-2…Because Short-Term Changes In Velocity Are Driven By Nominal Output

February 2021

February 2021

The bigger question is why velocity has declined so significantly over the past 20 years, and what this means for investors. Chart II-6Large Declines In Velocity Are Linked To Prolonged Periods Of Deleveraging

Large Declines In Velocity Are Linked To Prolonged Periods Of Deleveraging

Large Declines In Velocity Are Linked To Prolonged Periods Of Deleveraging

Panel 1 of Chart II-6 shows a long-dated history of M2 velocity, and highlights that the average or “normal” level of M2 velocity has historically been just under 1.8. Over the past century, there have been just four major deviations from this level: A major decline that began at the start of the Great Depression and prevailed until the Second World War (WWII) Significant volatility during and in the years immediately following WWII A sharp rise in velocity during the 1990s to a record level A downtrend beginning in the late 1990s that remains intact today Abstracting from the war period in which the economy was heavily distorted by government intervention, Chart II-6 also highlights that persistent declines in velocity appear to be explainable by major deleveraging events. The second panel of the chart shows a measure of the duration of private sector deleveraging, and highlights that the two periods of low velocity have been strongly (negatively) correlated with the prevalence of deleveraging. This explanation is simple but intuitive: excessive leveraging eventually causes households and firms to redirect a larger portion of their income to servicing or paying down debt, which weighs on real growth and, by extension, prices. While it is true that the recent 20-year downtrend in velocity began in the late 1990s and thus well before household deleveraging began in 2008, this seems to mostly reflect the reversal of an anomalous rise in velocity in the late 1990s. We largely view the decline in velocity from the late 1990s to 2008 as a “reversion to the mean.” It remains an option question why velocity rose so sharply in the 1990s. Some evidence seems to point to financial innovation and technological change: Chart II-7 highlights that the number of automated bank teller and point-of-sale payment terminals rose massively in the 1990s, alongside a significant acceleration in real cash in circulation. This is theoretically consistent with an increased “turnover” rate of money. But Chart II-8 highlights that a substantial portion of the rise in velocity during this period was attributable to denominator effects (persistently weak money growth), rather than numerator effects. Chart II-7Some Evidence Of Increased Money Turnover In The 1990s

Some Evidence Of Increased Money Turnover In The 1990s

Some Evidence Of Increased Money Turnover In The 1990s

Chart II-8The Rise In Velocity In The 1990s Was Driven By Slow Money Growth

The Rise In Velocity In The 1990s Was Driven By Slow Money Growth

The Rise In Velocity In The 1990s Was Driven By Slow Money Growth

Regardless of the cause, velocity was clearly anomalous on the upside in the 1990s, suggesting that it is not the downtrend in velocity over the past 20 years that is significant to investors. Rather, it is the collapse in velocity that has occurred since 2008 that is meaningful, and from the perspective of investors it appears to reflect already “known” information: the persistent household deleveraging that occurred following the global financial crisis, and the effect of Fed asset purchases on the stock of money at several points over the past decade. In the future, any meaningful increases in velocity are only likely to occur due to a significant reduction in the size of the Fed’s balance sheet, which is two to three years away at the earliest. The Fed could decide to taper its asset purchases sometime later this year or in early 2022, but tapering would merely slow the pace at which the Fed’s assets are increasing (and would thus not cause velocity to rise via a meaningful slowdown in money growth). Money And Future Inflation The final question to address is the issue of whether the enormous rise in money growth over the past year is likely to lead to higher, potentially much higher, inflation over the coming 6-12 months. This has been the main question from investors who have been unnerved by the surge in money growth and the collapse in the US government budget balance. Any link between money and inflation has to come through spending, so the question of whether a surge in money will lead to higher inflation is akin to asking whether the massive amount of savings that have been accumulated over the past year are likely to be spent, and over what period. We discussed this question in Section 1 of this month’s report, and noted that expectations of future tax increases and a permanent decline in some services spending will likely prevent all of these savings from being deployed once the practice of social distancing durably ends later this year. This implies that a substantial closure of the output gap is likely to occur in the second half of the year, but that major economic overheating will be avoided. Moreover, even if the output gap does rise into positive territory over the coming 6-12 months, this does not necessarily suggest that inflation will rise quickly back above the Fed’s target. In last month’s Special Report, we highlighted two important points about inflation that are often overlooked by investors. First, inflation’s long-term trend is determined by inflation expectations. Second, if inflation expectations are largely formed based on the experience of past inflation, then inflation is ultimately determined by three dimensions of the output gap: whether it is rising or falling, whether it is above or below zero, and how long it has been above or below zero. While market-based expectations of long-term inflation have risen well above the Fed’s target, both our adaptive expectations model for inflation as well as a simple five-year moving average are between 30-60 basis points below the 2% mark (Chart II-9). This may suggest that a persistent period of output above potential may be required in order to raise inflation relative to expectations and to raise expectations themselves above the Fed’s target unless the Fed’s efforts at “jawboning” them higher prove to be highly successful. Measured as a year-over-year growth rate of core prices, inflation is set to spike higher in April and May in the order of 50-60 basis points simply due to base effects (Chart II-10). However, inflation will only sustainably rise to an above-target rate over the coming 6-12 months if demand is even stronger than implied by consensus expectations, which is not our base case view. Chart II-9Adaptive Inflation Expectations Measures Are Still Well Below The Fed's Target

