Gov Sovereigns/Treasurys

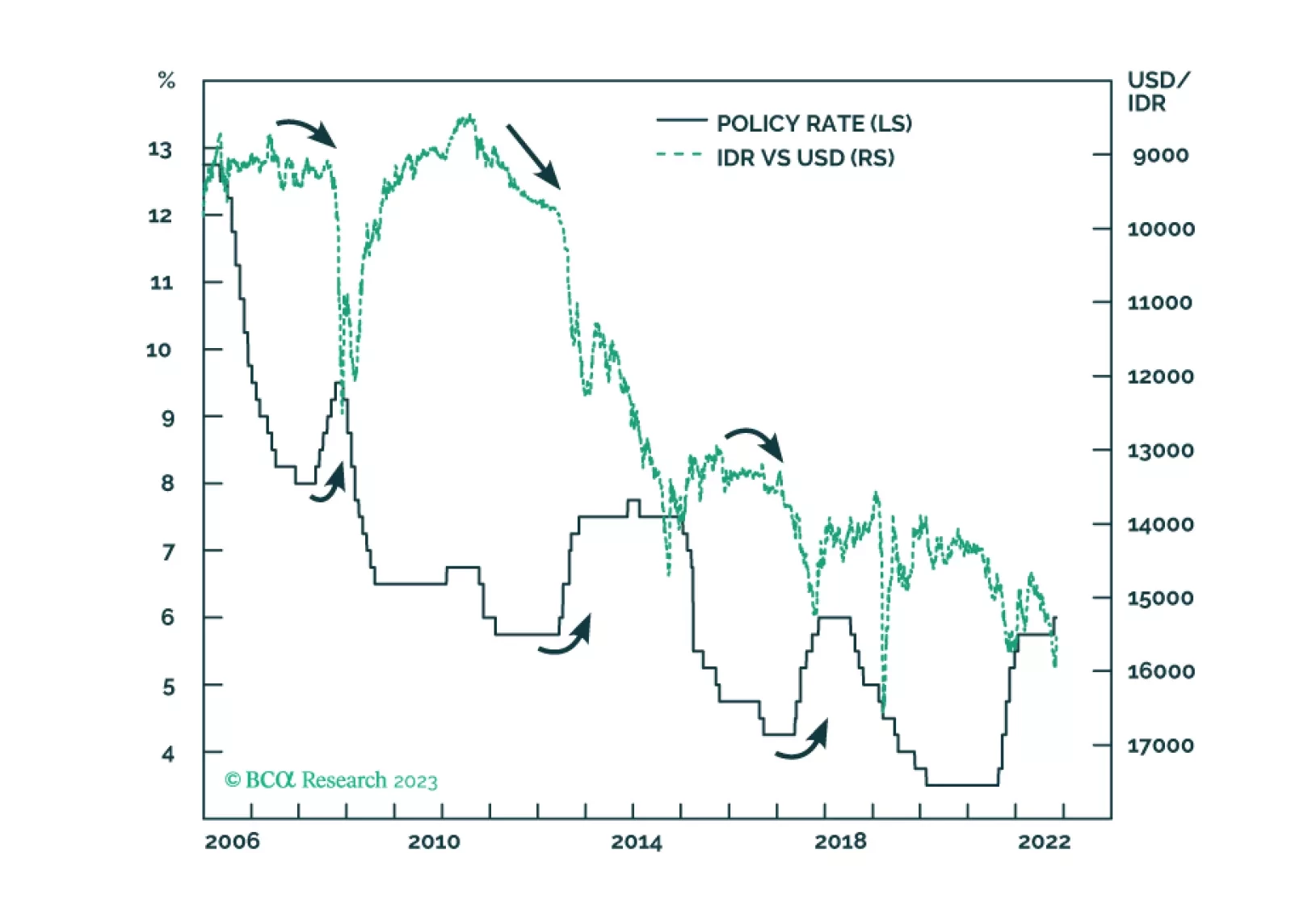

Despite very low inflation, Bank Indonesia raised its policy rates last month to support the currency. The strategy did not work before and will not work now. Stay short the rupiah.

