Iran

I spent the last week in London, speaking to a wide array of BCA Research clients. Throughout the early part of the week, well connected friends and sources in the Middle East warned me that a renewed US attack on Iran was imminent (by Friday, May 22, after the market close, bien sûr). Several clients with hefty AUM’s – and thus an impressive geopolitical consulting budget – in London confirmed that the US attack was all but assured.

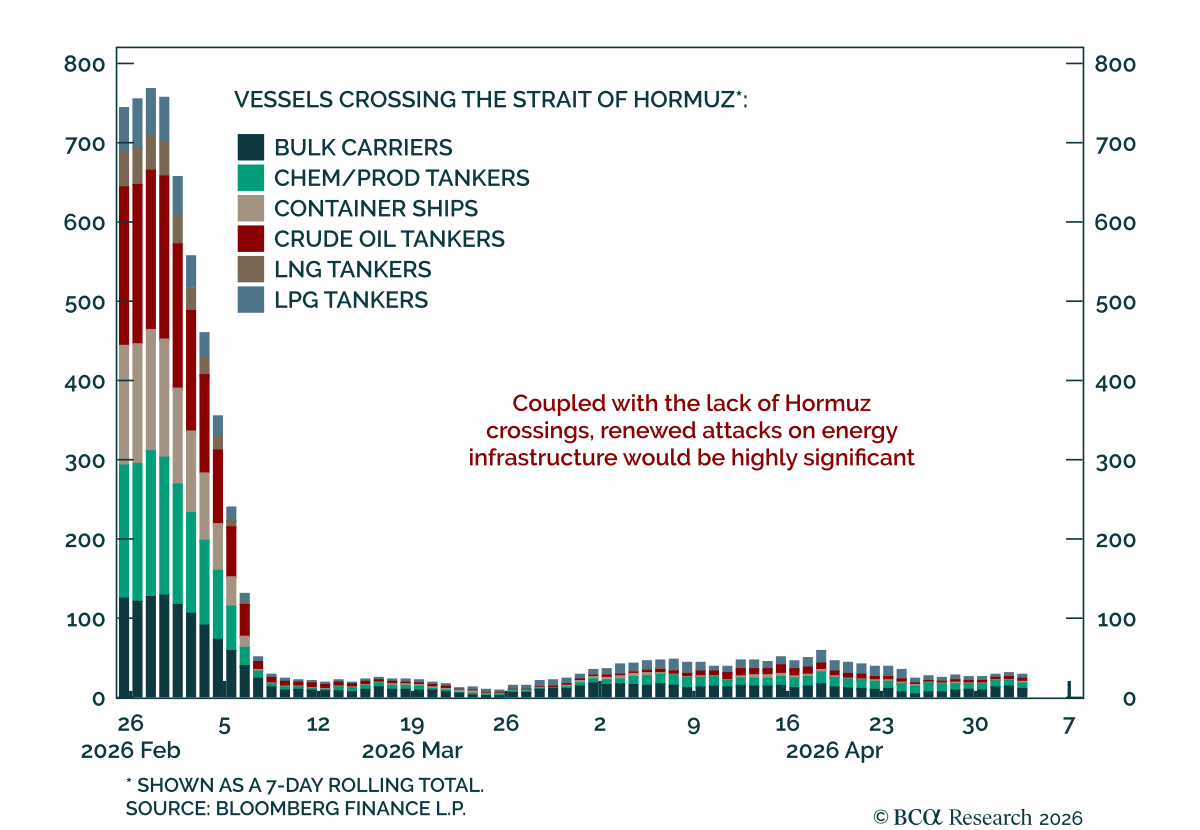

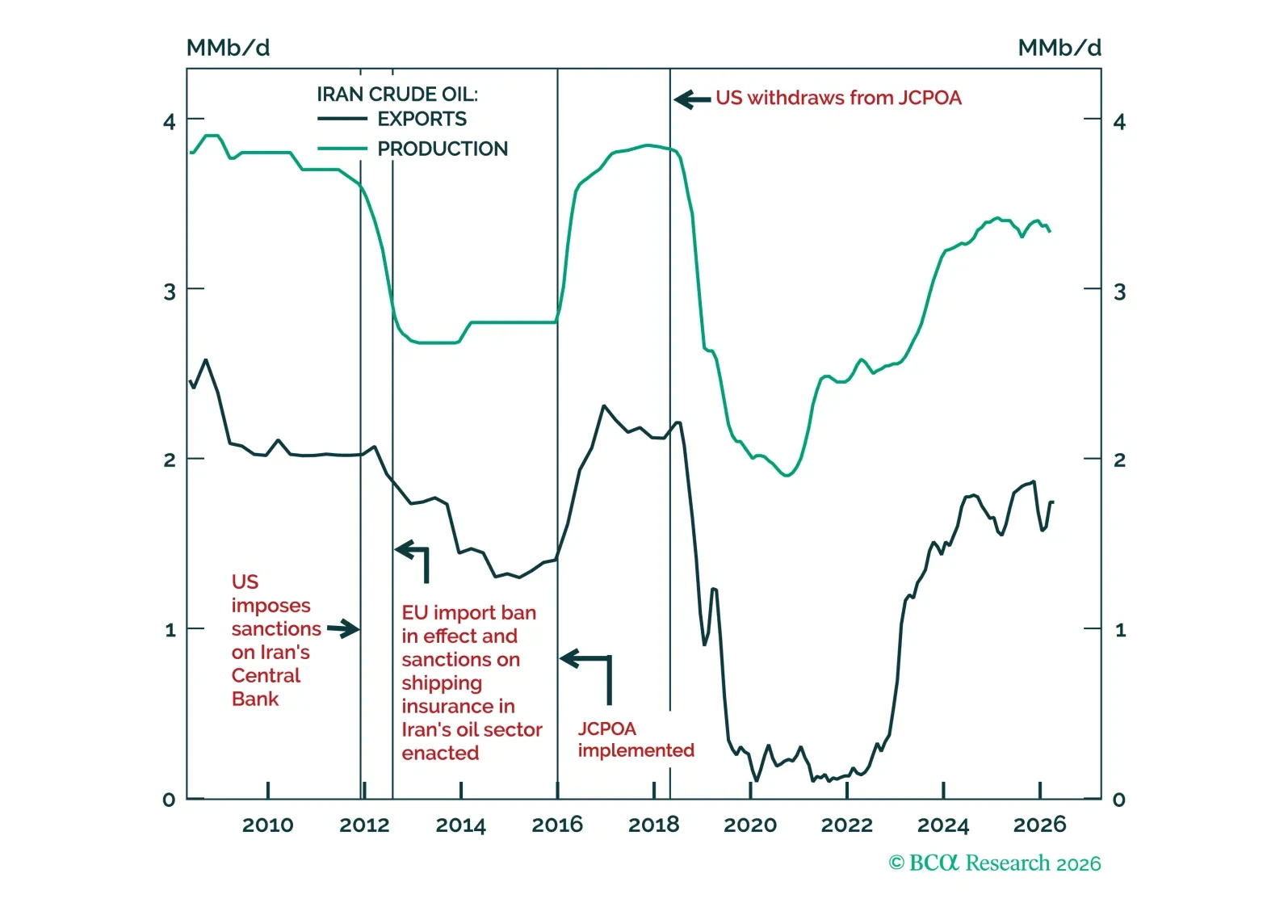

