Fixed Income

Our Portfolio Allocation Summary for October 2025.

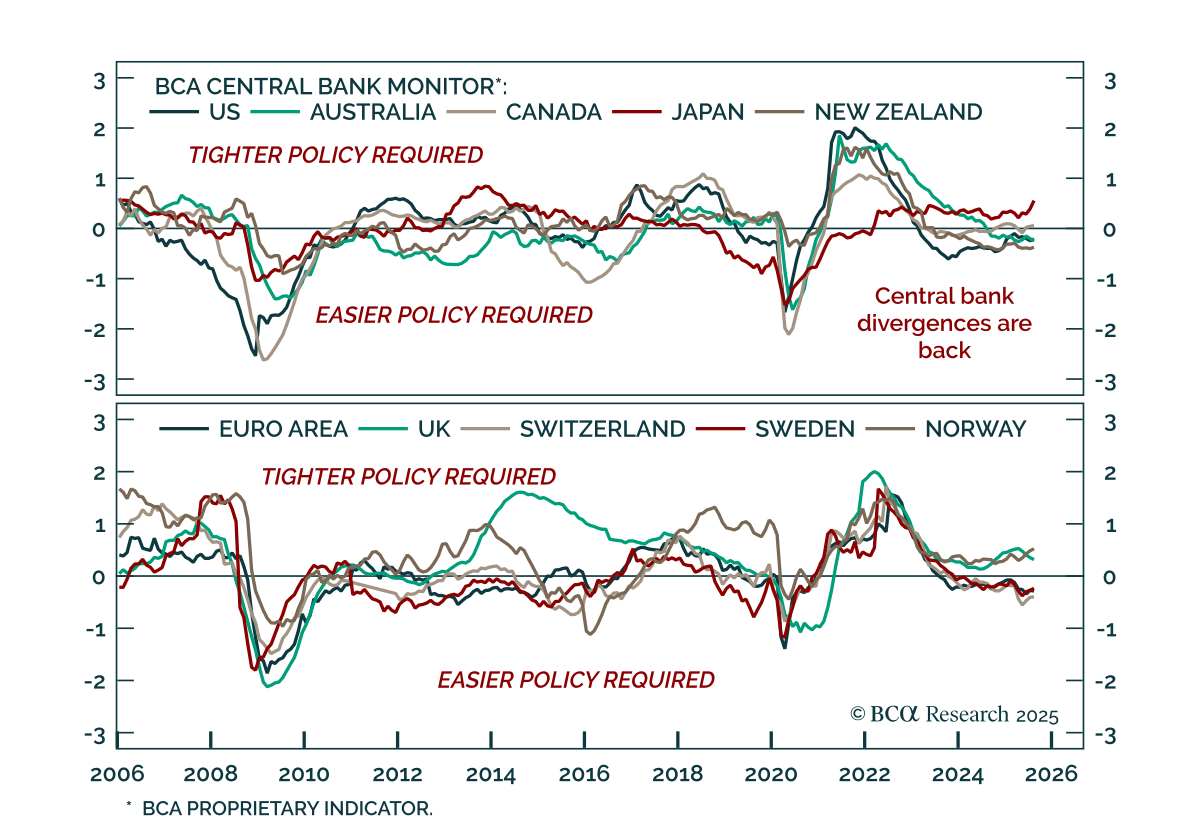

Our DM strategists recommend regional bond overweights in the UK, Canada, and Sweden, and express policy divergence through tactical FX trades: long USD, underweight GBP and SEK, and long JPY vs. EUR. Most G10 central banks are nearing neutral, but their next…

