Manufacturing

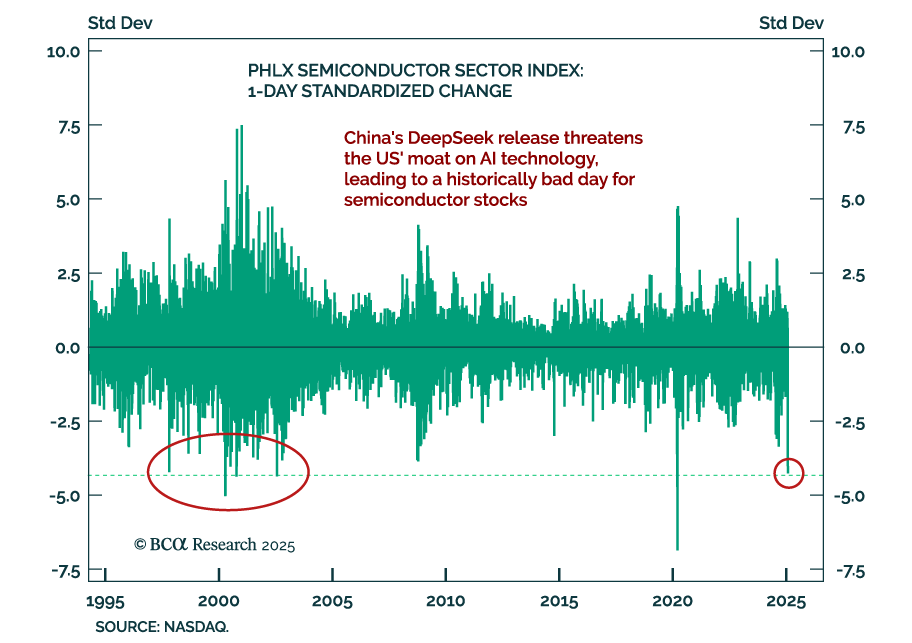

News of a cheaper Chinese-developed AI model sent a tremor through markets, with a selloff in the S&P 500, NASDAQ, and leading tech names associated with AI. The narrative on Monday was that the eye-watering sums spent on AI capex by mega-cap tech…

