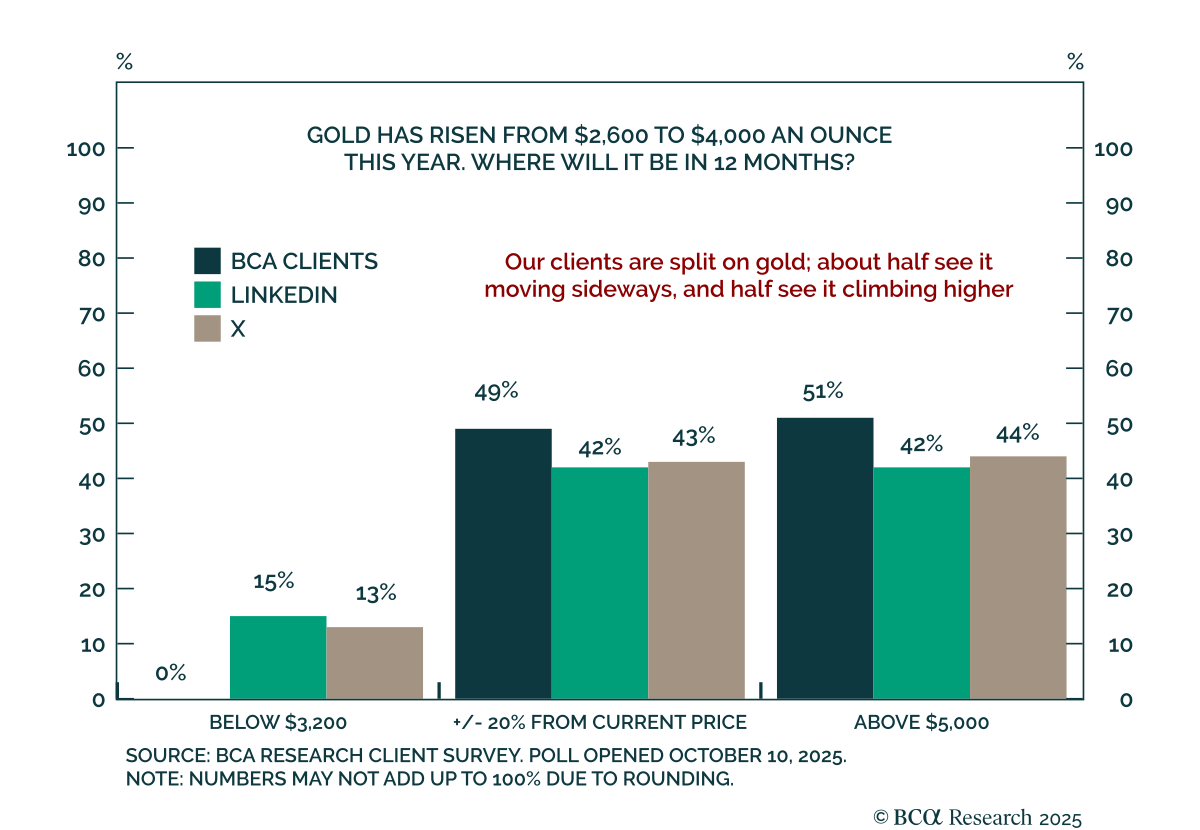

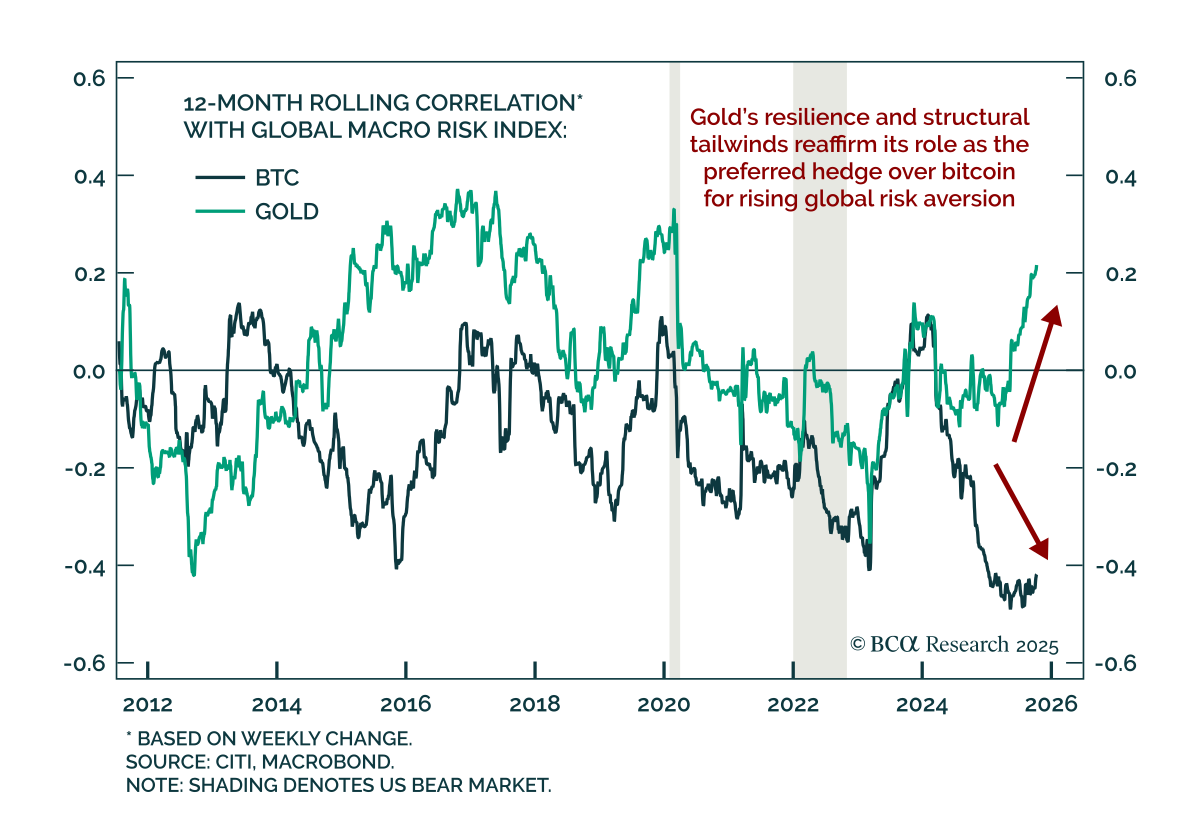

