Inflation Protected

Comments on yesterday’s CPI report and yield moves.

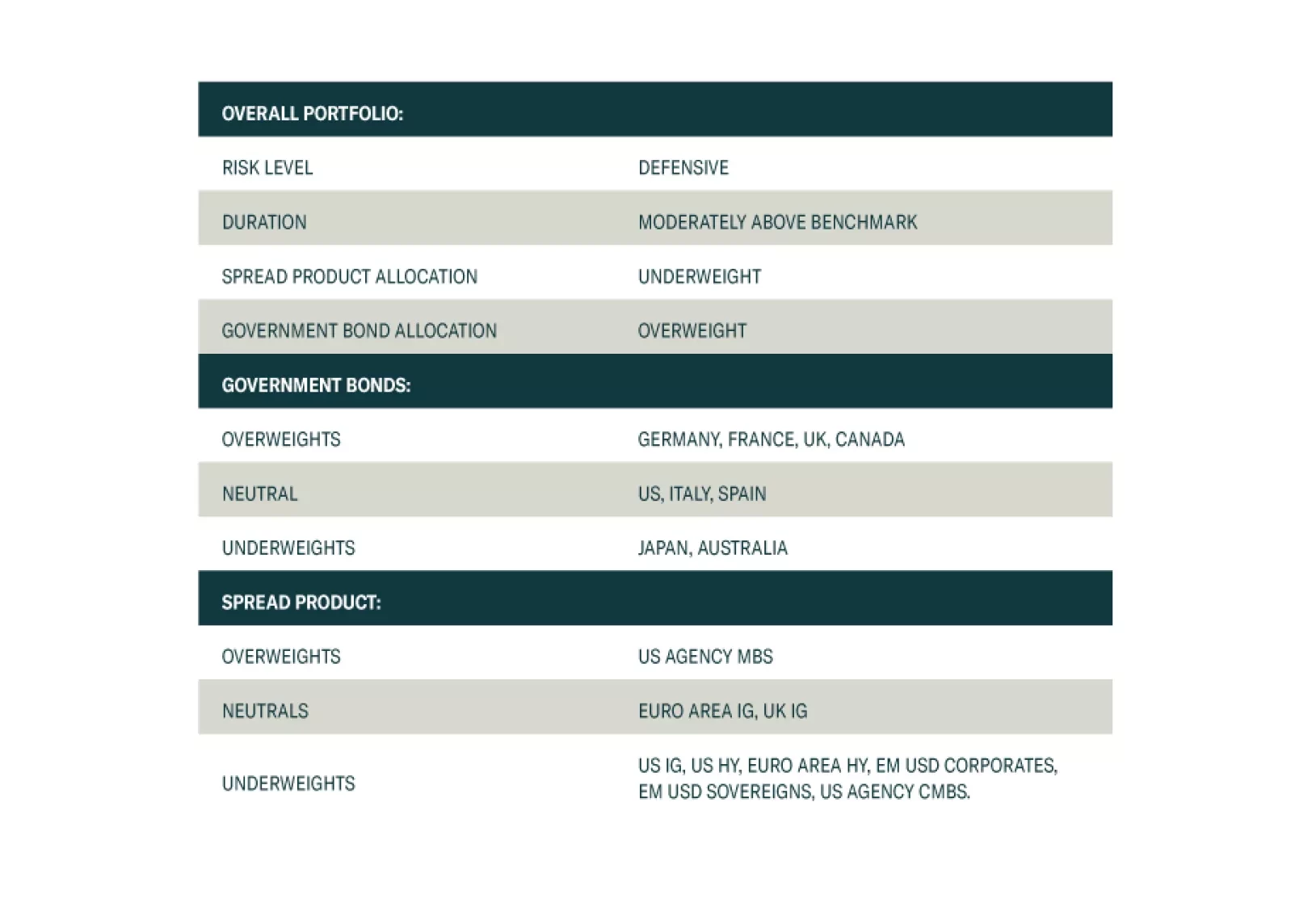

Our Portfolio Allocation Summary for February 2024.