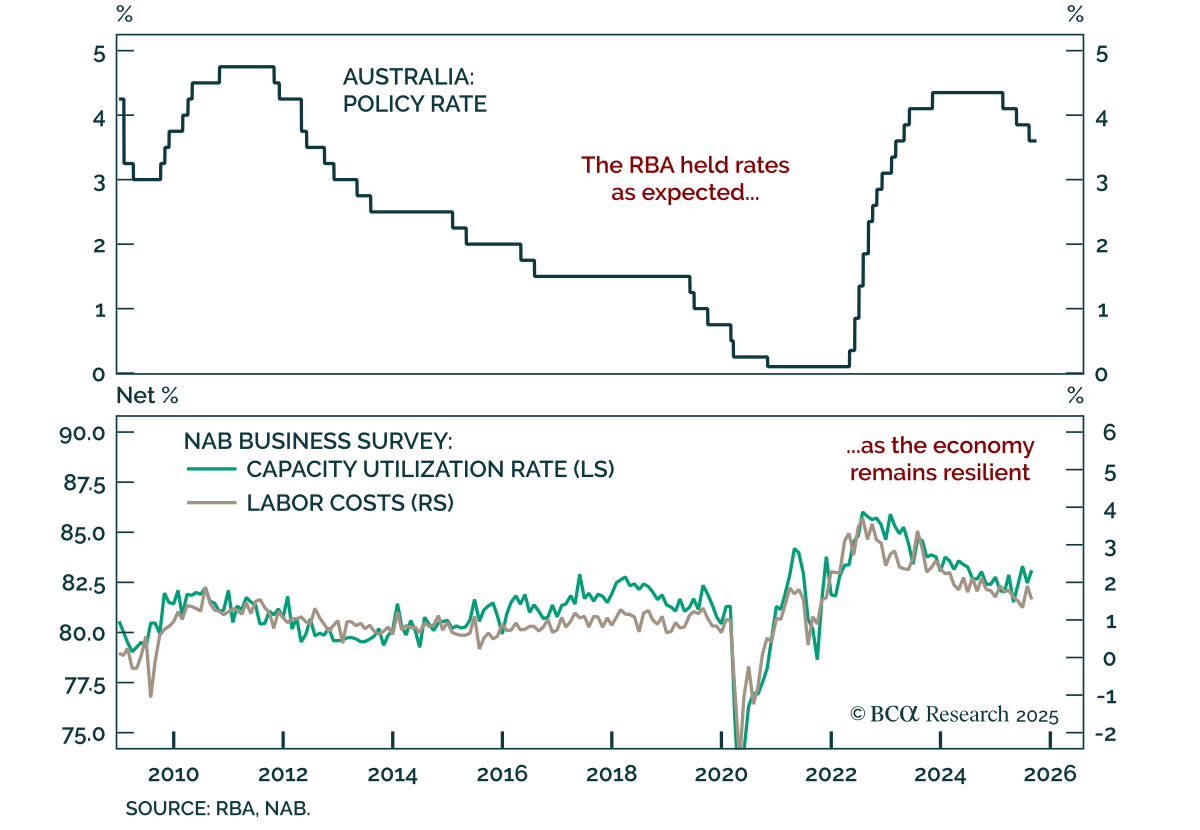

The RBA held rates at 3.6% as expected, maintaining caution as inflation could prove stronger than expected. Policy remains slightly restrictive, and at most one additional cut is on the table as the central bank has achieved a soft landing. While the RBA has…