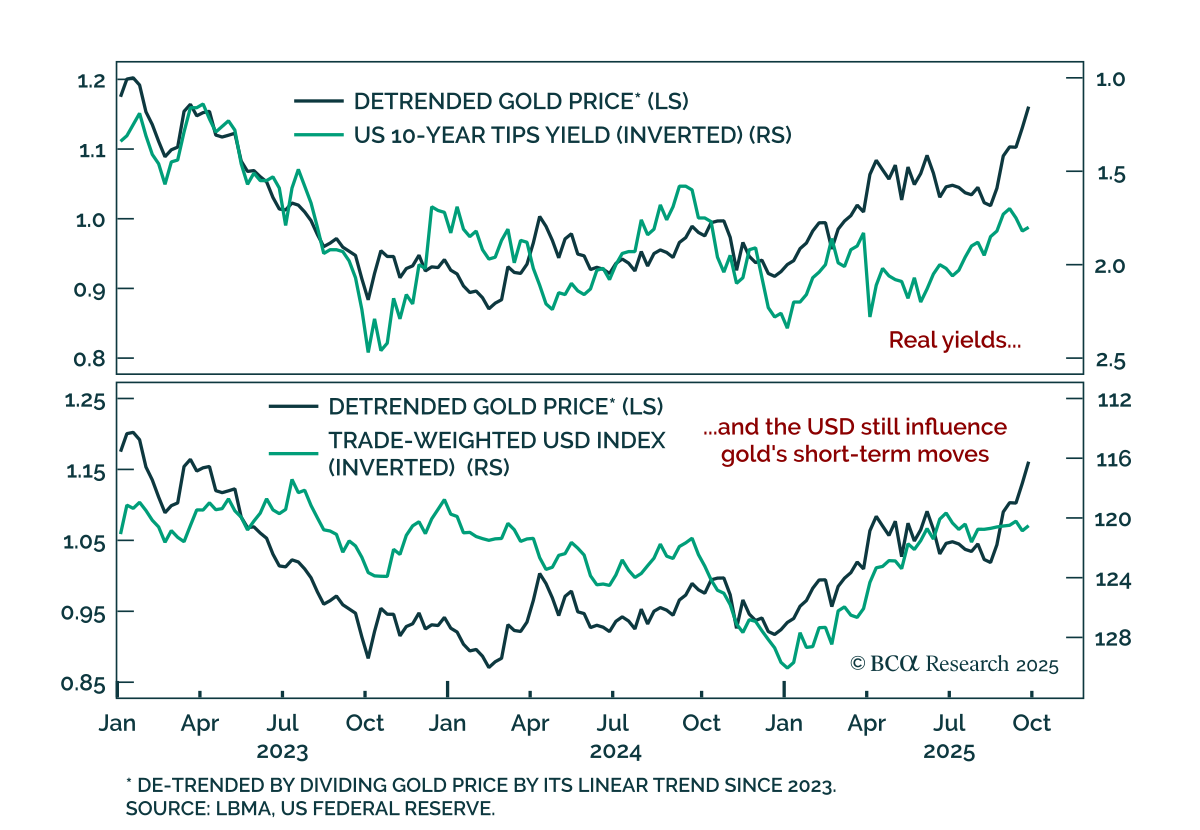

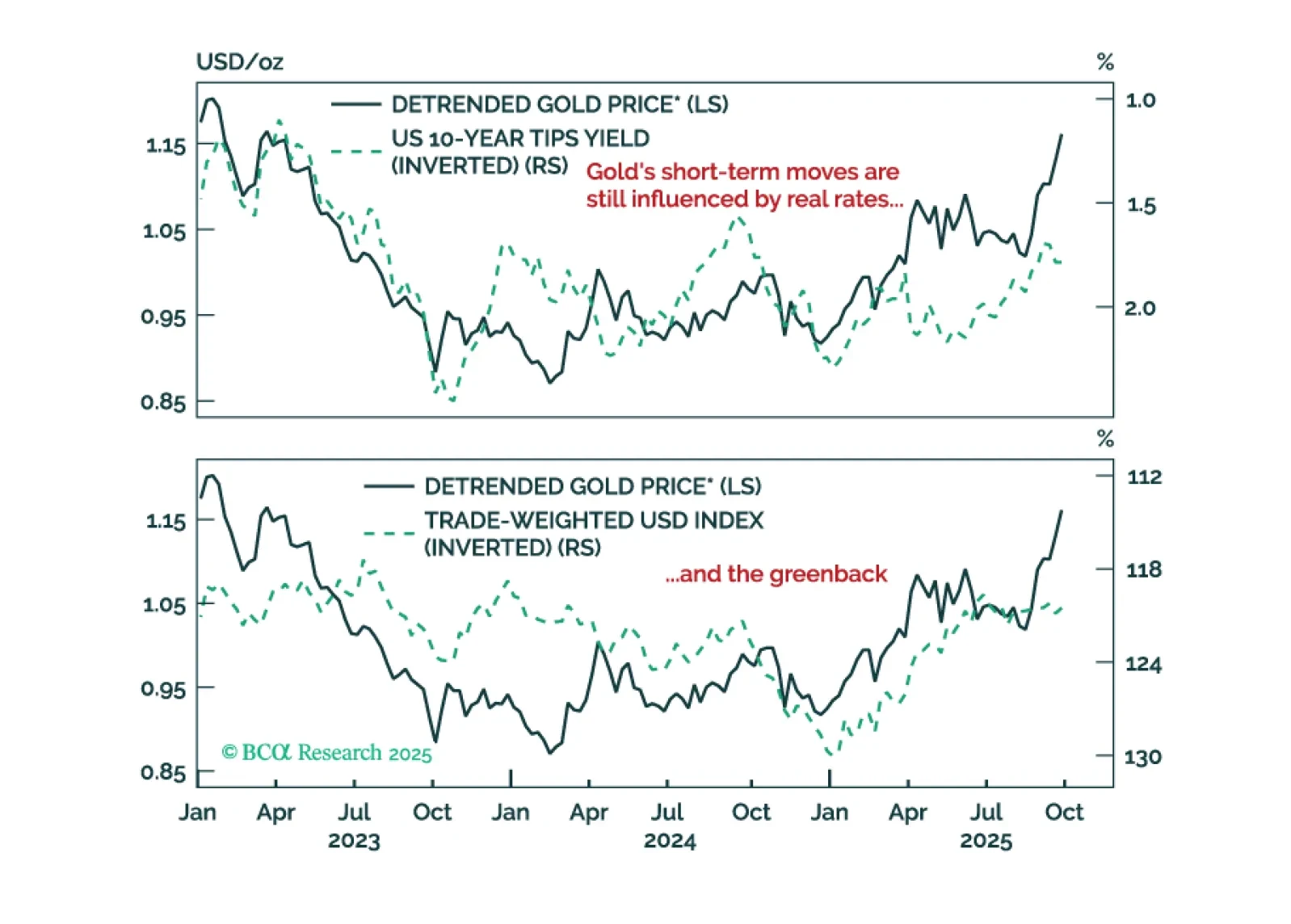

Gold