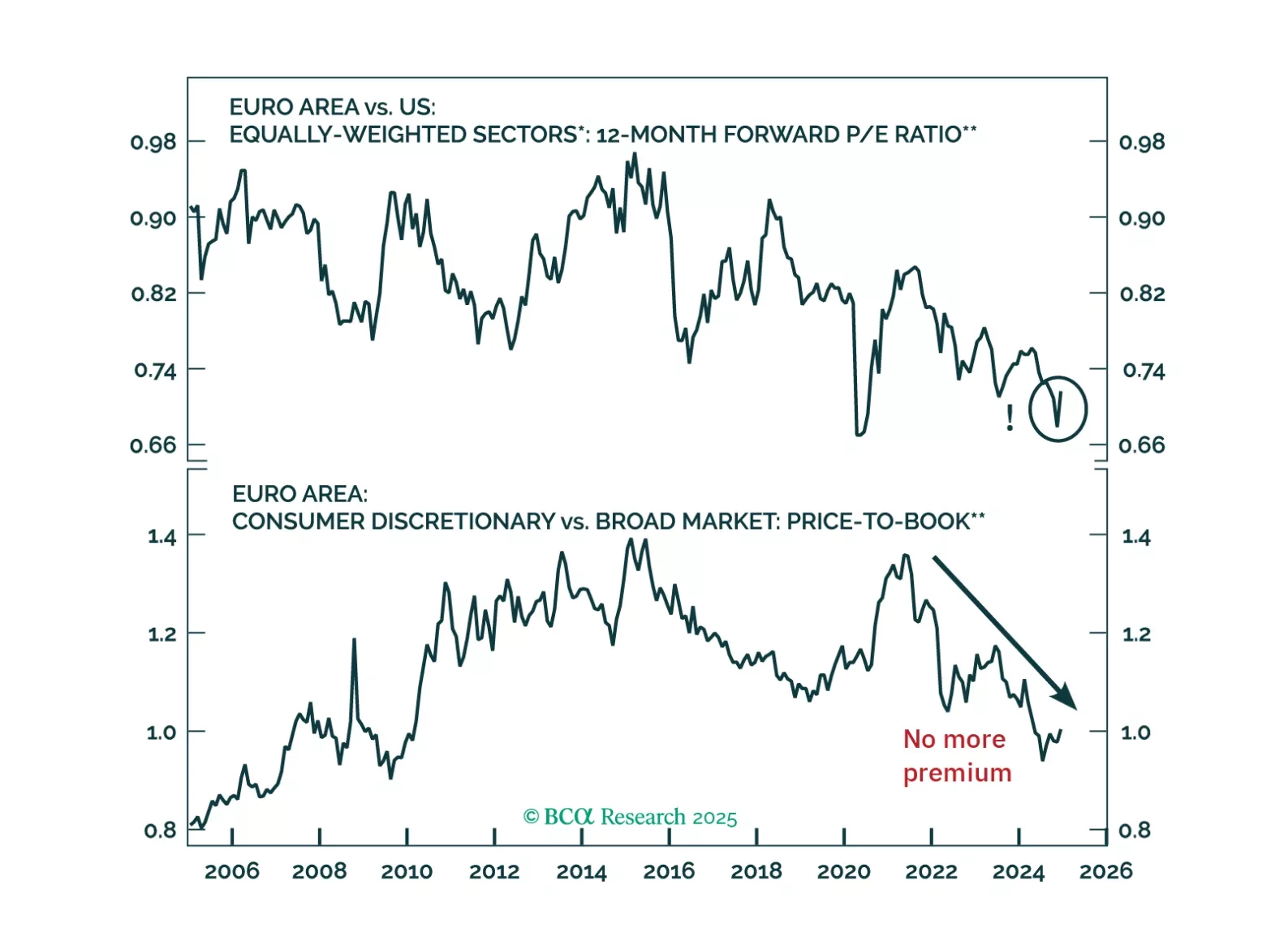

Global risk assets are engulfed in a wave of euphoria, which is pulling Europe higher along the way. However, risks still abound. How should investors adjust their allocation to Europe under these highly uncertain conditions?

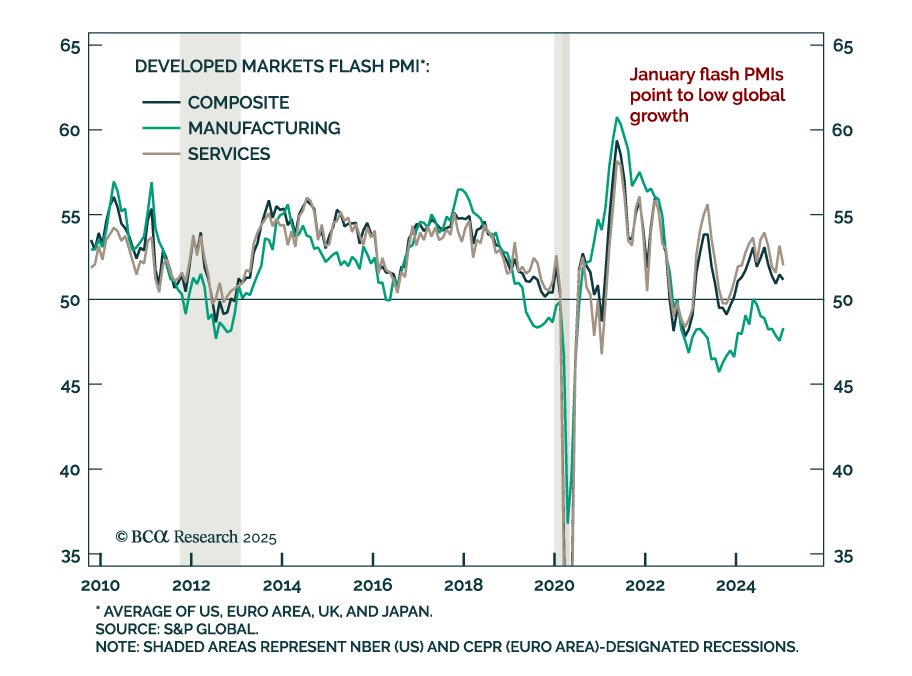

January’s flash PMIs for the major developed markets showed that manufacturing contracted at a slower pace and service activity continues to display significant regional differences. Moreover, the performance gap between the US and its DM peers…