We present the performance review of the Global Fixed Income Strategy Model Bond Portfolio for 2023. We also discuss the outlook for 2024 performance based on our Key Views for the year. The portfolio is positioned to benefit from a year where the global backdrop will be one of weak growth and further declines in inflation, leading central bank to begin cutting interest rates.

Our US fixed income team’s key investment views for 2024.

Our Portfolio Allocation Summary for December 2023.

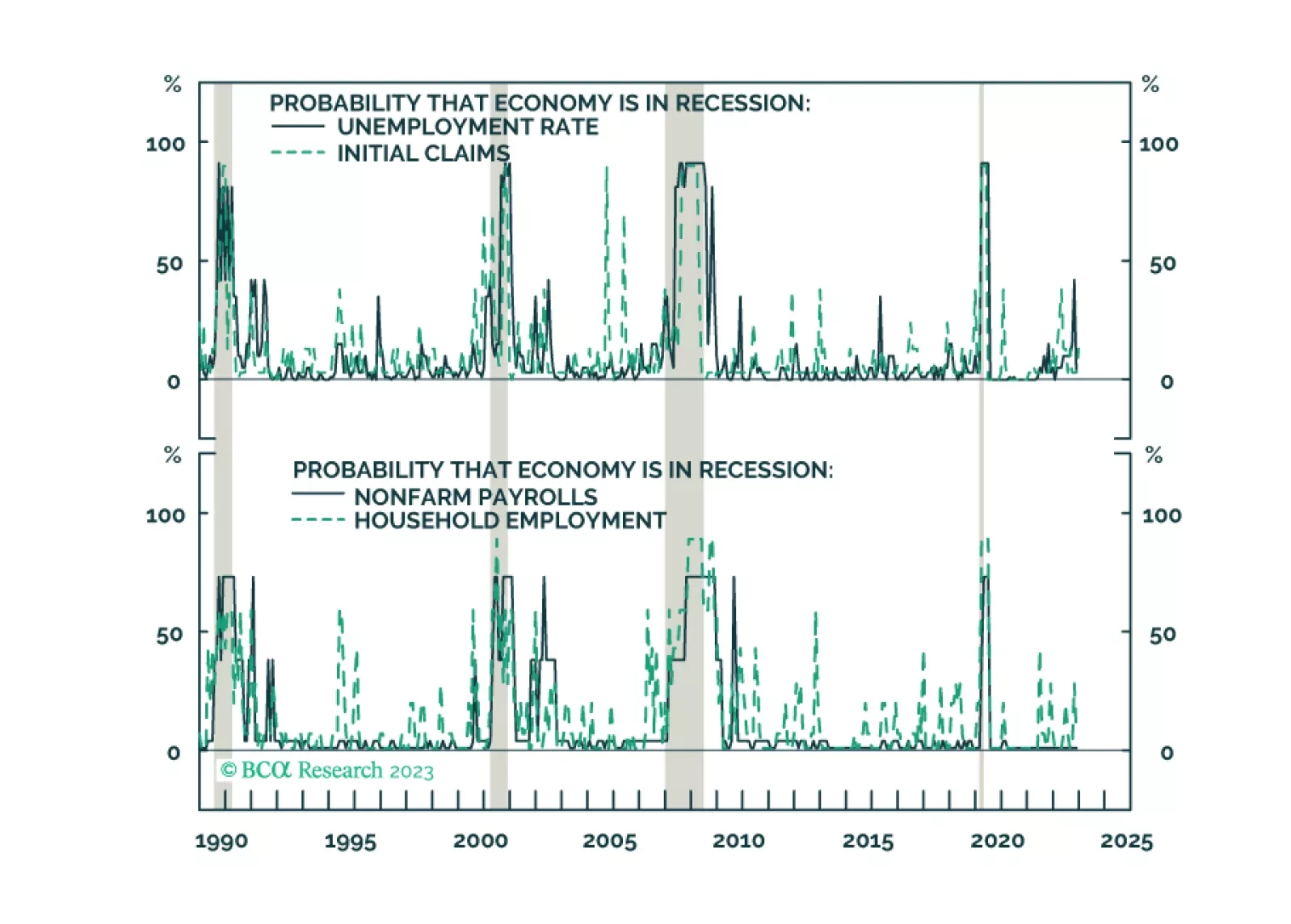

Inflation won’t fall fast enough for the Fed to cut rates preemptively before recession arrives. The risk/rewards balance is unfavorable for risk assets. Stay overweight bonds versus equities.