Adaptive Inflation Expectations Measures Are Still Well Below The Fed's Target

Adaptive Inflation Expectations Measures Are Still Well Below The Fed's Target

Chart II-10The Fed Will Look Through Base Effects On Consumer Prices

The Fed Will Look Through Base Effects On Consumer Prices

The Fed Will Look Through Base Effects On Consumer Prices

Investment Conclusions Investors can draw two conclusions from our analysis above. First, there is reason to be concerned about the enormous rise in the money supply if we are wrong in our assessment that some portion of the savings accumulated over the past year will not ultimately be spent. If US households ignore likely future tax increases and decide to fully spend their savings windfall, then the US economy is likely to overheat rather quickly. The second, more likely, threat to investors is if the sharp increase in the money supply, reflecting monetized fiscal stimulus and a meaningfully healthier financial system compared with the global financial crisis, ends up changing market expectations about the neutral rate of interest. Chart II-11The Pandemic Response May Raise Long-Term Rate Expectations

The Pandemic Response May Raise Long-Term Rate Expectations

The Pandemic Response May Raise Long-Term Rate Expectations

Chart II-11 that while 5-year/5-year forward Treasury yields are not much lower than they were pre-pandemic, that is an artificially low bar. Long-dated bond yields fell over 100 basis points in 2018 and 2019, in response to a global growth slowdown precipitated by the Trump administration’s trade war. While President Biden will pursue some protectionist policies, they are likely to be meaningfully less damaging to global growth than under President Trump and are extremely unlikely to act as the primary driver of macroeconomic activity over the course of Biden’s term (as they were during the period that long-dated bond yields fell). As such, if the pandemic ends this year with seemingly minimal lasting damage to the US economy, long-dated bond yields could re-approach their late 2018 levels or higher towards the end of the year. This would cause a meaningful rise in 10-year Treasury yields, even with the Fed on hold until the middle of 2022 or later. A significant rise in bond yields would be quite unwelcome to stock investors given how stretched equity multiples have become. Table II-2 presents a set of year-end scenarios to gauge the potential impact of an eventual rise in 10-year yields. We assume that forward earnings grow at 5% this year, and we allow the spread between the 12-month forward earnings yield and the 10-year yield (a proxy for the equity risk premium) to return to its 2003-2007 average as part of an assumed “normalization” trade. Table II-2Current Multiples Are Justified Only If The 10-Year Treasury Yield Does Not Rise Above 2.5%