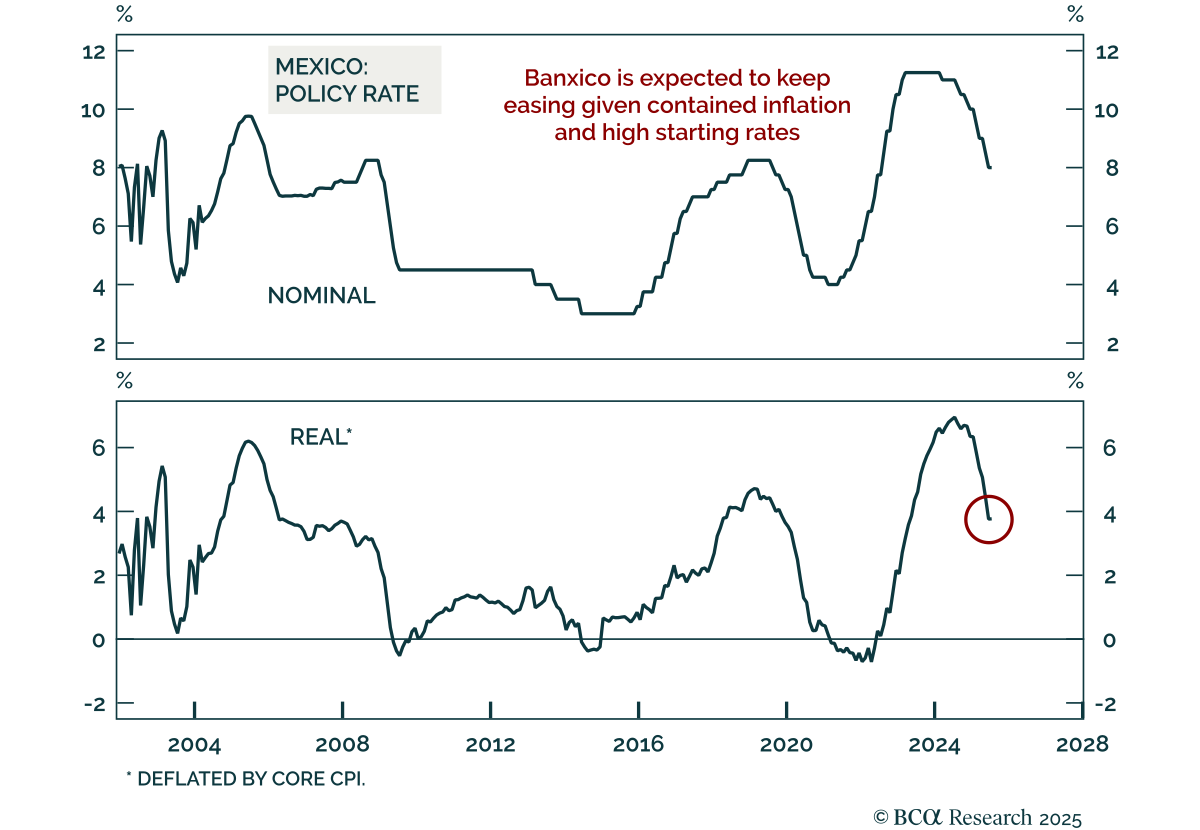

Banxico cut rates to 7.5%, reinforcing our call to go long Mexican local bonds and overweight Mexico across EM portfolios. Inflation is within target, giving policymakers space to ease. Sound fiscal management and strong external accounts continue to support…