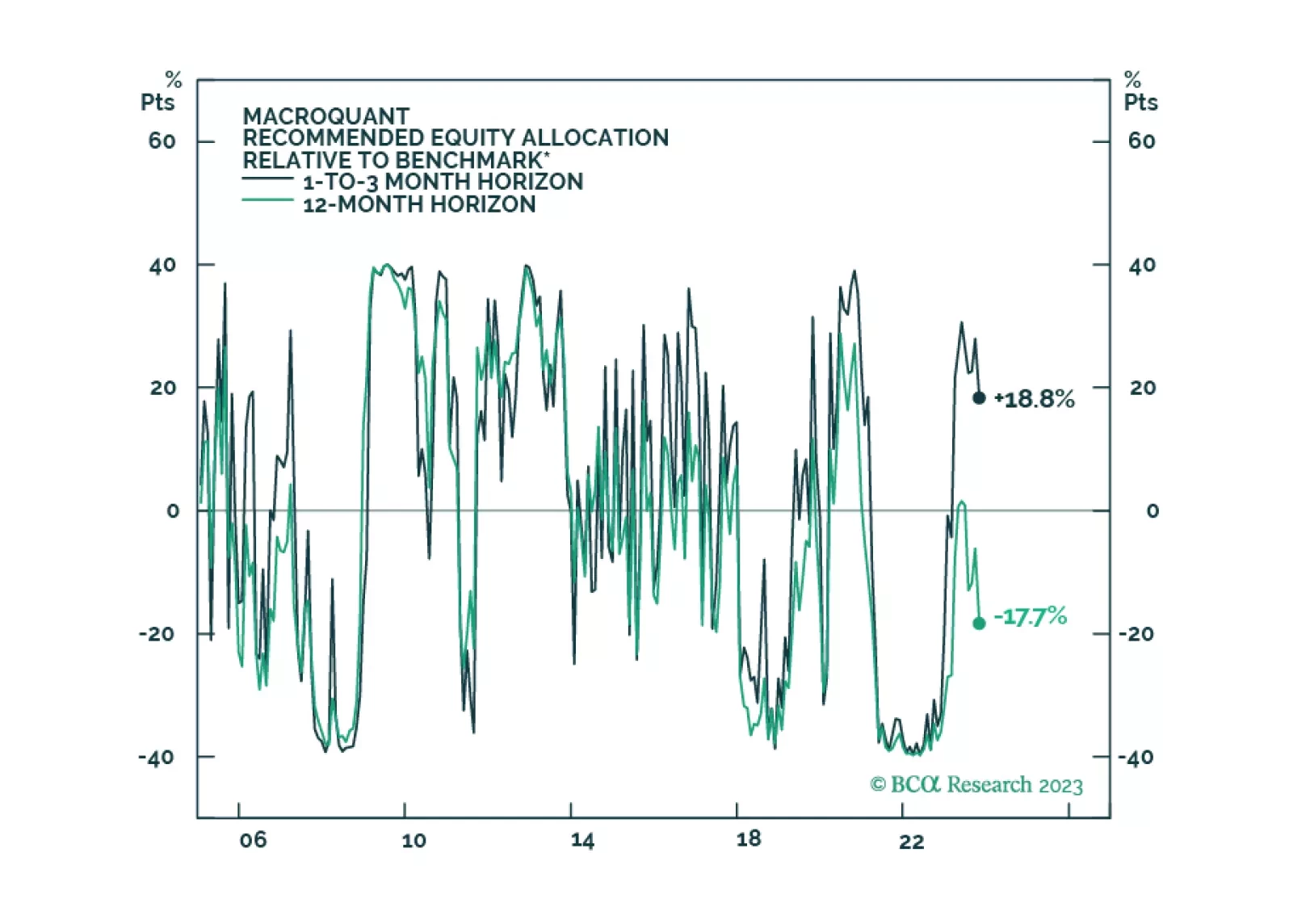

Our Portfolio Allocation Summary for November 2023.

