Factors

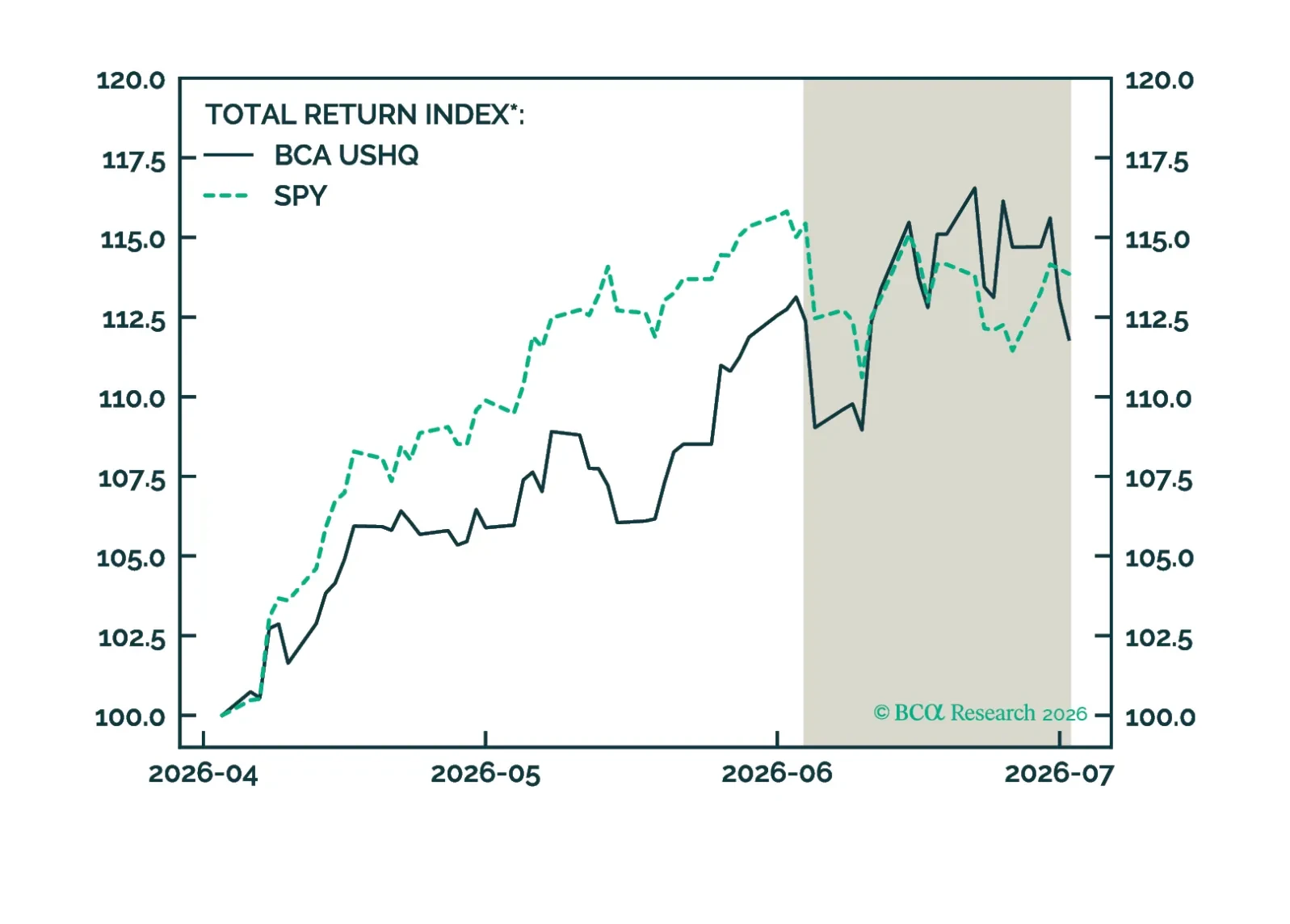

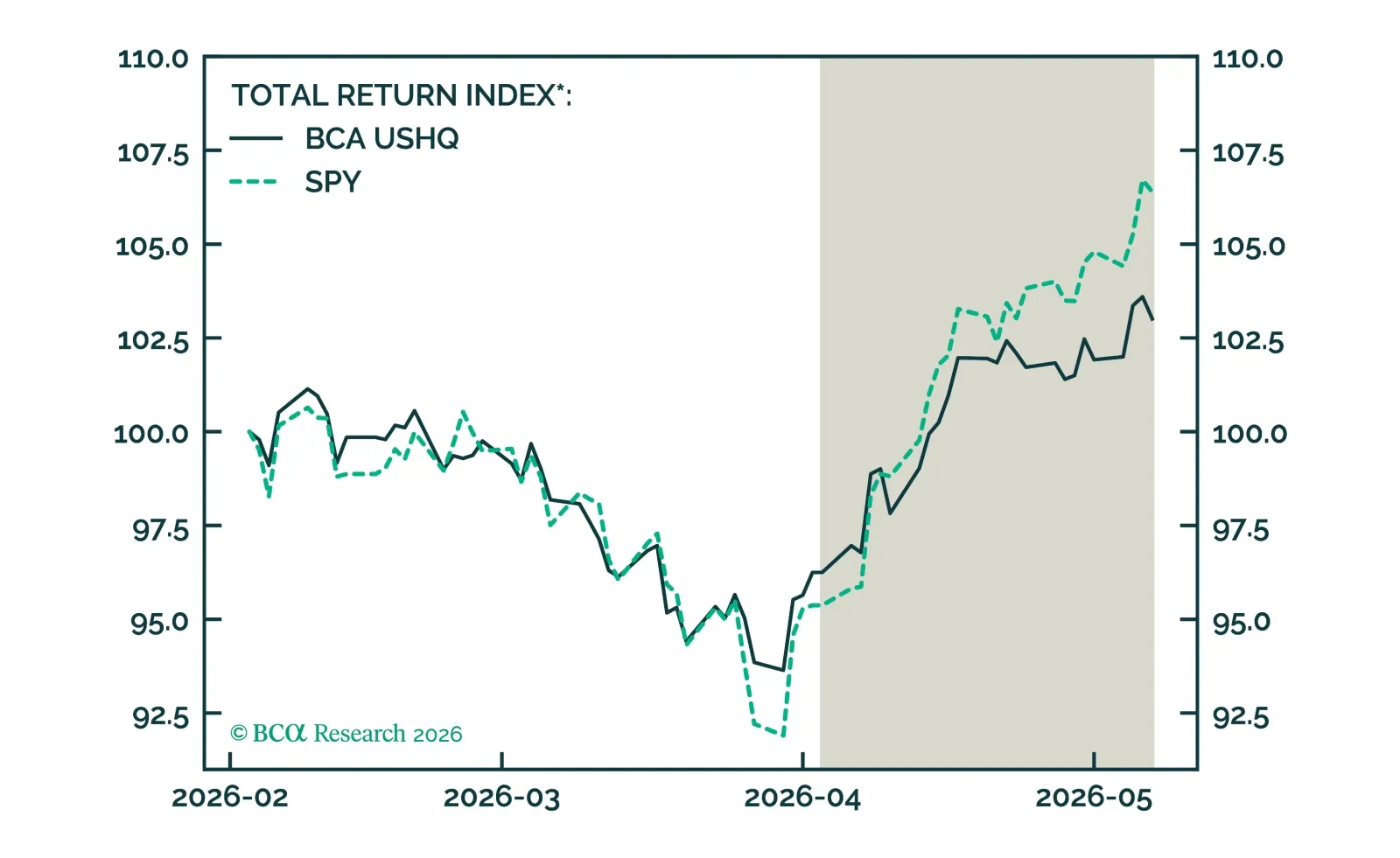

The US High Quality (USHQ) portfolio outperformed its benchmark through June, returning -0.50%, while its SPY benchmark returned -1.37%. On a trailing three-month basis, the USHQ portfolio’s performance was weaker than the benchmark, with USHQ underperforming by approx. 205bps.