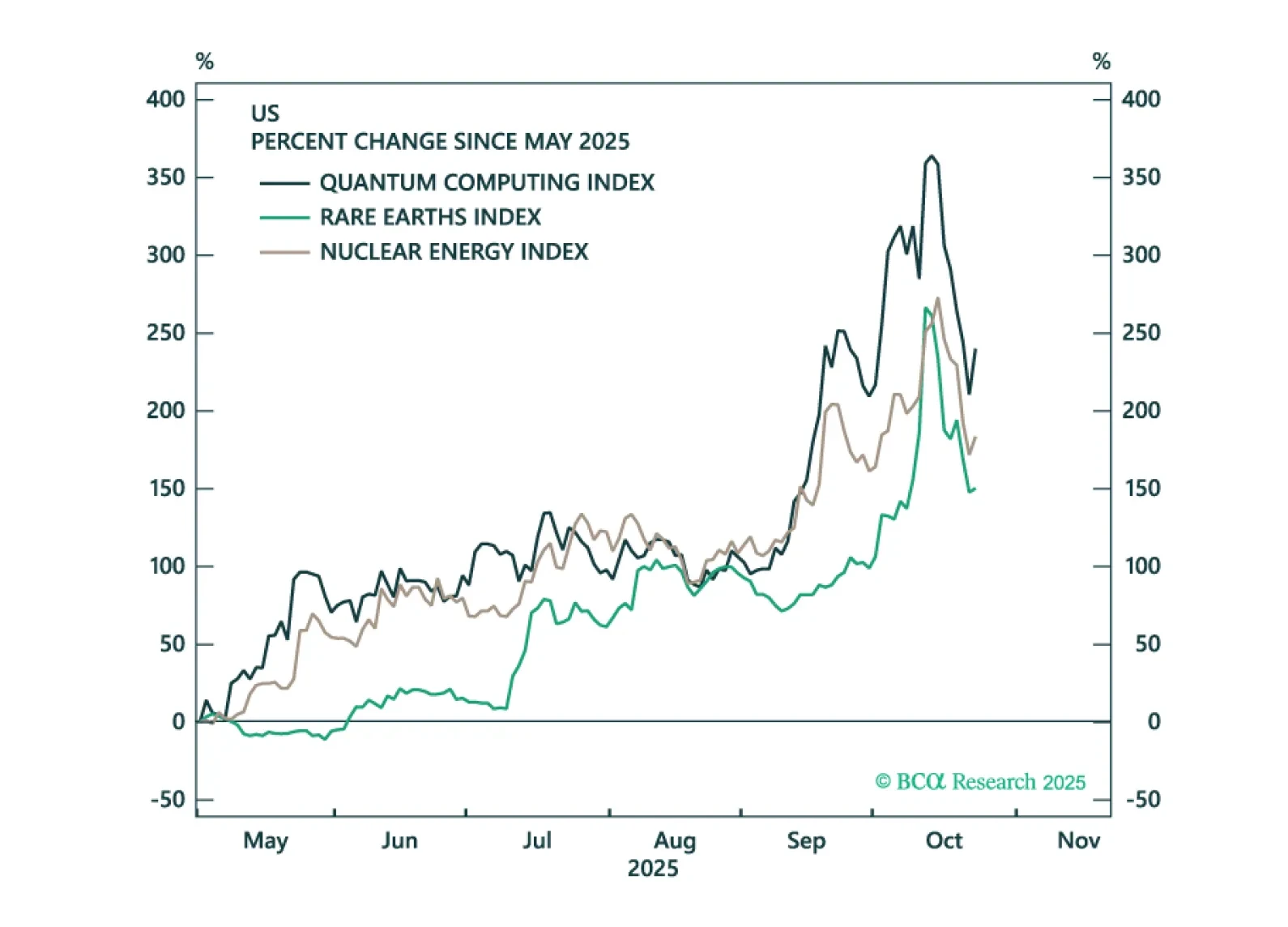

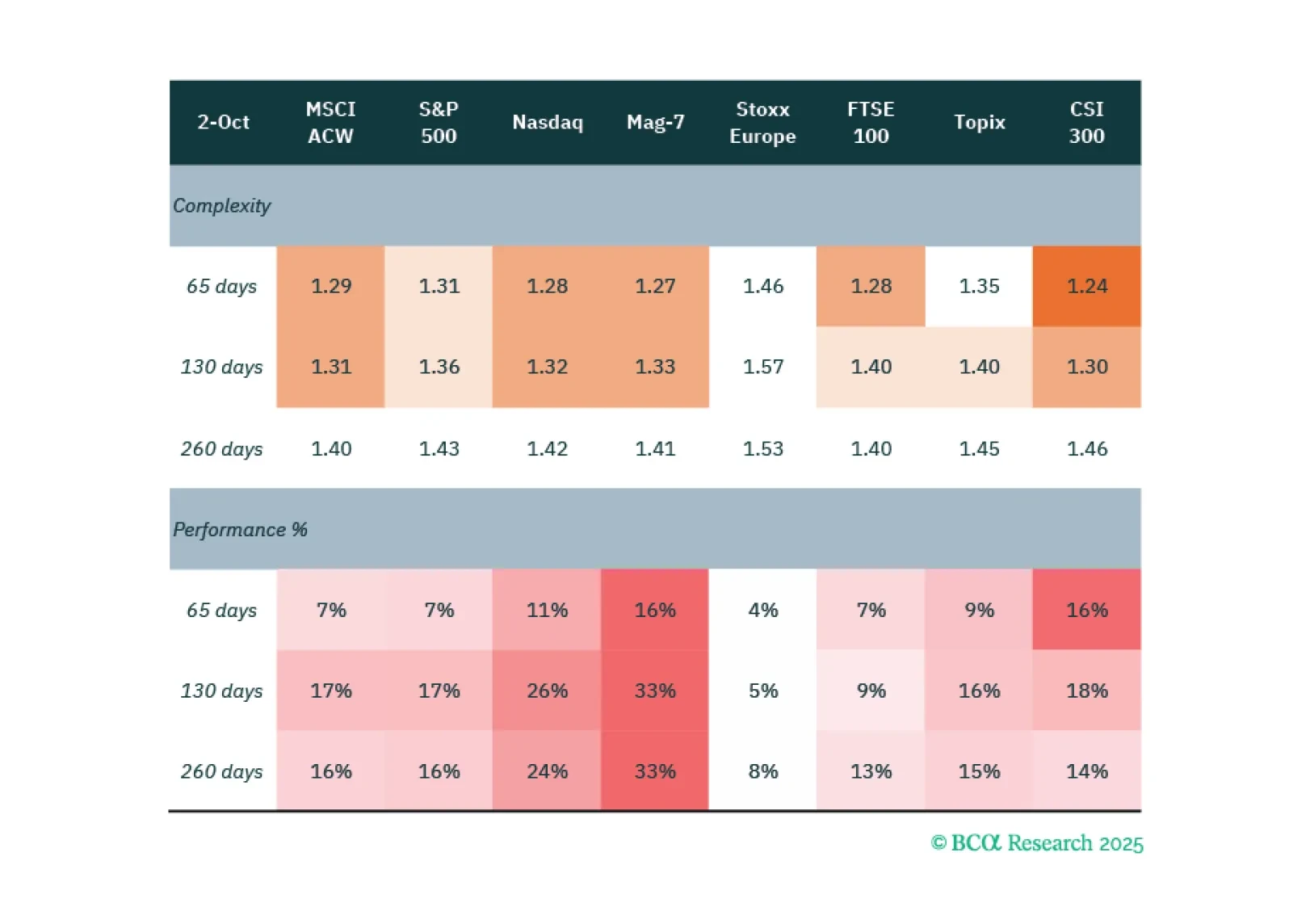

Precious metals, corporate credit, and tech stocks are all showing signs of late-cycle euphoria. We identify various trigger points that investors should monitor to turn more bearish.