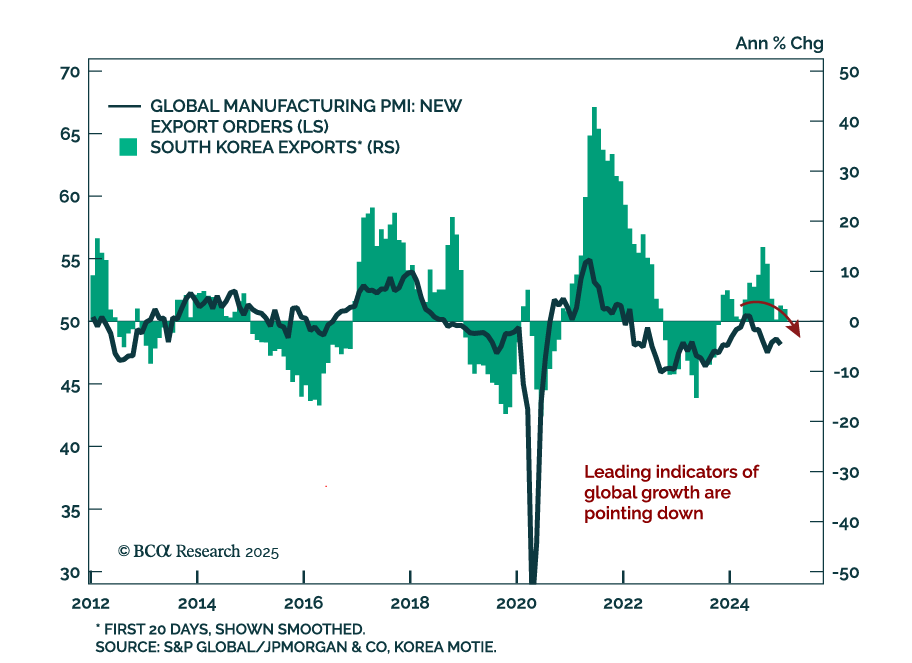

East Asian trade data was mixed in December and January. Taiwanese export orders for December were stronger than expected, rebounding to 20.8% y/y from 3.3% in November. On the other hand, Korean exports for the first 20 days of January fell 5.1% y/y, after…

