Manufacturing

Our colleagues at Global Investment Strategy have shown that postwar US (and global) manufacturing cycles have tended to last 3 years, divided equally between an 18-month up leg and an 18-month down leg. This framework has been a useful gauge for the…

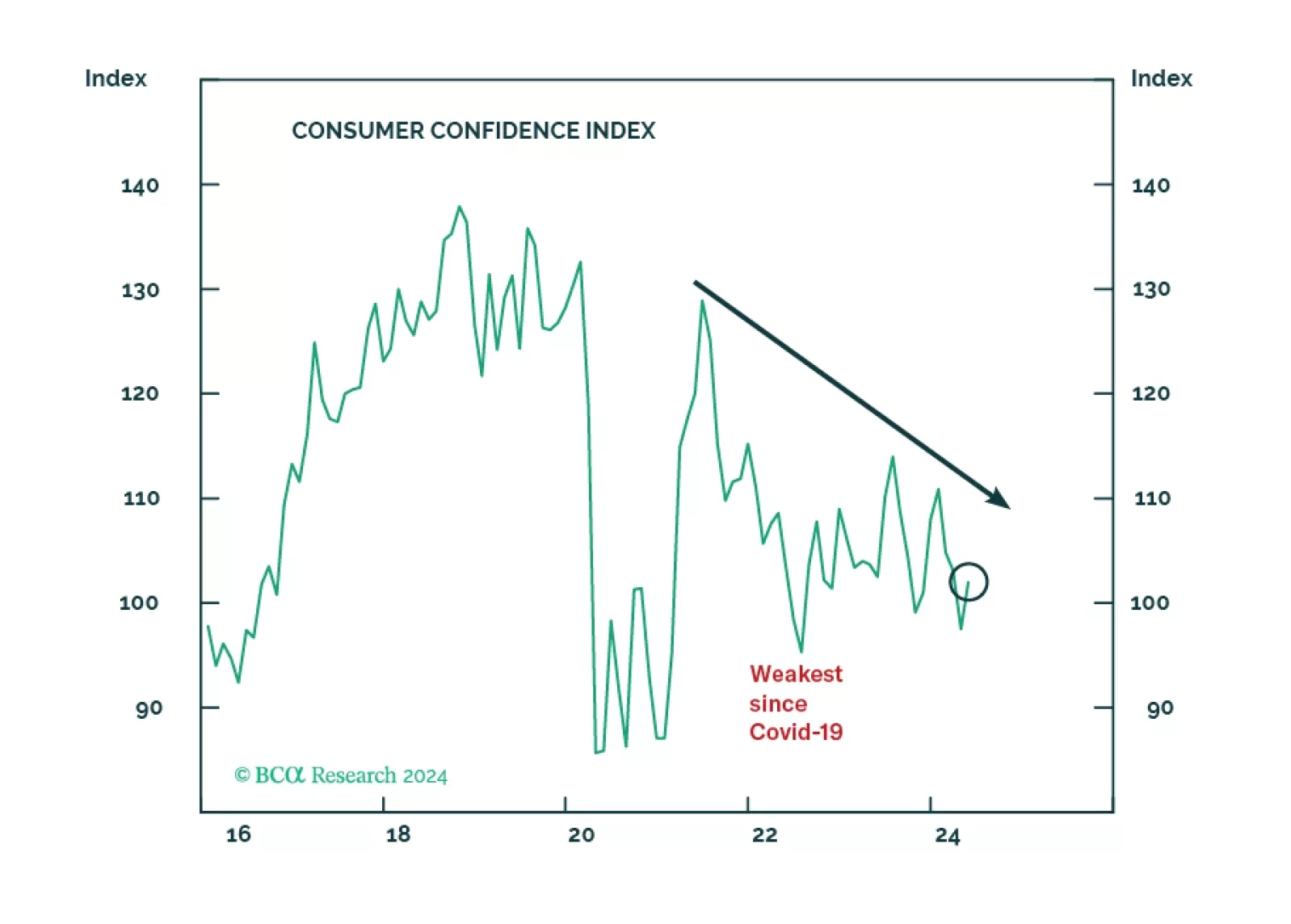

The US economy remains on a path towards a recession, most likely starting in late 2024 or early 2025. For now, investors should maintain a benchmark allocation to equities, but employ a barbell strategy of overweighting defensives and materials.

