Inflation

The SEC has just approved bitcoin spot ETFs, but does bitcoin have any ‘intrinsic’ value? In this Special Report we explain why the answer is yes, how bitcoin compares with gold, and why the bitcoin price could ultimately head well north of $100,000.

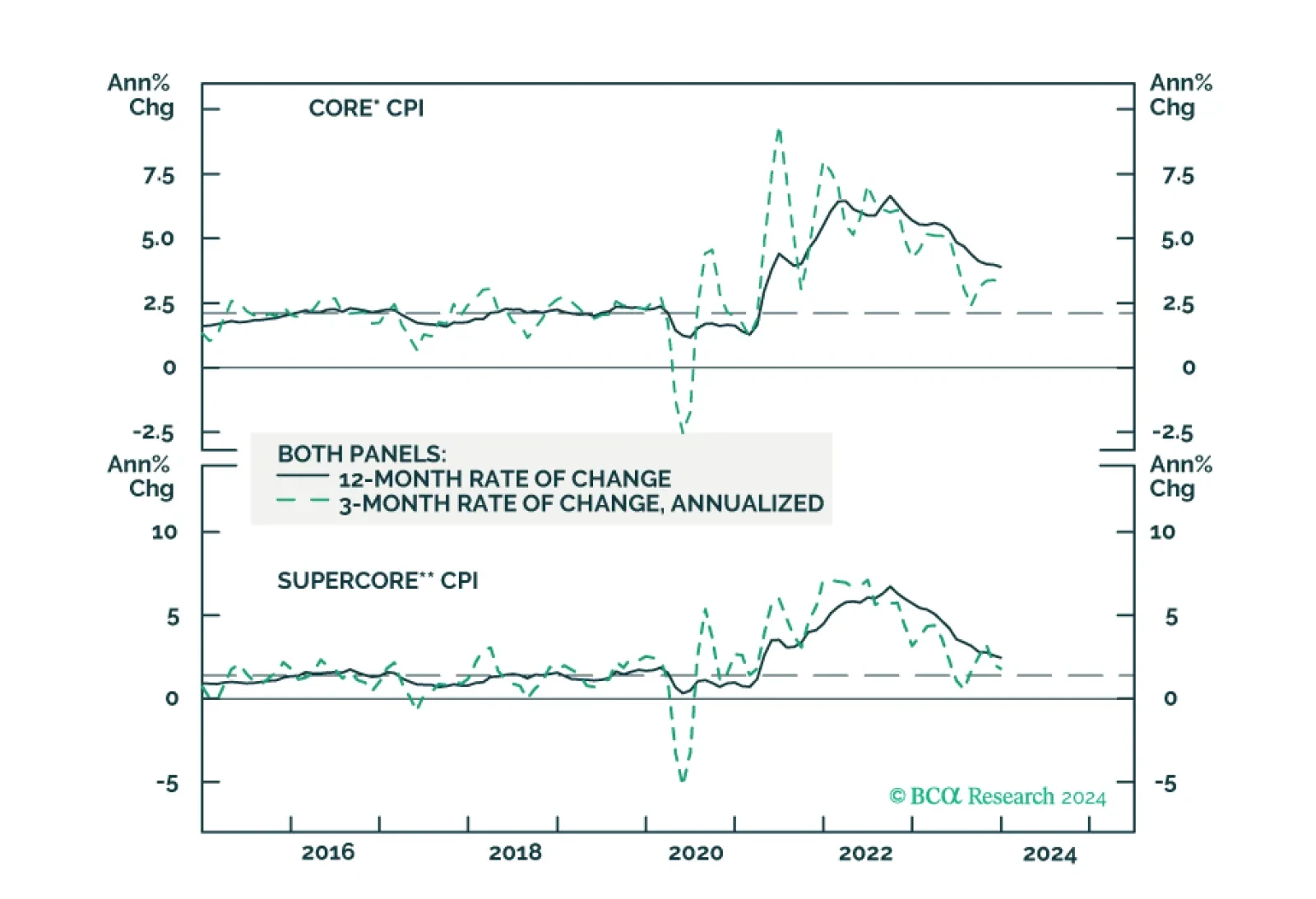

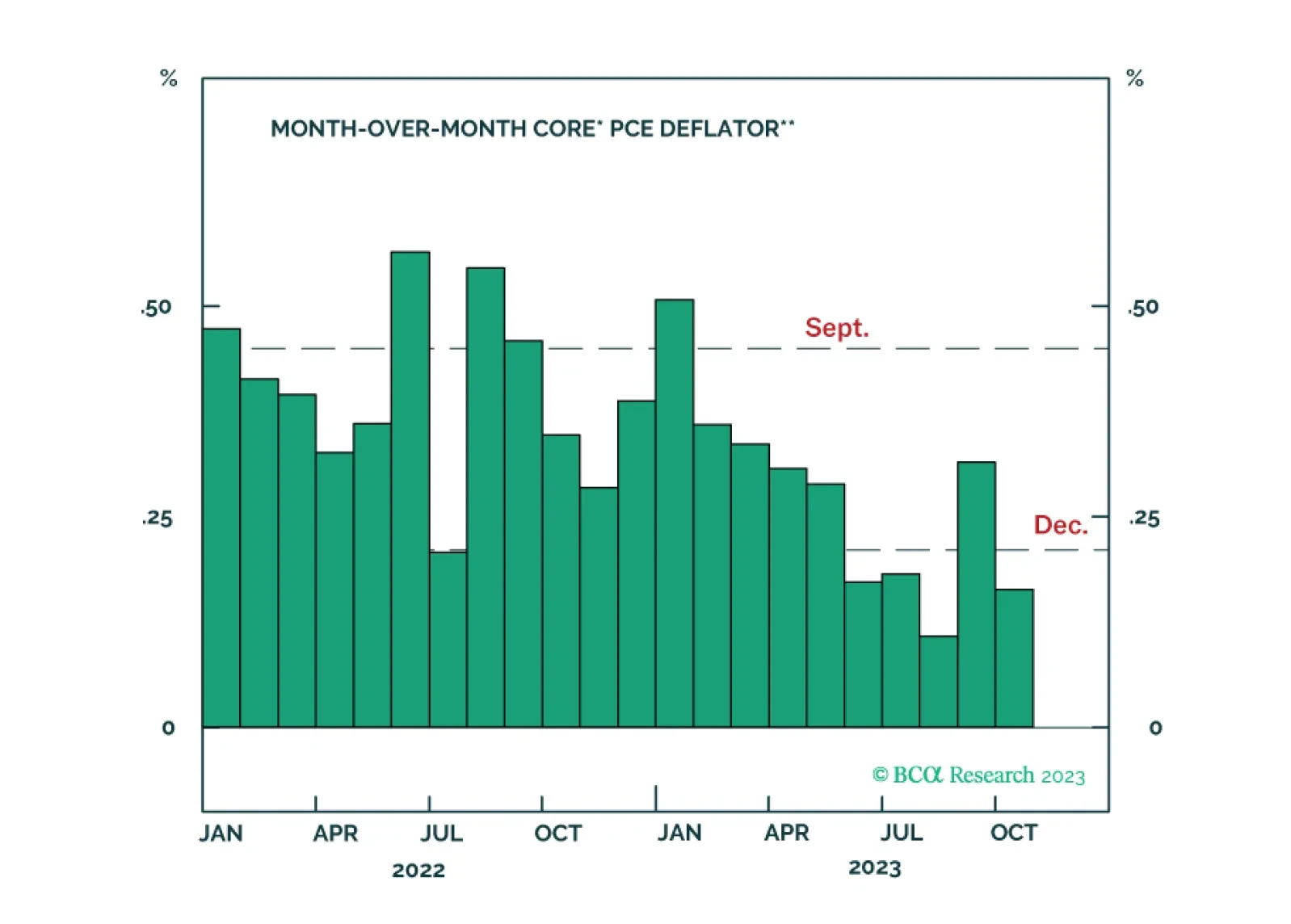

We update our inflation forecast following this morning’s CPI report.

Increasing gray-zone confrontations and another round of tariff and non-tariff barriers to trade are not being reflected in commodity prices. This is keeping inflationary pressures emanating from the real economy subdued. That said, inflation risks are increasing as threats to commodity supplies and supply chains grow. Standard monetary policy focused on aggregate-demand management is ill-suited for addressing these risks, and could exacerbate supply-side tightness. We remain long oil- and metals-producer equities exposure via the XOP and XME ETFs, and to commodities outright via the COMT ETF.