February 2021

February 2021

The table suggests that a 10-year Treasury yield of 2.5% will be the most that the interest rates could rise before the fair value of the S&P 500 falls below current levels. That roughly equates to a return to the late-2018 levels that prevailed for 5-year/5-year forward Treasury yields, given that the short-end of the curve will remain pinned close to the zero lower bound for some time. For now, it remains too early to conclude whether investors will significantly revise their long-term rate expectations, in large part because the scale of permanent damage in the wake of the pandemic is still unknown. But investors should remain vigilant and attentive to the fact that interest rates may pose a threat to financial markets later this year even in a scenario where the US economy is not immediately overheating, given the impact the secular stagnation narrative has had in keeping long-term rate expectations low and the extent to which easy money has boosted equity valuation multiples over the past year. Jonathan LaBerge, CFA Vice President The Bank Credit Analyst III. Indicators And Reference Charts BCA’s equity indicators highlight that the “easy” money from expectations of an eventual end to the pandemic have already been made. Our technical, valuation, and sentiment indicators are very extended, highlighting that a near-term pullback in stock prices remains a significant risk. Our monetary indicator is in a clear downtrend, reflecting a reduced intensity of monetary support, but it remains above the boom/bust line. The upshot is that while the marginal stimulus provided by monetary policy is falling, the level of stimulus from easy monetary conditions remains significant. Forward equity earnings already price in a complete earnings recovery, but for now there is no sign of waning forward earnings momentum. Net revisions and positive earnings surprises remain solidly positive. Within a global equity portfolio, the US underperformance that we noted last month continues, led by strong gains in emerging markets (including China). Euro area stocks have significantly underperformed EM over the course of the pandemic, are likely to emerge as the new regional leader within a global ex-US portfolio at some point later this year. The US 10-Year Treasury yield has broken convincingly above its 200-day moving average. Long-dated yields are technically stretched to the upside, but our valuation index highlights that bonds are still extremely expensive and that yields have room to move higher over the cyclical investment horizon. The technical and valuation profile is similar for the US dollar. The USD is technically oversold, but it remains expensive according to our models. We noted in Section 1 of this month’s report that the dollar has traded almost exactly in line with what one would expect from a counter-cyclical currency, suggesting that USD will continue to trend lower, at a more moderate pace, over the coming year. Raw industrials prices have recovered not just back to pre-pandemic levels, but also back to 2018 levels (i.e., before the Sino/US trade war). This underscores that many commodity prices are extended, and are likely due for a breather. US and global LEIs remain in a solid uptrend. A peak in our global LEI (GLEI) diffusion index suggests that the pace of advance in the GLEI will moderate, but the diffusion index has not yet fallen to a level that would herald a meaningful decline in the LEI. The waning US payroll momentum that we flagged in last month’s Section 3 culminated in a slowdown in economic activity that is likely to linger for the coming several weeks. However, the very significant amount of stimulus that is still set to arrive will provide a substantial reflationary bridge to help counter the negative impact on Q1 growth from the pandemic. EQUITIES: Chart III-1US Equity Indicators

