Europe

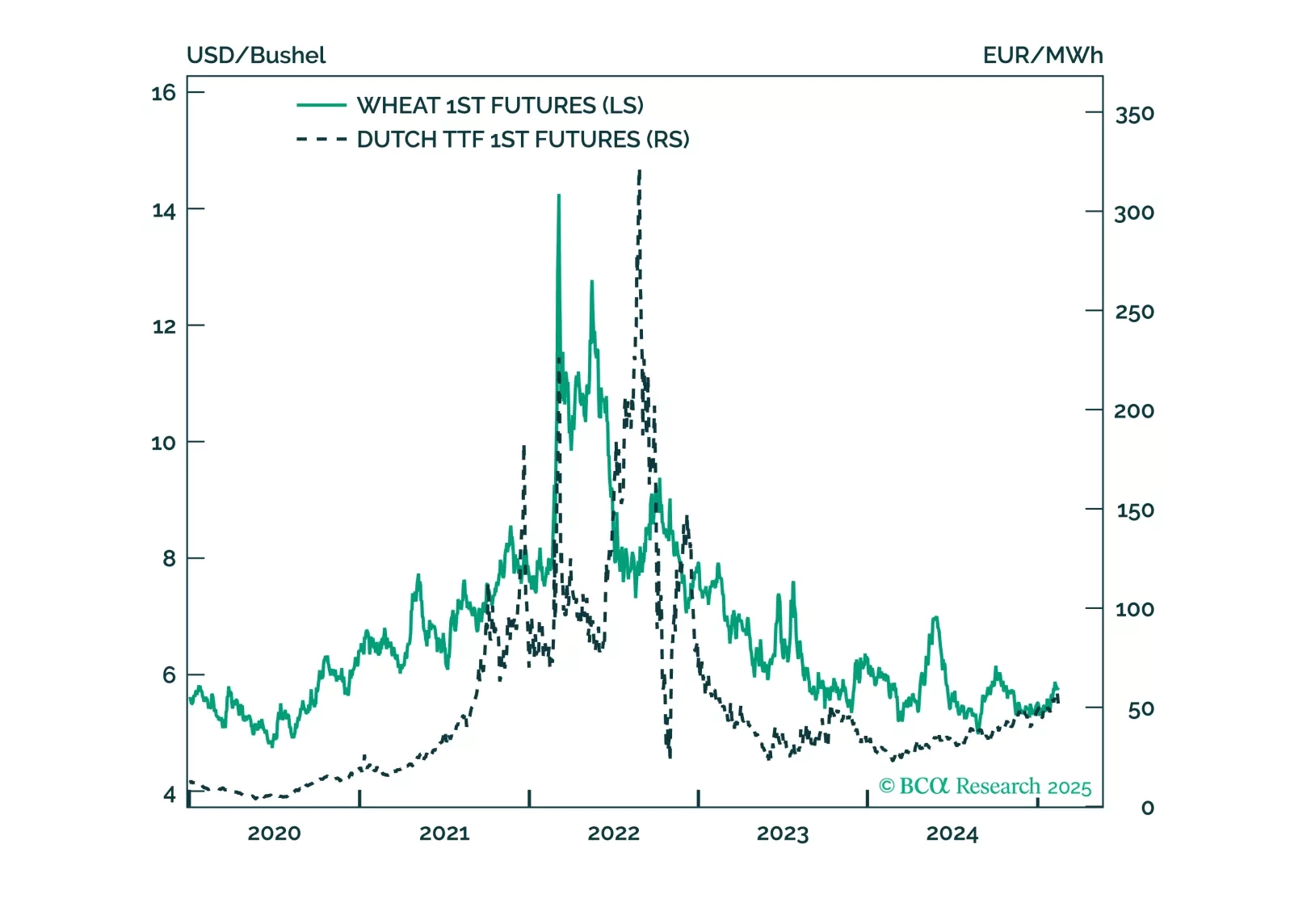

President Trump is negotiating a ceasefire in Ukraine. This will be a marginal headwind to some commodities which benefitted from the conflict like natural gas and wheat, and will be a marginal tailwind for European assets, specifically EM Europe. Use Trump’s tariff shock as an opportunity to buy European assets.