The Fed faces a dilemma. Cut rates early to avoid a recession, but at the risk of not slaying wage inflation. Or, not cut rates early to ensure that wage inflation is slayed, but at the risk of a downturn. Faced with such a dilemma, the lesser evil is to slay wage inflation even at the risk of a downturn. Meaning that the market has overpriced early rate cuts. We discuss some other investment implications, and identify two rebound candidates.

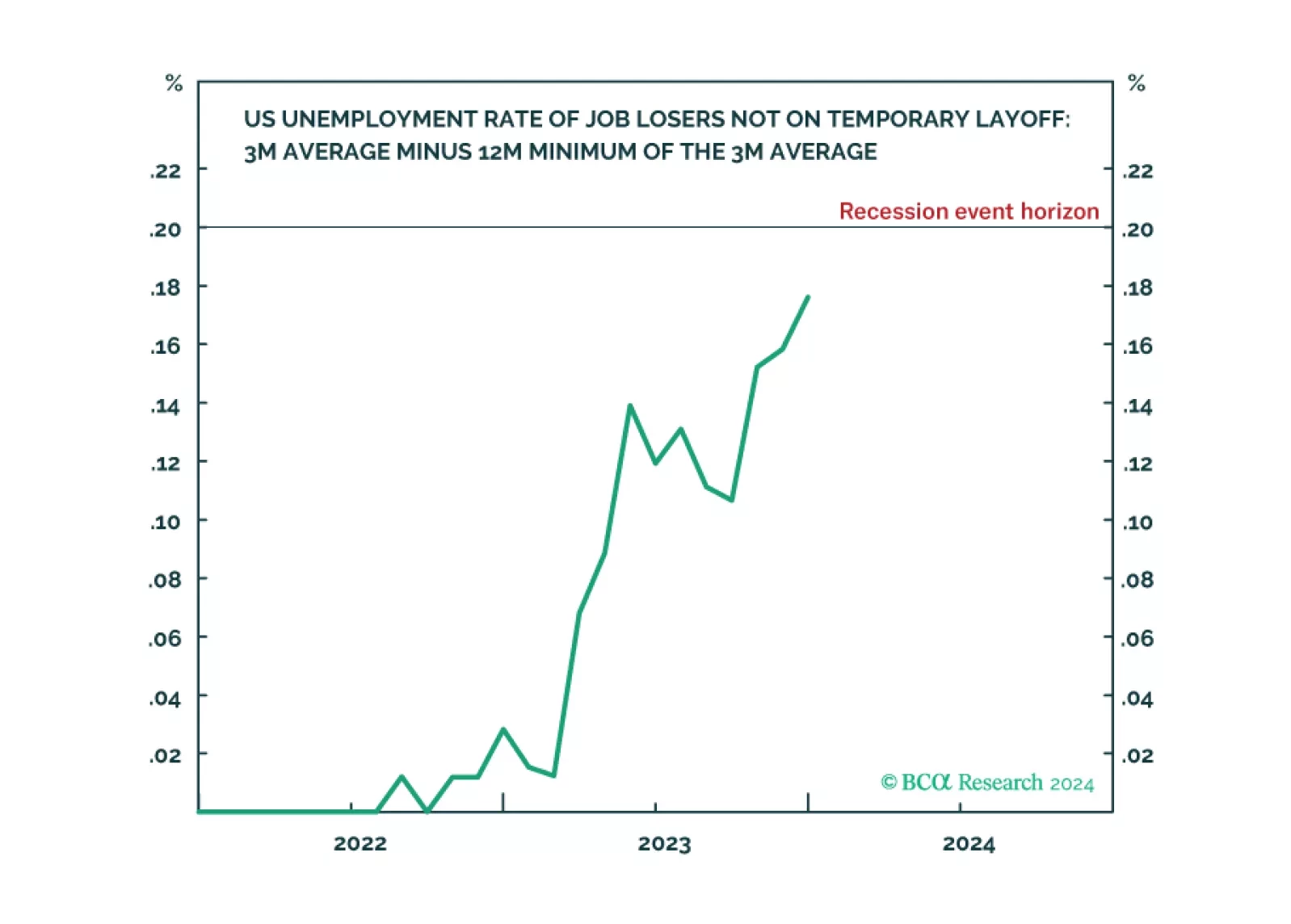

Following today’s US jobs data release, the Joshi rule real-time US recession indicator inched up to 0.18 and is now just a whisker from its recession event-horizon of 0.20.