US Equity Indicators

US Equity Indicators

Chart III-2Willingness To Pay For Risk

Willingness To Pay For Risk

Willingness To Pay For Risk

Chart III-3US Equity Sentiment Indicators

US Equity Sentiment Indicators

US Equity Sentiment Indicators

Chart III-4Revealed Preference Indicator

Revealed Preference Indicator

Revealed Preference Indicator

Chart III-5US Stock Market Valuation

US Stock Market Valuation

US Stock Market Valuation

Chart III-6US Earnings

US Earnings

US Earnings

Chart III-7Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

Chart III-8Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

FIXED INCOME: Chart III-9US Treasurys And Valuations

US Treasurys And Valuations

US Treasurys And Valuations

Chart III-10Yield Curve Slopes

Yield Curve Slopes

Yield Curve Slopes

Chart III-11Selected US Bond Yields

Selected US Bond Yields

Selected US Bond Yields

Chart III-1210-Year Treasury Yield Components

10-Year Treasury Yield Components

10-Year Treasury Yield Components

Chart III-13US Corporate Bonds And Health Monitor

US Corporate Bonds And Health Monitor

US Corporate Bonds And Health Monitor

Chart III-14Global Bonds: Developed Markets

Global Bonds: Developed Markets

Global Bonds: Developed Markets

Chart III-15Global Bonds: Emerging Markets

Global Bonds: Emerging Markets

Global Bonds: Emerging Markets

CURRENCIES: Chart III-16US Dollar And PPP

US Dollar And PPP

US Dollar And PPP

Chart III-17US Dollar And Indicator

US Dollar And Indicator

US Dollar And Indicator

Chart III-18US Dollar Fundamentals

US Dollar Fundamentals

US Dollar Fundamentals

Chart III-19Japanese Yen Technicals

Japanese Yen Technicals

Japanese Yen Technicals

Chart III-20Euro Technicals

Euro Technicals

Euro Technicals

Chart III-21Euro/Yen Technicals

Euro/Yen Technicals

Euro/Yen Technicals

Chart III-22Euro/Pound Technicals

Euro/Pound Technicals

Euro/Pound Technicals

COMMODITIES: Chart III-23Broad Commodity Indicators

Broad Commodity Indicators

Broad Commodity Indicators

Chart III-24Commodity Prices

Commodity Prices

Commodity Prices

Chart III-25Commodity Prices

Commodity Prices

Commodity Prices

Chart III-26Commodity Sentiment

Commodity Sentiment

Commodity Sentiment

Chart III-27Speculative Positioning

Speculative Positioning

Speculative Positioning

ECONOMY: Chart III-28US And Global Macro Backdrop

US And Global Macro Backdrop

US And Global Macro Backdrop

Chart III-29US Macro Snapshot

US Macro Snapshot

US Macro Snapshot

Chart III-30US Growth Outlook

US Growth Outlook

US Growth Outlook

Chart III-31US Cyclical Spending

US Cyclical Spending

US Cyclical Spending

Chart III-32US Labor Market

US Labor Market

US Labor Market

Chart III-33US Consumption

US Consumption

US Consumption

Chart III-34US Housing

US Housing

US Housing

Chart III-35US Debt And Deleveraging

US Debt And Deleveraging

US Debt And Deleveraging

Chart III-36US Financial Conditions

US Financial Conditions

US Financial Conditions

Chart III-37Global Economic Snapshot: Europe

Global Economic Snapshot: Europe

Global Economic Snapshot: Europe

Chart III-38Global Economic Snapshot: China

Global Economic Snapshot: China

Global Economic Snapshot: China

Jonathan LaBerge, CFA Vice President The Bank Credit Analyst Footnotes 1 Please see USBS Strategy Report "The Case Against The Money Supply," dated June 30, 2020, available at usbs.bcaresearch.com 2 Please see “Money creation in the modern economy,” Bank of England, Q1 2014 Quarterly Bulletin.

Highlights The general public and the financial markets have unrealistic hopes for what a Covid vaccine can achieve. The Covid vaccine will not be like the ‘one and done’ measles vaccine, but more like the ‘frequent jab’ seasonal flu vaccine. Underweight the so-called ‘economy reopening’ plays, particularly basic resources. The so-called ‘pandemic plays’ still have a lot of structural upside. As such, long-term investors should avoid value, and stick with growth. Stay structurally overweight healthcare, as governments will realise that the smart strategy is to add capacity to their healthcare systems. Stay structurally overweight healthcare-heavy DM versus resource-heavy EM. Fractal trade: Short KRW/USD. Feature Chart of the WeekThe UK Healthcare System Reached Its Limit At 60 Thousand Daily Covid Infections

The UK Healthcare System Reached Its Limit At 60 Thousand Daily Covid Infections

The UK Healthcare System Reached Its Limit At 60 Thousand Daily Covid Infections

The general public and financial markets have high hopes that a vaccine can banish Covid forever, just like the vaccine for measles gives us lifelong immunity against the disease. Unfortunately, these hopes are unrealistic (Chart I-2). Chart I-2Reopening' Plays Are Due A Reversal

