Geopolitics

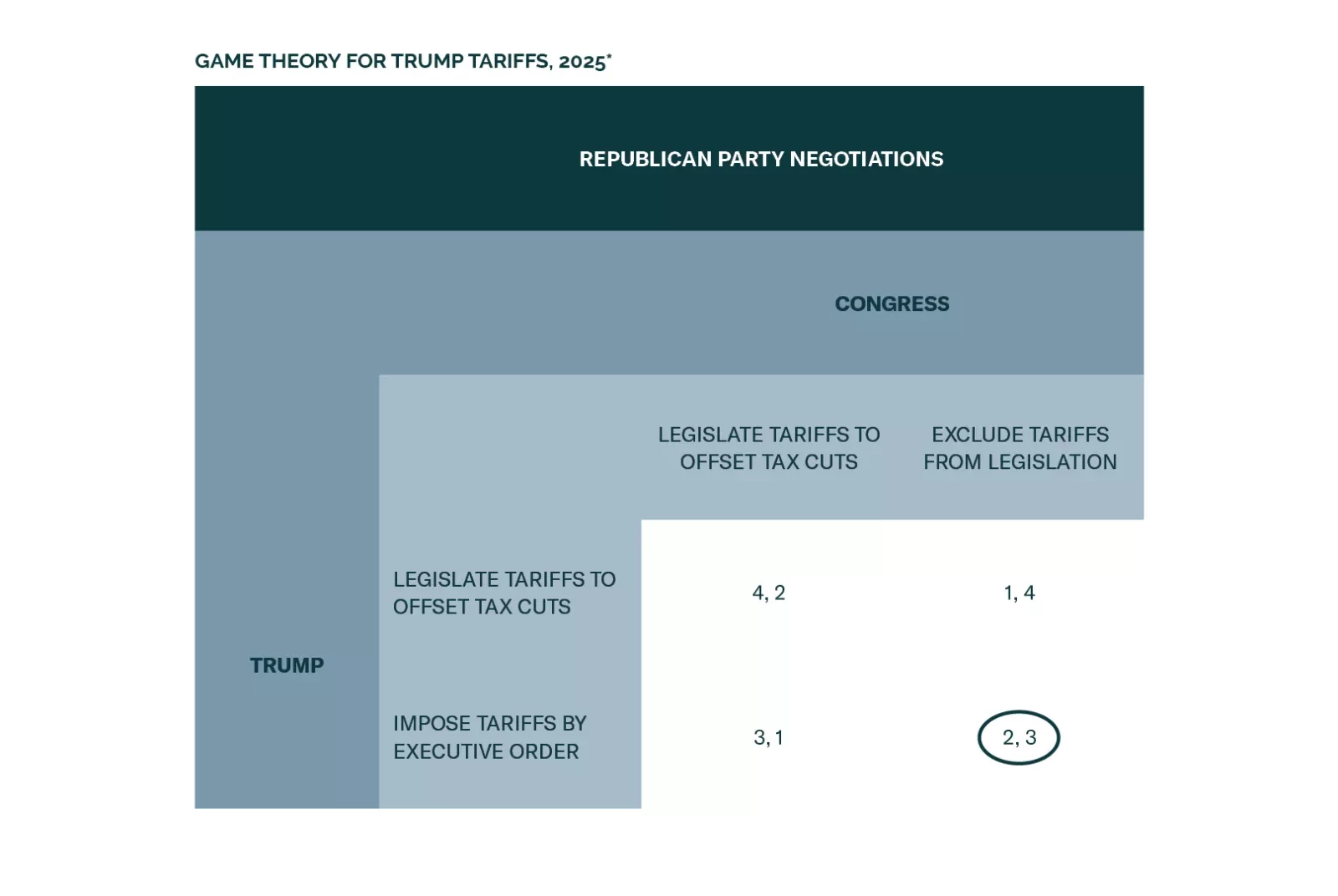

Simple games allow us to model several of the Trump administration’s most disruptive policies in 2025. We find that markets face an increase in volatility as Congress expands the budget, Trump implements tariffs on the world, China retaliates, and Taiwan tensions persist. A ceasefire in Ukraine is a marginally positive outcome for Europe, although it is not a long-term peace treaty.

