Global

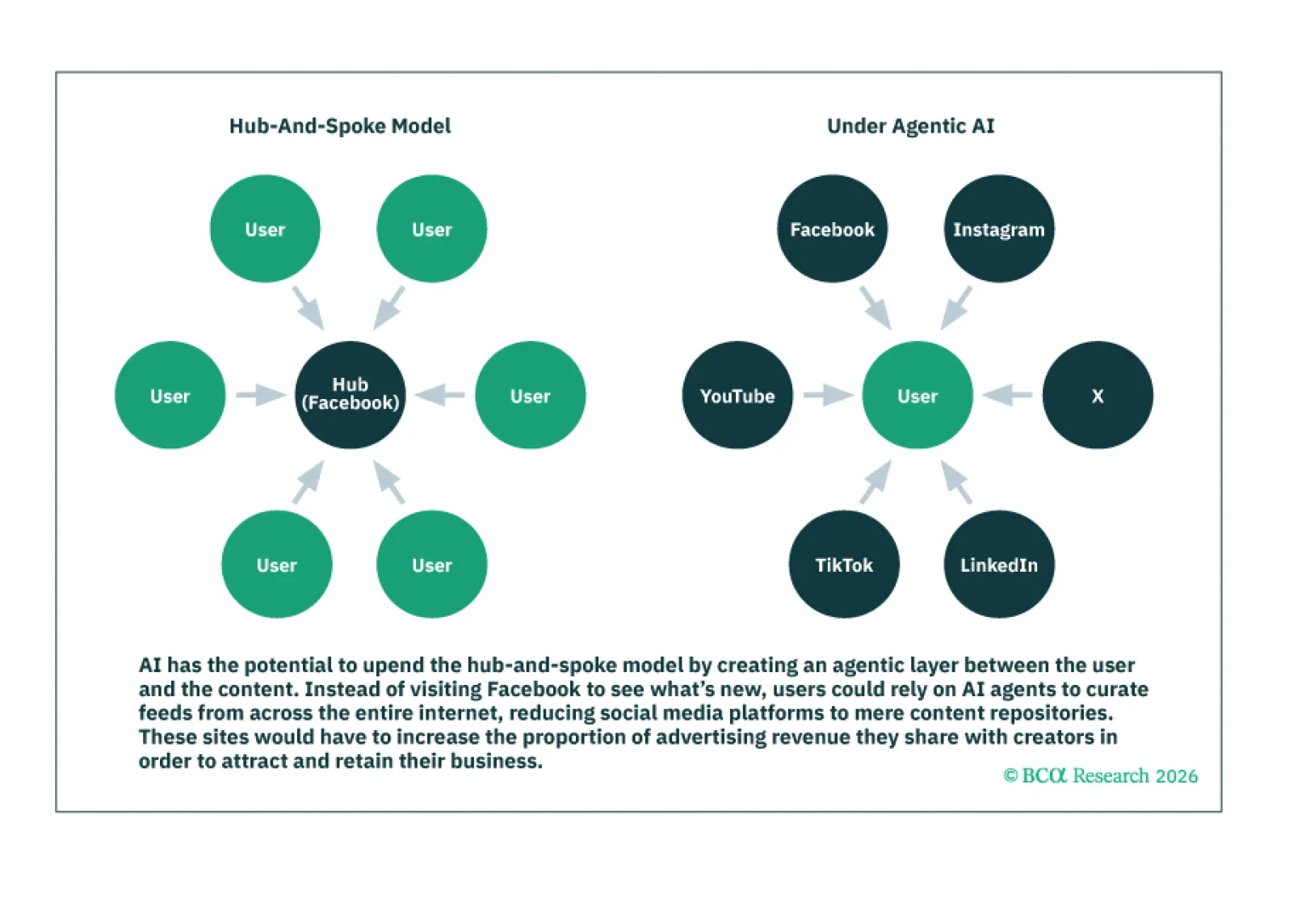

The magnitude of US tech/AI capital spending already rivals past bubble thresholds, threatening hyperscalers’ future returns on capital. There are echoes of previous market tops. Our preferred overlay strategy for equity portfolios remains long semiconductor producers / short hyperscalers.