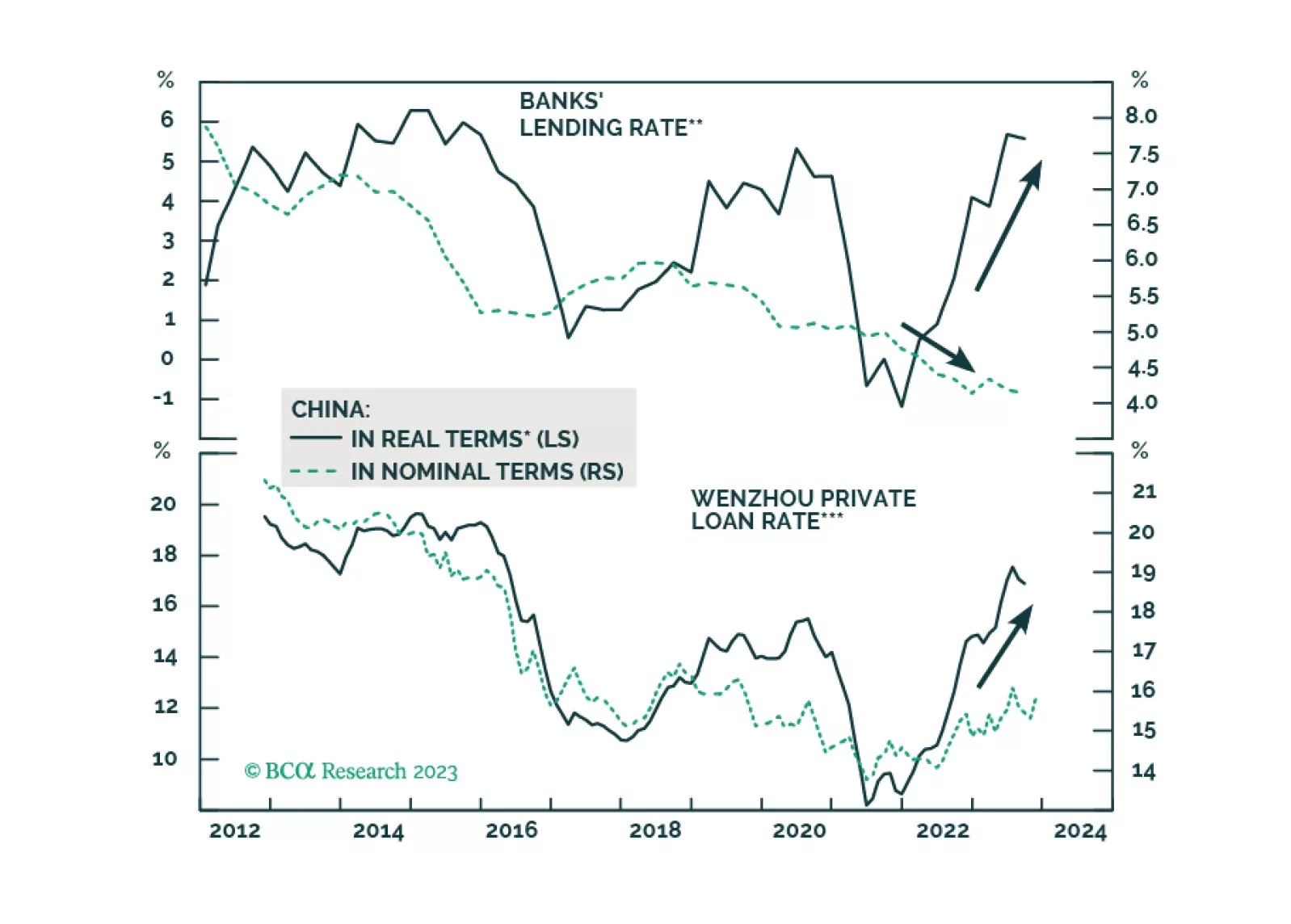

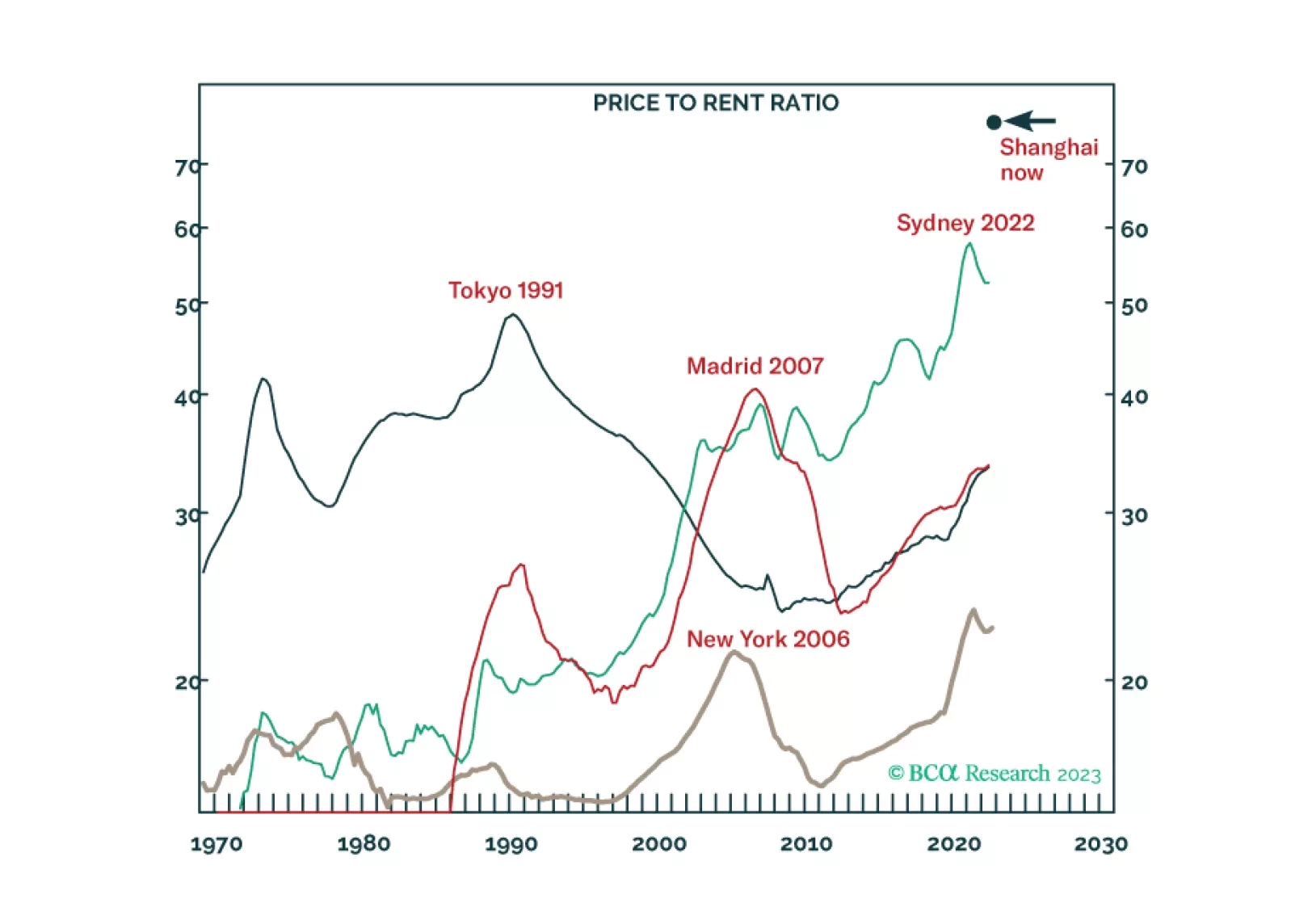

The statement from last week’s Central Economic Work Conference indicates that Chinese authorities are still not considering large-scale stimulus in 2024. Odds are that a full-fledged business cycle recovery in 2024 is unlikely. Chinese share prices remain vulnerable, and strengthening in the RMB will be short-lived.

Explore the eight main themes that will drive the returns of European assets in 2024.

The major question facing EM investors in 2024 is whether or not EM will cross the Rubicon. The path to a soft landing in the US remains elusive. The recent improvement in global manufacturing/trade will likely prove to be a mid-cycle bounce rather than the beginning of a cyclical recovery.

