Fixed Income

We apply our systematic approach to investing based on economic, inflation, and monetary policy surprises to the major global bond markets. The economic regimes defined by the current macro-surprises setup confirm our existing fixed-income portfolio tactical recommendations.

This year’s corporate bond sell off has hit high-yield more than investment grade, and high-yield spreads have turned relatively more attractive as a result.

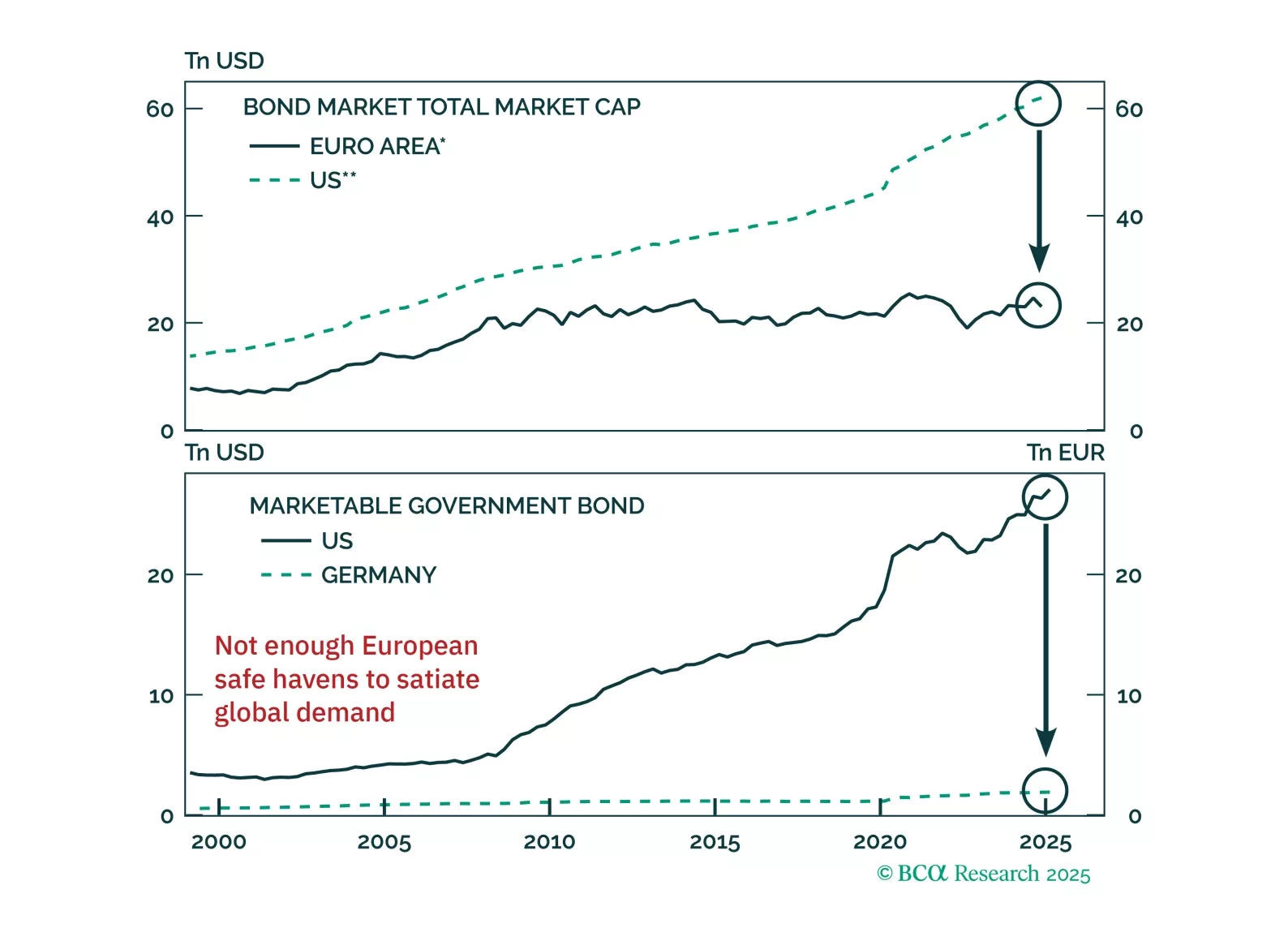

Are bunds the new Treasurys? The euro and German debt are gaining favor as safe havens, but markets may be overplaying the shift. Our latest report dissects what's durable, what's not, and how to trade the dislocation.