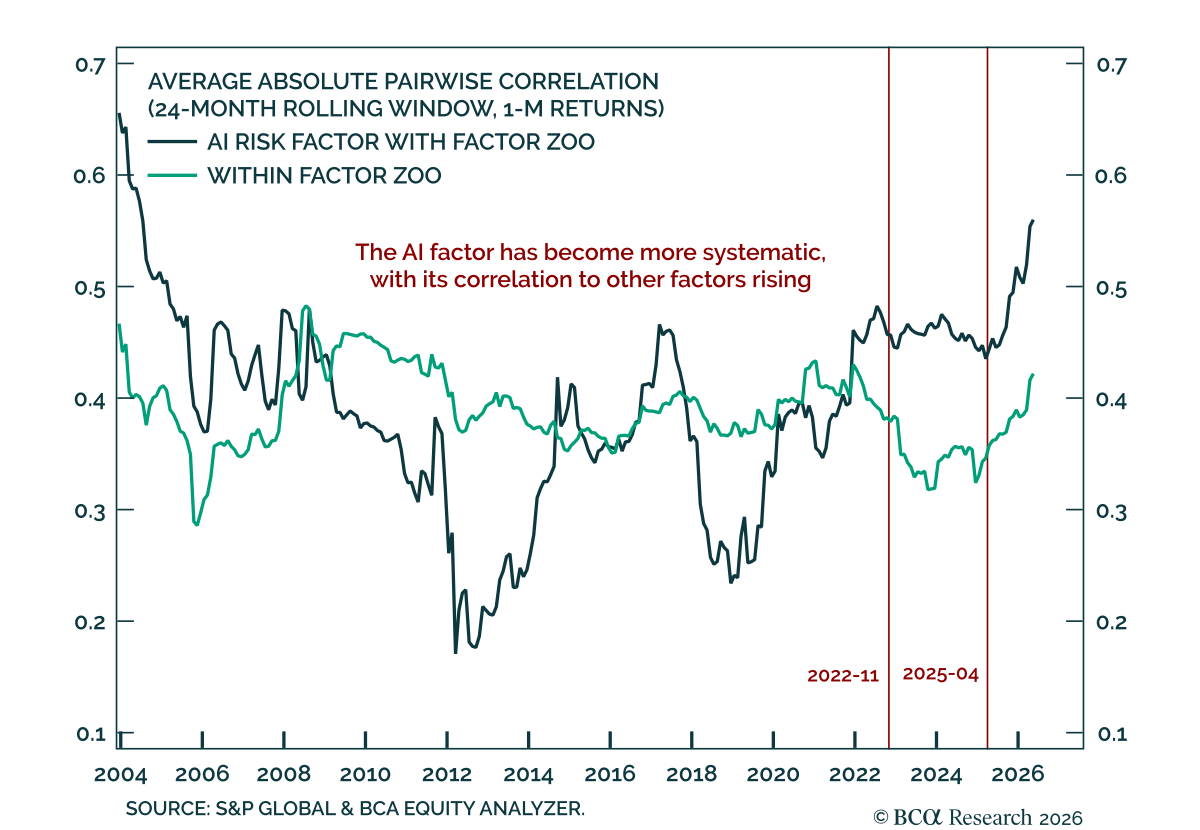

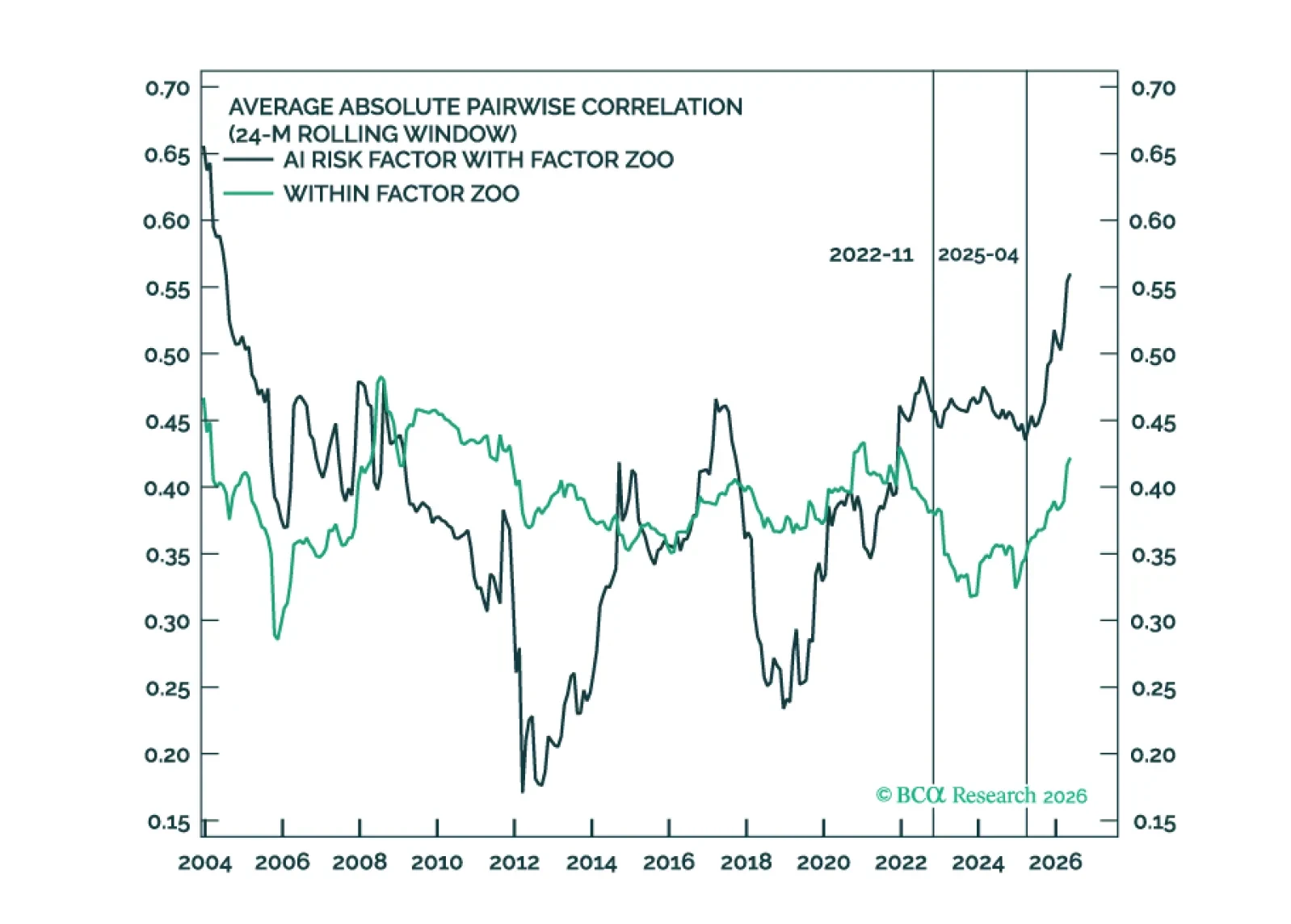

The S&P 500 has become increasingly concentrated. We know that. But the critical question is not how many stocks are driving the market; it is how many factors are driving stocks. We define an AI risk factor to test whether AI has become the dominant common exposure throughout much of the factor zoo.