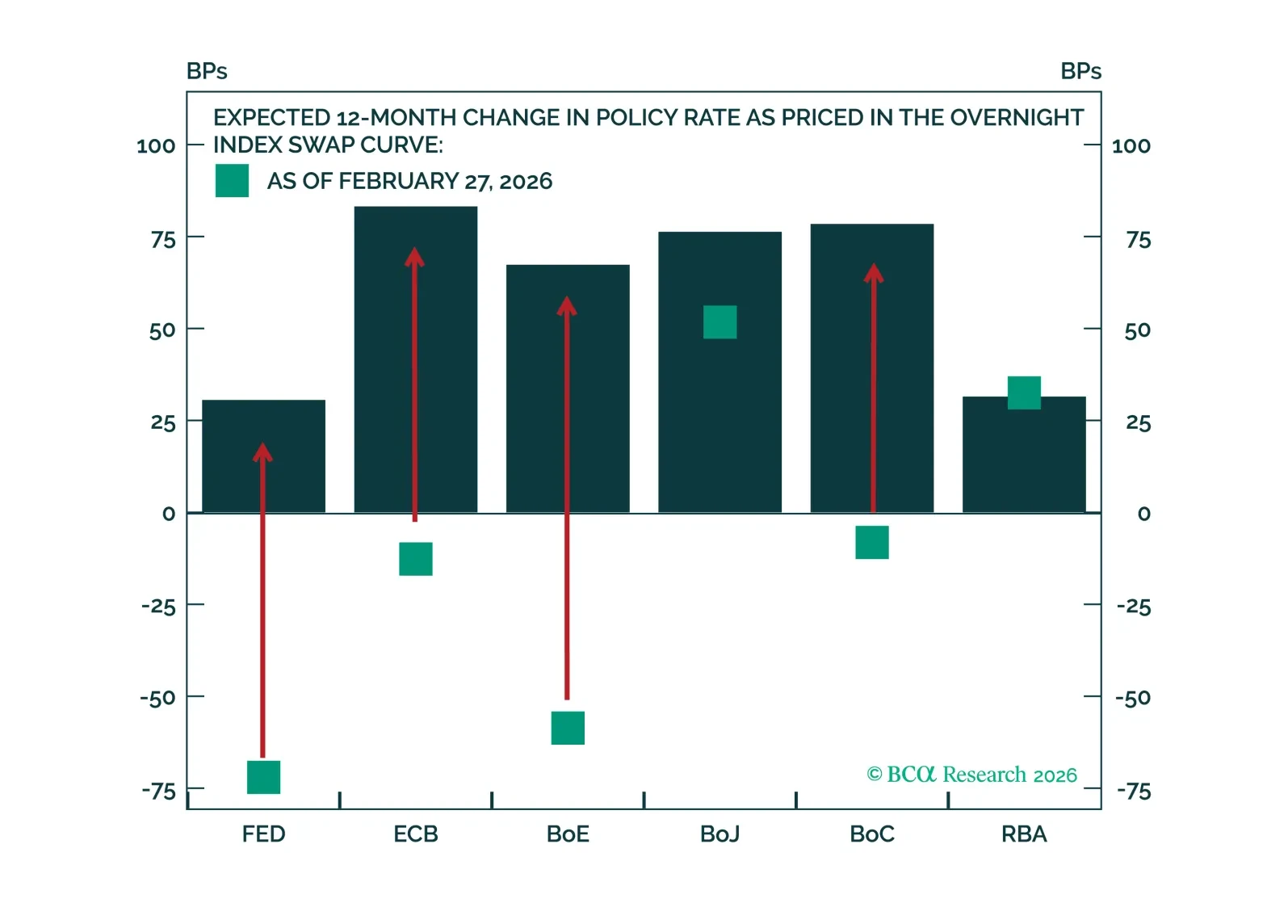

Downgrade global and US portfolio duration from “above benchmark” to “at benchmark” as the risk of hawkish monetary policy surprises is rising.

