Financial Markets

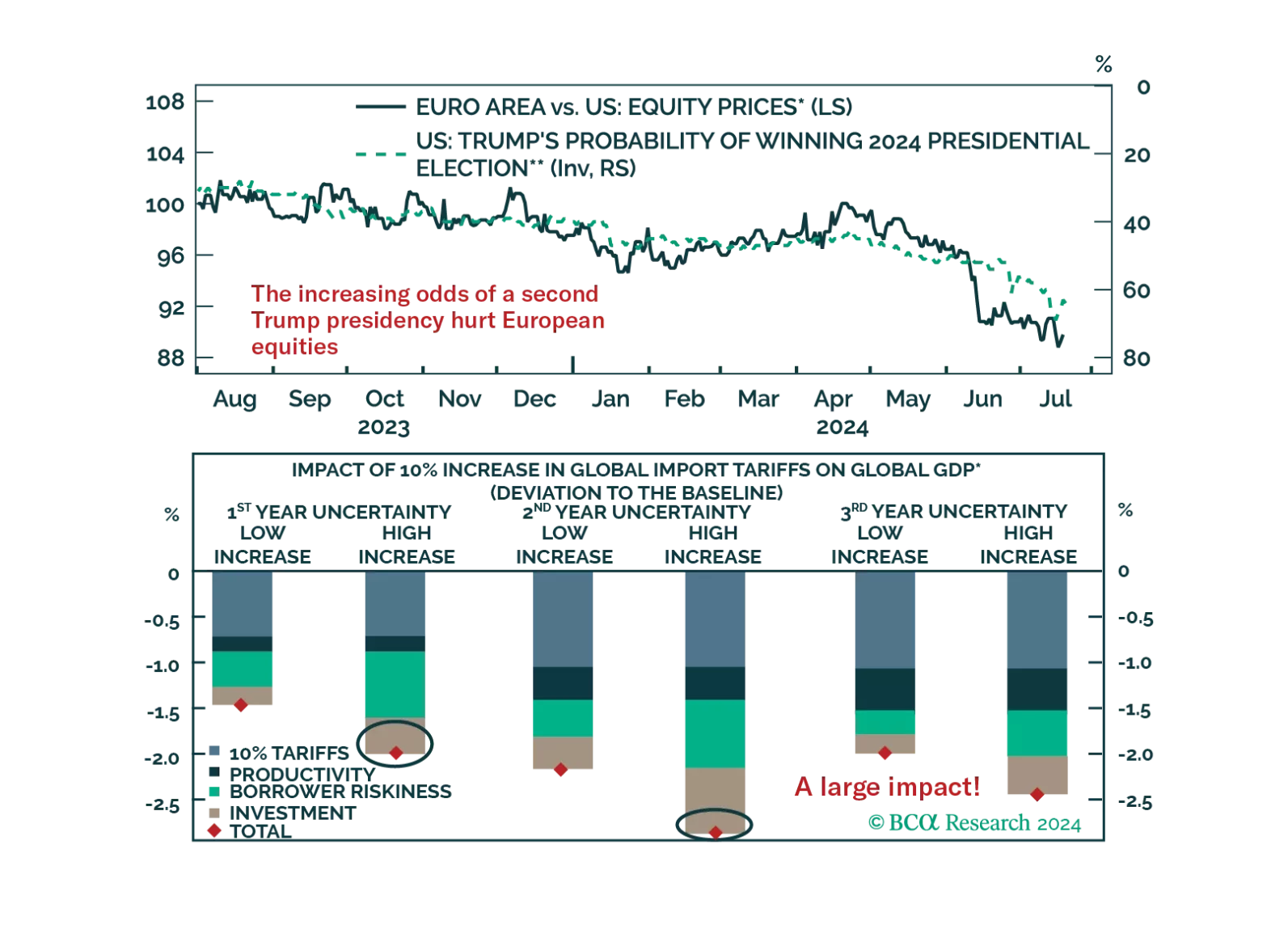

As Trump’s victory odds rise, the underperformance of European equities deepens. How negative would a global trade war be for European assets?

