Manufacturing

The stock market of the Eurozone’s largest economy keeps grinding higher with the DAX 40 closing at new highs last week. Since its October low, the index of German blue-chip companies advanced by 20%. Does this rally have legs? On a relative basis,…

China’s NBS PMI release indicates that the Chinese growth is stabilizing at a low level. The composite PMI came in at 50.9 – unchanged from January. The stabilization was led by the non-manufacturing sector though both the manufacturing and non-manufacturing…

According to BCA Research’s Geopolitical Strategy and The Bank Credit Analyst services, trade policy under a second Trump presidency represents the greatest cyclical risk to investors. In 2018, the Trump administration’s trade war with China and several…

The US ISM manufacturing PMI release for February disappointed consensus expectations. The headline index relapsed to 47.8 after climbing to a 15-month high of 49.1 in January, falling below expectations of a continued slowdown in the pace of contraction to…

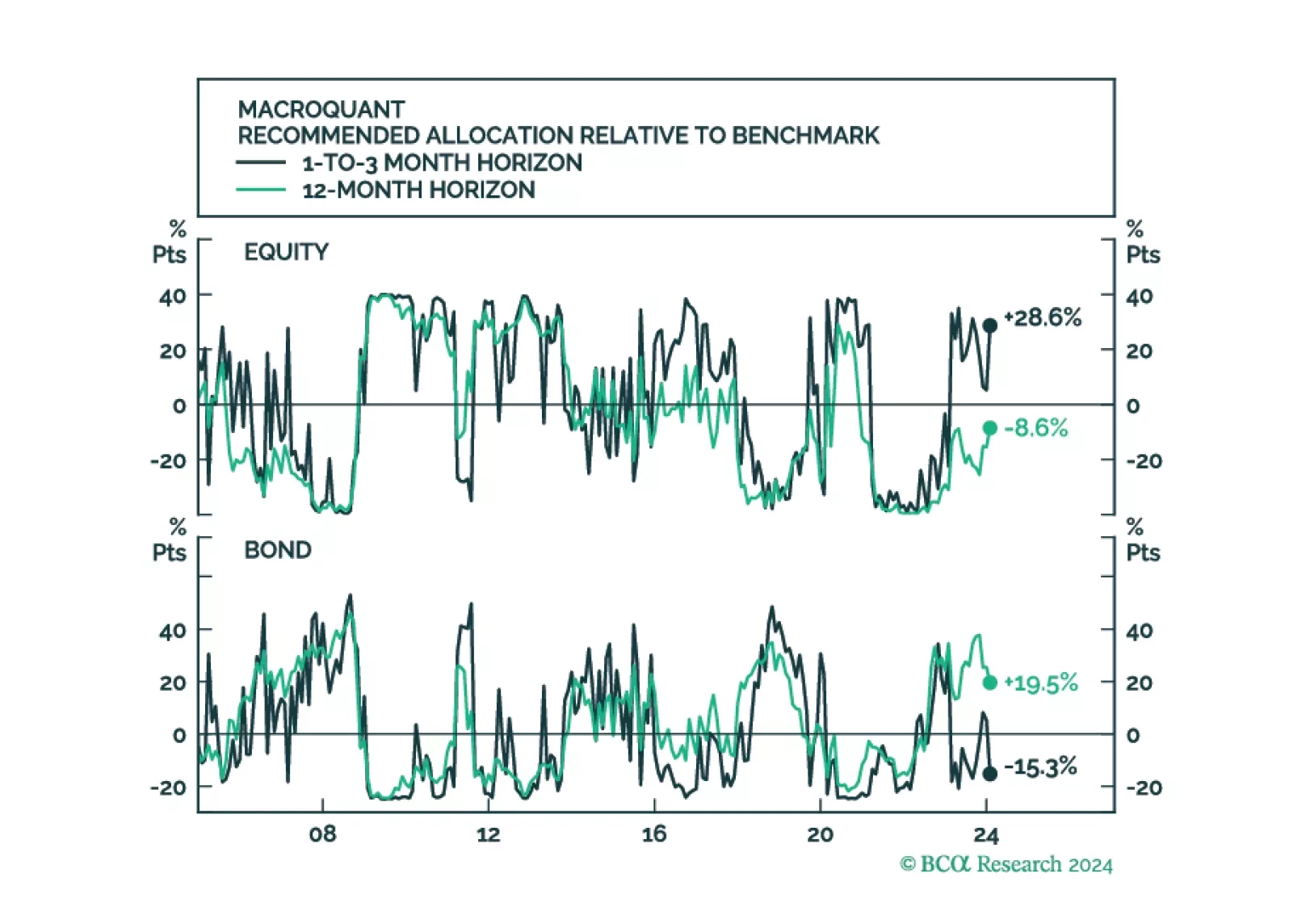

MacroQuant upgraded equities to overweight in February on a tactical short-term (1-to-3 month) horizon, but it continues to see downside risks to stocks on a medium-term (12-month) horizon. Consistent with the model’s relatively somber medium-term growth outlook, it sees more downside for bond yields on a 12-month horizon than on a 1-to-3 month horizon.

On the surface, the latest Taiwanese export orders release delivered a positive signal on the global trade cycle. The 1.9% y/y expansion in January marks a significant improvement from the 16.0% contraction in December. Moreover, a 28% surge in orders from…

On the surface, the US durable goods report delivered a negative surprise on Tuesday. The 6.1% m/m drop in new orders in January fell below expectations and the December figure was revised down to 0.3% m/m from 0.0% m/m. However, the details of the…

Monday’s release of the Dallas Fed’s manufacturing index corroborates the signal from other regional Fed surveys that manufacturing conditions are picking up in the US. The headline Current General Business Activity index jumped from -27.4 to -11.3 in…

According to BCA Research’s European Investment Strategy service, Germany will likely drag the overall Euro Area into contraction, even if, individually, other countries manage to avoid a recession. This slightly better economic outcome will nonetheless…

Germany’s IFO Business Climate index ticked up 0.3 points to 85.5 in February, in line with consensus estimates. Expectations for the next 6 months explain the improvement in sentiment among German companies (up 0.6 points to 84.1), while their assessment of…