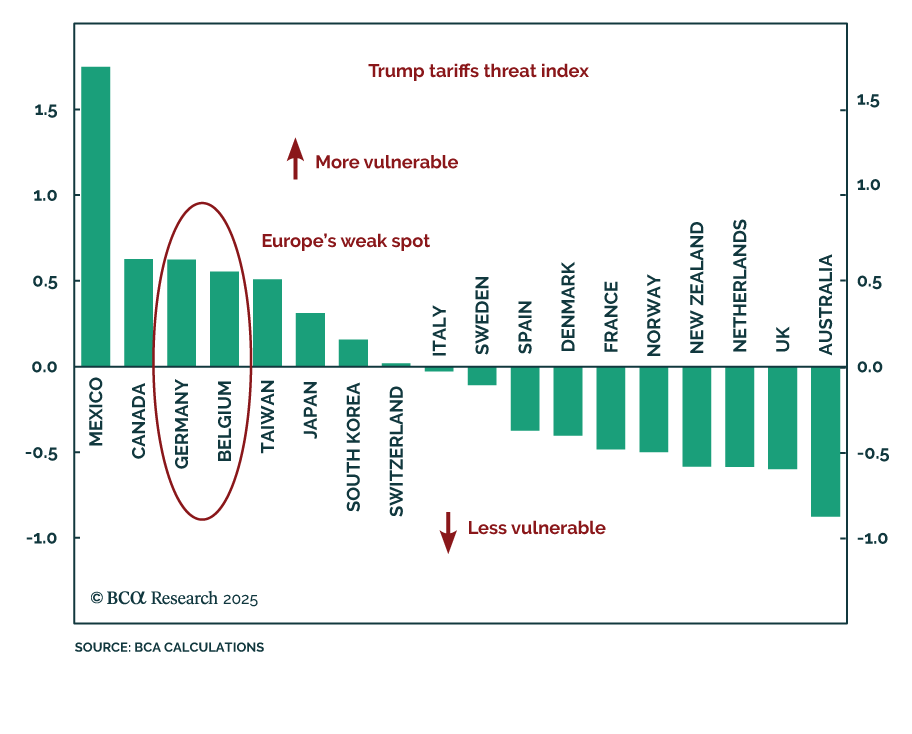

Our Chart Of The Week comes from Mathieu Savary, Chief Strategist of our European Investment Strategy service. Mathieu investigates why President Trump started his global trade offensive with an attack on Canada and Mexico, the US’ two closest…

Our Emerging Markets strategists put together a hypothetical conversation between President Trump and Treasury Secretary nominee Scott Bessent on what economic policy would look like for the Trump 2.0 administration. Secretary Bessent is expected…