US Treasuries typically outperform both equities and global government bonds during downturns. Recent political shifts could lessen that outperformance this cycle, but we doubt it will disappear completely.

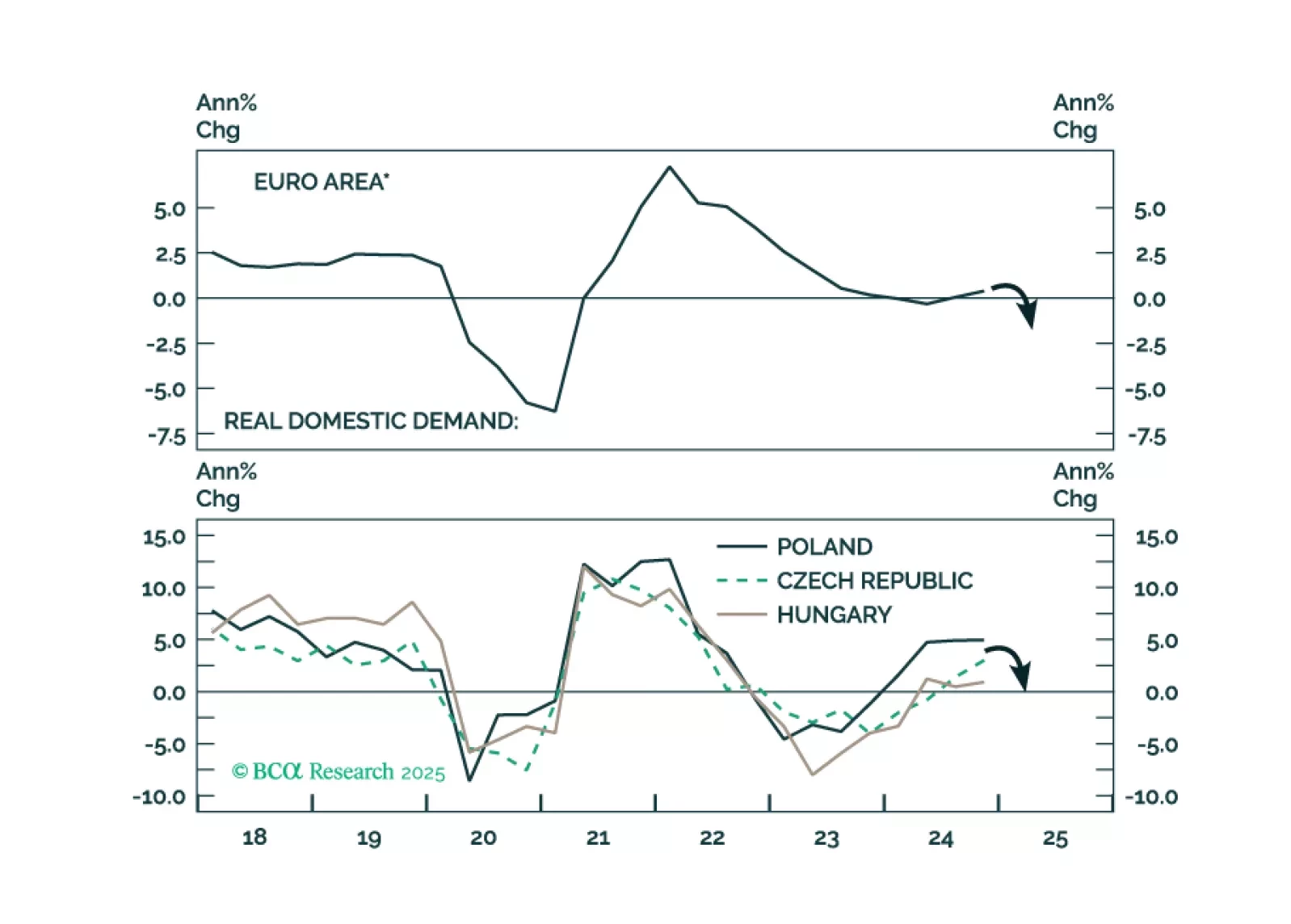

The European economies are facing a major deflationary shock. We recommend that investors stay long a basket of Central European (CE3) domestic bonds. They should also upgrade CE3 bonds and stocks in their respective EM portfolios.

