Manufacturing

Preliminary PMI estimates suggest that service sector activity is expanding across DM economies in February. Most notably, services PMIs are back at or above 50 in Australia and the Eurozone from previously contracting levels. Meanwhile, the services sectors…

Democrats remain favored for reelection in 2024, which implies gridlock and policy status quo in 2025. That is not negative for stocks in the near term. However, economic, political, and geopolitical risks will escalate from here, causing volatility.

Much of the focus of investors concerned about lingering price pressures has been on services prices. There is good reason for that. Even though core CPI inflation remains relatively elevated at 3.9% y/y in January, core goods prices fell by 0.3% y/y and are…

The hotter-than-anticipated US PPI report for January prompted a selloff in Treasuries on Friday. The monthly and annual changes in both the headline as well as the core measures of final demand PPI came in above expectations. Core PPI’s 0.5% m/m increase…

The Global Manufacturing PMI clocked in at 50 in January – exactly on the boom-bust line. The index has been on a general uptrend since mid-2023 with the January figure marking the first non-contractionary reading since August 2022. The headline index…

The first two regional fed manufacturing surveys for February delivered strong upside surprises. The New York Fed’s Empire Index surged from -43.7 to -2.4, unwinding its January slump. Similarly, the Philly Fed current activity index jumped by 15.8 points to…

The German economy was a laggard at the end of last year, posting a 0.3% q/q real GDP contraction in Q4 2023 while the broader Eurozone economy stagnated. Importantly, while economists have been revising up their 2024 forecasts for the US economy, they have…

Over the past few months we have been highlighting that there are some budding signs of a recovery in global manufacturing activity. Most notably, the new orders-to-inventories ratio of Sweden’s manufacturing PMI has been rebounding. To the extent that Sweden…

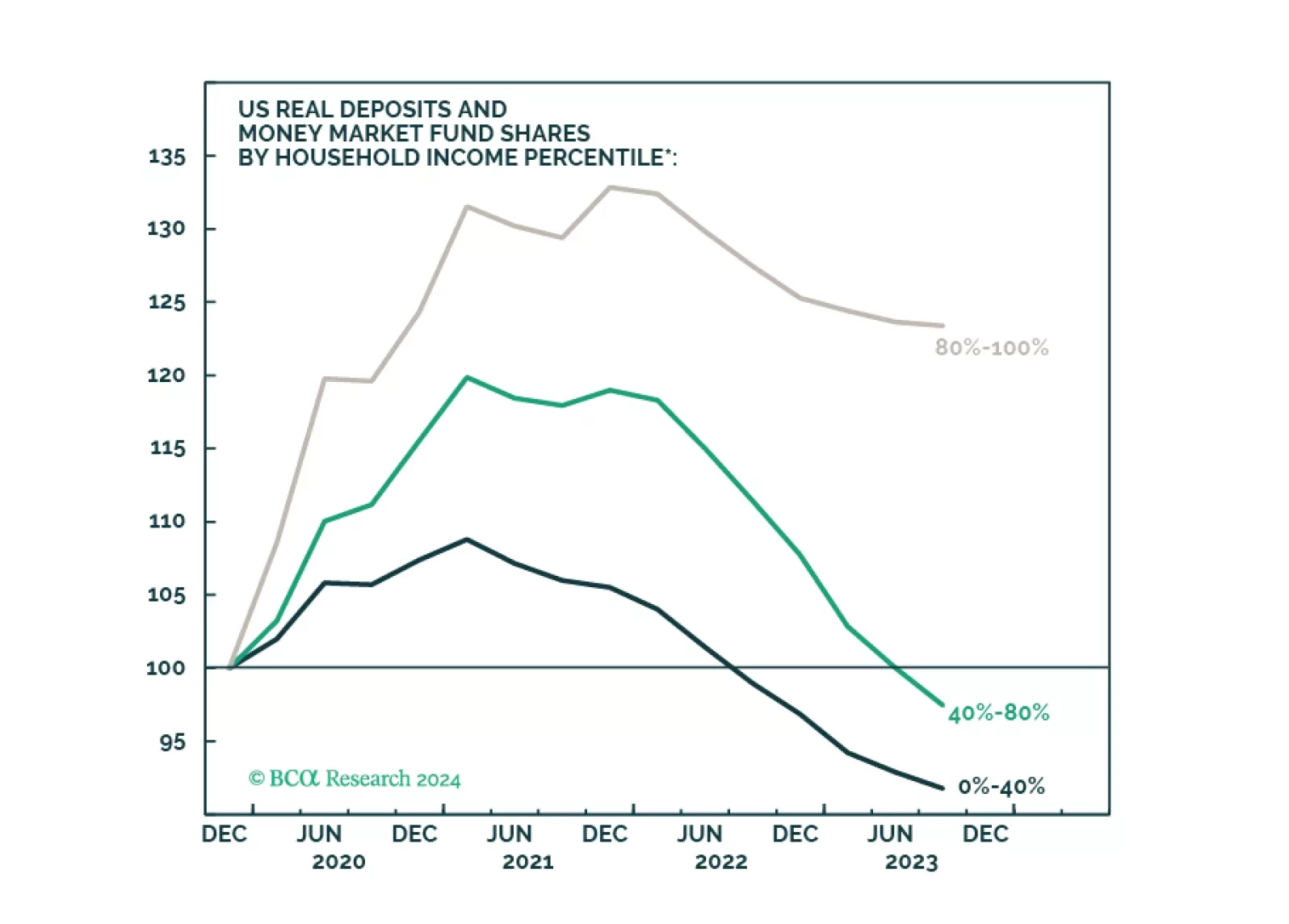

Easier financial conditions, rising home prices, rebounding consumer sentiment, and a stabilization in manufacturing activity all augur well for near-term US growth prospects. An unsustainably low savings rate is a key risk to the US economic outlook. Our revised forecast is centered on a recession starting in late 2024 or early 2025.

German factory orders delivered a positive surprise on Tuesday, unexpectedly increasing on both a monthly and annual basis. The 8.9% m/m increase in December came in well above consensus estimates of a 0.2% m/m decline. This translated to a 2.7% y/y rise,…