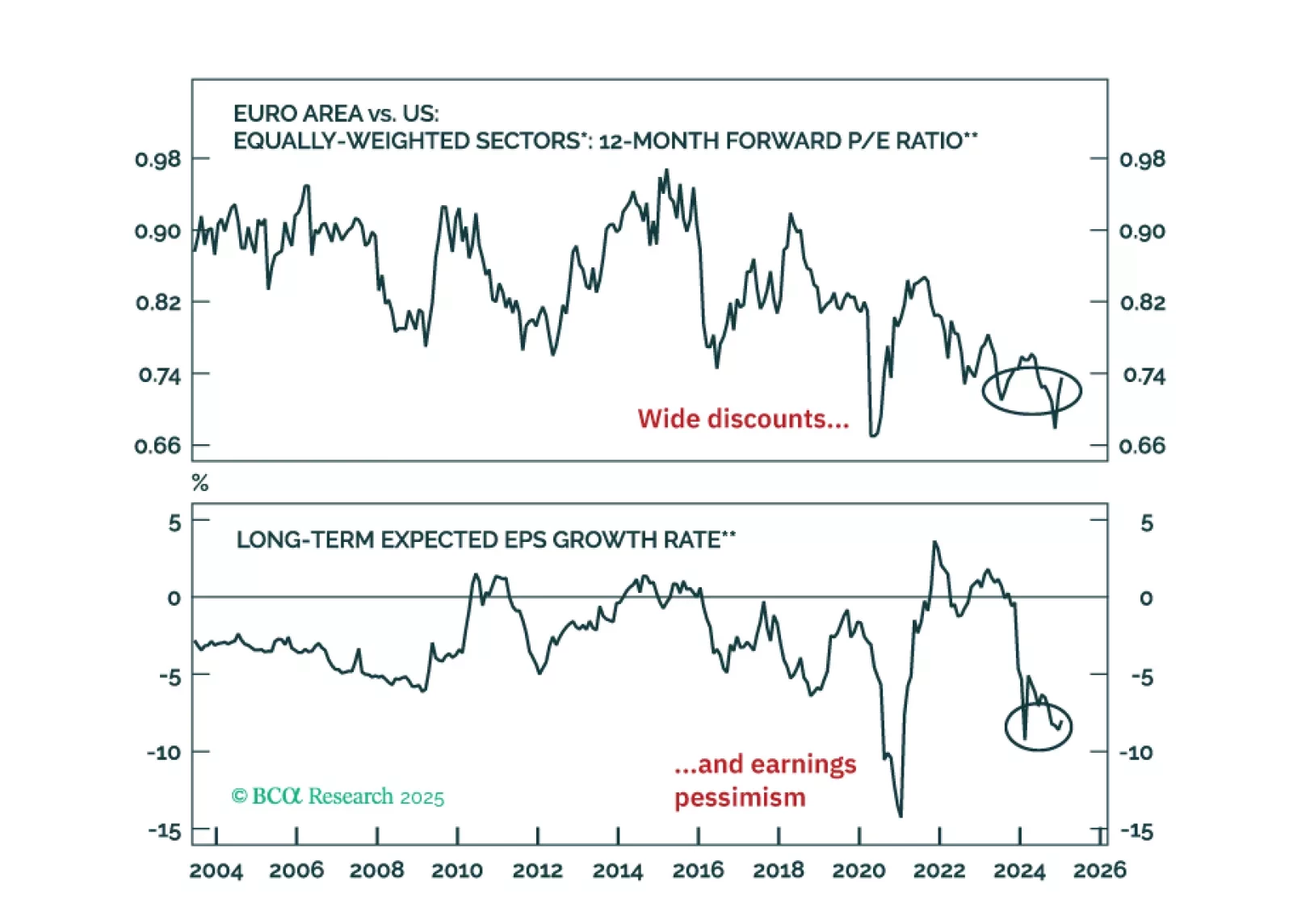

Thanks to their attractive valuations, European equities are piquing the interest of global investors. Is there more to the appeal of European stocks or do they remain a mere value trap?

Thanks to their attractive valuations, European equities are piquing the interest of global investors. Is there more to the appeal of European stocks or do they remain a mere value trap?

Questions about fiscal risks and their impact on bond markets have become more frequent in client conversations. This Special Report provides a framework to assess a country’s fiscal sustainability and how it affects its bond market outlook. On an individual country basis, Spain has shown a remarkable turnaround in its fiscal sustainability outlook while the fiscal outlook for France continues to deteriorate.