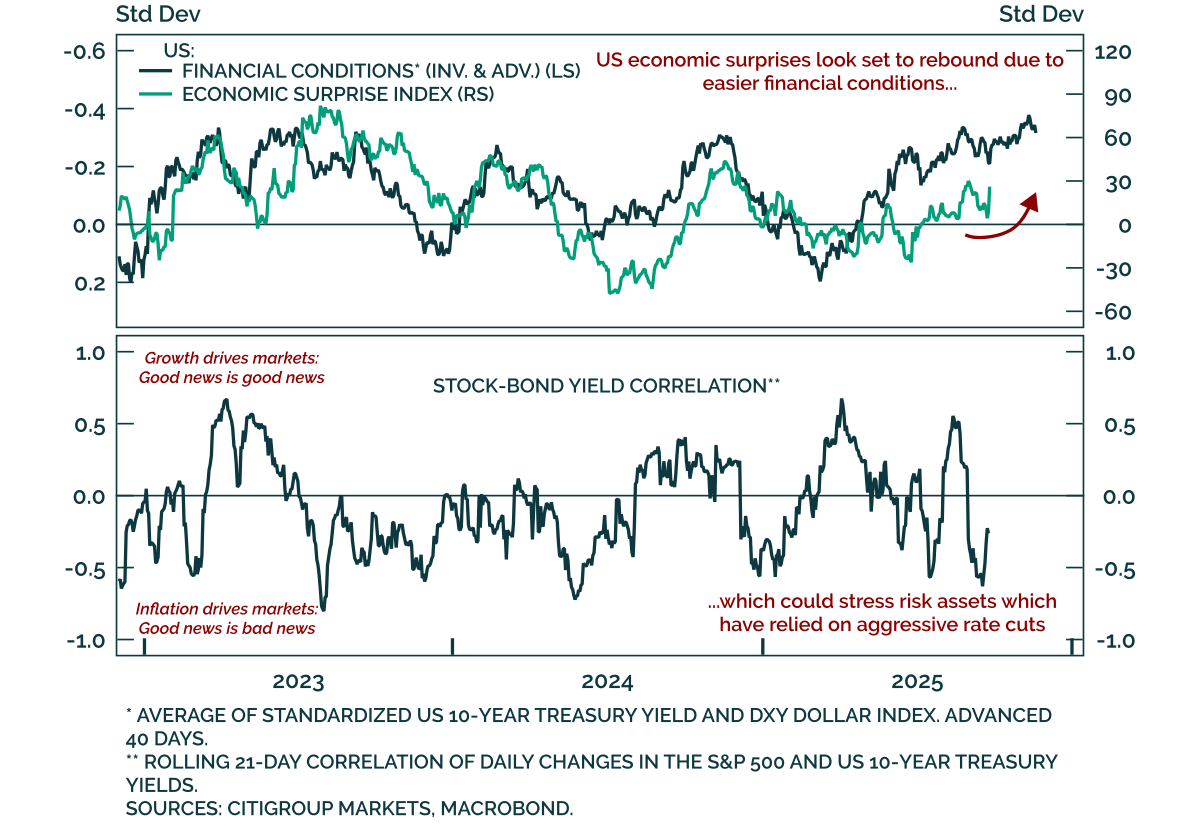

Our tactical framework, which tracks the reflexive loop between financial conditions and economic surprises, points to stronger near-term growth, leaving equities vulnerable if inflation re-accelerates. Data surprises move markets, while bond yields and the…

This week’s US Bond Strategy Special Report takes a look at the two most provocative papers presented at last month’s Jackson Hole conference.

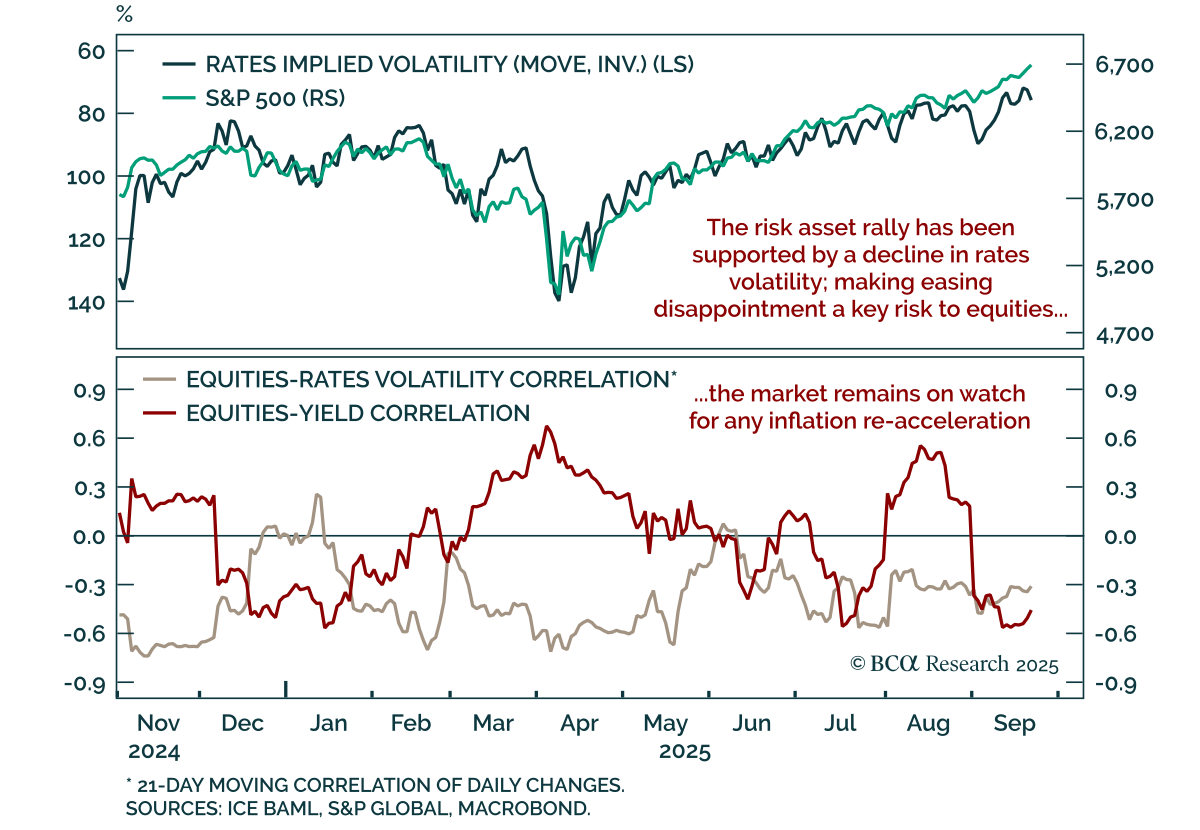

Low rates volatility has been a key tailwind for equities, but the fragile equilibrium leaves markets exposed to AI sentiment and inflation risks. Rates volatility, measured by the MOVE index, has drifted to multi-year lows and sits below its 20th percentile…