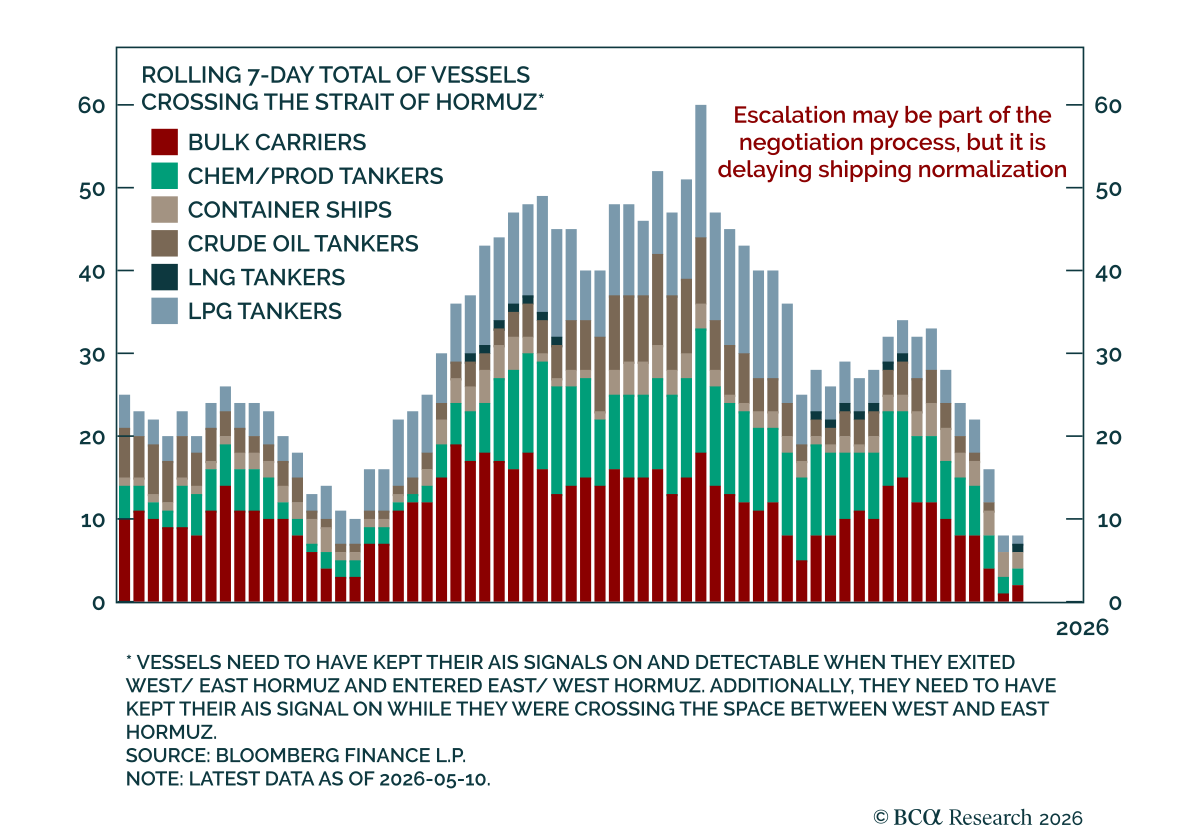

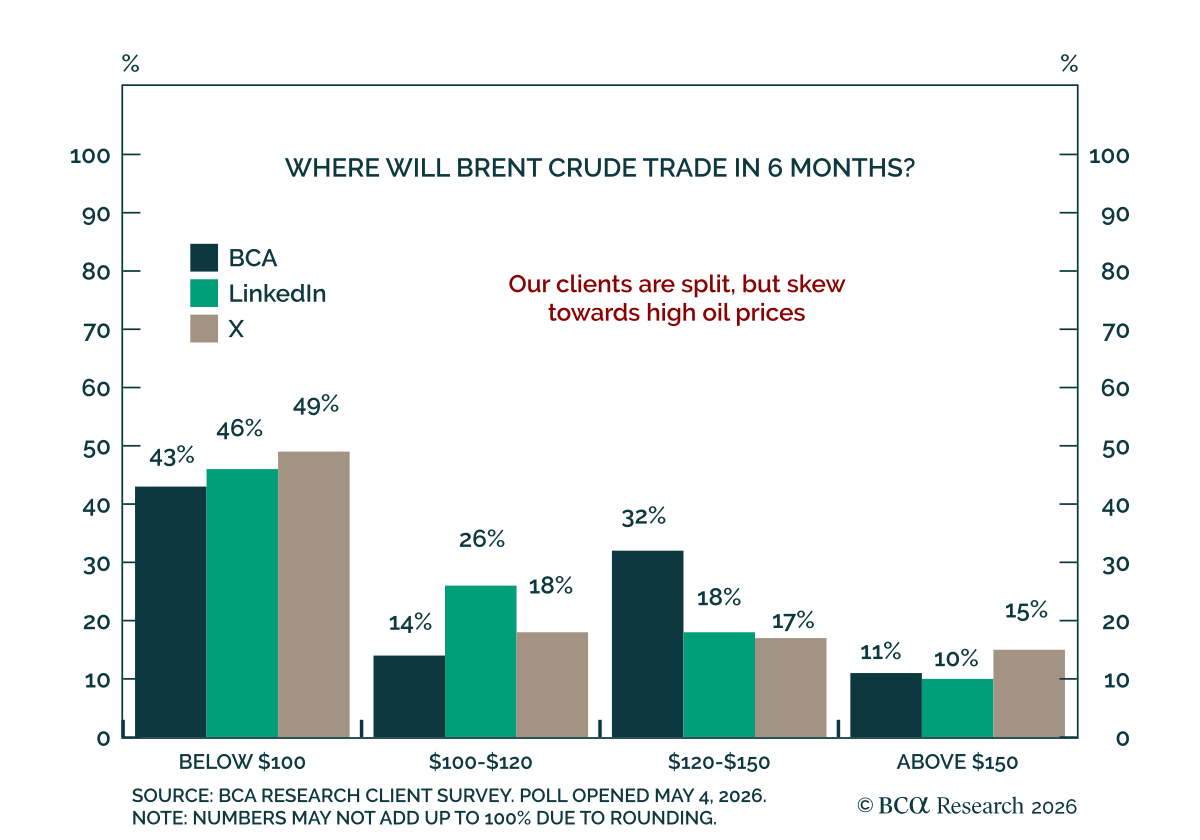

Hopes for an imminent Middle East de-escalation have capped oil prices in recent weeks, but that restraint may soon fade.

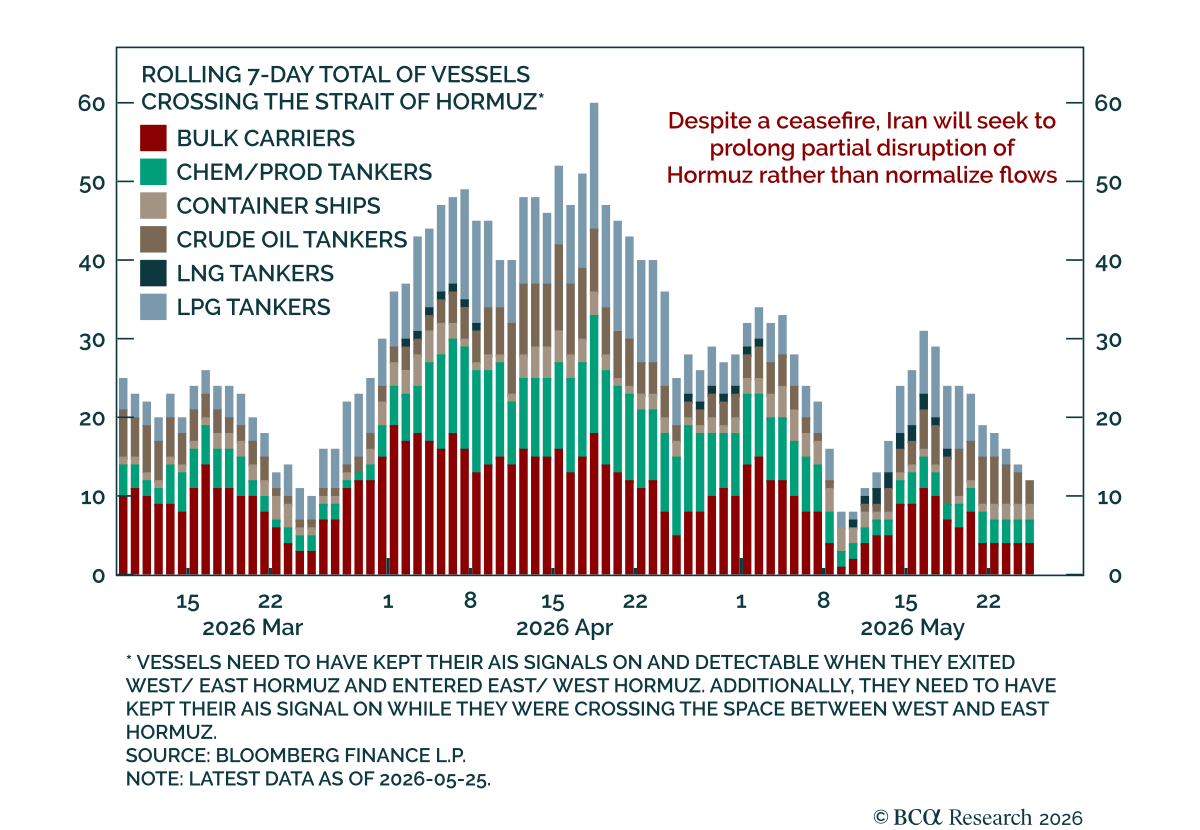

The surprisingly solid ceasefire between Iran, the US, Israel, and GCC countries broke on May 4 with a ballistic missile and drone attack against the UAE. According to reports, UAE defense forces intercepted 12 ballistic missiles, three cruise missiles, and four drones, launched by Iran.