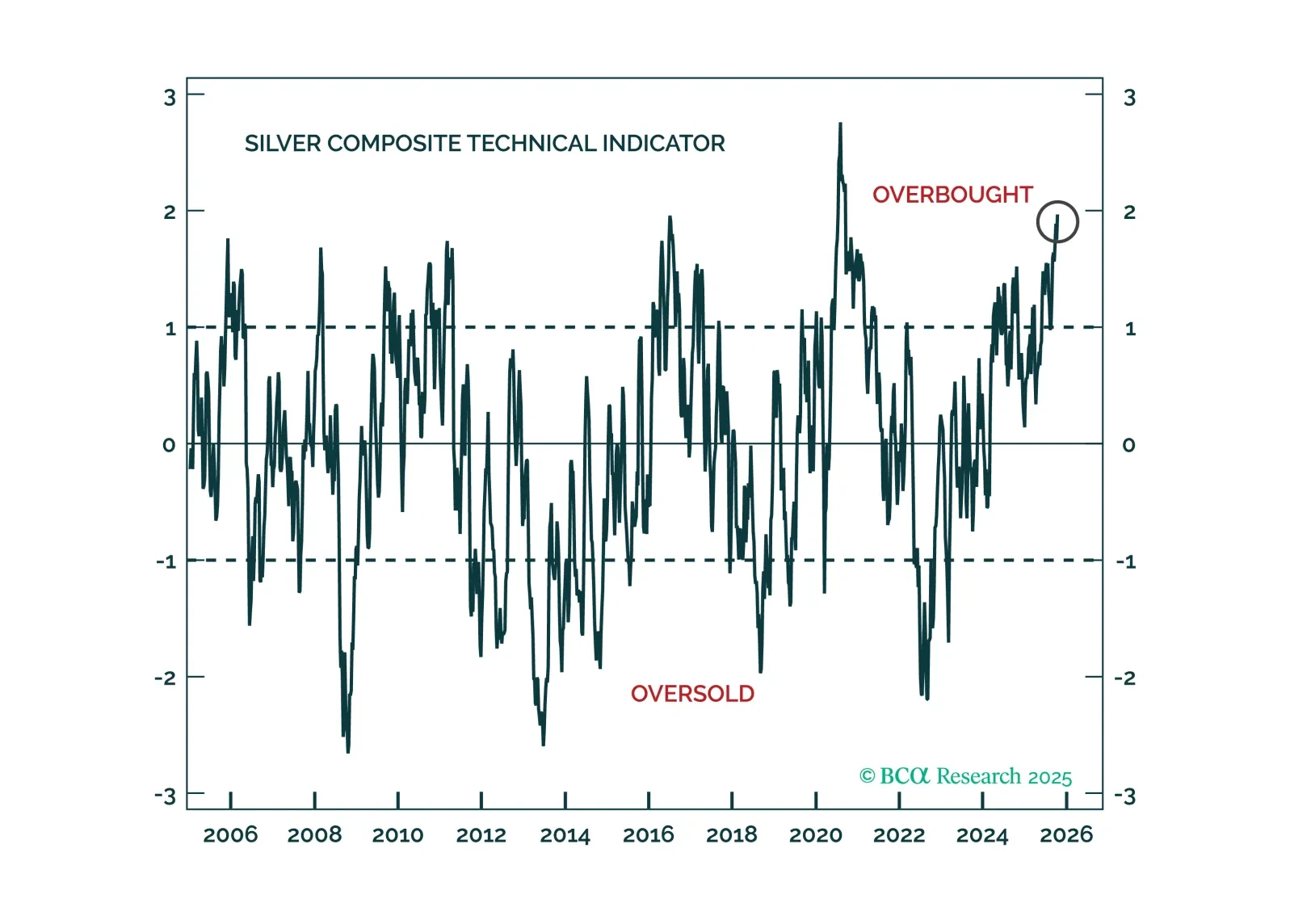

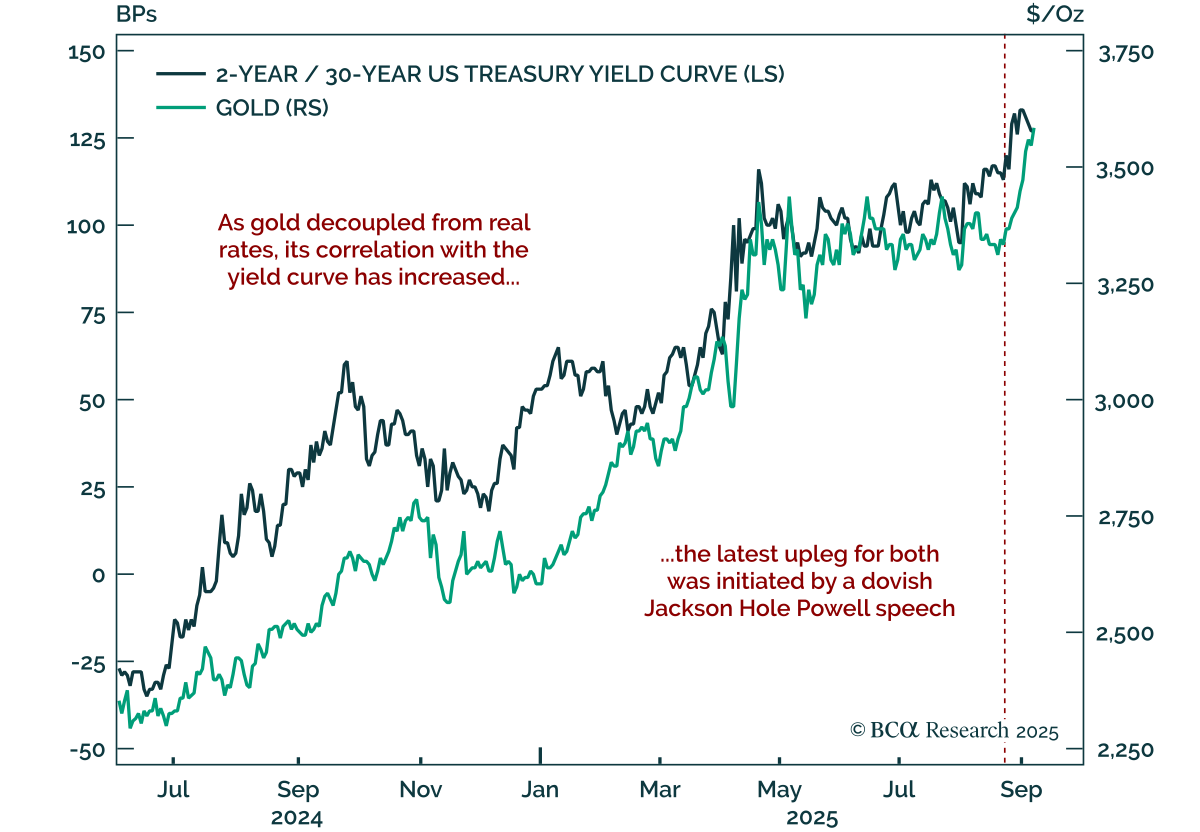

Speculative froth has built up across all precious metals, yet gold’s structural tailwinds will allow it to weather corrections better than its peers.

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.

Commodity market breadth would need to improve for it