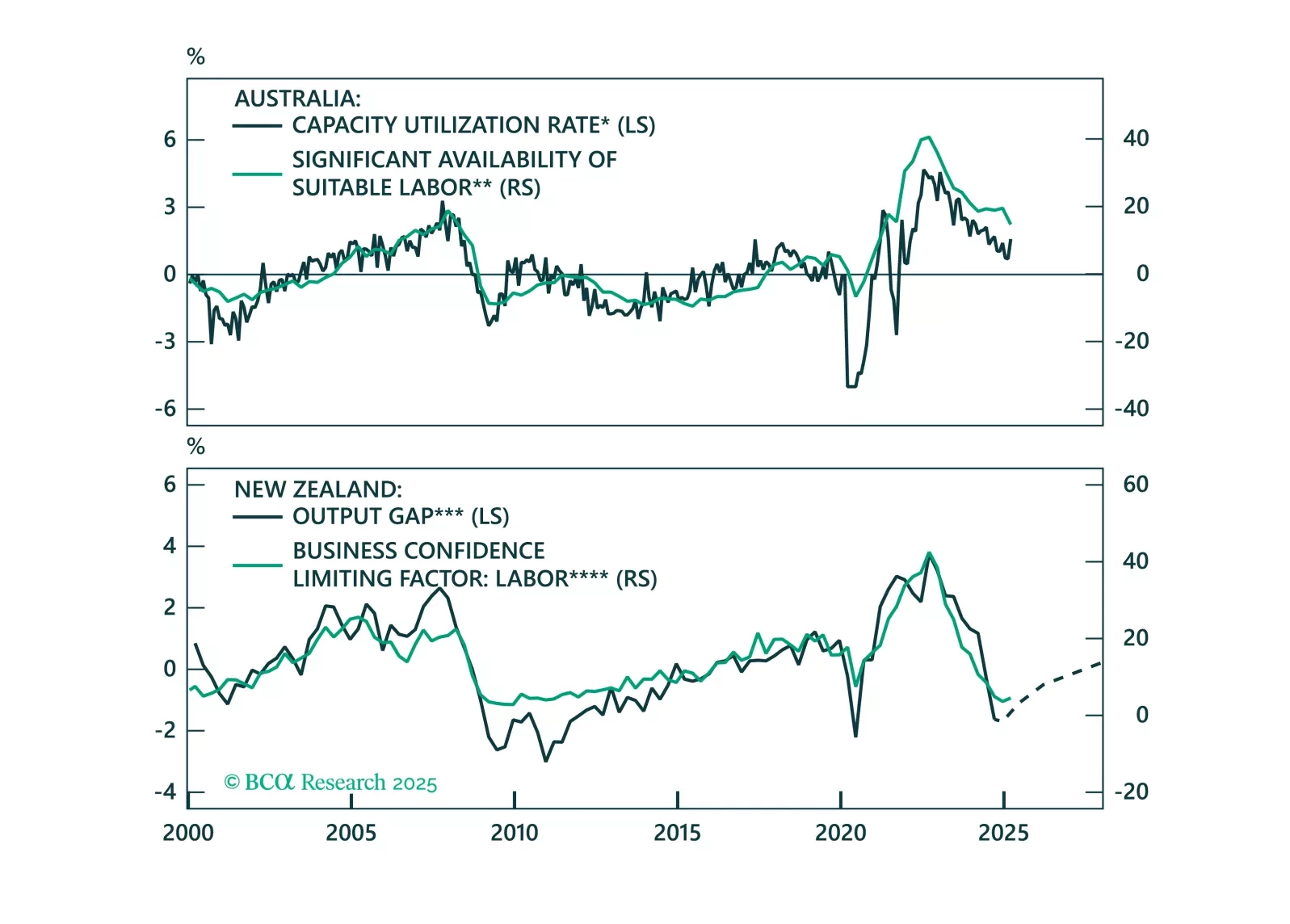

Following the escalation of the US-China trade war, the Reserve Bank of Australia is priced to cut rates most aggressively among its G10 peers. Across the Tasman Sea, the Reserve Bank of New Zealand has already cut rates aggressively, but the economy has yet to respond to this policy easing. This Special Report will examine the prospects of monetary policy for both of these central banks.