Tech companies have historically generated profits from three main sources: 1) economies of scale; 2) network effects; and 3) proprietary technologies. AI threatens to undercut all three sources.

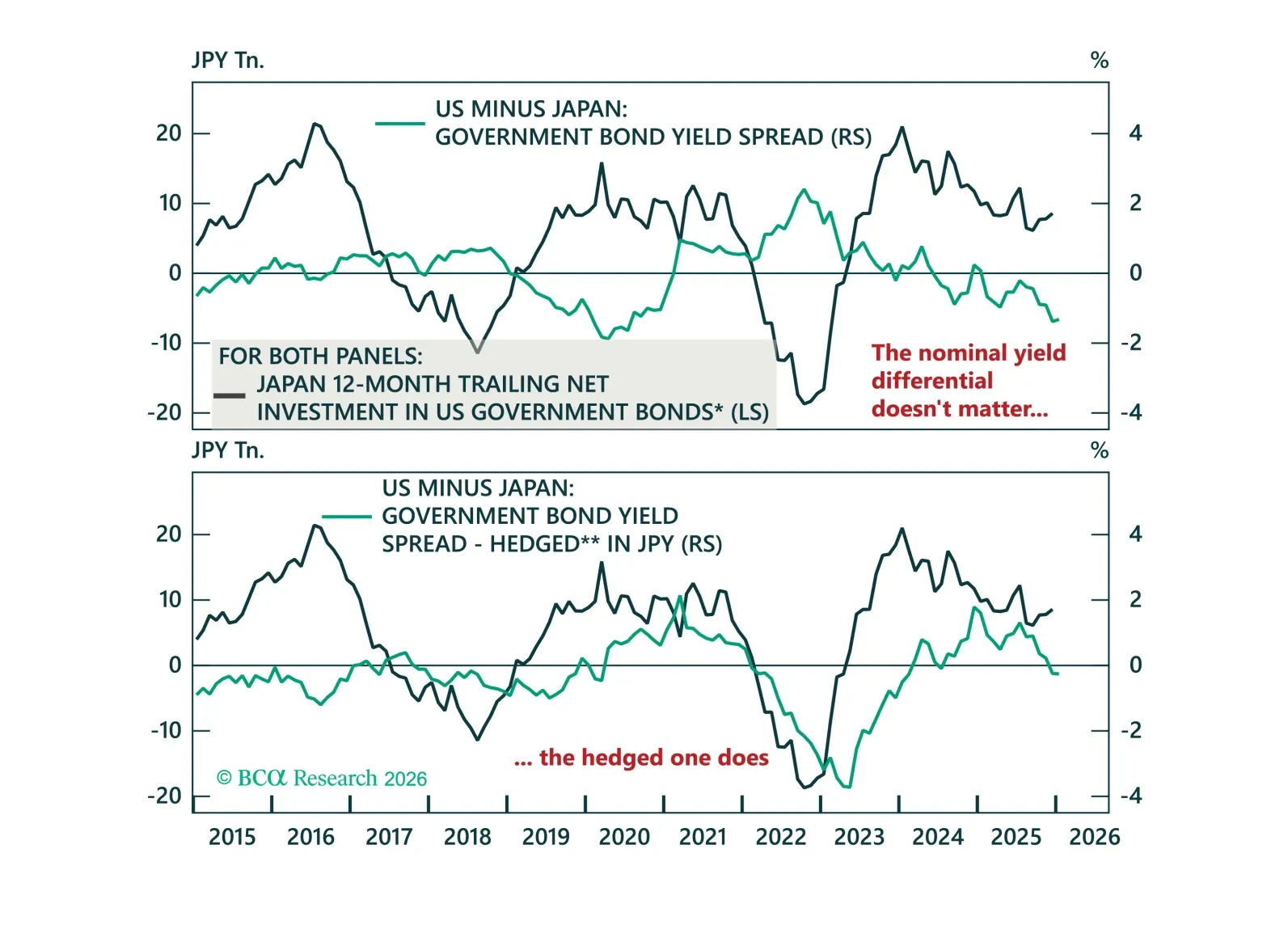

We spent last week meeting investors in Switzerland. This Strategy Insight revisits the most prominent topics we discussed, including repatriation fears, SNB intervention, and Dutch pension reform.