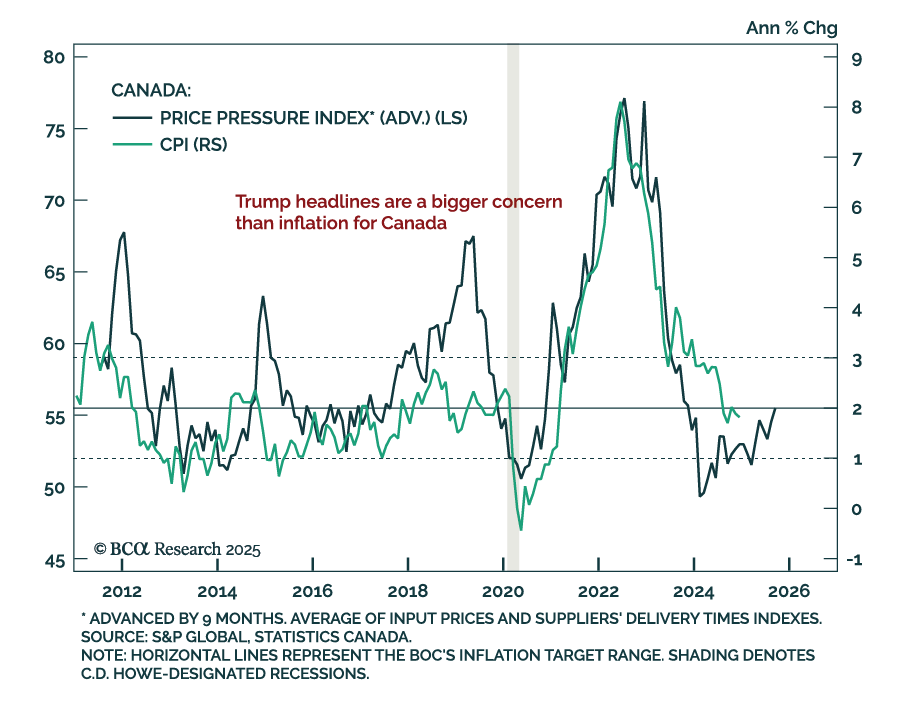

The December Canadian CPI was roughly in line with estimates, with headline inflation ticking down to 1.8% y/y from 1.9% in November. The BoC’s core inflation measures, median and trim, also decreased from 2.6% to 2.4% and 2.5%,…

The January ZEW index for Germany missed estimates, with expectations falling to 10.3 from 15.7 in December. However, the euro area level index ticked up to 18 from 17 a month prior. Measures of current conditions also rose. The lack of momentum for…

President Trump’s inaugural speech outlined his second term agenda. The theme was that the US will become “far more exceptional” than it already is. Trump pledged to reverse America’s decline, rebalance the justice system, streamline government, protect…

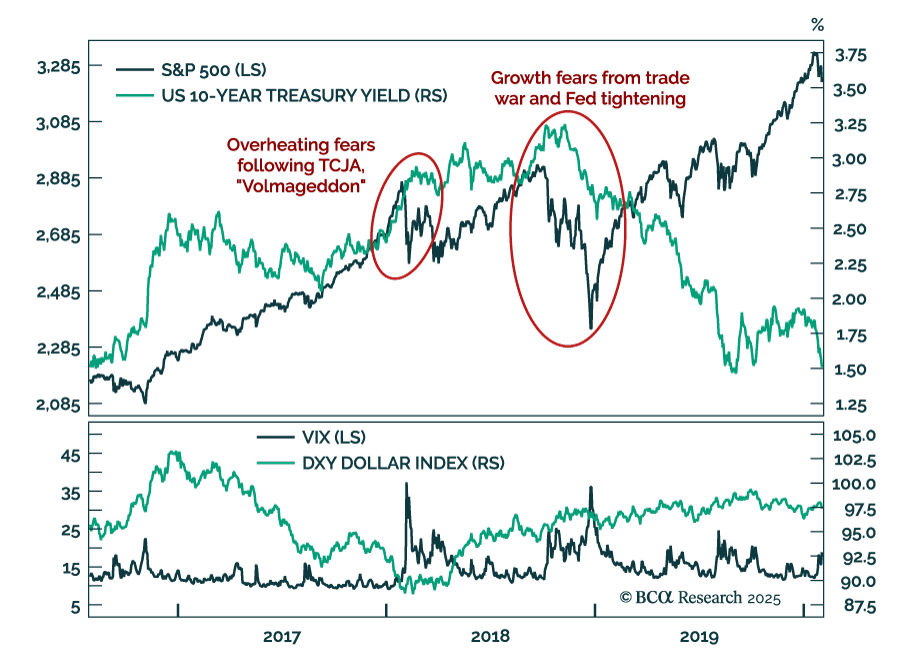

We look at President Trump’s first mandate for lessons on how markets would likely react to different policies. On the fiscal front, the 2017 Tax Cuts and Jobs Act (TCJA) was the first pro-cyclical stimulus in decades. Markets pushed back, as the early 2018…