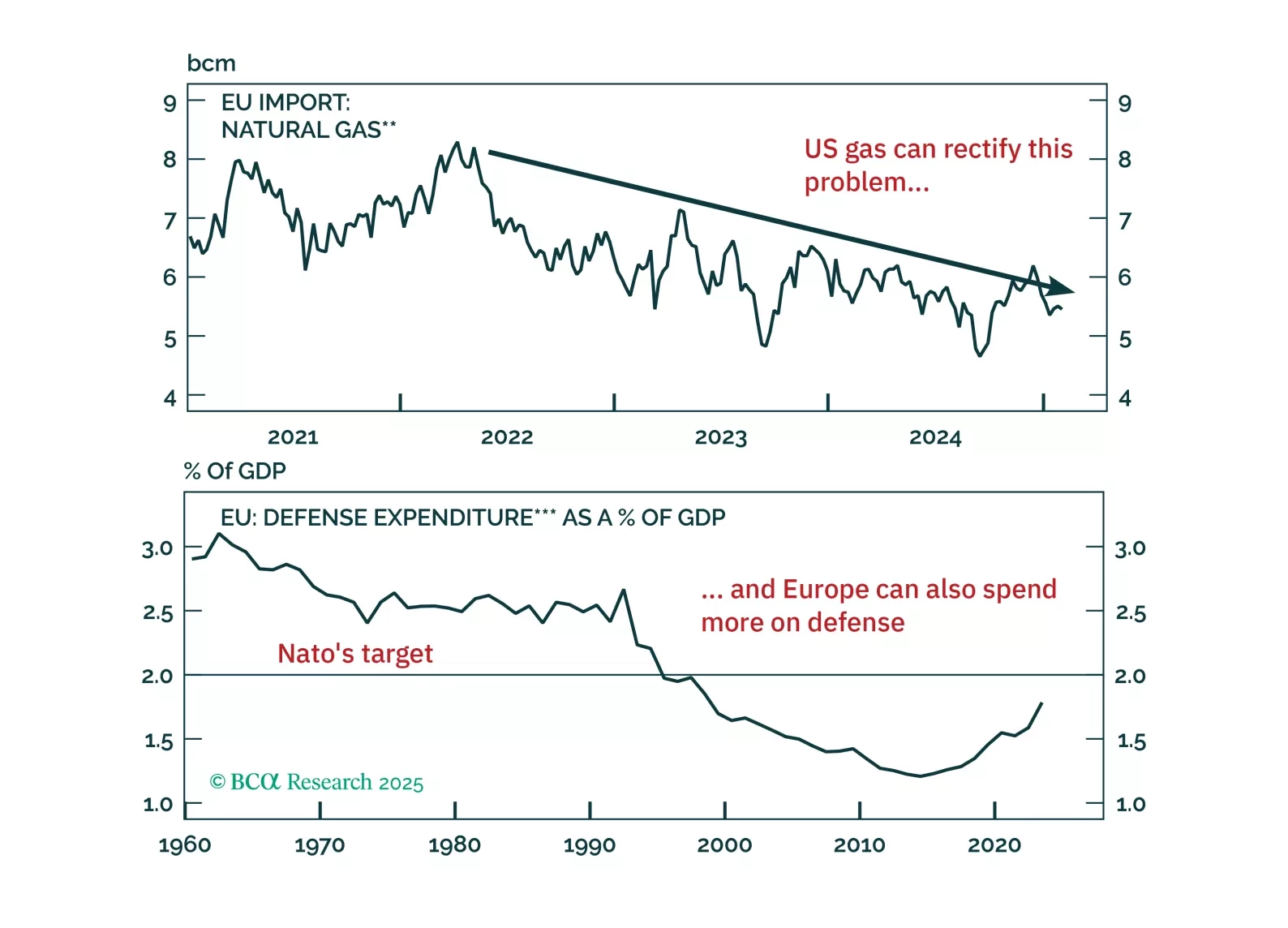

Europe is about to become President Trump’s next target. The good news: a US/EU trade war will be short as common ground to achieve a deal exists. The bad news: European assets remain at the mercy of heightened uncertainty. How should investors position themselves in this tricky context?