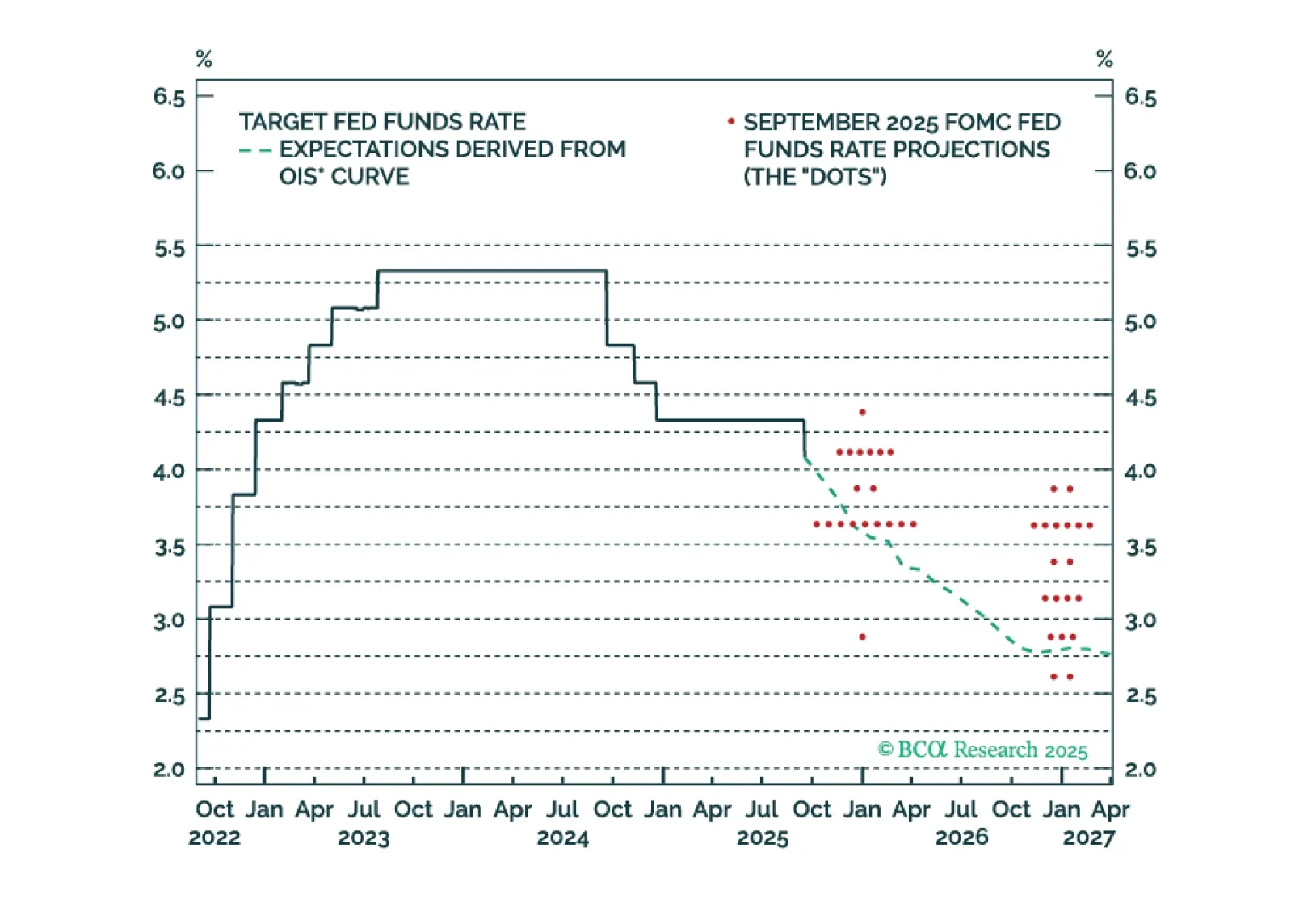

Post-FOMC speeches reveal divisions across the committee, reinforcing long duration as policy remains mildly restrictive. The September dots showed a split, with half of participants expecting at most one 25 bps cut and the rest seeing at least two. Gov.…

The Fed’s actions tell us that it has chosen to avoid a recession at the cost of moving its inflation goalposts to 3 percent. Thus begins the slippery slope to price instability. Long-term investors should underweight the dollar, own some gold, but better than gold is bitcoin. Plus, a new tactical trade is short GOOGL vs. SPY.