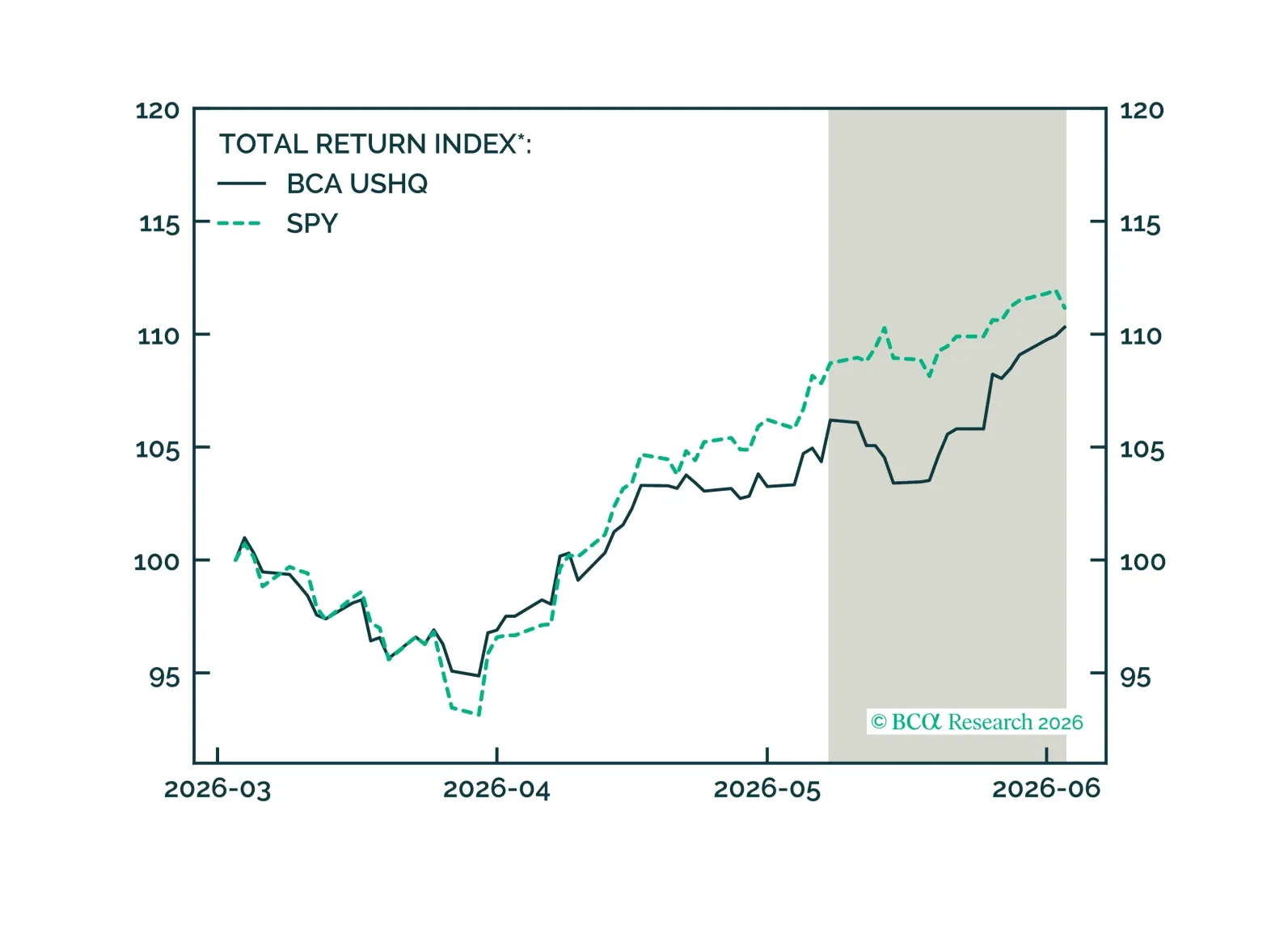

The US High Quality (USHQ) portfolio outperformed its benchmark through May, returning 3.88%, while its SPY benchmark returned 2.25%. On a trailing three-month basis, the USHQ portfolio’s performance was weaker than the benchmark, with USHQ underperforming by approx. 86bps.

