Financial Markets

After entering 2025 with depressed growth expectations, measures of European sentiment have seemingly bottomed, and European assets rallied. However, given the changing geopolitical order and Europe’s forceful response thus far, are we at a structural turning…

This report is our Part III series on valuation and subsequent returns, where we recalibrate our short-term models to emphasize signals over the next nine-to-twelve months. We will henceforth call these models STTM: Short Term Timing Models.

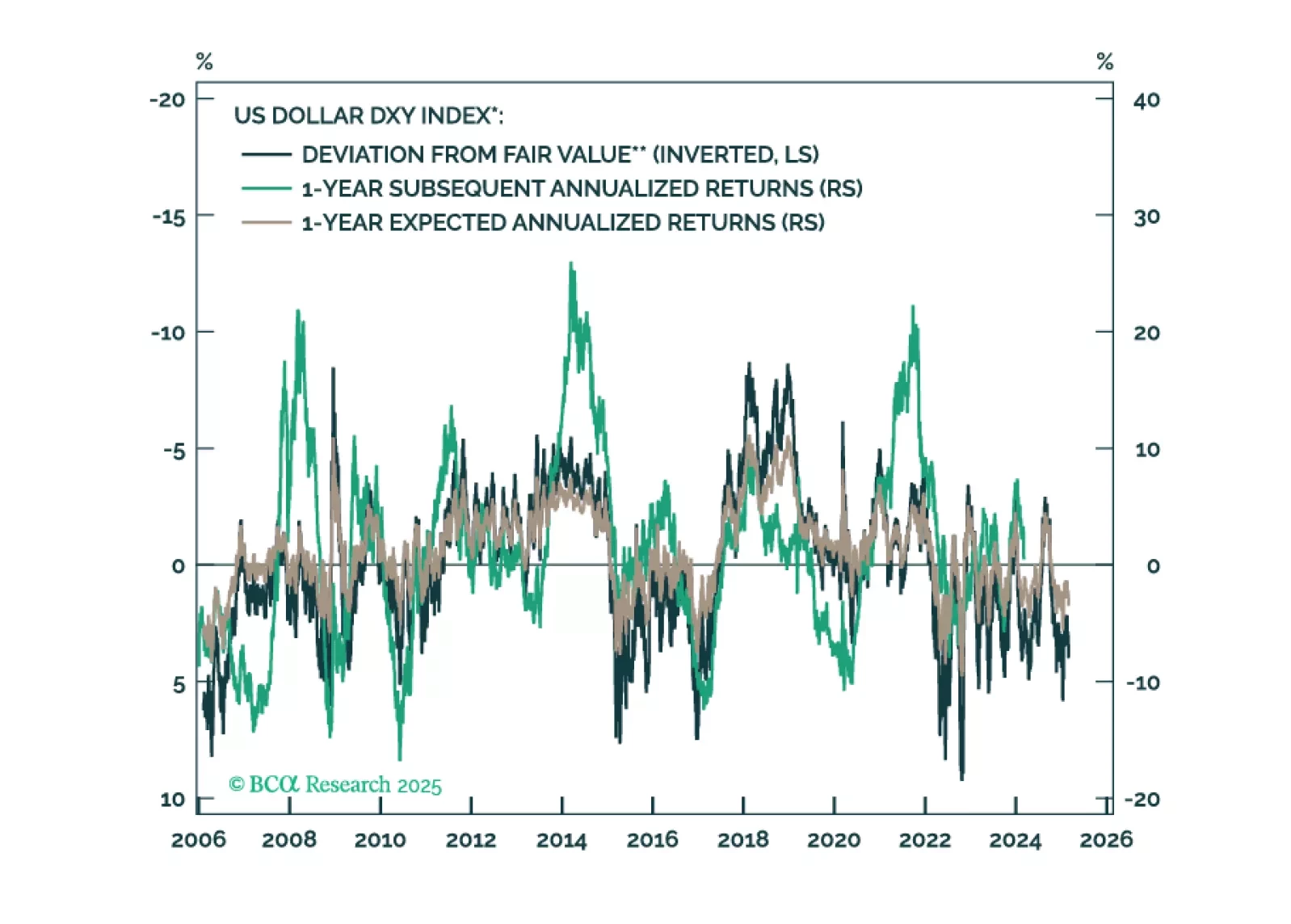

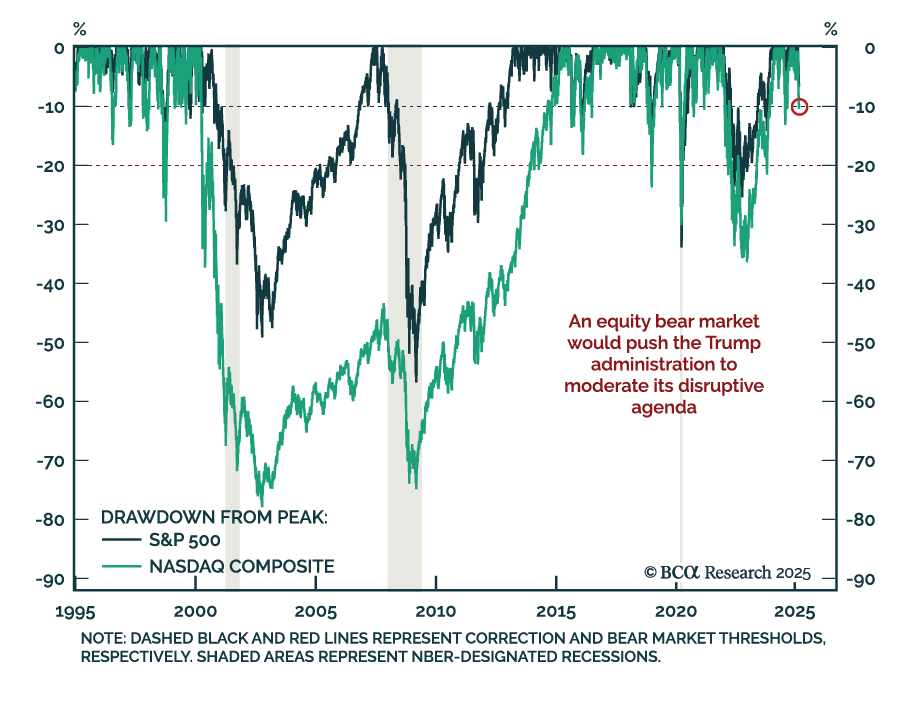

Treasury Secretary Scott Bessent said there is no “Trump put”, and acknowledged the administration’s policy could create short-term pain to achieve long-term gains. The concept of a “market put” implies policymakers would aim to put a floor under the equity…