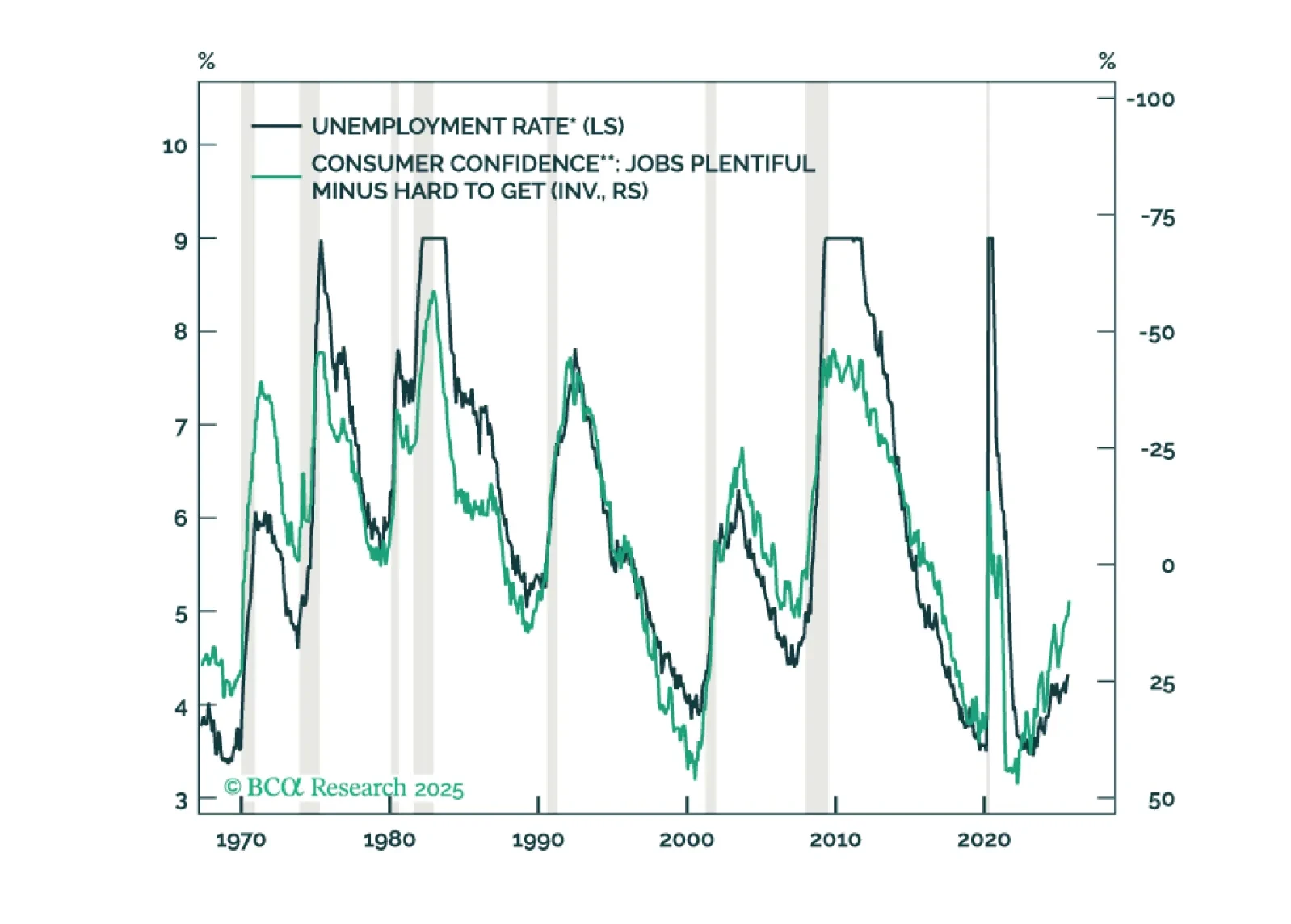

Median Fed unemployment rate projections are overly optimistic. The Fed will end up cutting more in 2026 than it currently anticipates.