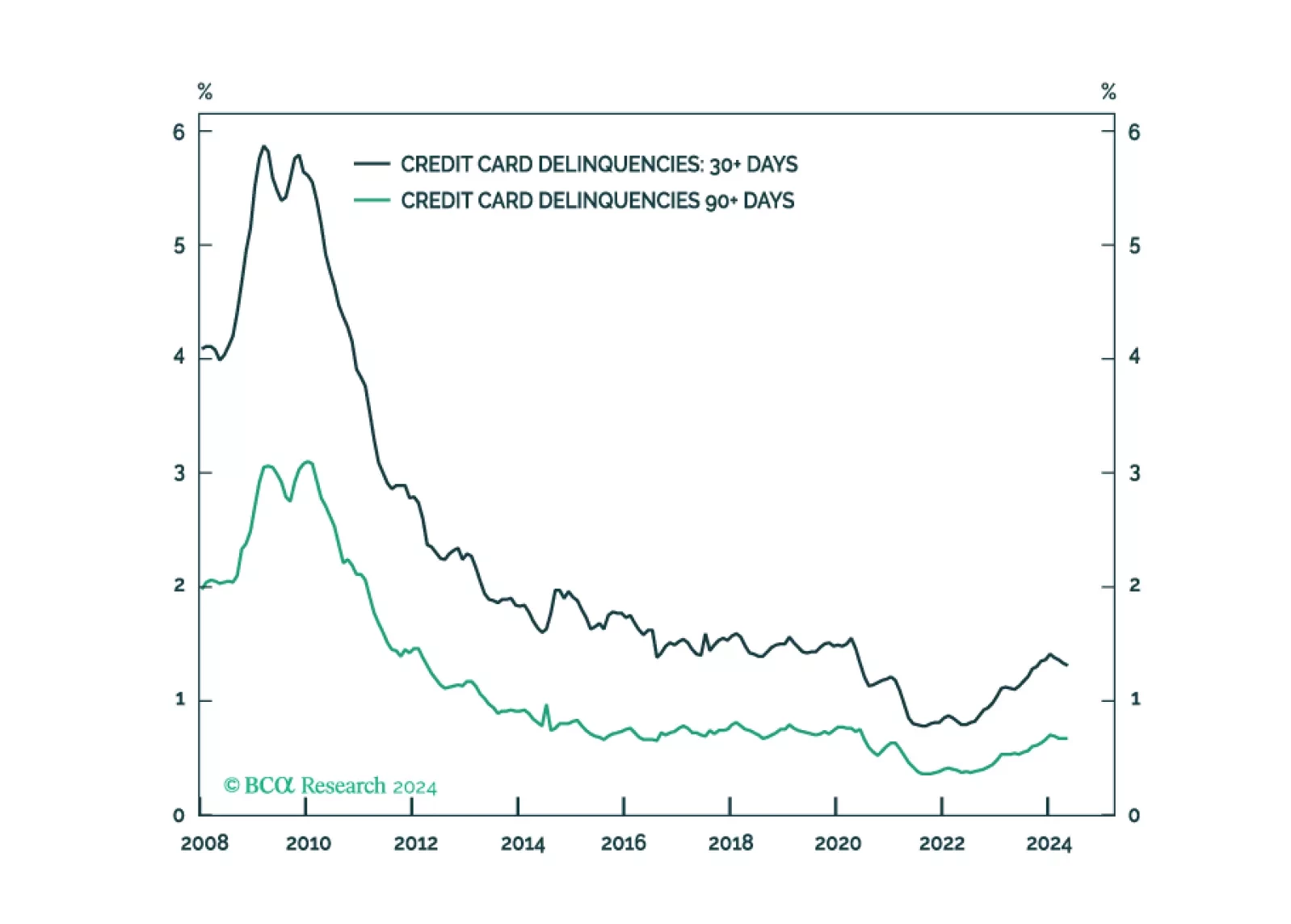

It’s status quo for the SIFI banks, as they don’t see consumer credit performance materially worsening from now-normalized levels and they are not meaningfully exposed to commercial real estate losses.