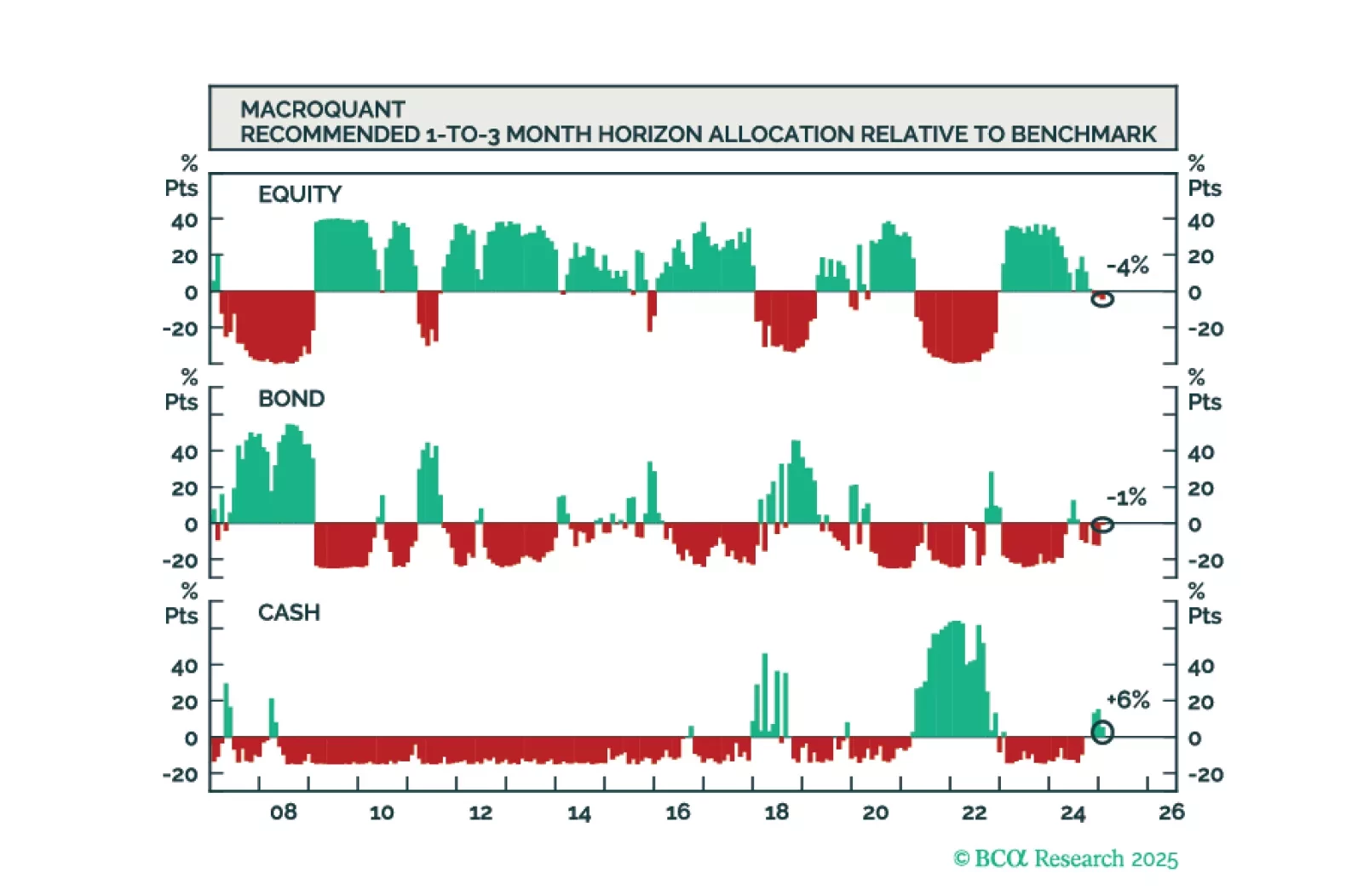

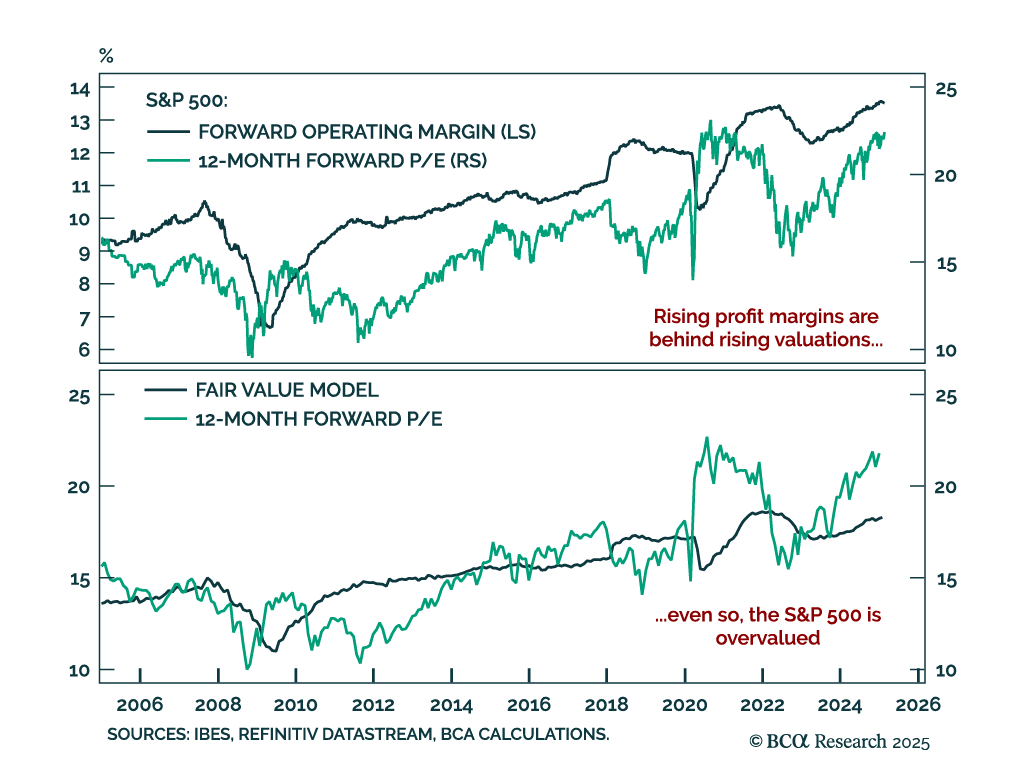

The MacroQuant model is no longer bullish on stocks but is not yet prepared to turn underweight. Subjectively, the Global Investment Strategy team is more bearish on equities than the model.

The MacroQuant model is no longer bullish on stocks but is not yet prepared to turn underweight. Subjectively, the