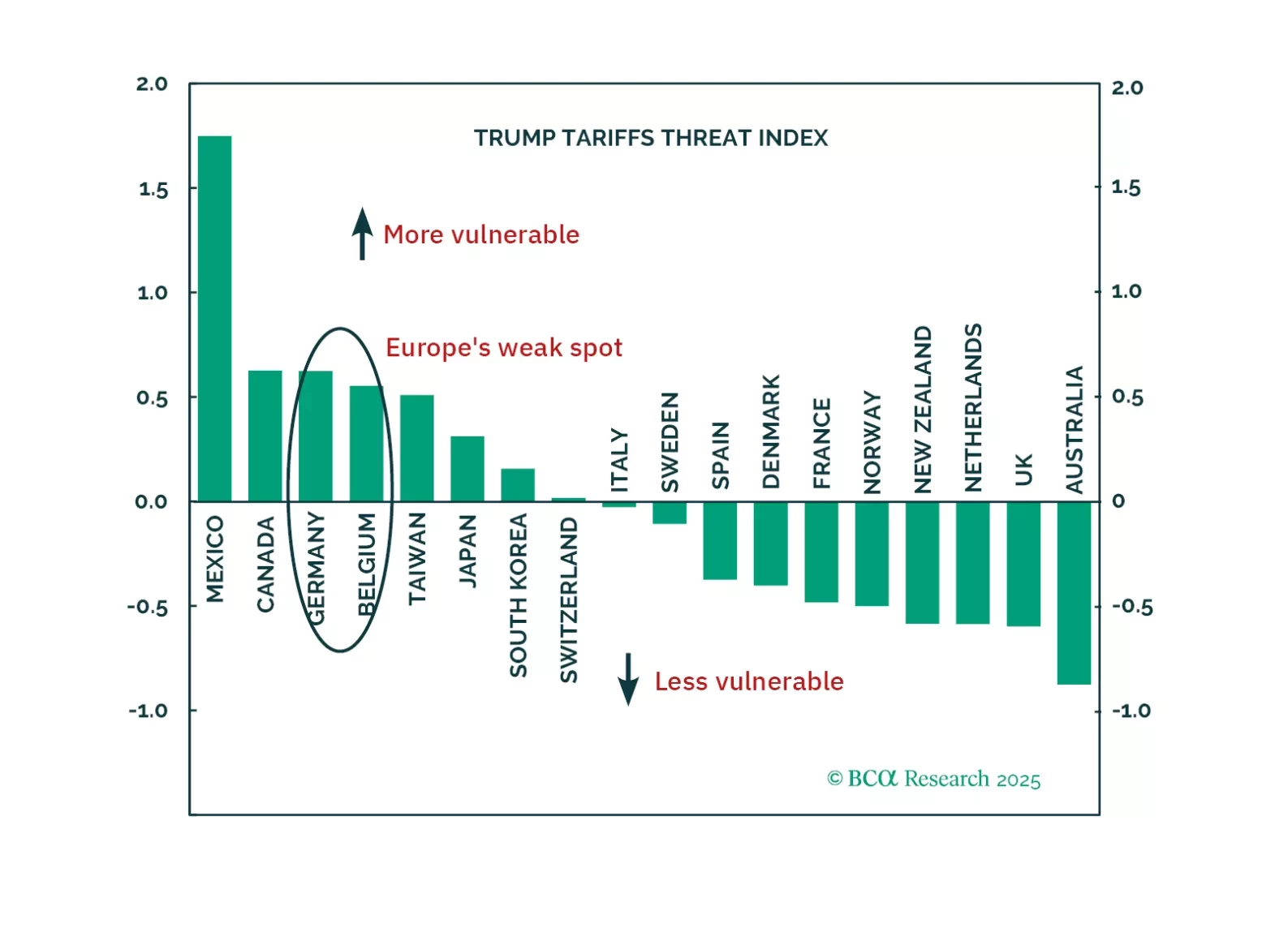

President Trump is about to be inaugurated. Investors often assume all his policies will hurt Europe, but the reality is more nuanced.

