Financial Markets

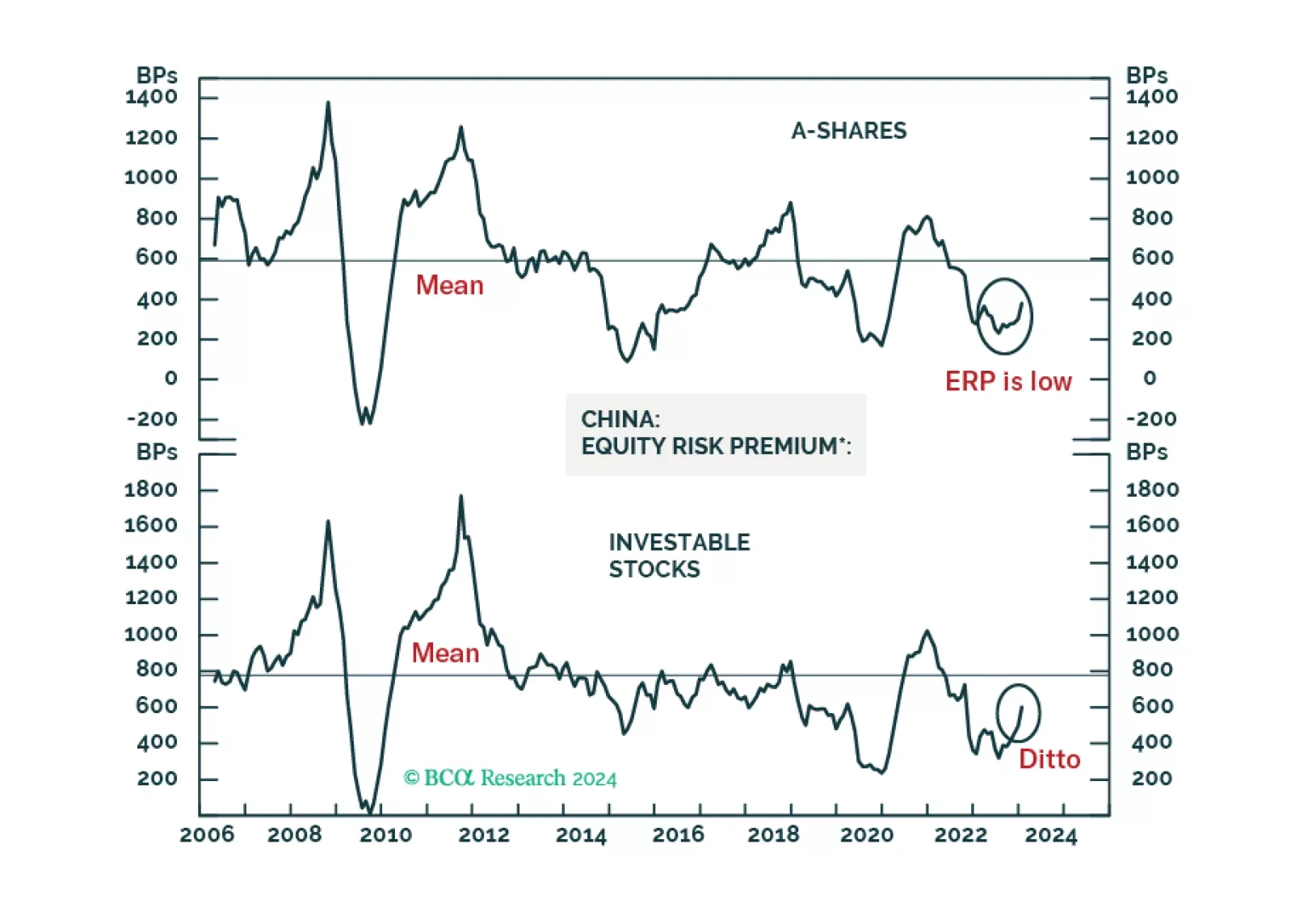

Chinese A-shares will probably begin forming a volatile bottom. The basis is that authorities will likely throw the kitchen sink at the onshore market in an attempt to stabilize share prices. The same is not true for offshore listed stocks. Hong Kong-traded Chinese share prices will likely continue to fall. Beijing is less concerned with offshore stocks as their holders are primarily foreign investors.

The disinflation to date has been benign because it has come almost entirely from improving supply. But the supply-side tailwind has exhausted, so the last mile of the journey to 2 percent inflation will be the hardest, especially in the US and the UK. We discuss the investment implications. Plus, we highlight an interesting sector pair-trade.