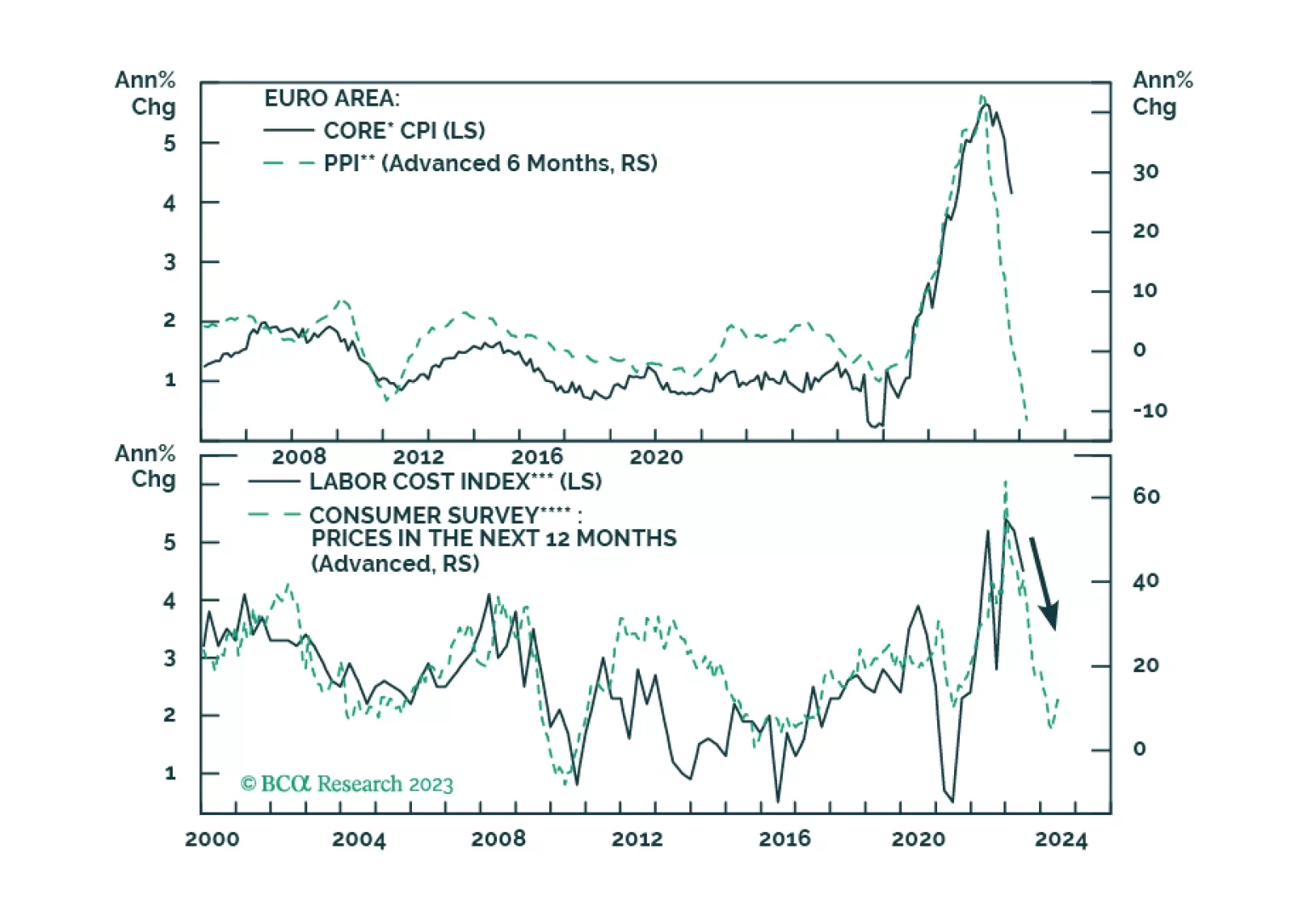

The Eurozone’s inflation will continue to slow over the coming months. While this trend will help Bund prices, will it boost the appeal of European equities?

We are approaching another phase transition from boom to bust. Stocks should rally into year-end, but investors should look to reduce equity exposure early next year while increasing bond exposure.

