Manufacturing

Chinese activity indicators were mixed in November, reflecting the dynamic of a resilient supply side coupled with weak demand. Industrial production growth was roughly flat at 5.4% y/y vs. 5.3% in October, while retail sales slowed down to 3.0% y/y from…

The post-COVID US recovery was different from previous cycles. Despite an ebullient economy, US consumers and firms have just not been feeling it, as reflected by the depressed signals from so-called soft, survey-based indicators. The main reason behind this…

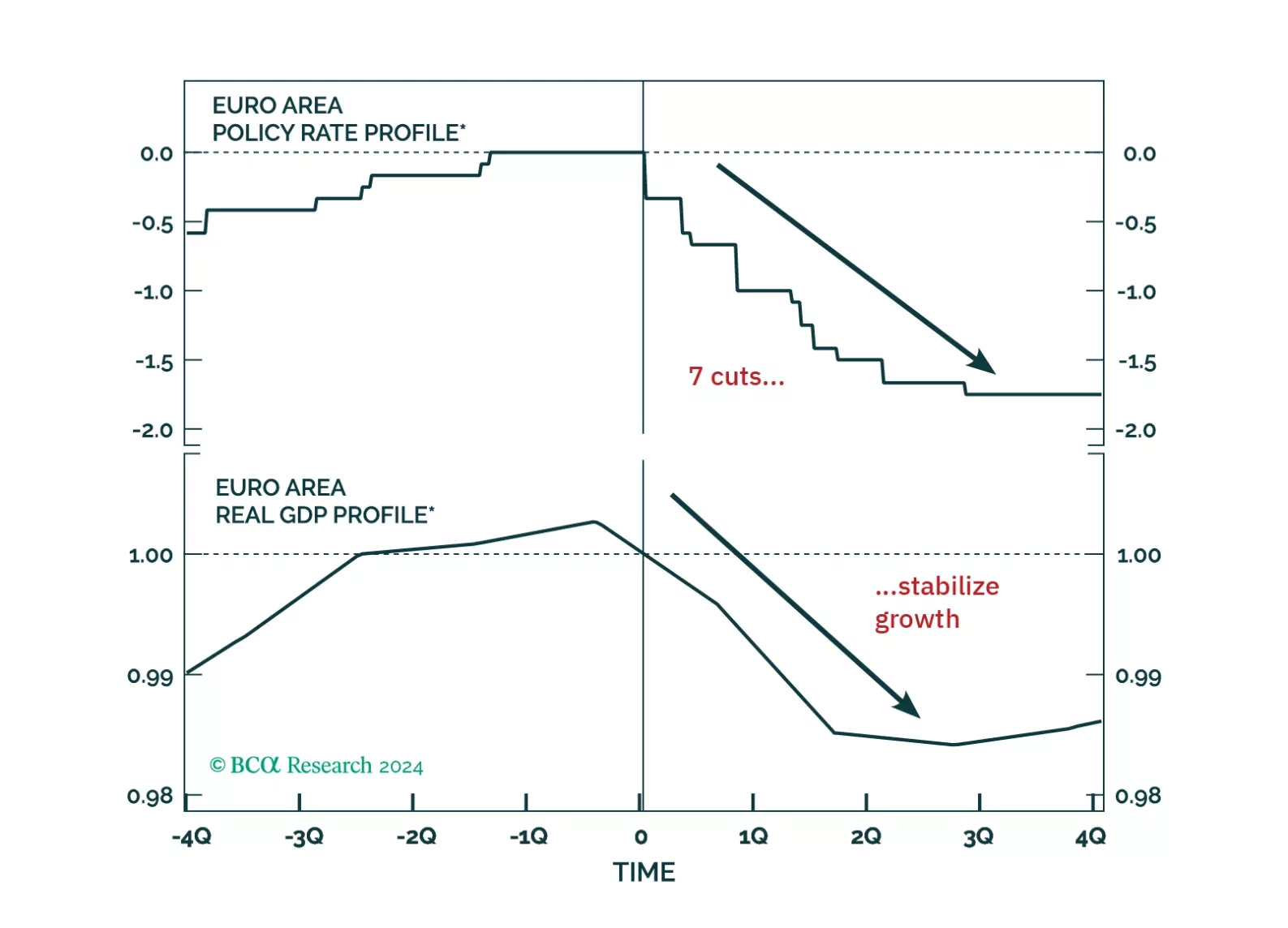

For our last publication of the year, we explore five key themes that will dominate the European macro landscape and markets next year. While the start of 2025 will be challenging for European assets, the latter part will offer some much-needed relief.