Reopening' Plays Are Due A Reversal

Reopening' Plays Are Due A Reversal

The latest evidence suggests that the Covid vaccine will not be like the ‘one and done’ measles vaccine. It will be more like the seasonal flu vaccine, requiring regular refreshing. As if to prove this point, Moderna announced this week that it will trial a new Covid vaccine to tackle variants of the virus. Vaccines Against RNA Viruses Are Not Highly Effective Measles, the flu, and Covid are all diseases caused by ‘RNA viruses’ in contrast to, say, smallpox which is caused by a ‘DNA virus.’ One of defining characteristics of RNA versus DNA is its inferior proofreading ability during replication. As a result, RNA viruses have very high mutation rates. This means there are very few effective vaccinations against them. As the Journal of Immunology Research puts it:1 “No vaccine or specific treatment is available for many of these RNA viruses and some of the available vaccines and treatments are not highly effective.” Measles is an exception. While the flu virus mutates constantly and requires a yearly jab, a two-dose vaccine against measles during childhood confers lifelong immunity. This is because the measles virus is ‘antigenically monotypic.’ In plain English, the proteins that the measles virus uses to infect a cell cannot mutate even slightly without breaking. Meaning that any mutation to the virus destroys its ability to infect. Hence, the measles virus cannot evade the ‘one and done’ childhood vaccine. Is the Covid virus antigenically monotypic? No, we now know that the Covid virus can mutate and still infect, because we have already seen three region-specific mutations – the Brazilian variant, the UK variant, and the South African variant. The next question is, can any of these mutations evade the current vaccinations? Unfortunately, the answer is yes. As researchers at the South Africa National Institute for Communicable Diseases point out:2 “SARS-CoV-2 501Y.V2 (the South African variant), a novel lineage of the coronavirus causing COVID-19, contains multiple mutations within two immunodominant domains of the spike protein… This lineage exhibits complete escape from three classes of therapeutically relevant monoclonal antibodies… and may foreshadow reduced efficacy of current spike-based vaccines.” (Figure I-1) Figure 1Vaccines Against RNA Viruses Are Not Highly Effective

Measles Or The Flu? – Covid’s Vaccine Response Is Critical

Measles Or The Flu? – Covid’s Vaccine Response Is Critical

But if the current spike-based vaccines have only limited efficacy, why aren’t the vaccine manufacturers and policymakers warning us? The answer is that they are, but in coded form. Moderna’s decision to trial a new vaccine is a coded warning that its current vaccine might have only limited efficacy against emerging variants. Meanwhile, the UK health minister, Matt Hancock recently warned: “If we vaccinated the population, and then you got in a new variant that evaded the vaccine, then we’d be back to square one.” These warnings are coded because anything more blatant would undermine the mass vaccination programs that governments have spent a lot of blood, sweat, and tears (and money) to initiate. Furthermore, when the healthcare system is at breaking point, a vaccine that provides limited efficacy is better than no vaccine at all. In fact, whether the current vaccines are effective or not against the South African variant is moot. The much bigger point is that, just like the flu virus, the Covid virus will continue to mutate. And the mutations of the virus that get around the population’s immunity are more likely to spread and become the new dominant strains. If the current mutations cannot evade the vaccinations, then a future mutation eventually will. It’s just a matter of time. The immunity from the Covid vaccine will be short-lived. Hence, the evidence strongly suggests that the immunity from the Covid vaccine will be short-lived. How To Contain Covid Unlike smallpox and the measles, a mass vaccination program for Covid is unlikely to banish the disease. Instead, like the flu, vaccination will only contain the disease before it re-emerges in a new guise within a year or, worse, six months. In this regard, the Australia/New Zealand strategy of sealing national borders is not a strategy. It just buys time to form a strategy. No advanced open economy can shut its borders for ever. Meanwhile, a strategy to implement an all-seeing government track and trace system seems to be successful in China. However, it would be impossible to implement in liberal democracies, where the public would not accept the government watching your every move. In which case, can we just adopt the same strategy for Covid as we use for the seasonal flu – offer vaccinations to the most medically vulnerable once or twice a year? In theory, yes. But in practice, this strategy would overwhelm our healthcare systems. This we know because a bad flu season, by itself, was already pushing some healthcare systems to the limit. So how would this strategy cope with Covid, which creates conservatively five times as many casualties? Understand that the key metric is not the mortality rate, but the morbidity (severe illness) rate. Or more specifically, the morbidity rate versus the healthcare system’s intensive care unit (ICU) capacity (Chart I-3). Death requires very little medical intervention and resource, whereas severe illness requires massive medical intervention and resource. Moreover, when the severe illness is a respiratory illness, it leaves the sufferer struggling to breathe and needing critical care. No civilized society can deny critical care to somebody who is struggling to breathe (Chart I-4). Chart I-3Critical Care Capacity Is Limited

Measles Or The Flu? – Covid’s Vaccine Response Is Critical

Measles Or The Flu? – Covid’s Vaccine Response Is Critical

Chart I-4Healthcare Systems Are Running Out Of Capacity

Healthcare Systems Are Running Out Of Capacity

Healthcare Systems Are Running Out Of Capacity