The silver-to-gold ratio has surged close to 10% this year on the back of silver prices catching up to gold. Silver has returned 22% on a YTD basis, against 12% for gold, 13% for industrial metals and 5% for the broad commodity complex, making the white metal…

The ISM manufacturing PMI declined further in May, from 49.2 to 48.7, thus disappointing expectations of a slower pace of deterioration. Similar to dynamics observed with their Chinese counterparts (see Country Focus), both US manufacturing PMI measures…

The Caixin Chinese manufacturing PMI reached a two-year high in May, expanding at a larger-than-expected rate from 51.4 to 51.7. The Caixin figure thus contrasts with the alternative NBS manufacturing PMI, which unexpectedly contracted in May. The Caixin…

The Swiss KOF Barometer is a composite leading indicator of the Swiss economy. It surprised to the downside in May, coming in at 100.3 from 101.9, below expectation of an acceleration to 102.1. Switzerland’s economy is highly pro-cyclical and…

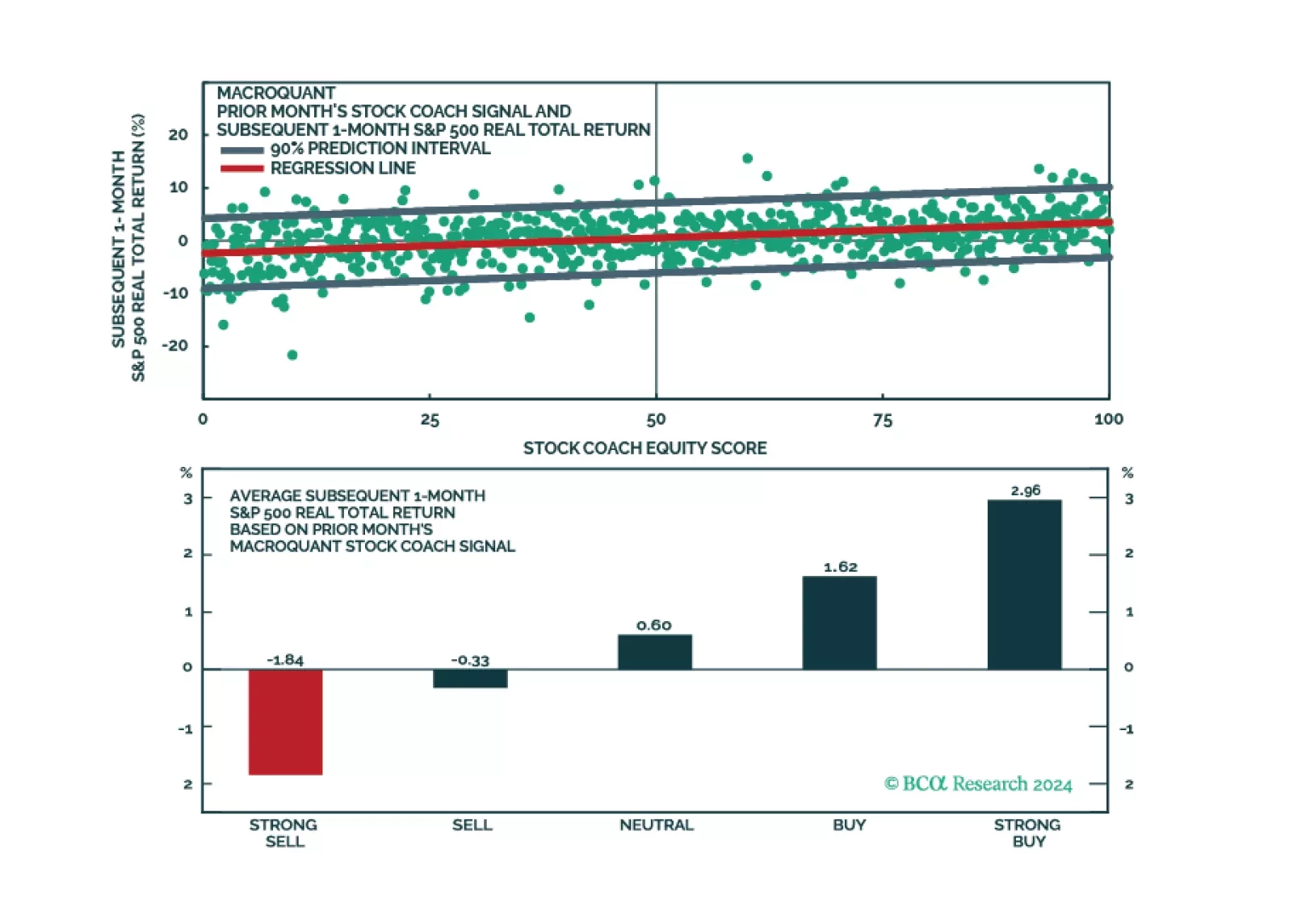

MacroQuant sees significant downside risks to stocks over a 1-to-3 month horizon and suggests increasing allocation to long-term bonds. The model favours defensive equity sectors but is also hedging its bets by overweighting materials.

Chinese PMIs from the National Bureau of Statistics (NBS) disappointed in May. The manufacturing PMI contracted in May (49.5), breaking a two-month expansion streak and disappointing expectations of continued growth. Meanwhile, the services sector PMI…

Favor defensive sectors, low-beta assets, and long-duration bonds until the election uncertainty is lifted one way or another over the next five months.

Chinese industrial profits rose by 4.0% y/y in April, from a 3.5% y/y contraction in March. They grew by 4.3% in the first four months of the year, compared to the same period in 2023. In March, the central government pledged funds to incentivize…