We do not believe that NYCB is a canary in the coal mine for a new round of bank distress. The MidCap 400 Regional Bank Index’s subsequent 10% decline looks to us like a juicy opportunity for stockpickers who can separate the wheat from the chaff. Our Special Report is meant to assist them with their initial winnowing.

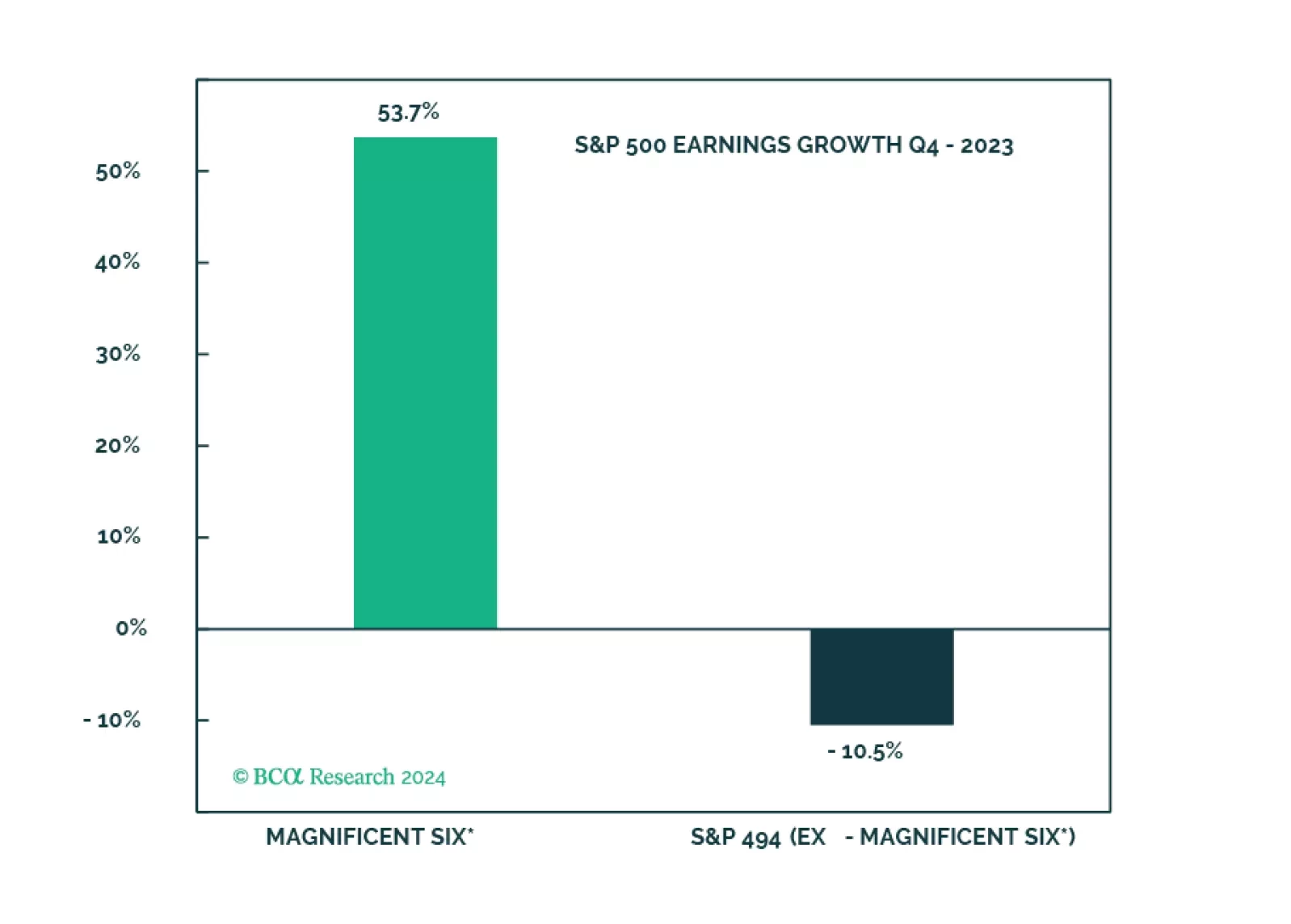

The soft landing and rate cuts narrative is being priced out, and the S&P 500 is overvalued and getting overbought. The Magnificent Seven are about to get a new moniker on the back of performance dispersion. However, without the cohort, S&P 500 earnings would have been even deeper in the red.