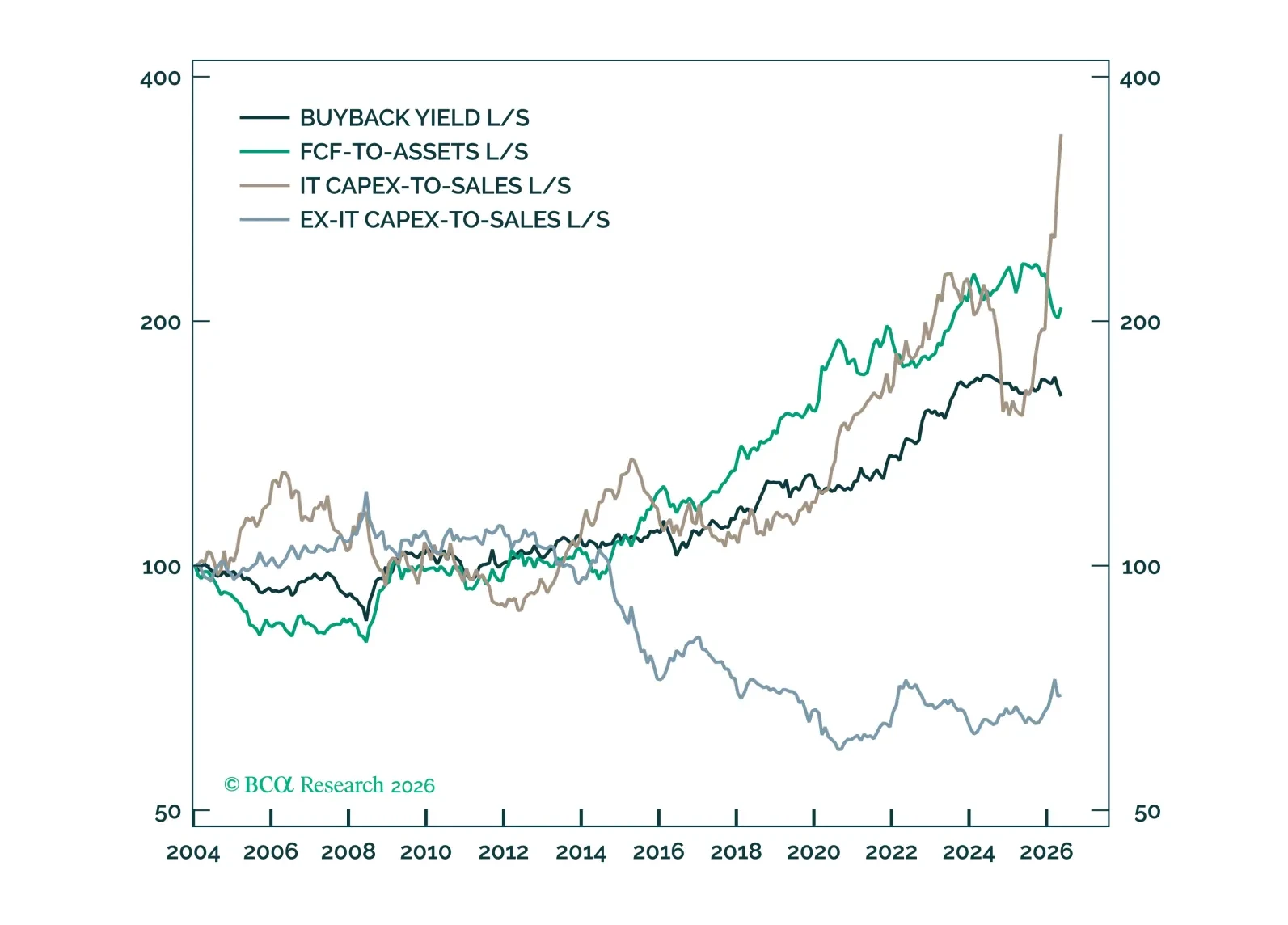

Tech, and increasingly the market, is moving from a cash-return regime to a reinvestment regime. After the GFC, investors rewarded companies that returned cash to investors. In the AI cycle, they are rewarding companies that put that cash back to work. This is not just a story of falling free cash flow; it is the mirror image of a market rewarding reinvestment. Tech has defined both regimes, revealing the old cash-flow “stars” as sector bets masquerading as alpha.