The November NFIB Small Business Optimism index beat expectations, jumping to 101.7 from 93.7 in October. Outside of inventory satisfaction, which was flat, all index subcomponents increased, led by measures of expectations. The outlook for general business…

German factory orders decreased less than expected in October, falling 1.5% m/m after rising 7.2% in September. Excluding major orders, which often distort the overall picture, core new orders rose 0.1%, after rising 2.7% a month prior. Despite the…

The November ISM Services PMI missed expectations, declining to 52.1 from 56 in October. All subcomponents declined, with new orders falling from 57.4 to 53.7. Employment also weakened but remains in expansion, while price pressures were roughly unchanged. …

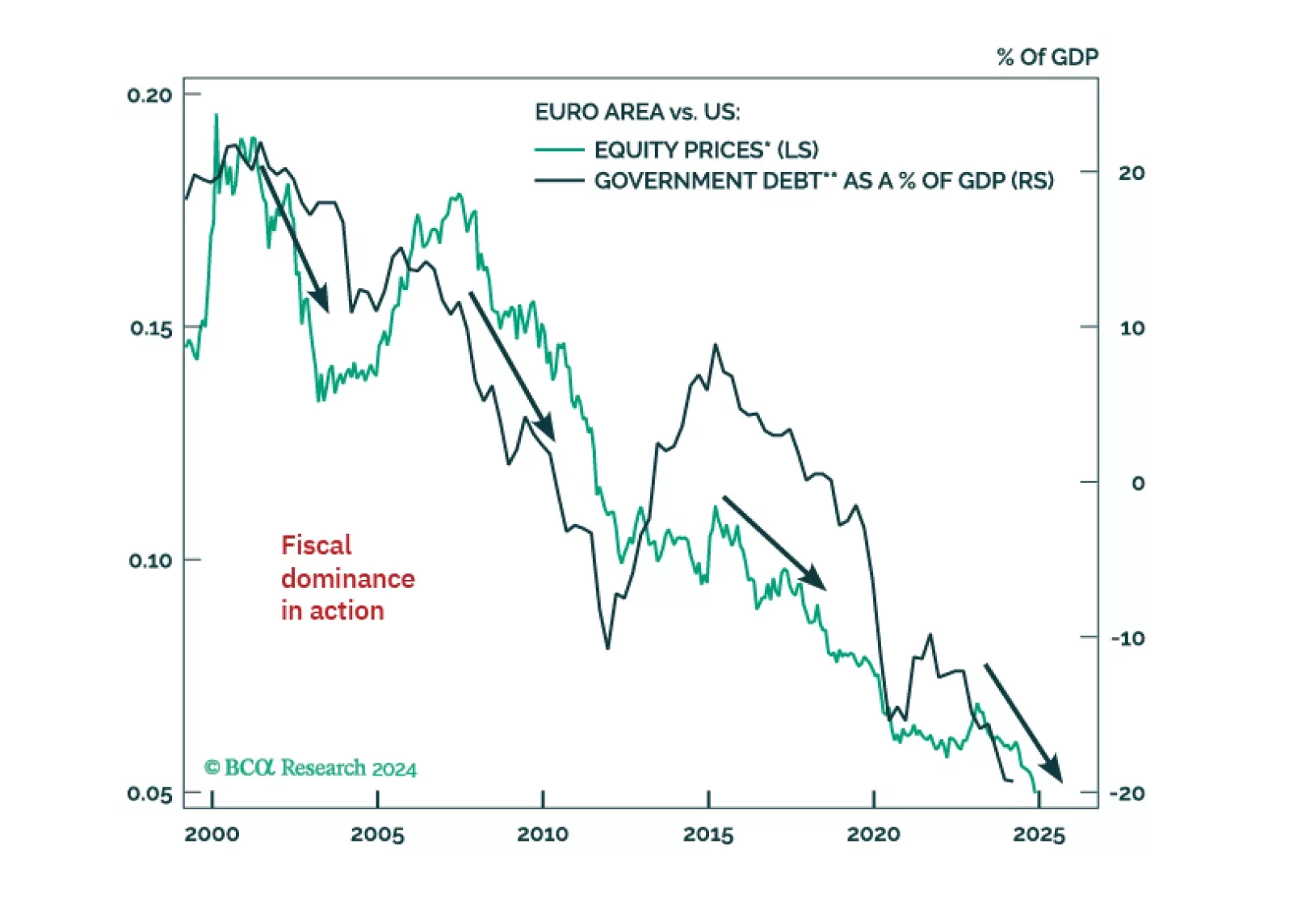

Our European Investment Strategy and GeoMacro Strategy teams published a joint report, digging into the structural challenges behind Europe’s economic underperformance, while pointing out to potential turnaround opportunities. Europe’s prolonged…

The November Caixin services PMI ticked down to 51.5, which along with a rising manufacturing PMI pushed the composite up to 52.3 from 51.9. Components such as new orders and employment also ticked down, and output prices fell to 49.6. Services also weakened…

The Federal Reserve’s Beige Book shows a modestly growing economy imbued with post-election optimism, while highlighting some caution about employment. The latest Beige Book is in line with other sentiment indicators showing modest growth but increased…

Investors have given up on European assets, which now suffer exceptional discounts to US ones. However, tighter US fiscal policy, the end of Europe’s austerity and deleveraging, the LNG Tsunami about to hit European shores, and the global capex fueled by the Impossible Geopolitical Trinity mean that Europe’s time to shine will soon come back.