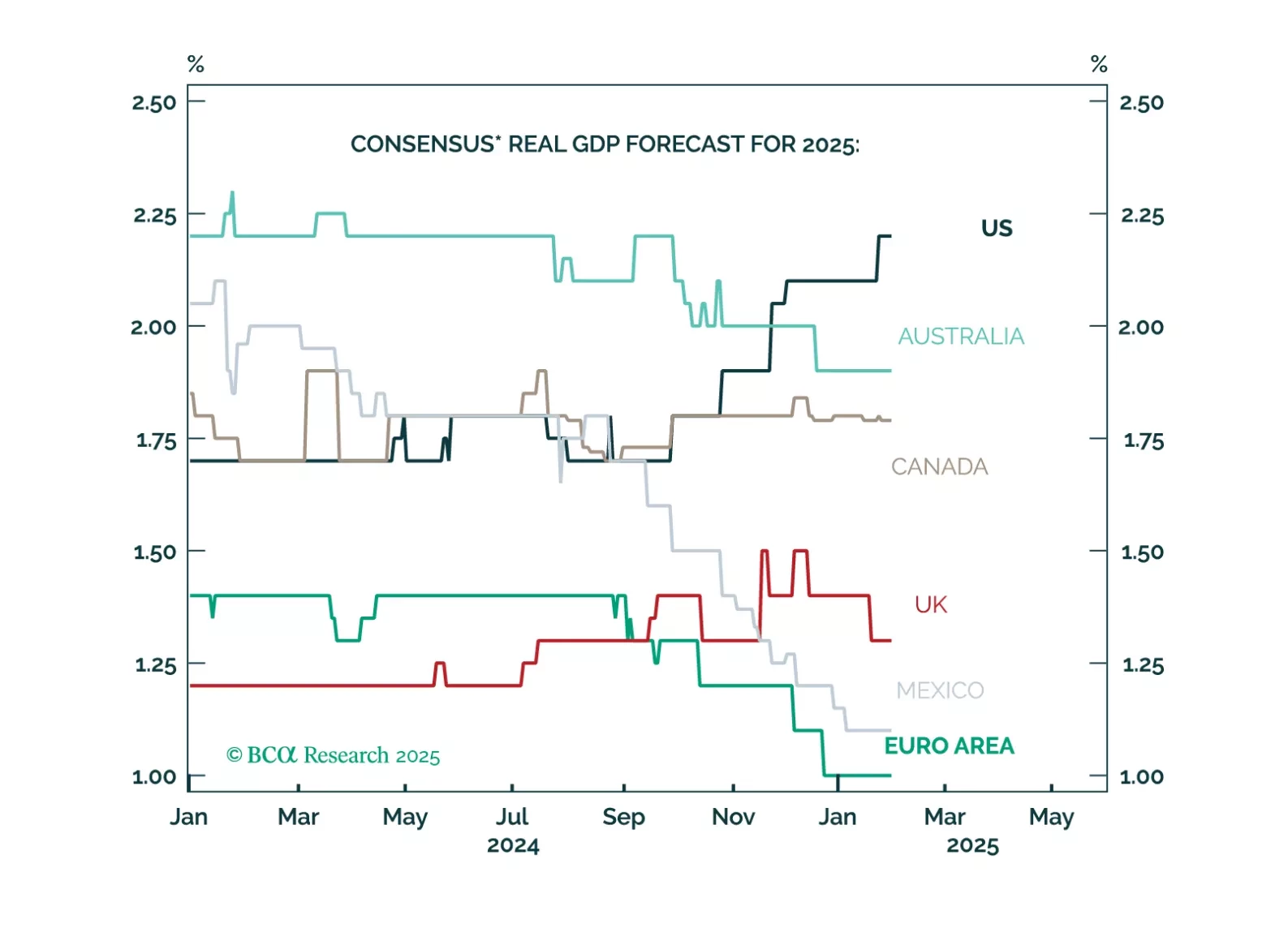

Markets and forecasters anticipate a “Golden Age” for Trump’s America, with US growth expectations soaring while the rest of the world lags. However, this extreme optimism means that there is a lot of room for disappointment. Cooling income growth, weak housing and less deficit spending than expected will result in US growth underperforming expectations. Maintain a modest underweight to equities and modest overweight to fixed income. US markets have become more expensive relative to the rest of the world even as quality differentials have stabilized. Prepare to downgrade US equities to underweight and to upgrade Euro Area and China to overweight. We will wait to pull the trigger until we have more clarity on trade policy and when the dollar's momentum turns negative.