to signal bullish conditions for the aggregate commodity complex. We maintain a defensive tilt within commodities, favoring precious metals over the more cyclically sensitive energy and industrial metals.

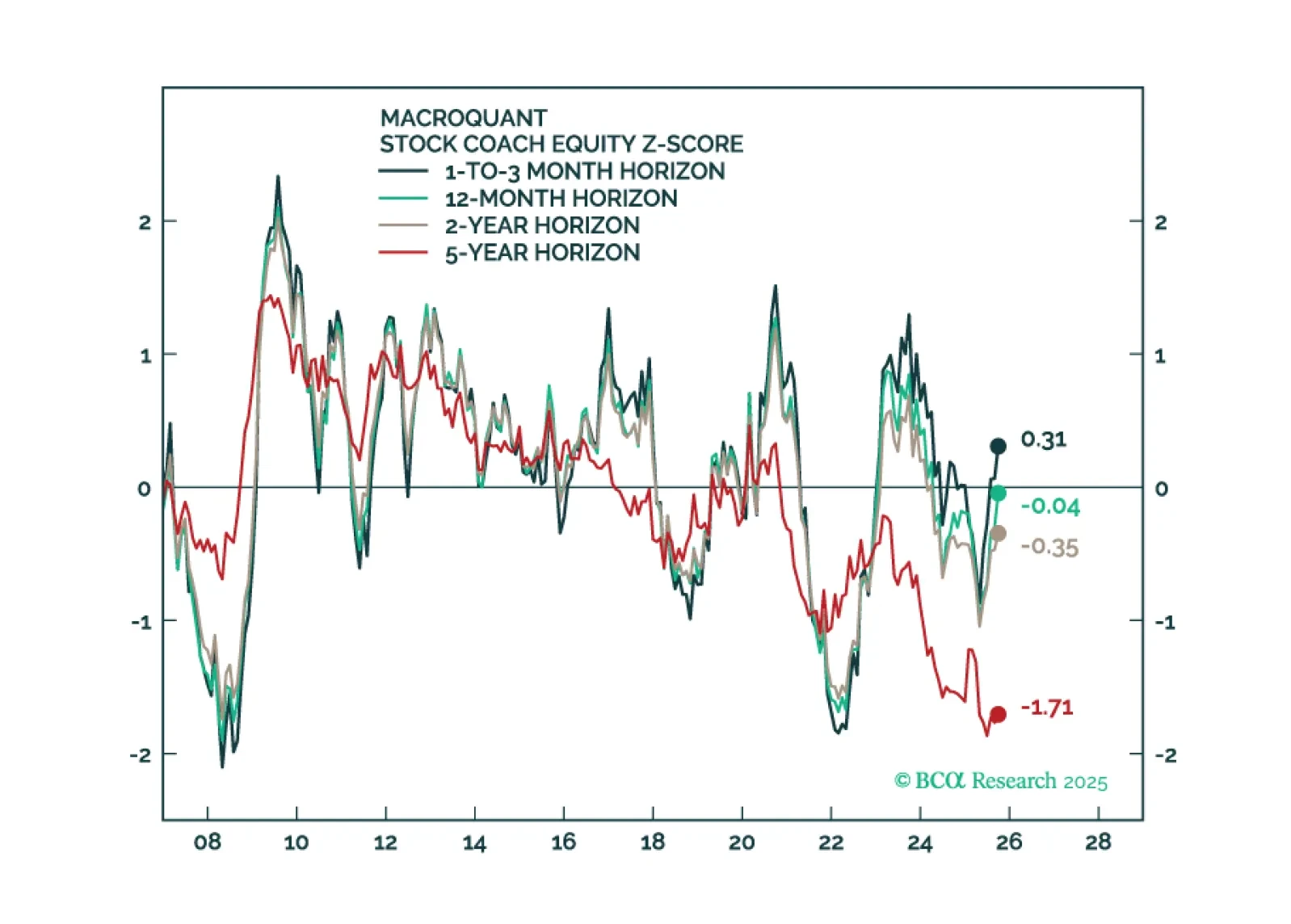

A short guide on how best to use and interpret our real-time fractal heatmap for asset allocation.