Global Investment Strategy team is more bearish on equities than the model.

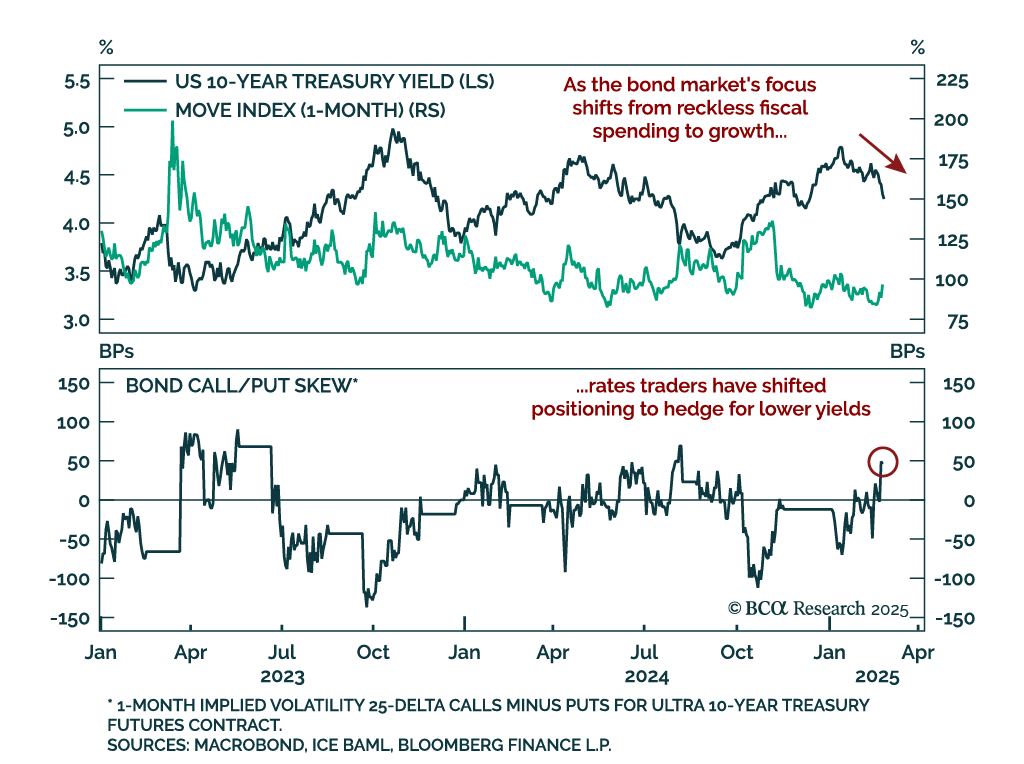

Our US Equity strategists held a roundtable, which led to many client questions addressed in the team’s latest report. Long-term interest rates will decline if disinflation persists, deficits shrink, or economic growth slows, though each scenario…