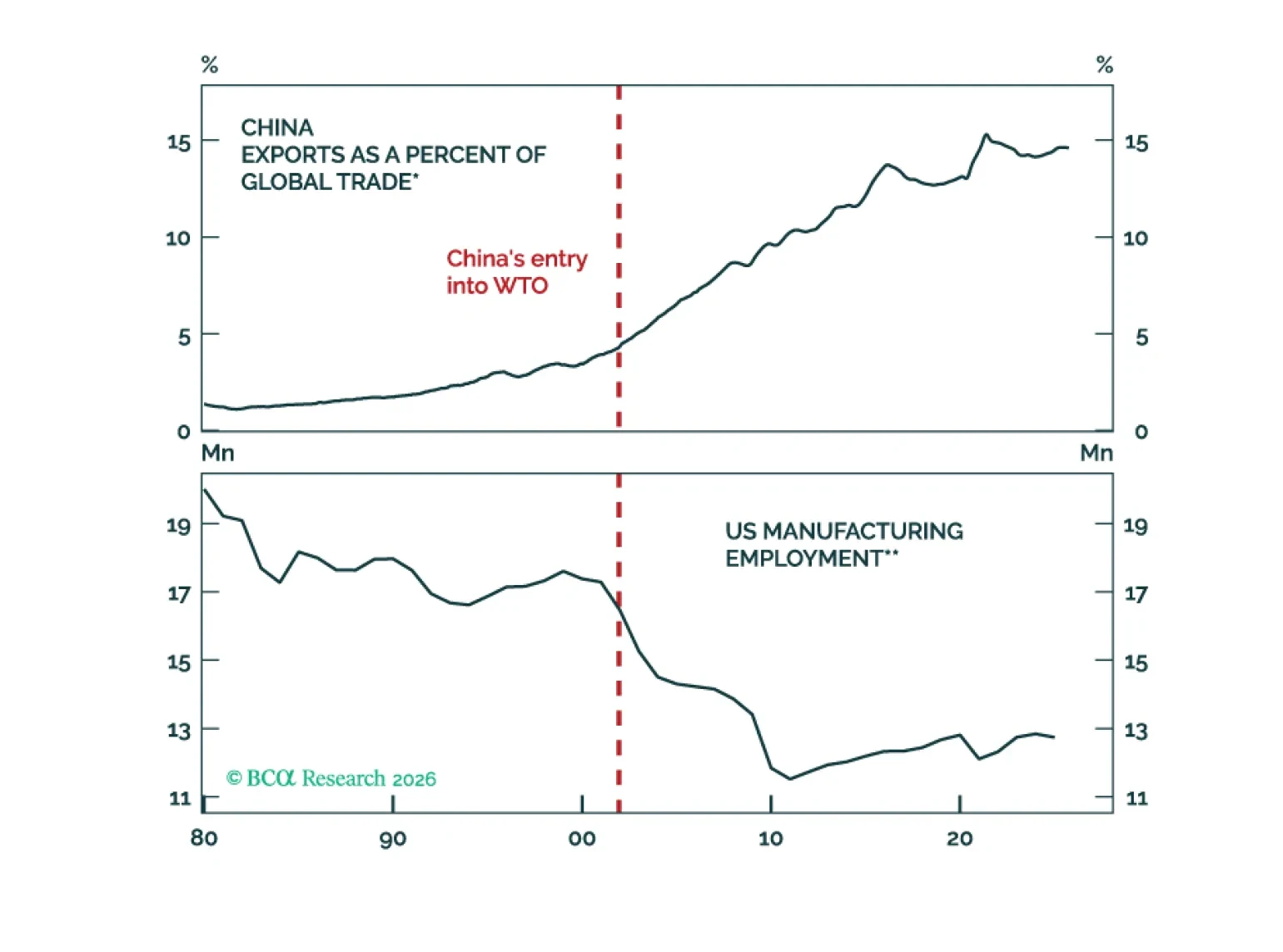

If humanoid robots were to become substitutable for workers, the AI age could lead to rapid growth in the size of the effective global labor force. The result could be a larger version of the “China shock,” which followed China’s entry into the global economy.