The US High Quality (USHQ) portfolio underperformed its benchmark through April, returning 7.02%, while its SPY benchmark returned 11.55%. On a trailing three-month basis, the USHQ portfolio’s performance was weaker than the benchmark as well, with USHQ underperforming by approx. 338bps.

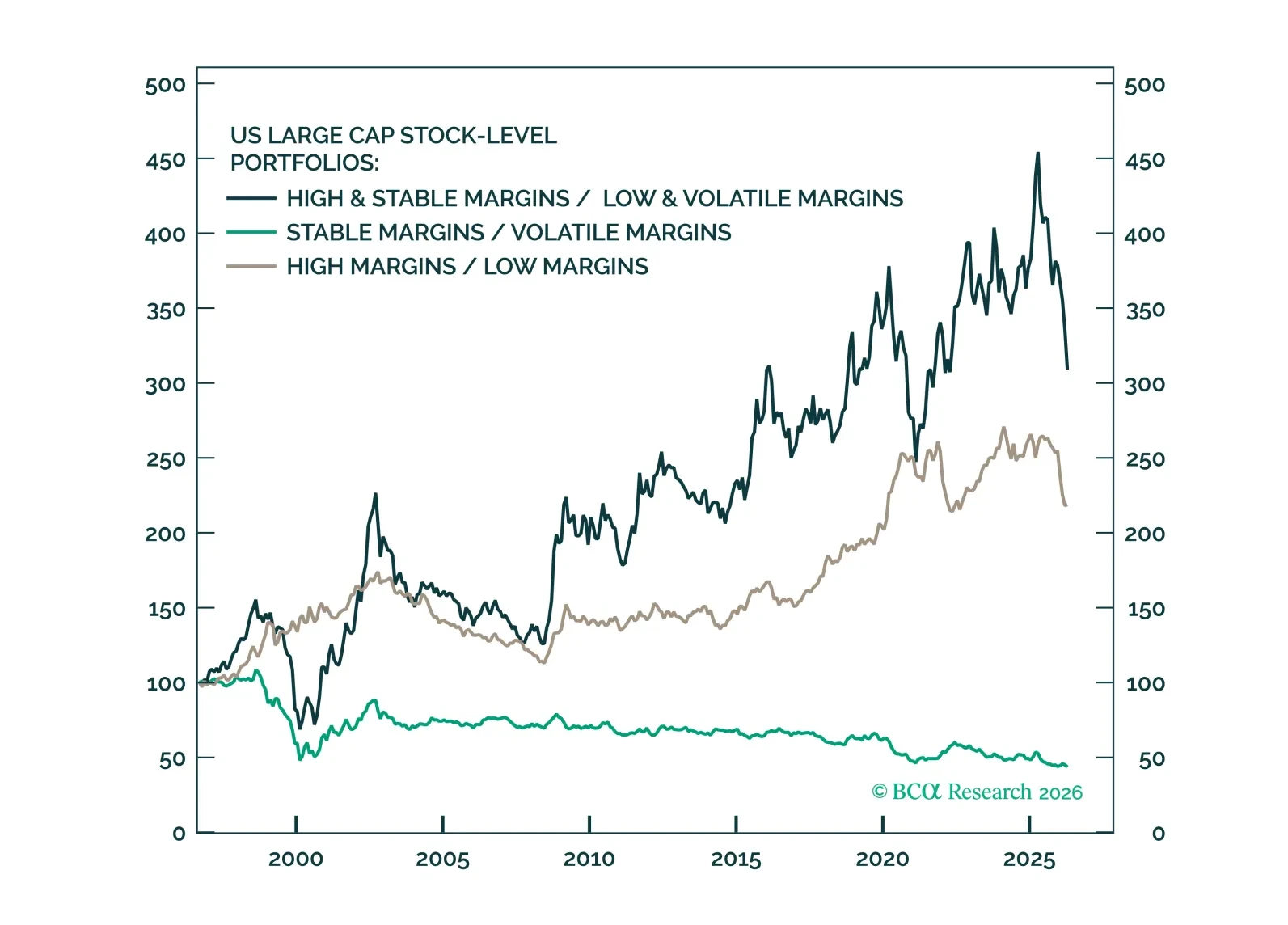

Based on our previous work on margins, three aspects of margins may matter to investors: their level, their variability, and their likely trend. We add two margin-themed baskets: a stock-level High & Stable vs. Low & Volatile basket and an industry-level AI-Supported vs. AI-Insulated basket.