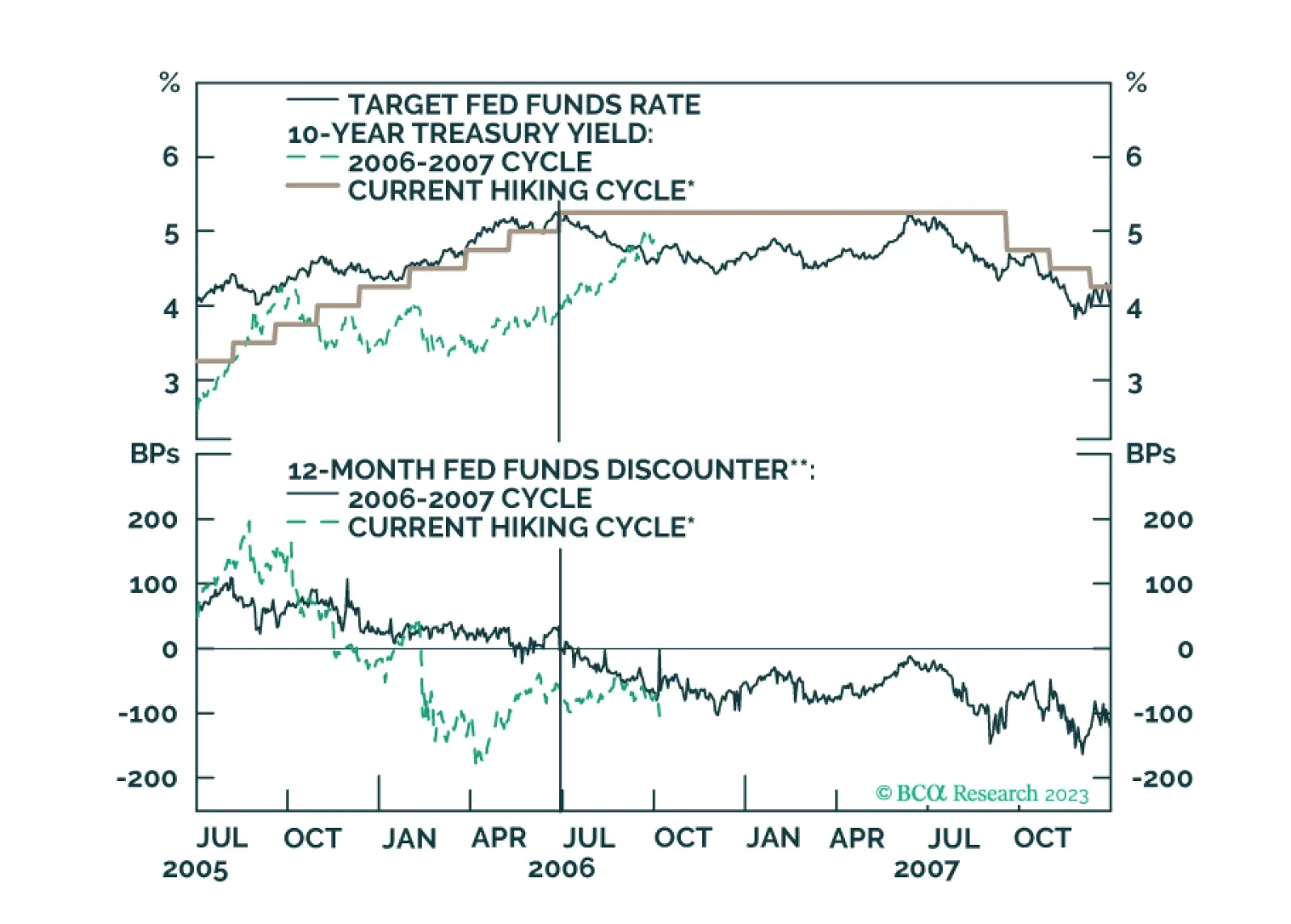

Our reaction to today’s FOMC meeting and the Treasury’s Quarterly Refunding Announcement.

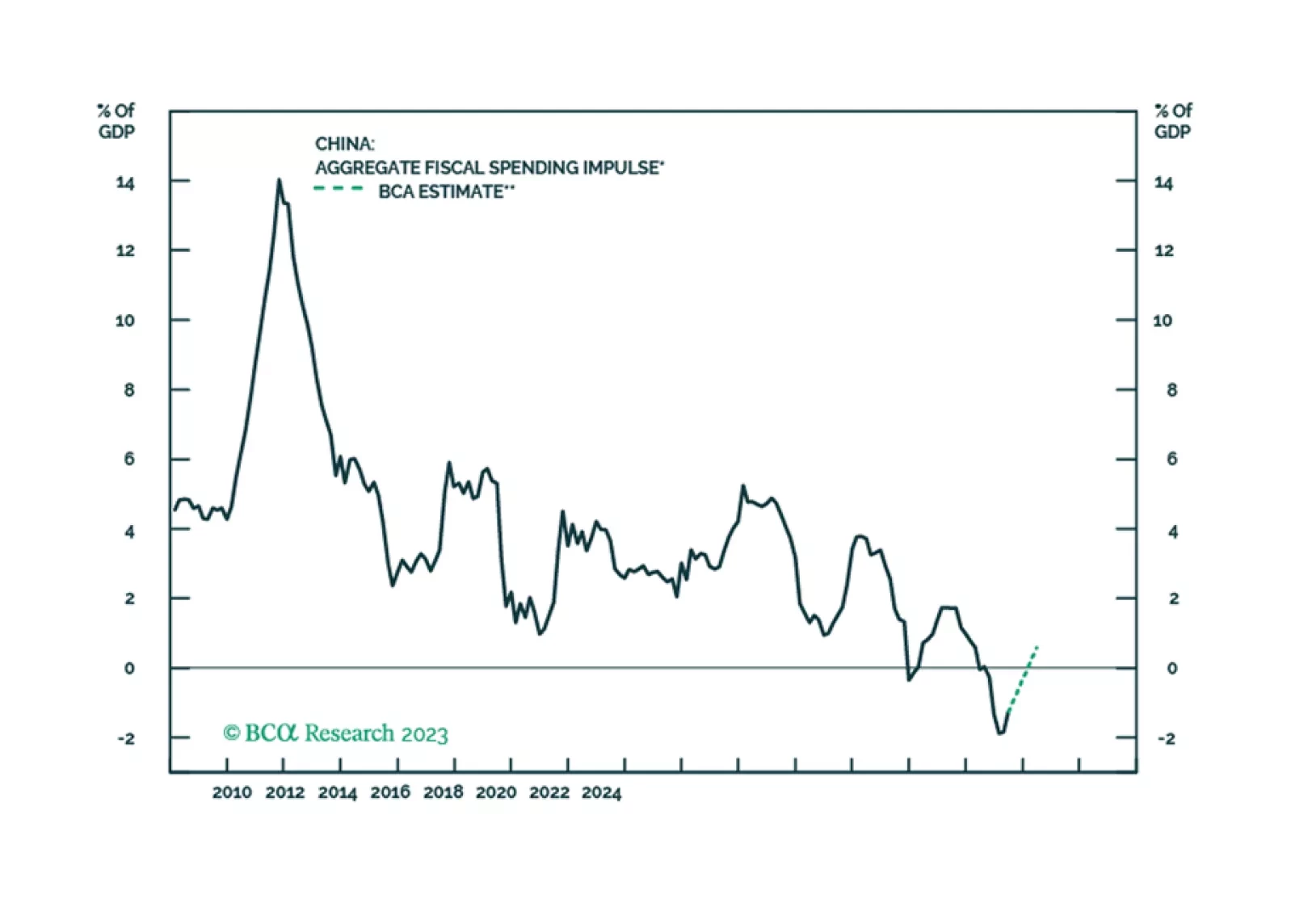

We maintain our view that China’s economic growth in the coming months will remain lackluster. Beijing's recent measures to provide additional financing may help to bridge the gap in government spending in the rest of 2023 and into 2024, but the impact on growth will be very limited.

