Financial Markets

The market’s pricing of a soft landing means that geopolitical risks are becoming more, not less, relevant in 2024. US domestic divisions will invite challenges as foreign powers rightly fear that US policy will turn more hawkish after the election.

Despite the blah opening to the year, we do not think stocks have reached an inflection point. We expect that incoming data will continue to flatter the soft-landing narrative for another couple of months, helping the S&P 500 to establish a new all-time high before the rally runs out of steam.

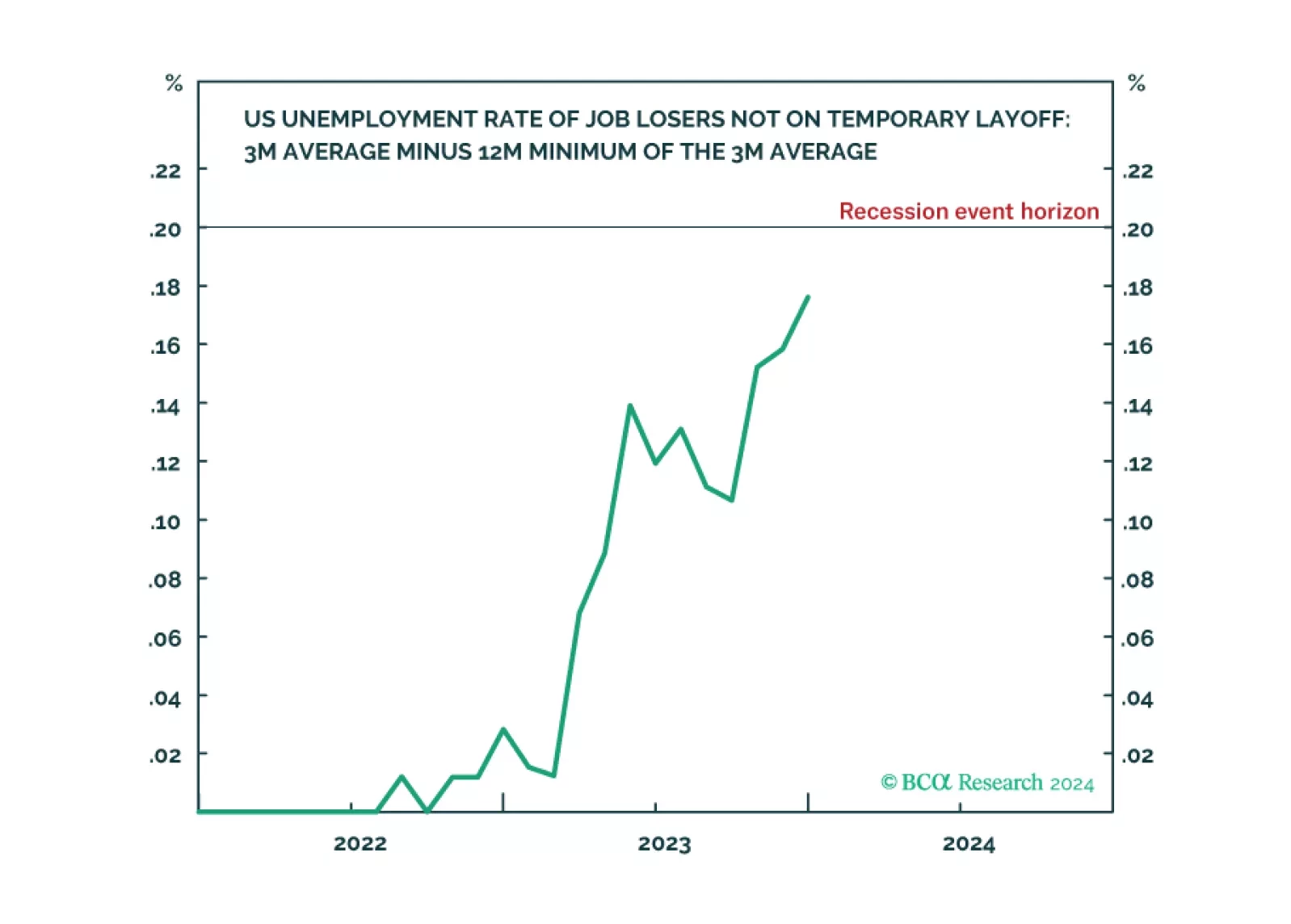

Following today’s US jobs data release, the Joshi rule real-time US recession indicator inched up to 0.18 and is now just a whisker from its recession event-horizon of 0.20.

A soft landing can be achieved but not maintained. We are cutting our tactical recommendation on stocks from overweight to neutral and scaling back our long-duration stance.