Our US bond team’s thoughts on this afternoon’s FOMC meeting and yesterday’s CPI release.

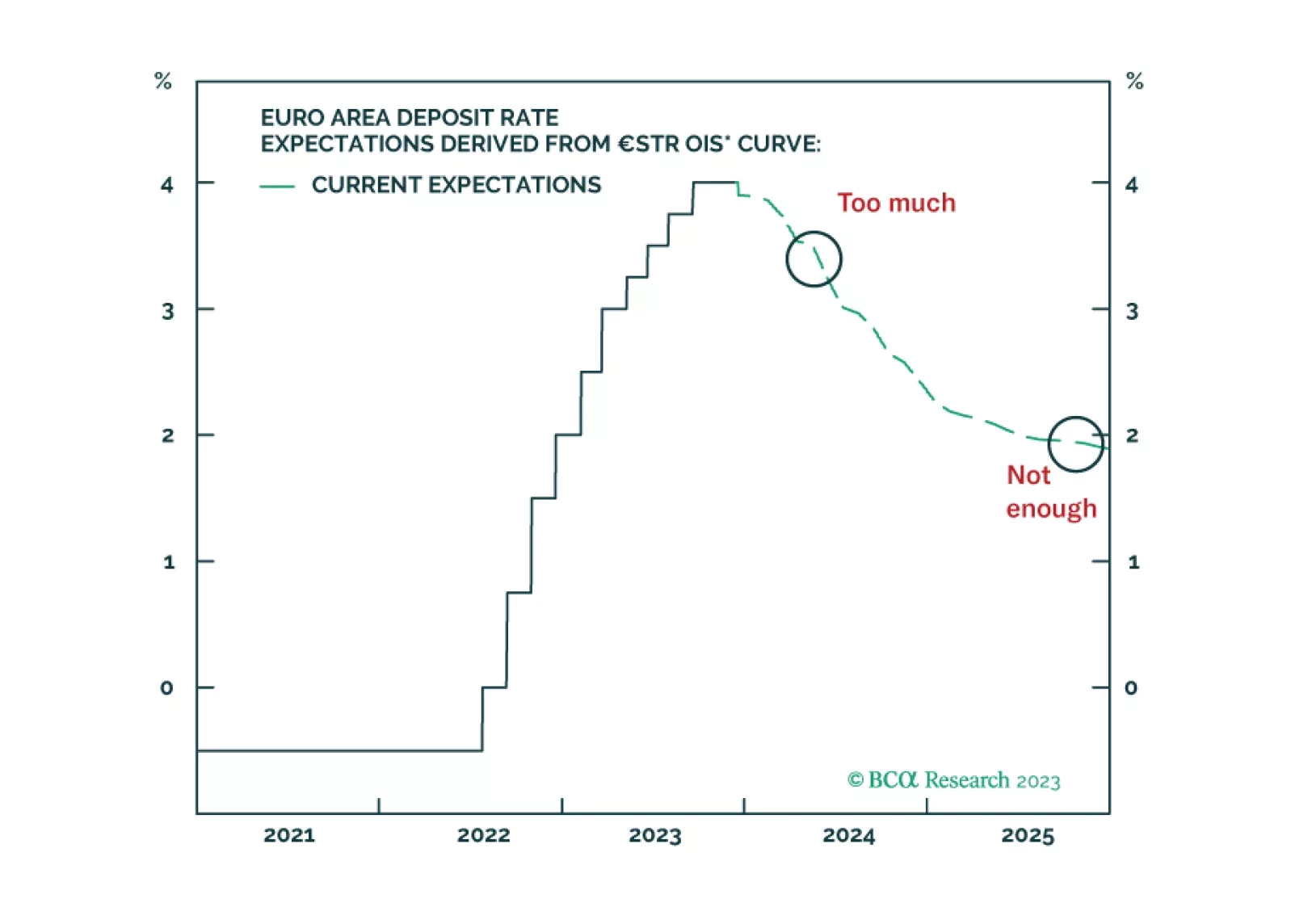

Our 2024 outlook can be encapsulated into just 39 words and three key views. Key view 1: The end of China’s housing boom means the end of the world’s main growth engine. Key view 2: If the Fed and ECB don’t kill the economy, they won’t kill inflation. Key view 3: The AI gold rush will struggle to find any gold. We go through the investment implications for the year ahead.