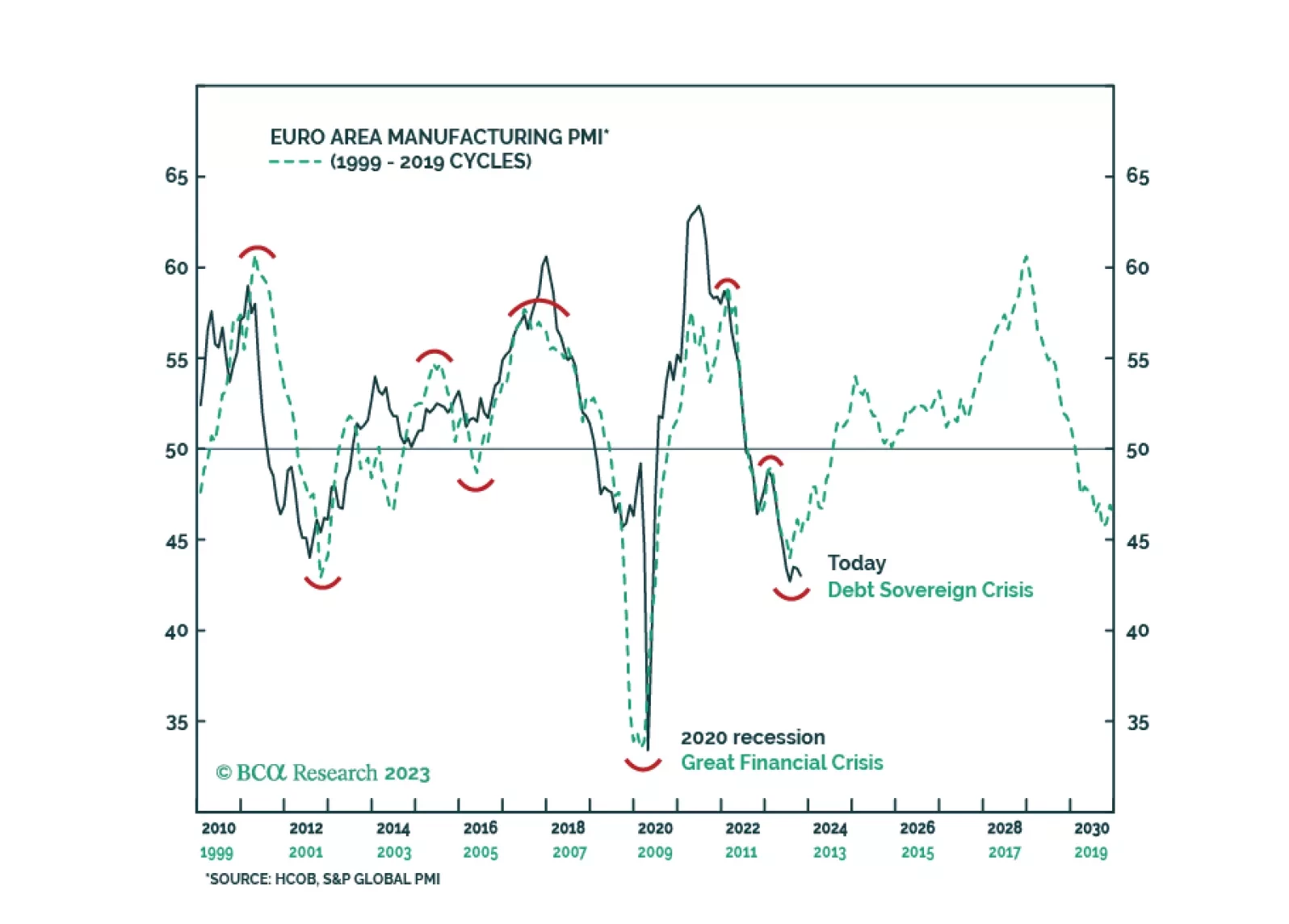

What will the next manufacturing cycle look like in Europe and how will risk assets perform? Lessons from the recent past.