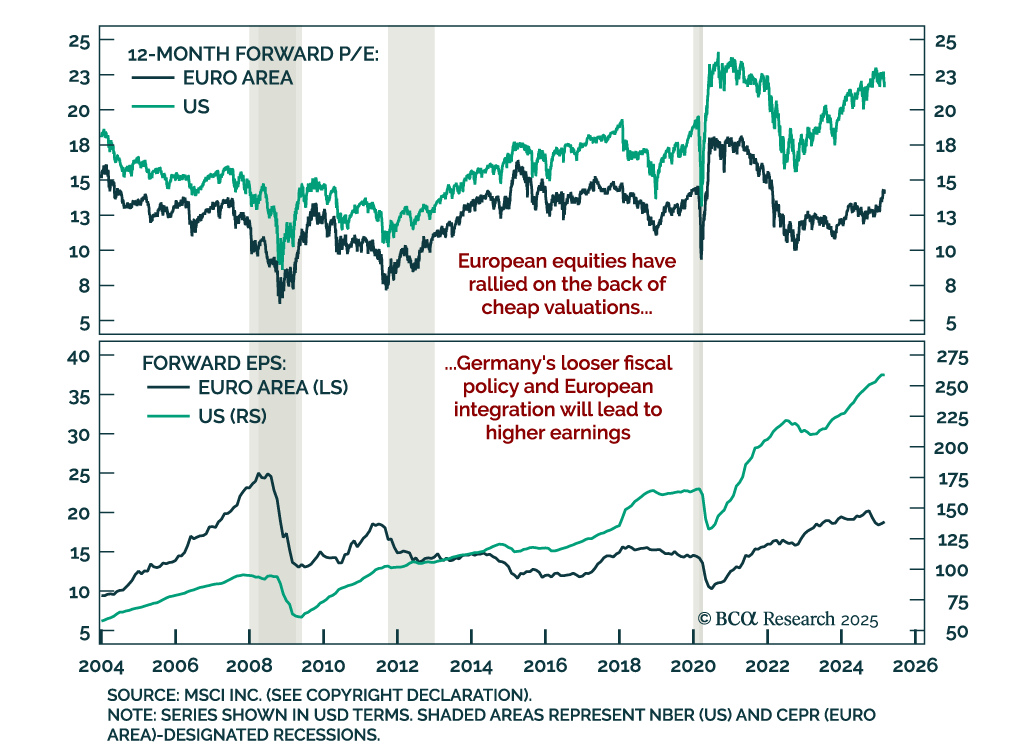

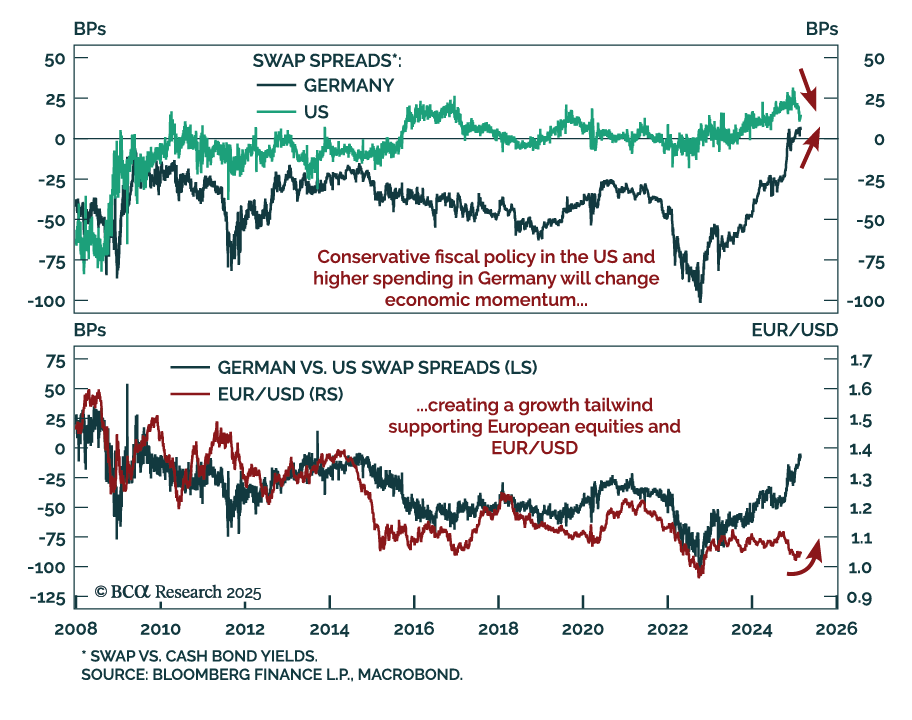

European equities have outperformed the US so far in 2025, especially after Euro Area economic surprises started outperforming as the US is starting to disappoint. The current leadership change between US and European assets reflects extremely one-sided…

The House of Representatives passed a Budget Resolution bill that adds $2.8tn to the deficit by 2034. Our Geopolitical strategists highlighted during our BCA Live & Unfiltered meeting that the Senate is likely to modify it by increasing tax cuts and…