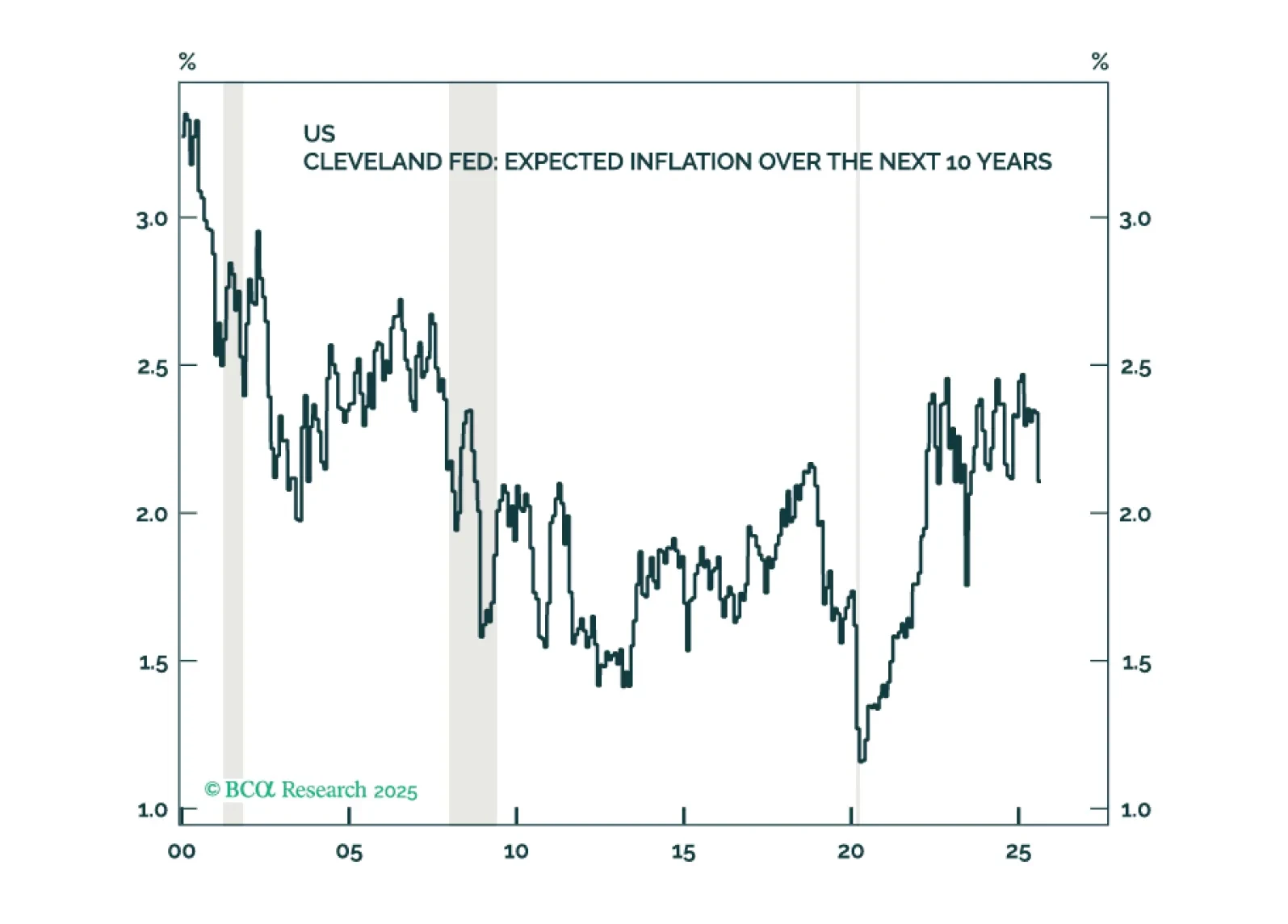

Inflation expectations in the US remain reasonably well anchored and there are few signs of a brewing wage-price spiral. Thus, the near-term risks to growth outweigh the risks of higher inflation. Looking beyond the next year or two, however, we are worried about stagflation.