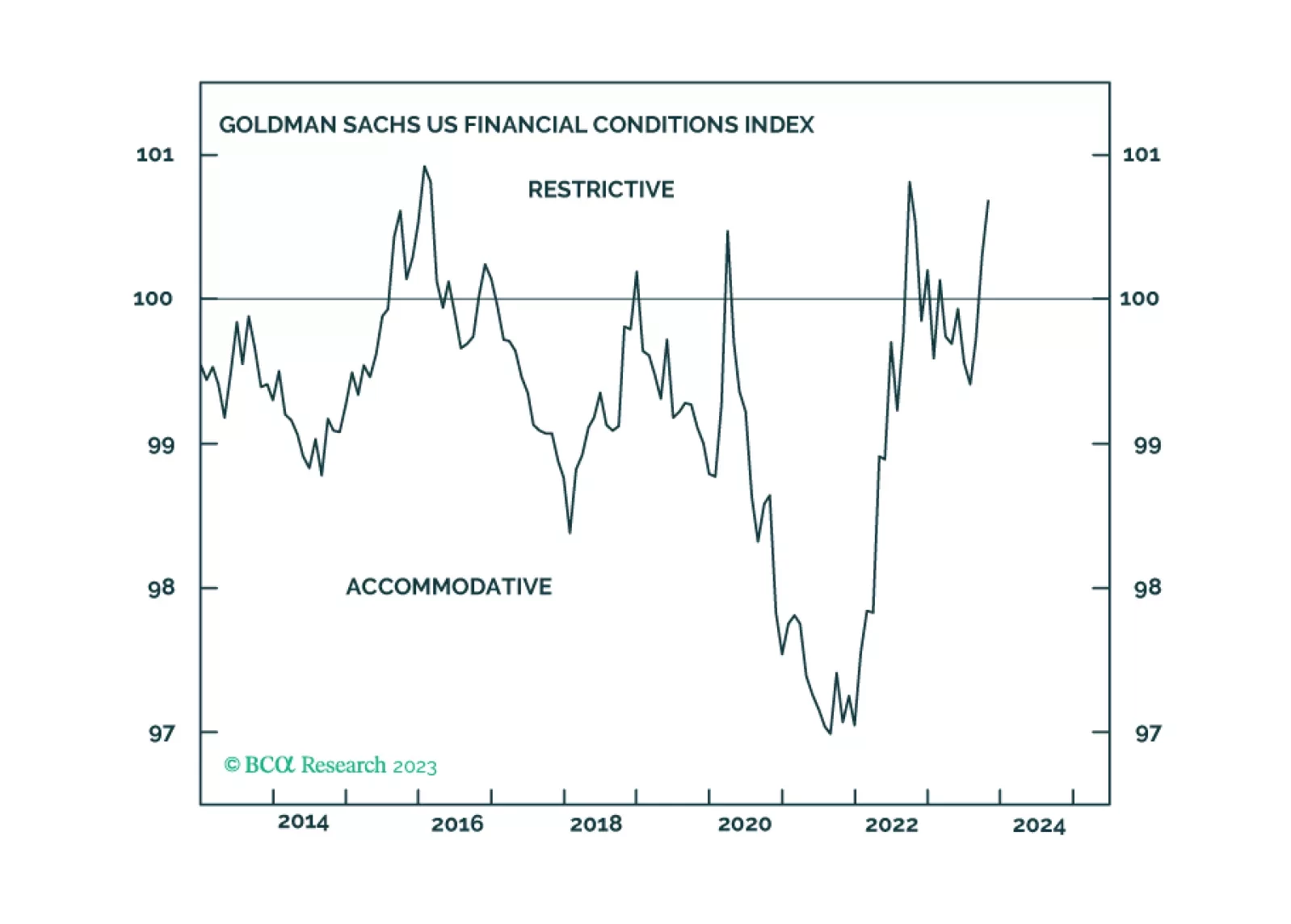

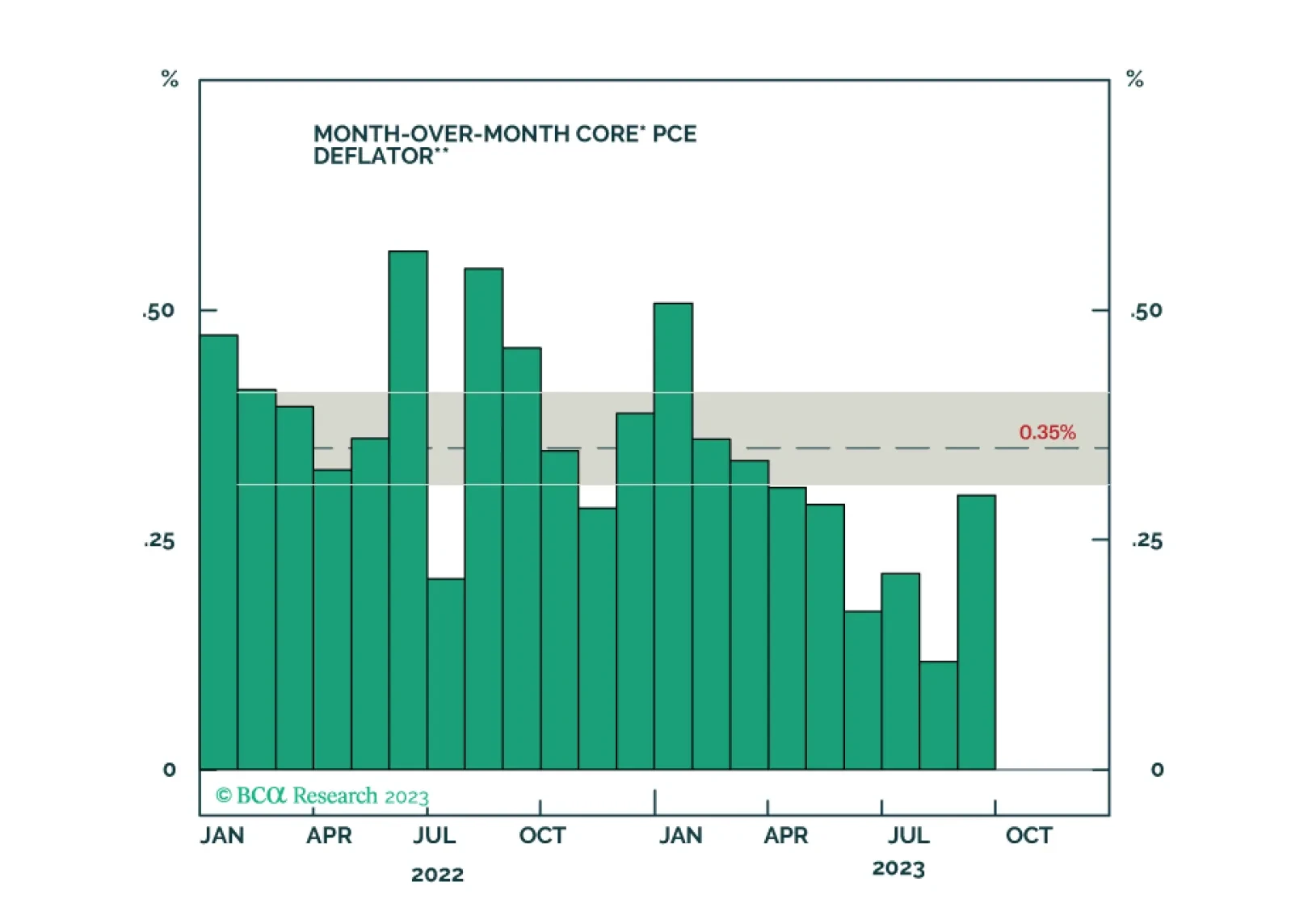

A look at recent data on economic growth, inflation and the labor market, and a discussion of the implications for Fed policy and bond strategy.