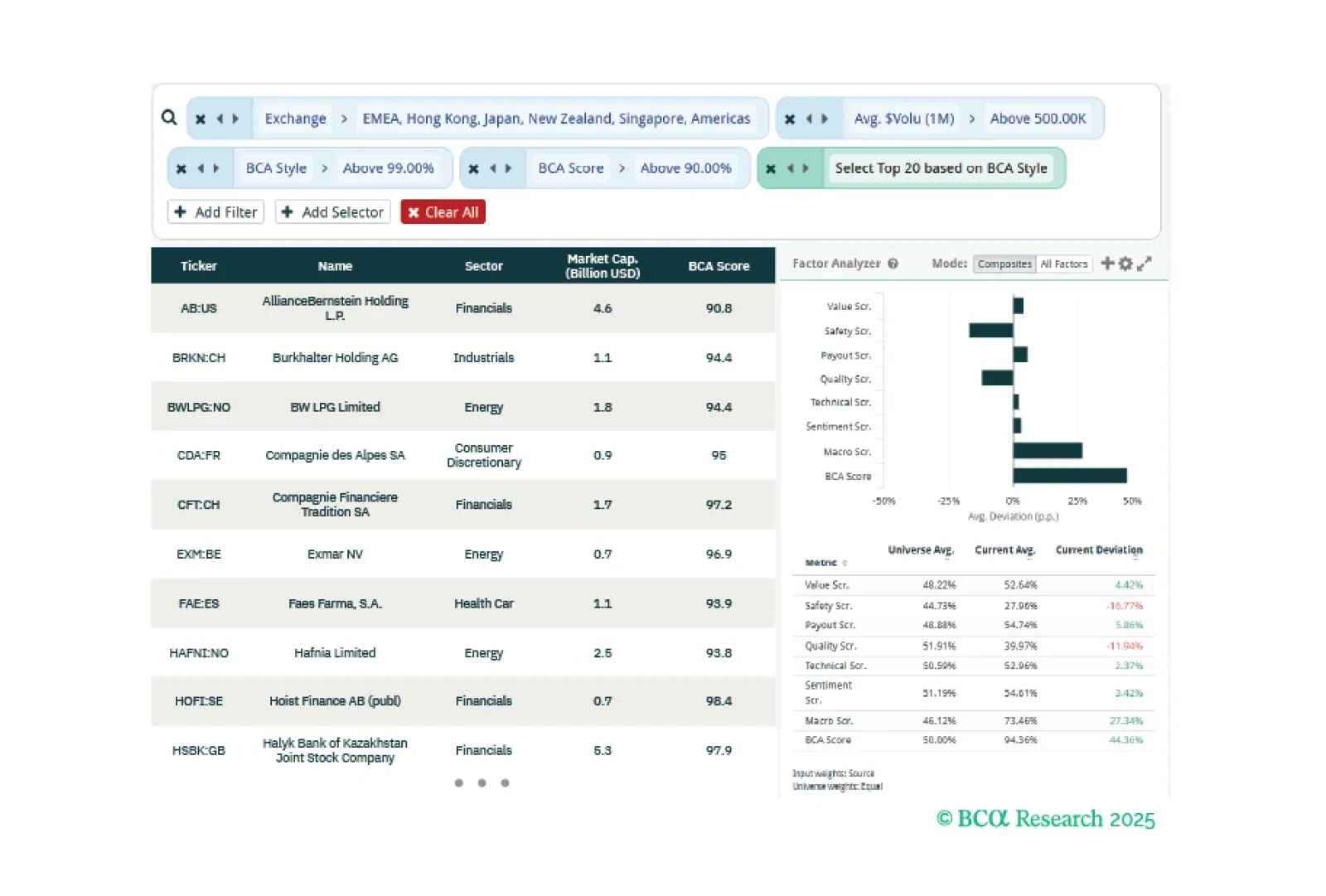

This week, our three screeners explore global small-cap value stocks, European equities, and BCA’s nuclear energy themed equity baskets.