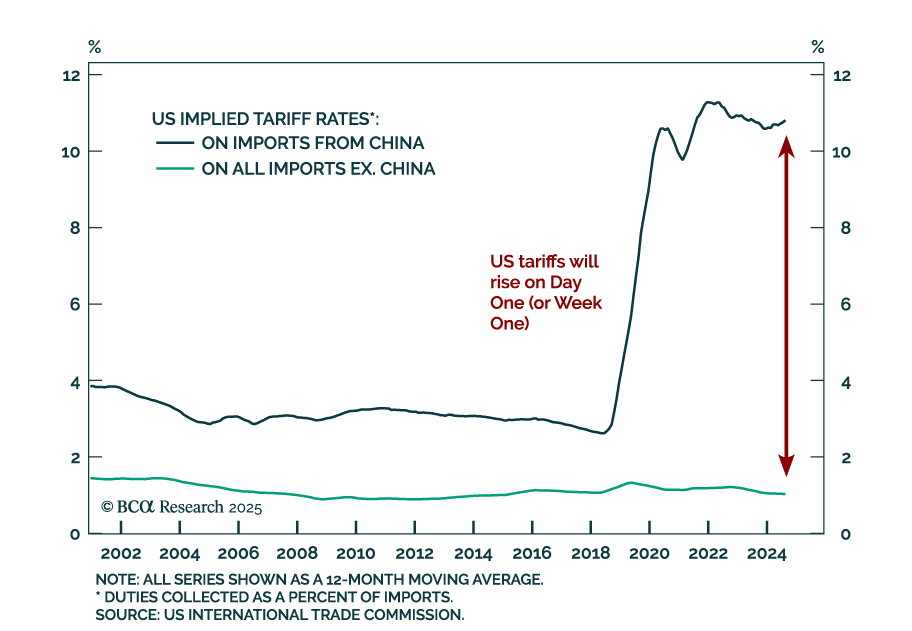

Our US Political strategists published a Special Report on the trade and fiscal policies likely to be implemented on Day One as the Trump administration takes over Washington. Trump is likely to implement significant tariffs early in his term,…

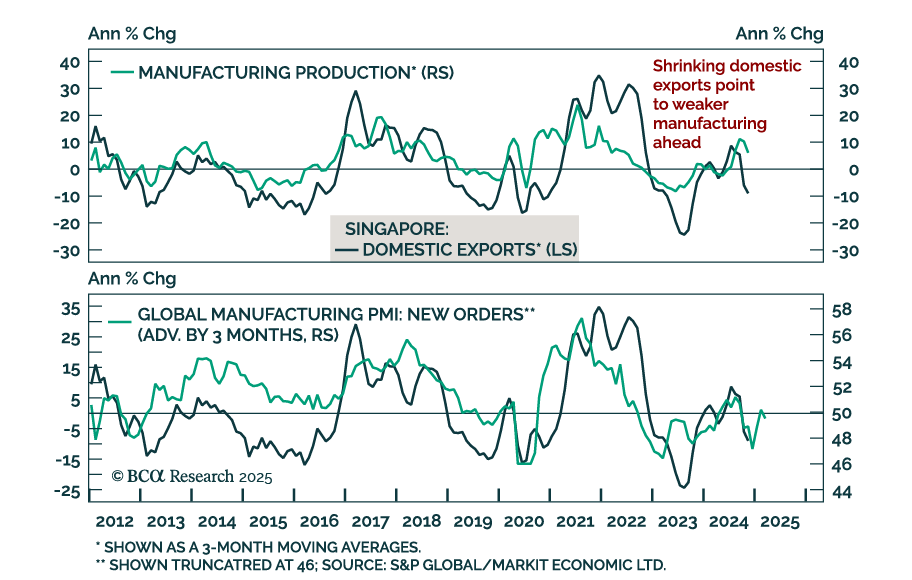

Our Emerging Markets strategists just published a report on Singapore stocks after a significant rally over the past year. Singapore’s manufacturing sector faces headwinds from contracting global new orders, which signals that a recovery in exports is…

Please join us for a BCA Expert Webcast, Thursday, January 16 at 10:00 AM EDT, with Brendan Kelly, former Director for China Economics on the US National Security Council, veteran of the New York Federal Reserve, Treasury Department, Defense Department, and life member of the Council on Foreign Relations.