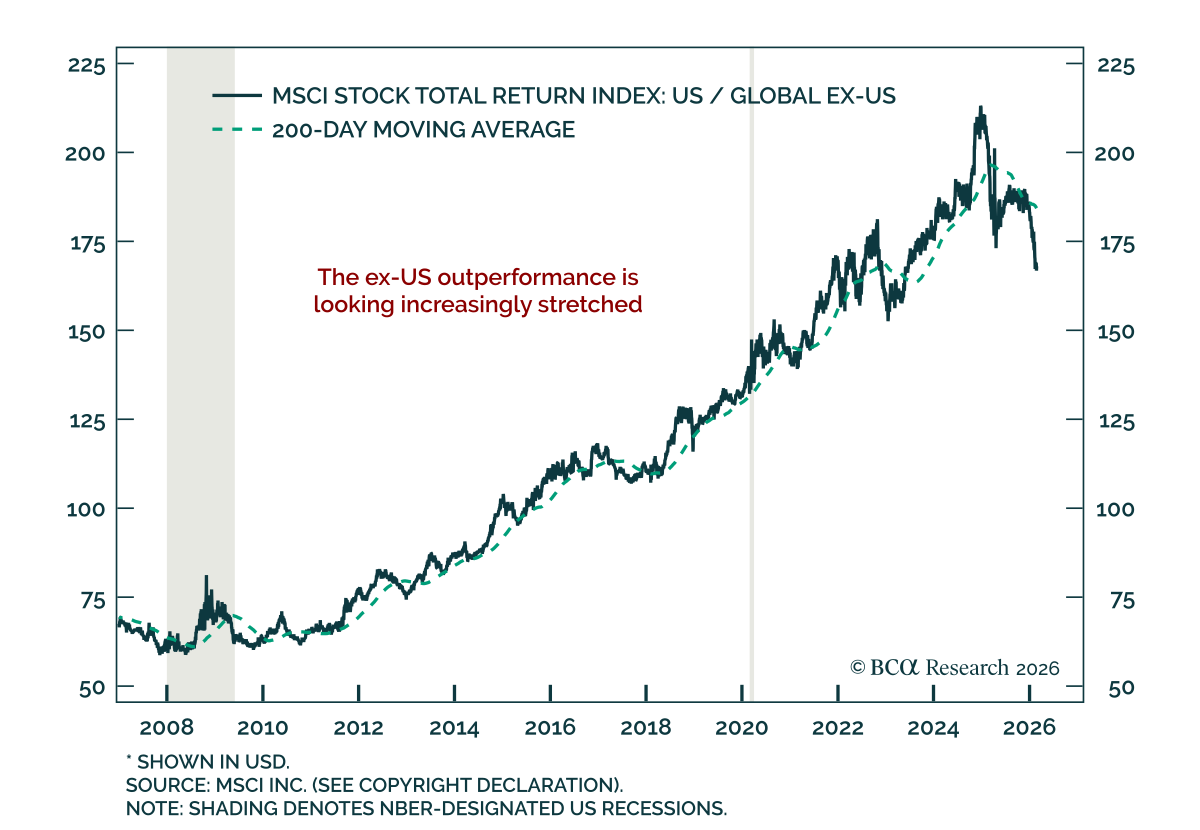

The actions of the Trump administration have dominated the headlines over the past month. They are all noise. Focus on the reactions from the rest of the world. Policy makers outside of the US are now determined to stimulate and reform their domestic economies. Global growth is accelerating without a corresponding increase in inflation. This combination is not only positive for risk assets but is also supercharging returns for Ex-US stocks. Downgrade Fixed Income and duration.