German election results were roughly as expected, but Europe’s biggest economy suddenly just got more interesting. While the details of the governing coalition have yet to be finalized, Chancellor Merz has floated options to ease the “debt brake”, which…

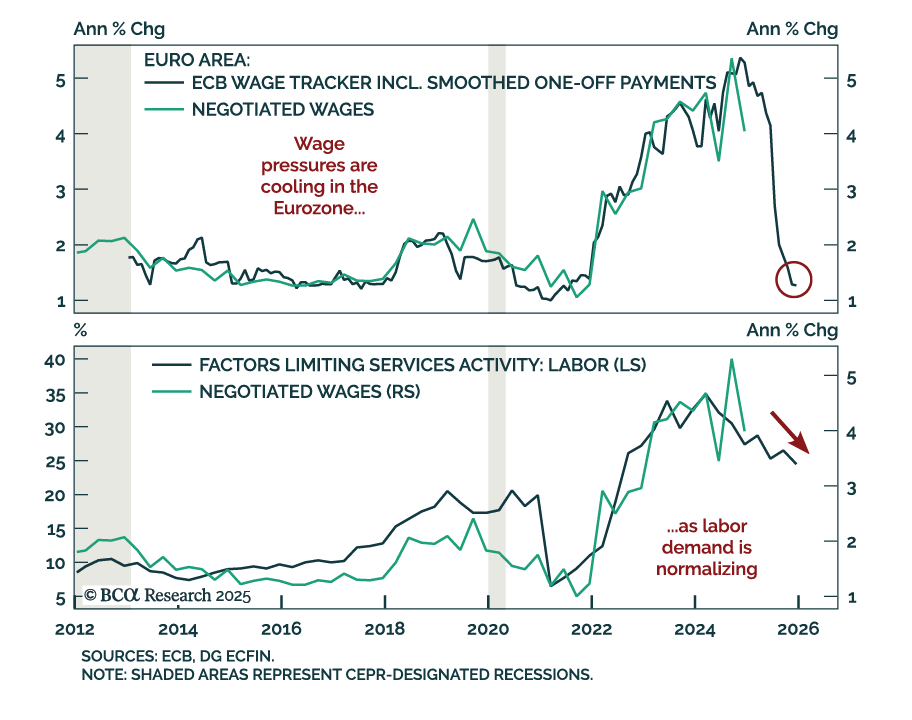

Fourth-quarter European negotiated wages growth cooled to 4.1% y/y, down from the 5.4% peak seen in Q3. The cooling is in line with the ECB’s Wage Tracker showing wage growth decelerating to 1.3% by the end of the year. Labor demand is easing in Europe,…