Manufacturing

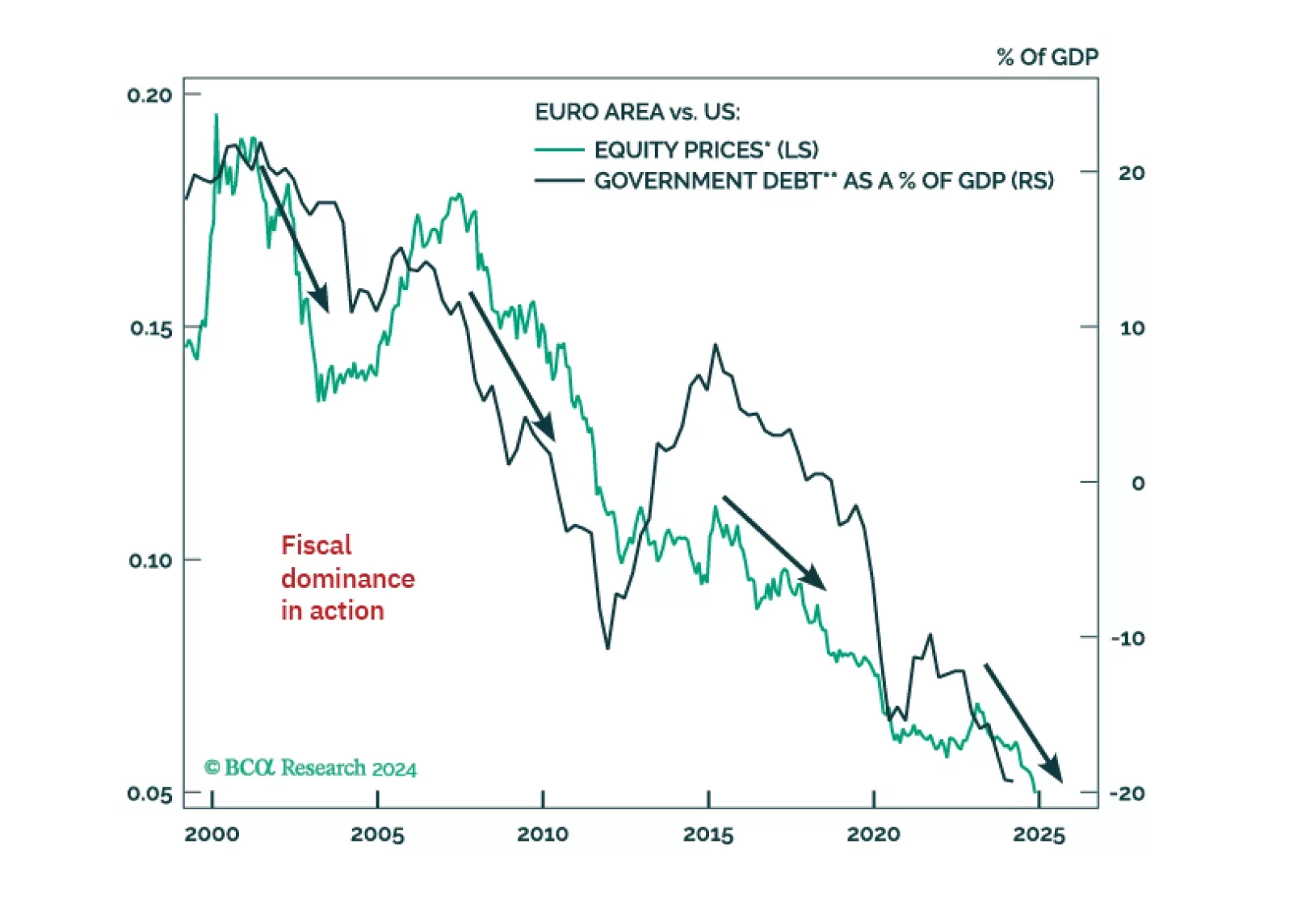

Investors have given up on European assets, which now suffer exceptional discounts to US ones. However, tighter US fiscal policy, the end of Europe’s austerity and deleveraging, the LNG Tsunami about to hit European shores, and the global capex fueled by the Impossible Geopolitical Trinity mean that Europe’s time to shine will soon come back.

China’s November PMIs were mixed, and reflected very low growth. The official composite PMI was unchanged at 50.8, driven by a small uptick in manufacturing to 50.3 and a small downtick of services to 50. The Caixin manufacturing PMI jumped to 51.5 from…

The November ISM Manufacturing index beat expectations, increasing to 48.4 from 46.5 in October. The improvement was partly driven by the new orders component, which increased to 50.4 from 47.1. Price pressures moderated. The underlying details of…

The November Tokyo CPI beat expectations, with headline inflation accelerating to 2.6% y/y from 1.8%. The core (ex. fresh food) and “core core” (ex. fresh food and energy) measures also reaccelerated to 2.2% and 1.9%, respectively. The Tokyo CPI provides…

Consumer confidence came in as expected in November, with The Conference Board’s index rising to 111.7 from 108.7 in October, a level not seen since August 2023. Both the assessment of consumers’ present and future situation drove the increase. The…

Flash PMIs for November extended recent global growth trends. US growth is holding up despite an ailing manufacturing sector, while the rest of the world shows deteriorating weak growth. The US composite beat expectations and accelerated to 55.3 from 54.1…

As talks of a market “meltup” abound, we used last Friday’s edition of our BCA Live & Unfiltered meeting to assess our asset allocation recommendations. Our House View has been underweight equities since March, a recommendation reinforced by two of our…

October retail sales beat expectations, printing 0.4% m/m on top of positive revisions for September. However, the numbers were weaker when adjusting for autos or other volatile components, with the control group declining 0.1% from 0.7% growth in September. …

Chinese activity indicators showed resilience in October, with retail sales jumping from 3.2% to 4.8% y/y. Industrial production growth was roughly unchanged at 5.3% y/y. New and used home prices keep falling, albeit at a slower pace. We would fade this…

Economic expectations for Germany and the Eurozone disappointed, with the November ZEW decreasing to 12.5 from 20.1. The assessment of current conditions also worsened, implying the sentiment rebound from September will not be sustained. The outlook…