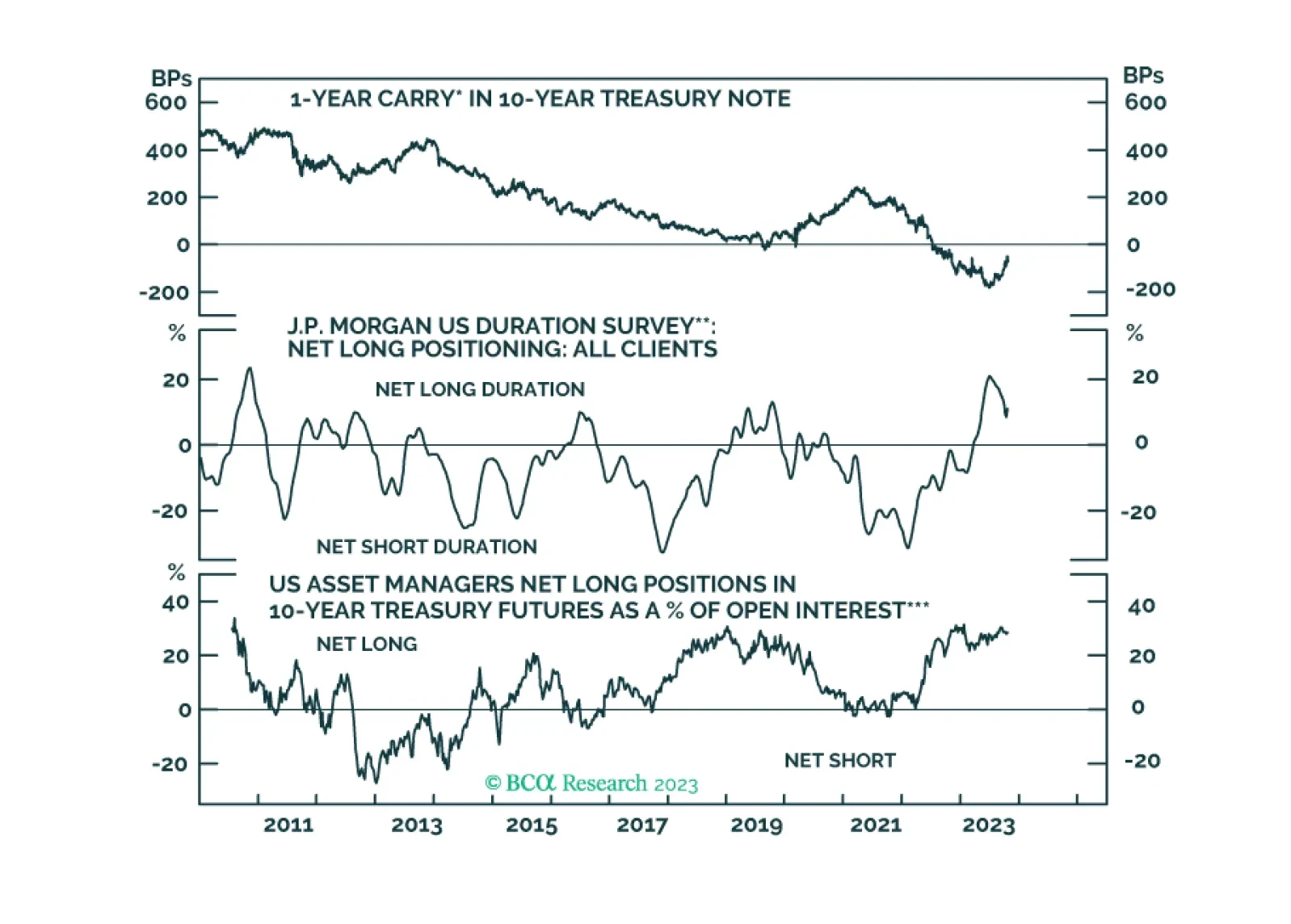

This week’s report contains an update on the Treasury curve’s recent bear-steepening trend and a look at different measures of long-maturity Treasury valuation.

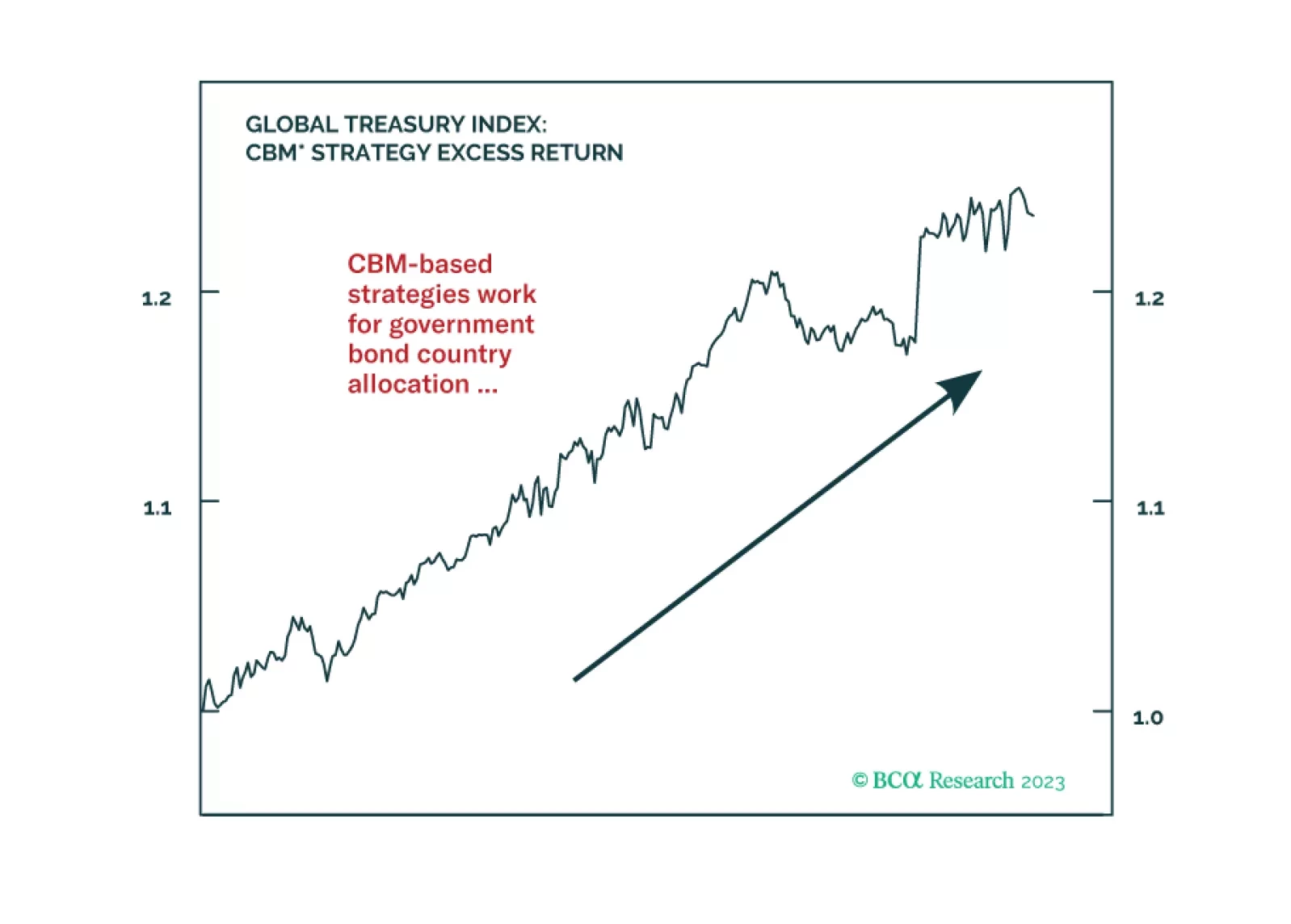

In this Special Report, we introduce two strategies that use our Central Bank Monitors for global fixed income country allocations and currency trades. We find that using the Monitors in country selection helps improve the performance of a developed markets government bond portfolio. The CBMs can also help substantially minimize the drawdowns on a standard FX carry strategy.