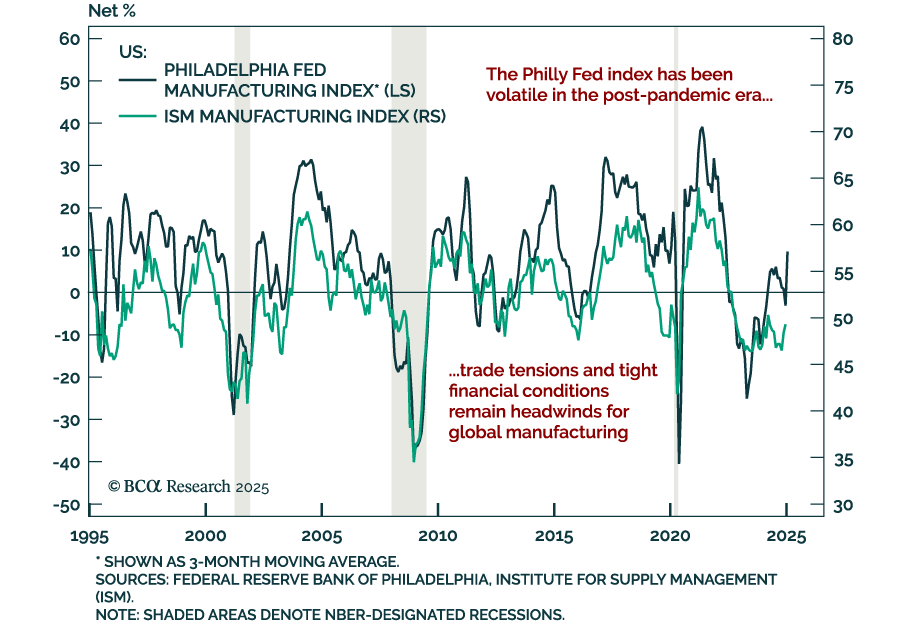

The January Philly Fed Manufacturing index blew past estimates, soaring to 44.3 vs. a revised 10.9 points contraction in December. Most subcomponents rose for both the current and expected categories. Measures of prices paid and received also ticked…

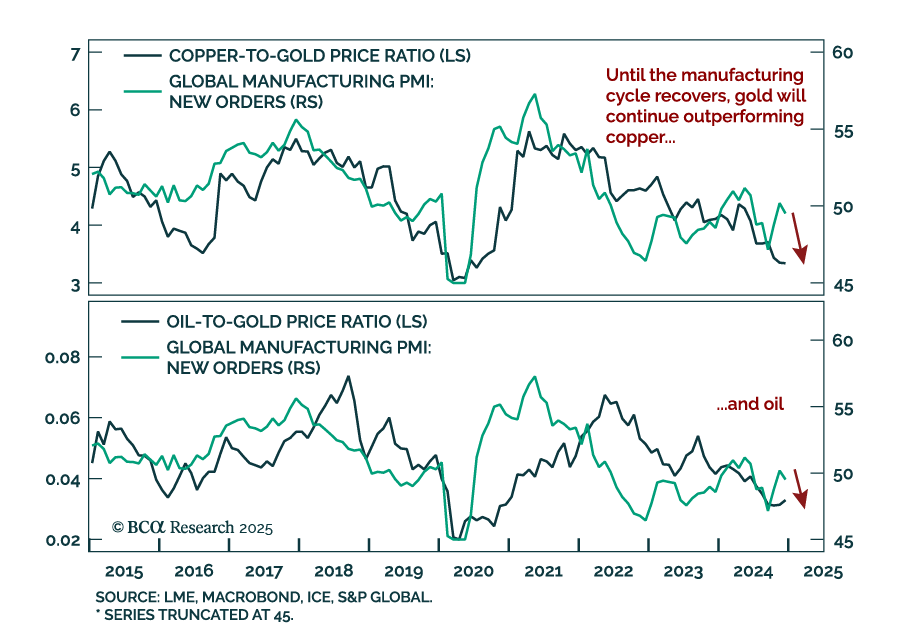

Our Commodities & Energy strategists published a special report outlining three themes they see in the space for 2025. The themes are the following: Sluggish global demand and weak industrial activity will likely weigh on cyclical commodities,…