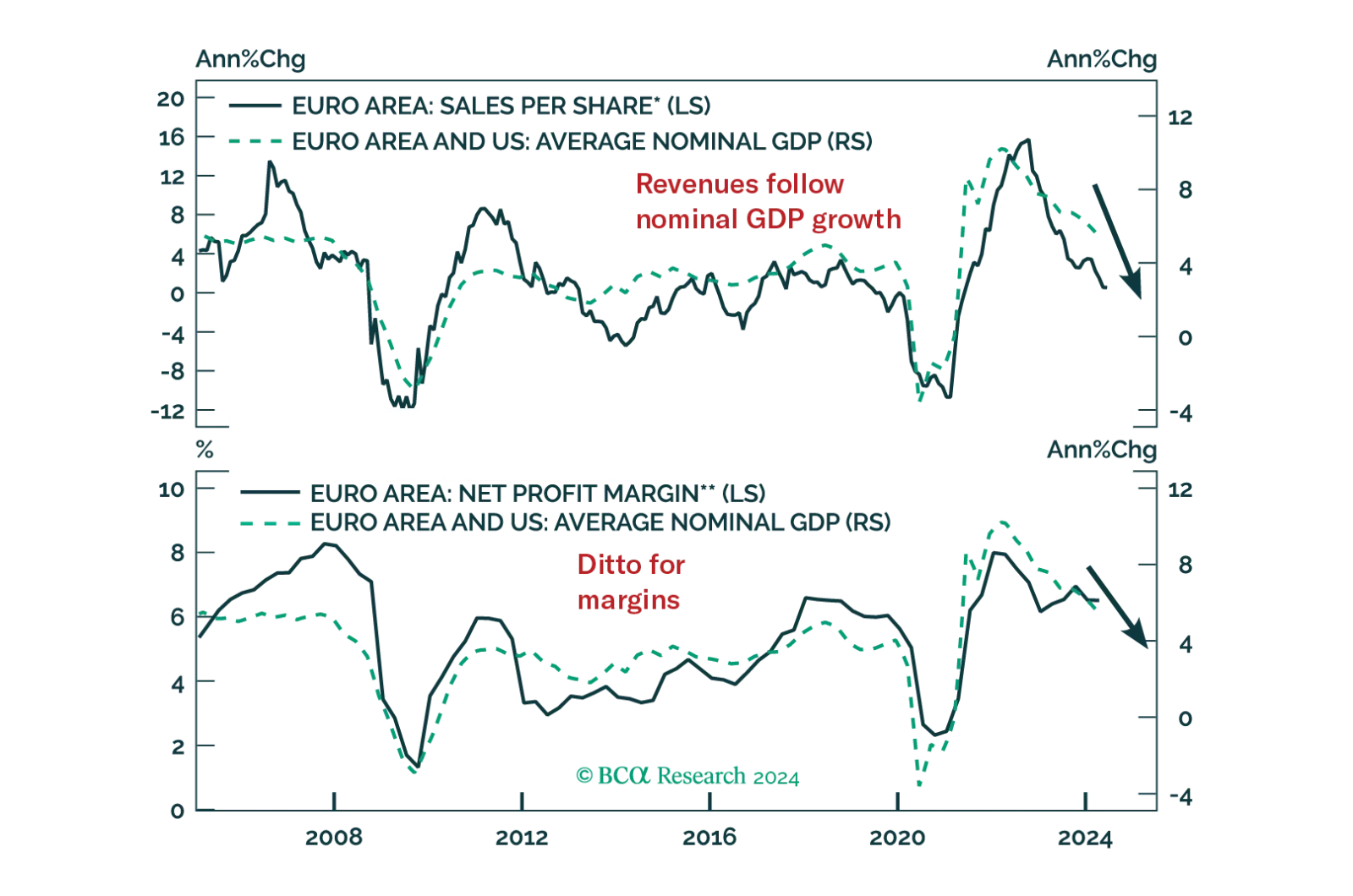

The real threat to European equities is growth, not political risk. How low will Eurozone earnings fall during the coming recession and how much will equities decline in response?