Based on our previous work on margins, three aspects of margins may matter to investors: their level, their variability, and their likely trend. We add two margin-themed baskets: a stock-level High & Stable vs. Low & Volatile basket and an industry-level AI-Supported vs. AI-Insulated basket.

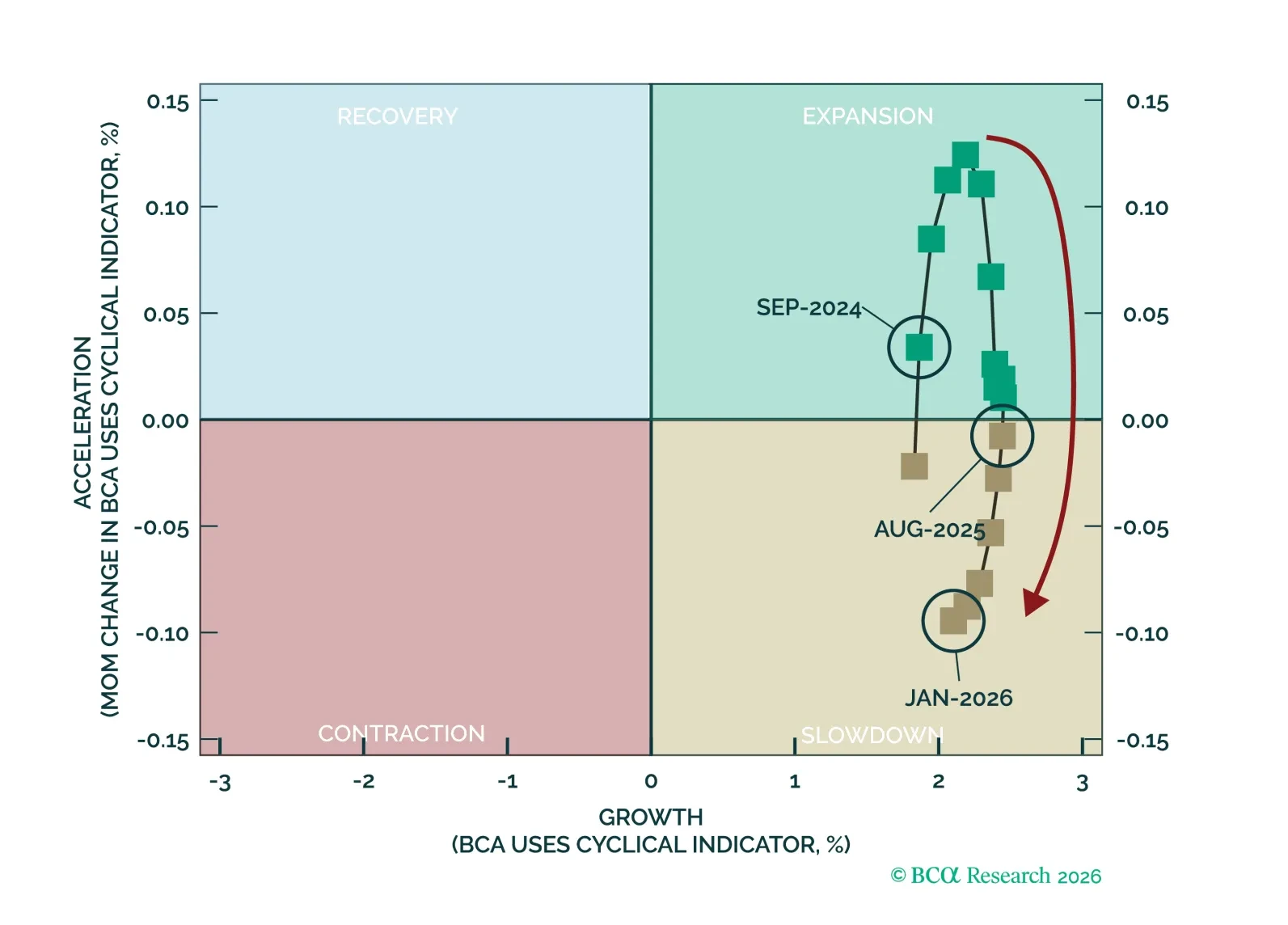

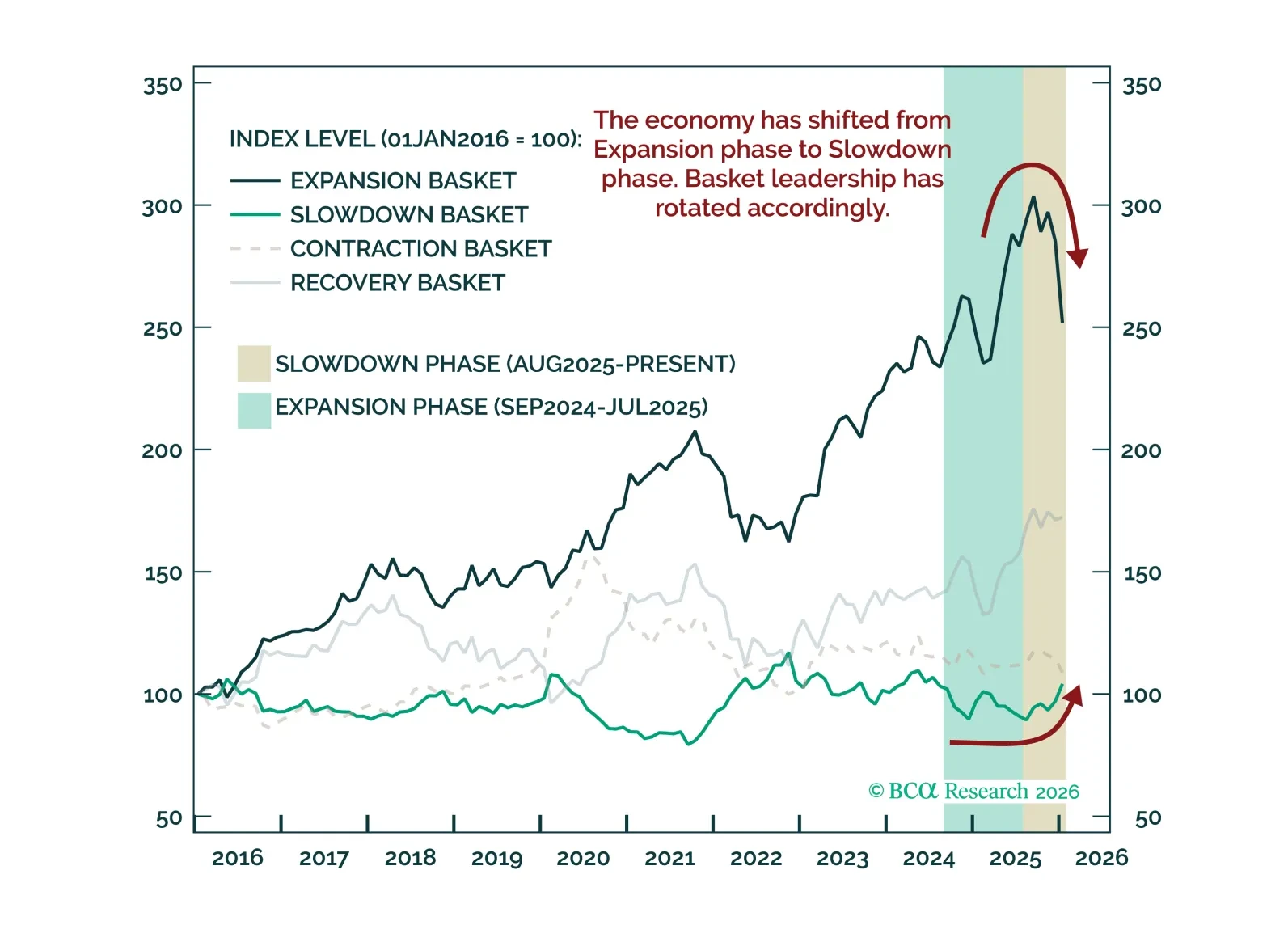

This screener report builds on the US Equity Strategy and Equity Analyzer collaboration published on 23 February 2026, where we introduced our latest framework for assessing the US business cycle. Here, we apply the framework to our screener to identify how bottom-up equity positioning should adapt as the cycle evolves.

The US economy is in the Slowdown phase of the business cycle, according to our measure of aggregate US economic activity; growth remains positive but acceleration is negative. Historically, this phase more often resolves in reacceleration than recession. Recent market price action, from the index, to sectors, to relative industry performance, broadly reflects typical Slowdown phase dynamics.