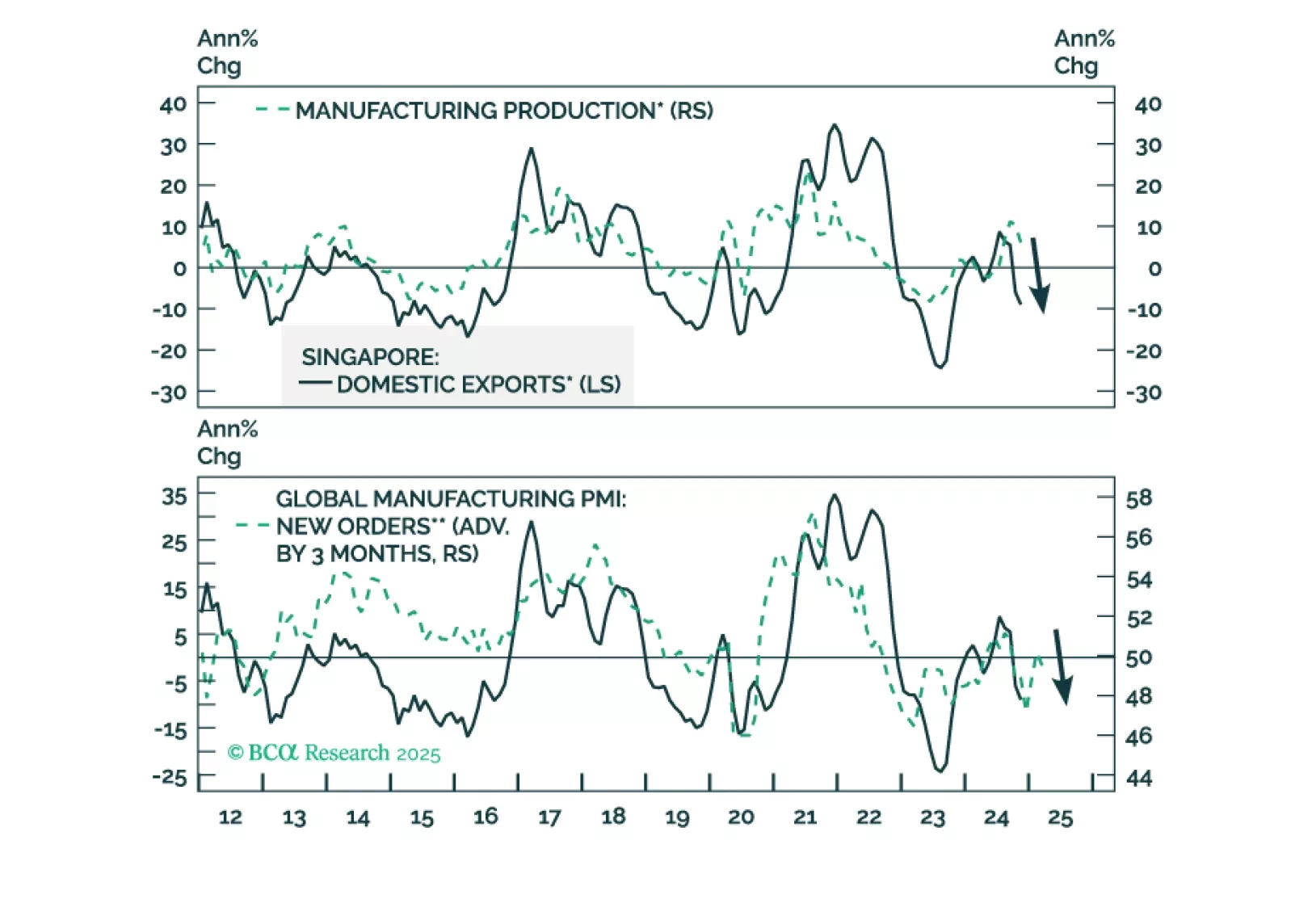

Can Singapore stocks continue the bull run into 2025? What does the city-state’s manufacturing and export outlook foretell? Is the Singapore dollar still competitive? See our analysis and investment recommendations in today’s report.