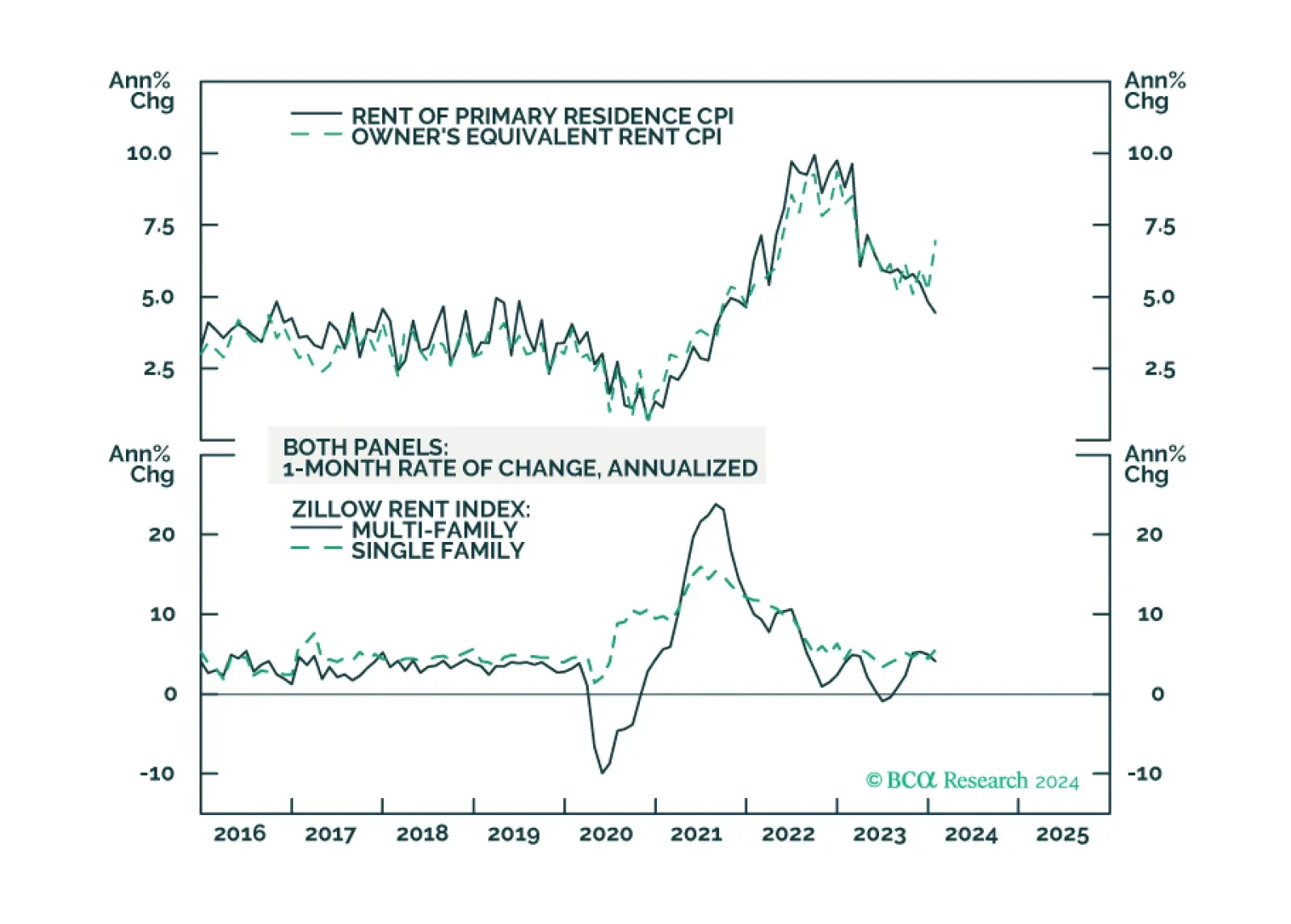

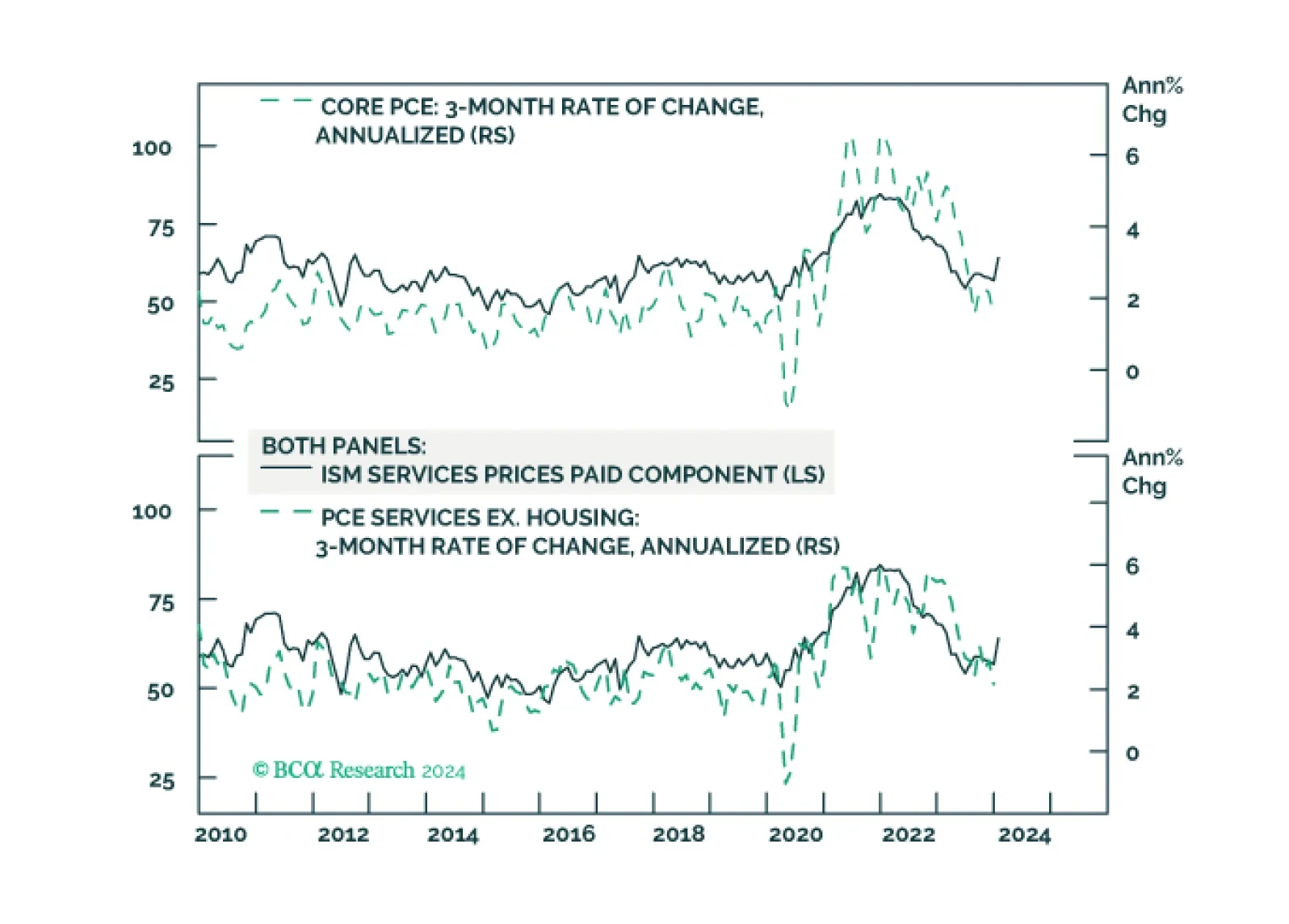