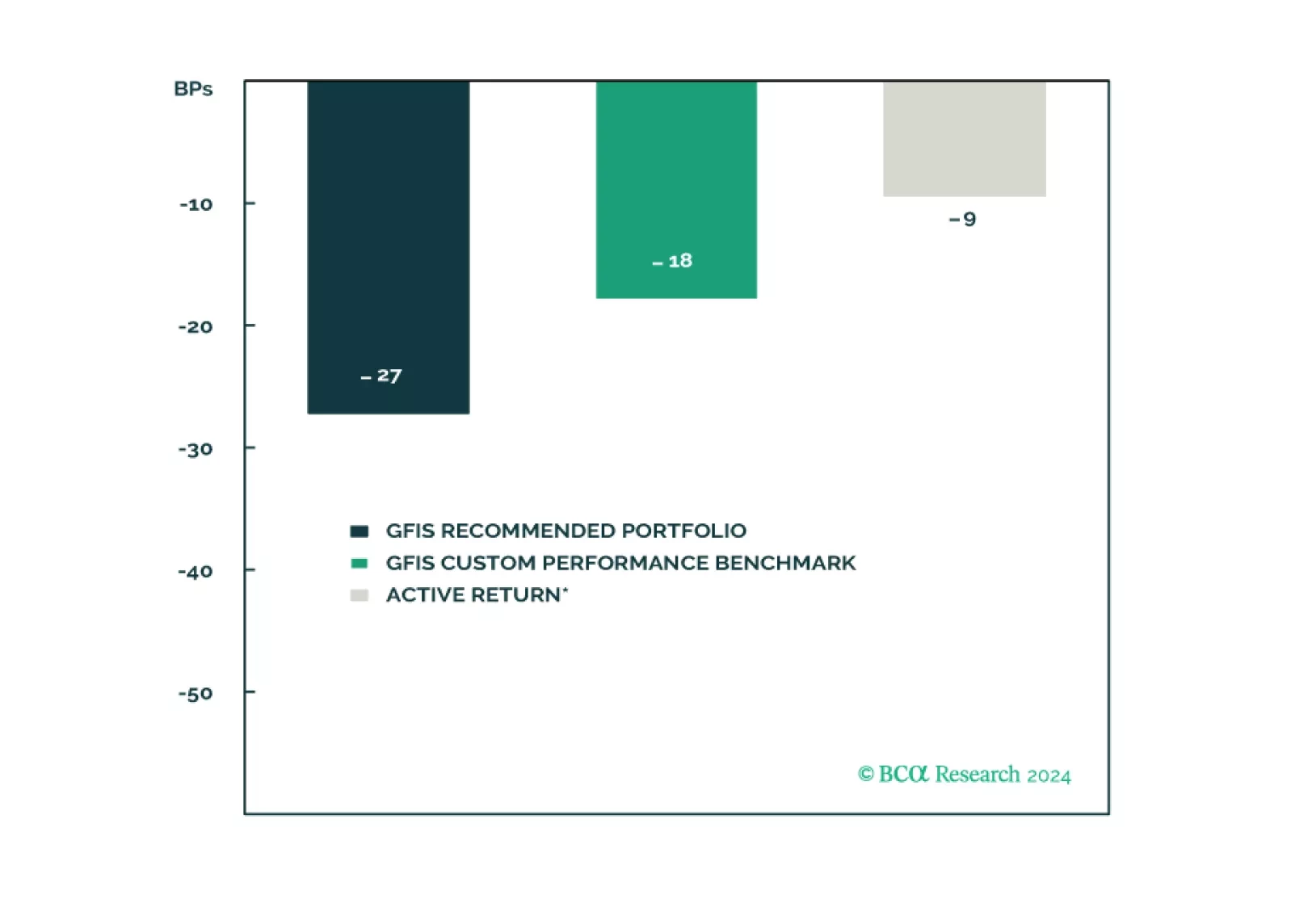

In this report, we present the quarterly review of our Model Bond Portfolio. Rebounding growth and political instability led to slightly negative portfolio performance in Q2/2024. As global growth starts to moderate, we continue to favor government bonds over credit. Maintain a defensive portfolio stance.