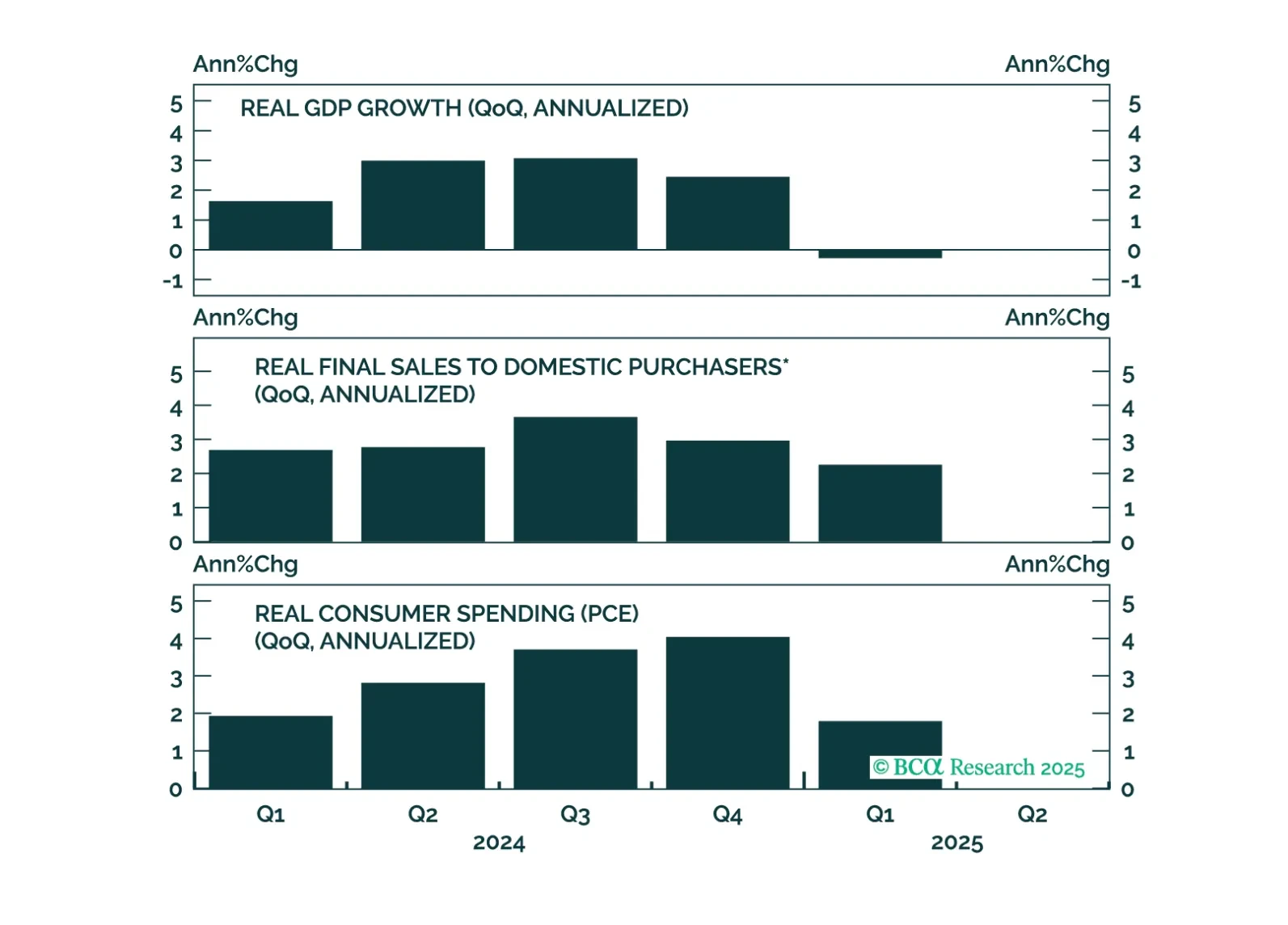

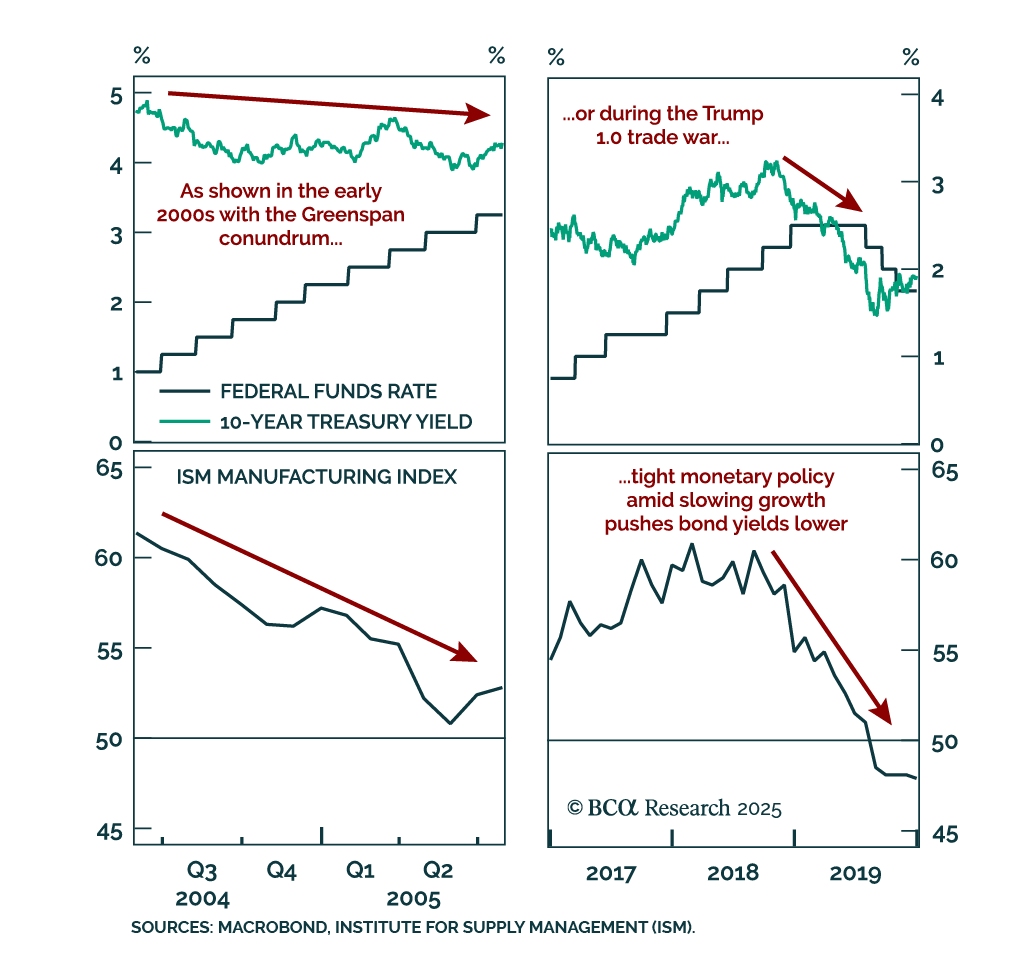

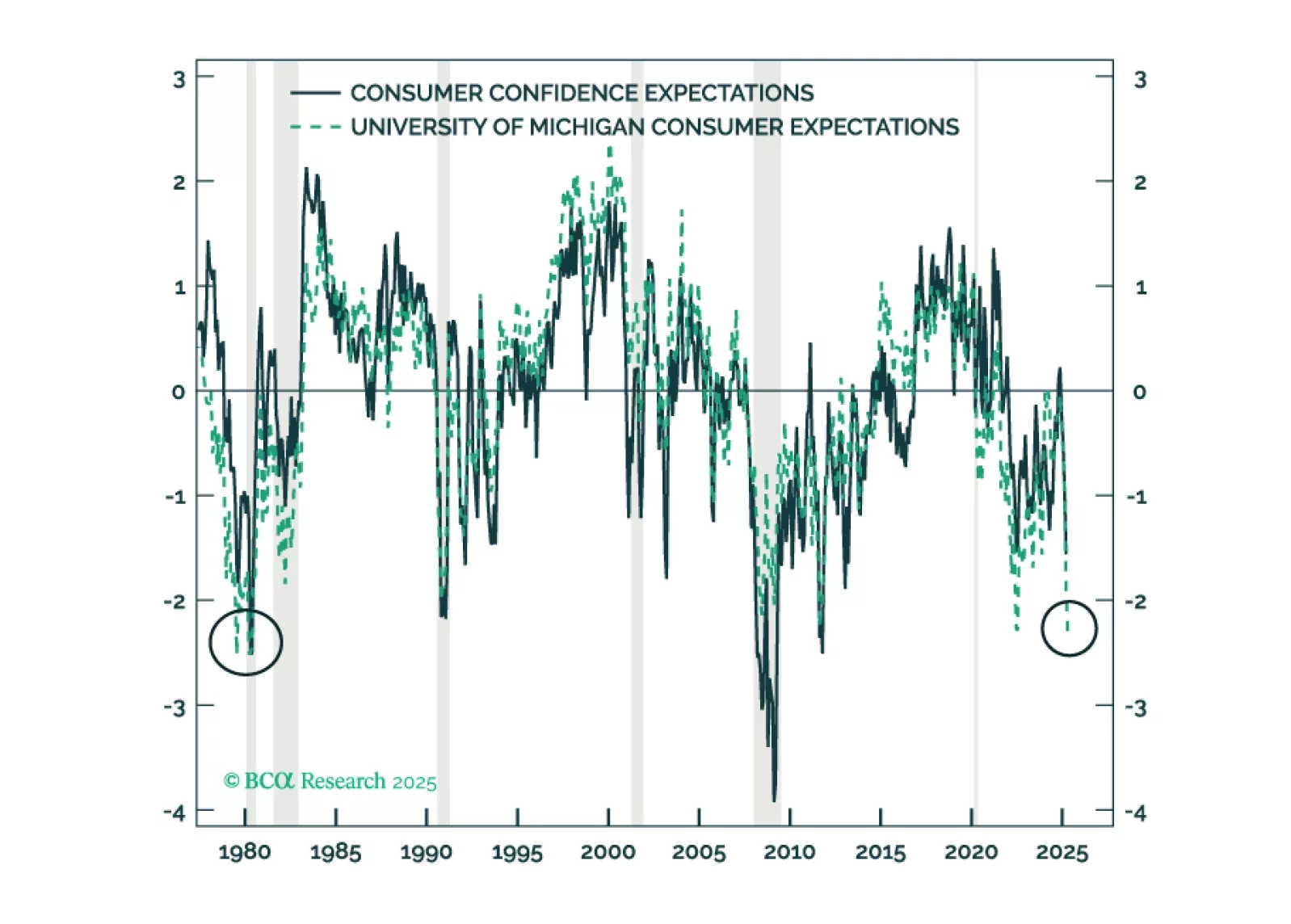

The policy-induced decline in consumer confidence has spread to businesses and investors, increasing the probability of a recession even if the administration reverses field on its aggressive tariff measures. We reiterate our defensive asset allocation recommendations.