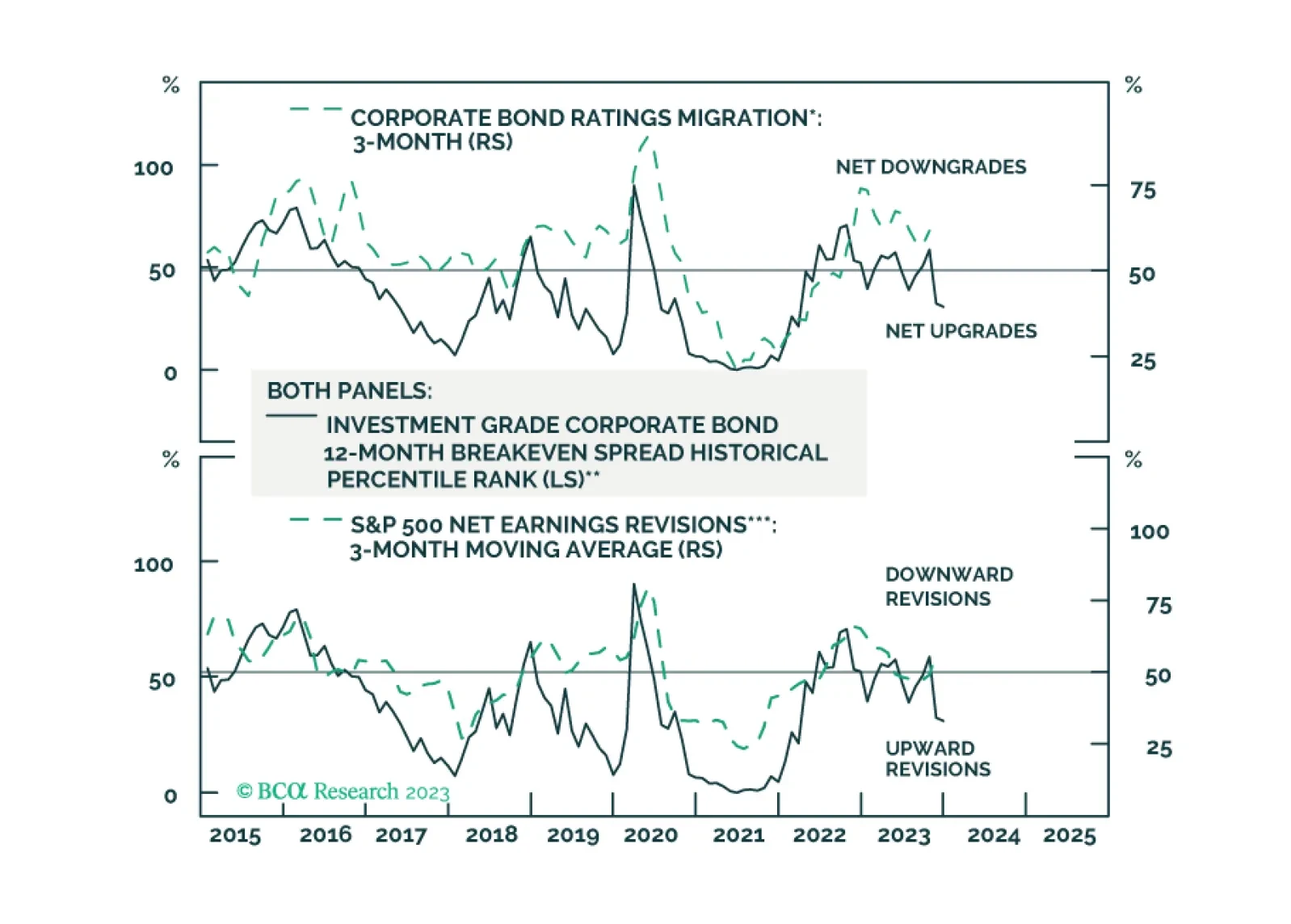