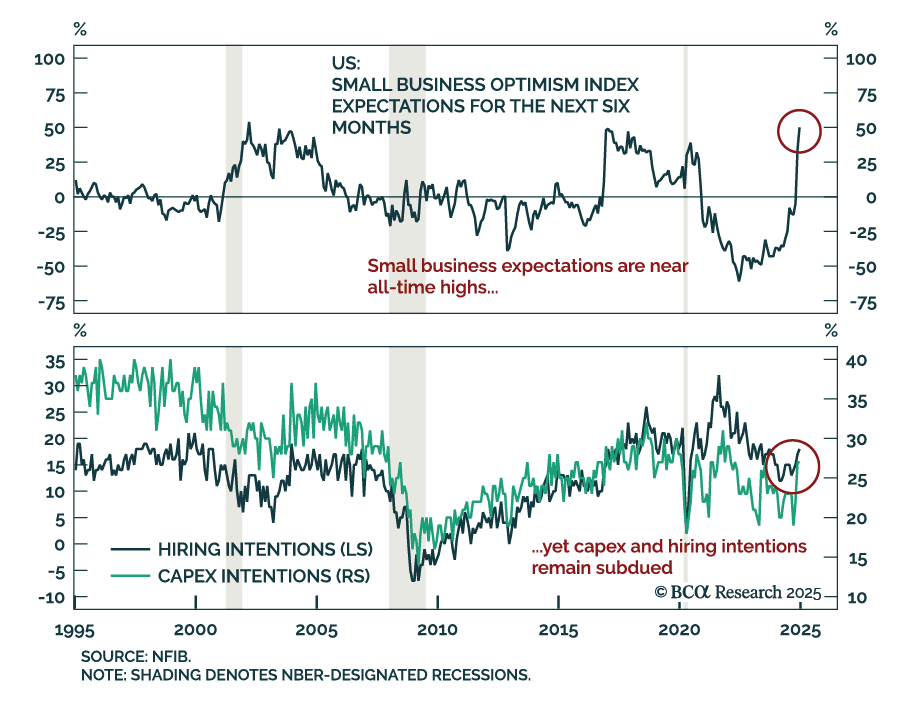

The December NFIB Small Business Optimism Index beat expectations, jumping to 105.1 from 101.7 in November. Most index subcomponents increased, led by measure of expectations, notably for the state of the economy and real sales. After jumping 39 percentage…

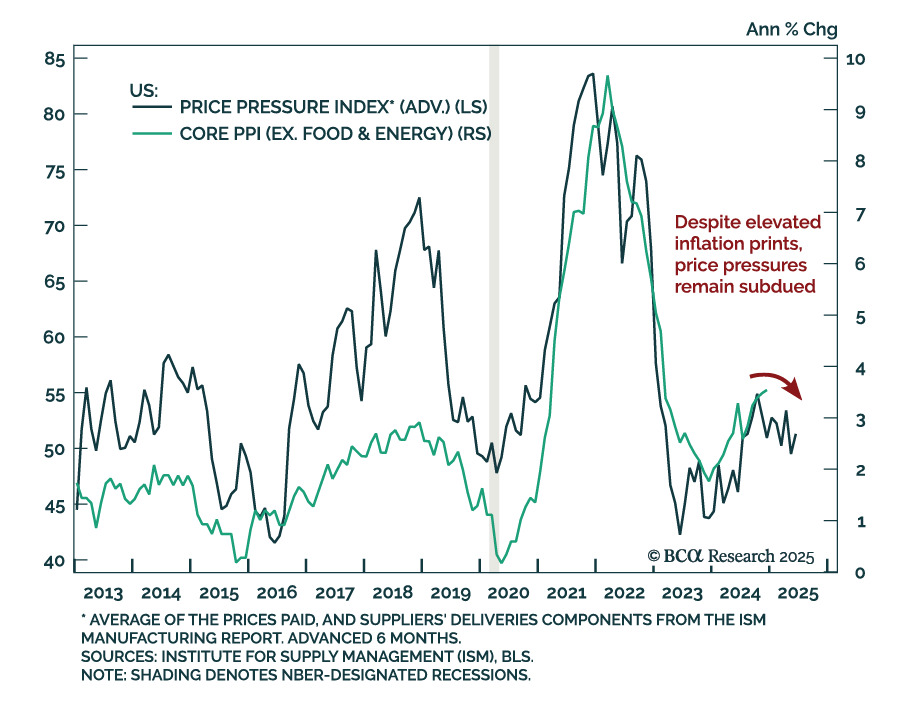

The December US Producer Price Index came in cooler than expected, increasing 0.2% m/m, a deceleration from 0.4% in November. Core PPI, excluding food and energy, was flat after increasing 0.2% a month prior. Inflation is a lagging variable, as…