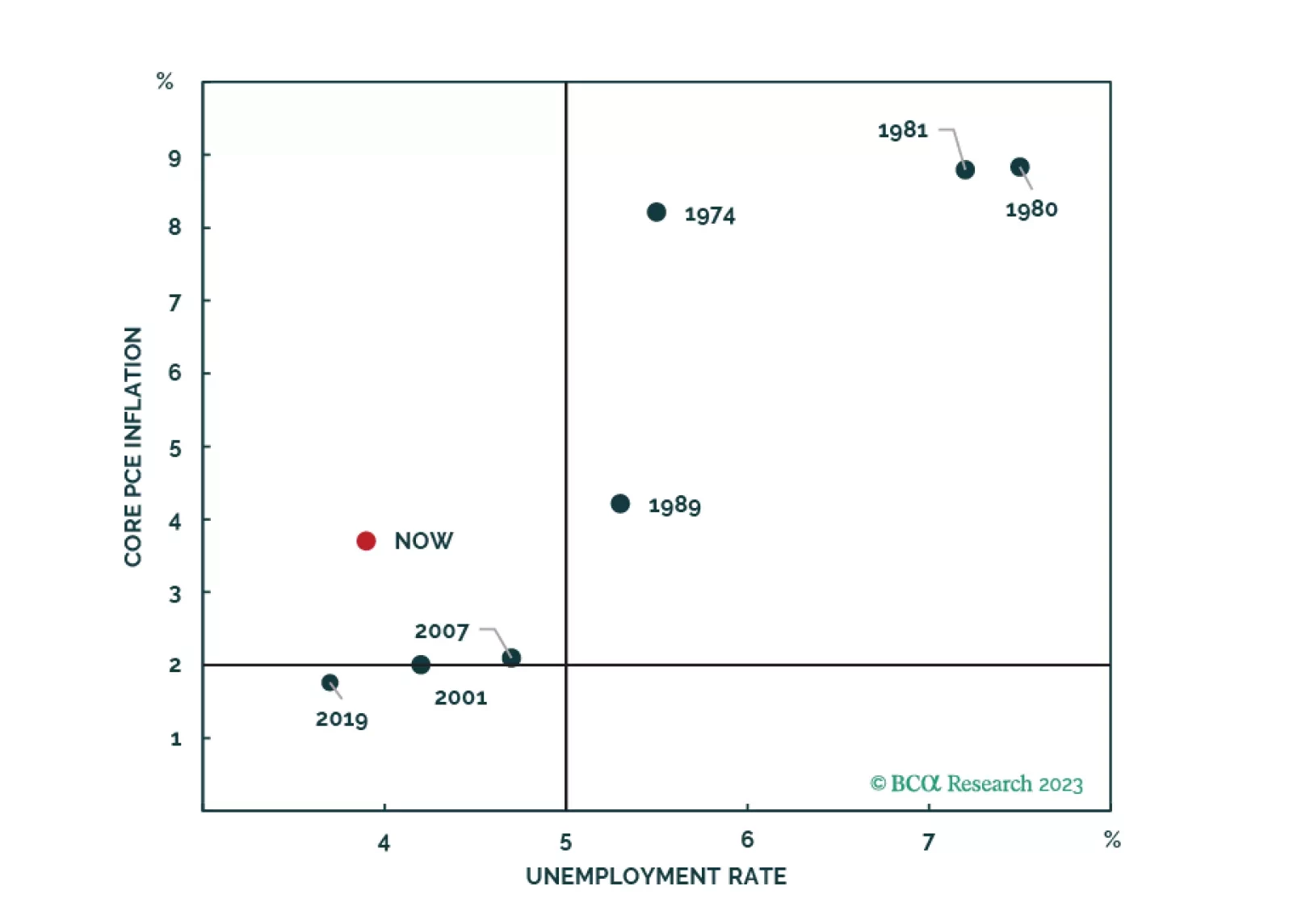

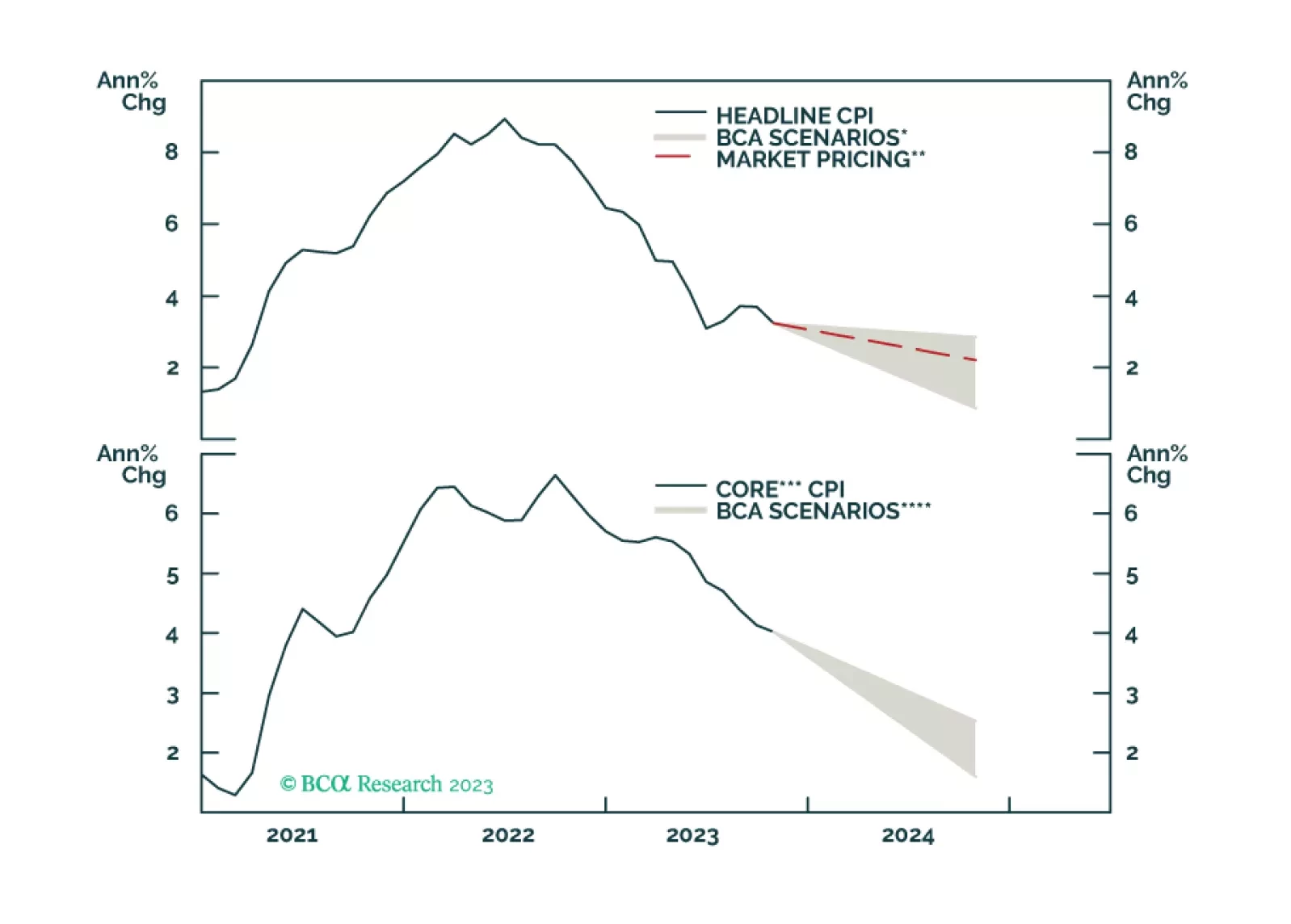

This week’s Special report revisits our TIPS Golden Rule. We provide a 12-month inflation forecast and discuss how it impacts our TIPS view.

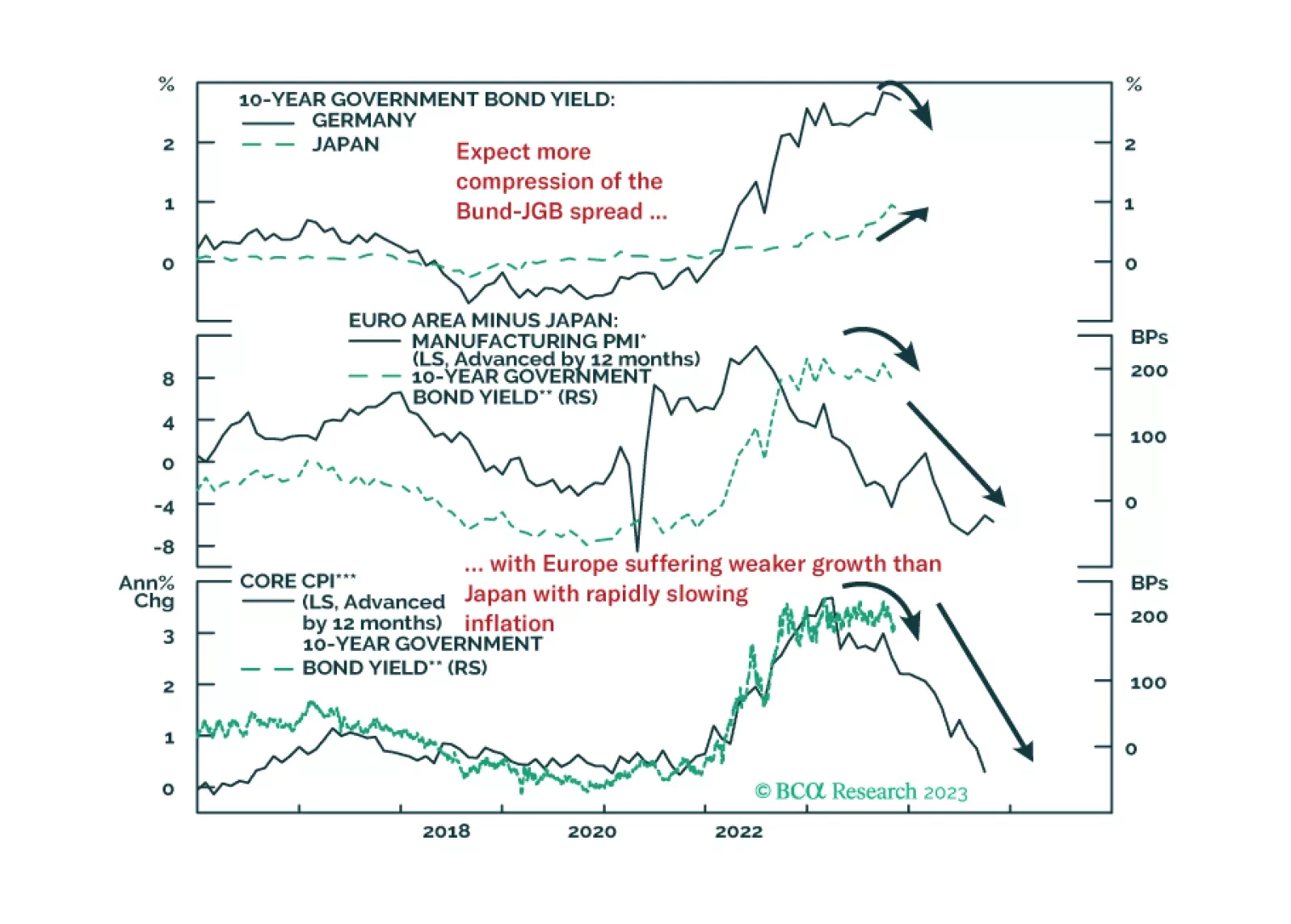

In this Insight, we review the performance and rationale for our current set of tactical fixed income trade recommendations. Our highest conviction positions also happen to be our most successful trades: positioning for a narrowing of the German bund-JGB spread and wider Japanese inflation breakevens.