Monetary

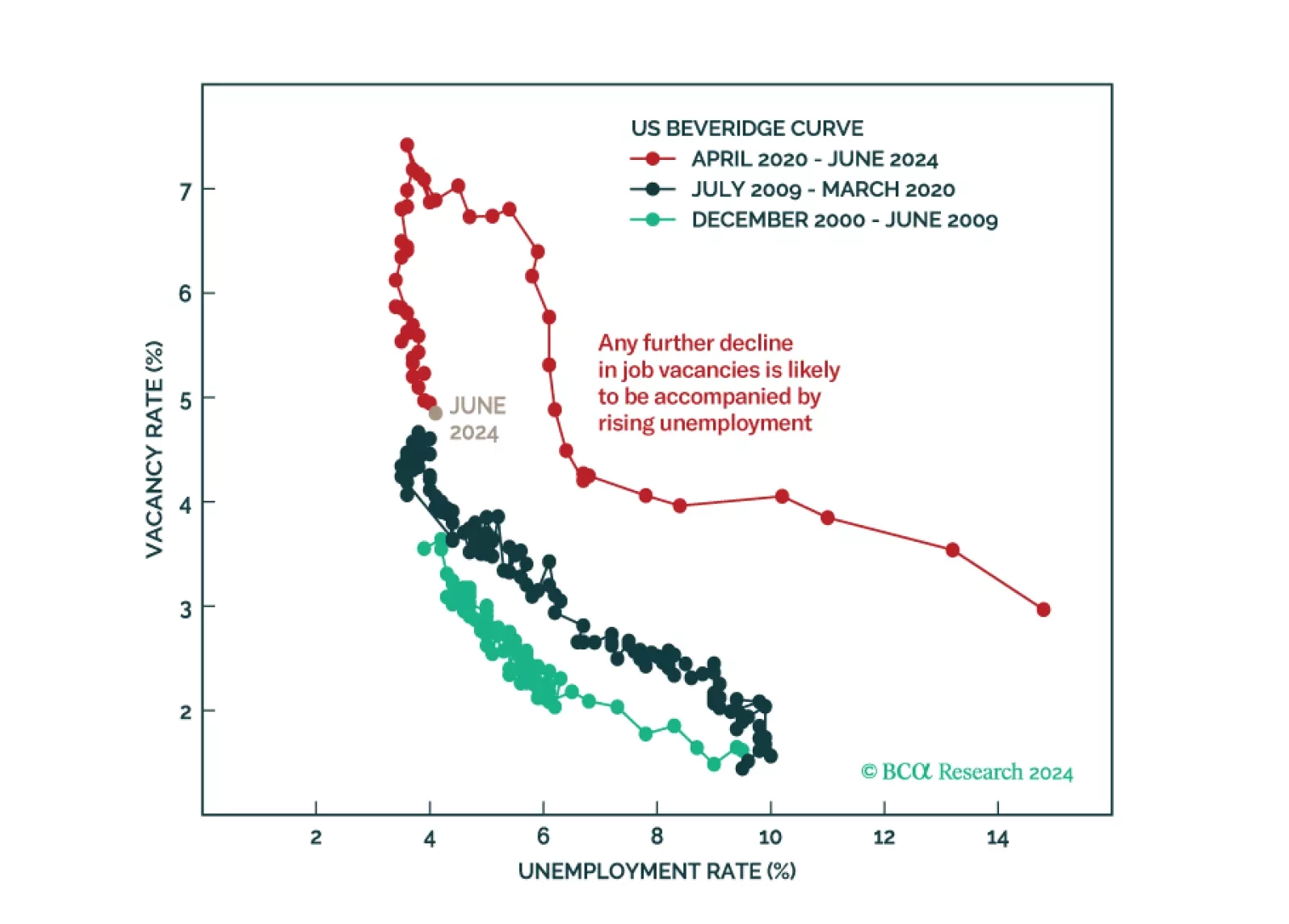

We have high conviction that continued labor market softening will tip the US economy into a recession by year-end or early next year. It will reverberate to the rest of the world given that the US has been the main driver of global demand in this cycle. …

According to BCA Research’s US Bond Strategy service, it is time to increase portfolio duration from “at benchmark” to “above benchmark” on a 6-12 month horizon. Since February, our colleagues have been closely tracking three labor market indicators: the…

The Bank of Canada (BoC) reduced its policy rate by 25bps for the second meeting in a row on Wednesday. We highlighted in a recent Insight that the soft June inflation print and weakening labor market increased the odds of more aggressive BoC easing. …

UK’s CPI growth stands right on the Bank of England’s (BoE) 2% target. However, services inflation remains sticky, growing at a constant 5.7% y/y in June. Moreover, the deceleration in wage growth remains insufficient to temper inflationary pressures in the…

The PBoC lowered the 7-day reverse repo rate from 1.80% to 1.70% on Monday. The 5-year and 1-year loan prime rates declined by 10 basis points (bps) to 3.85% and 3.35%, respectively. However, this 10-bps cut is unlikely to have any meaningful stimulative…

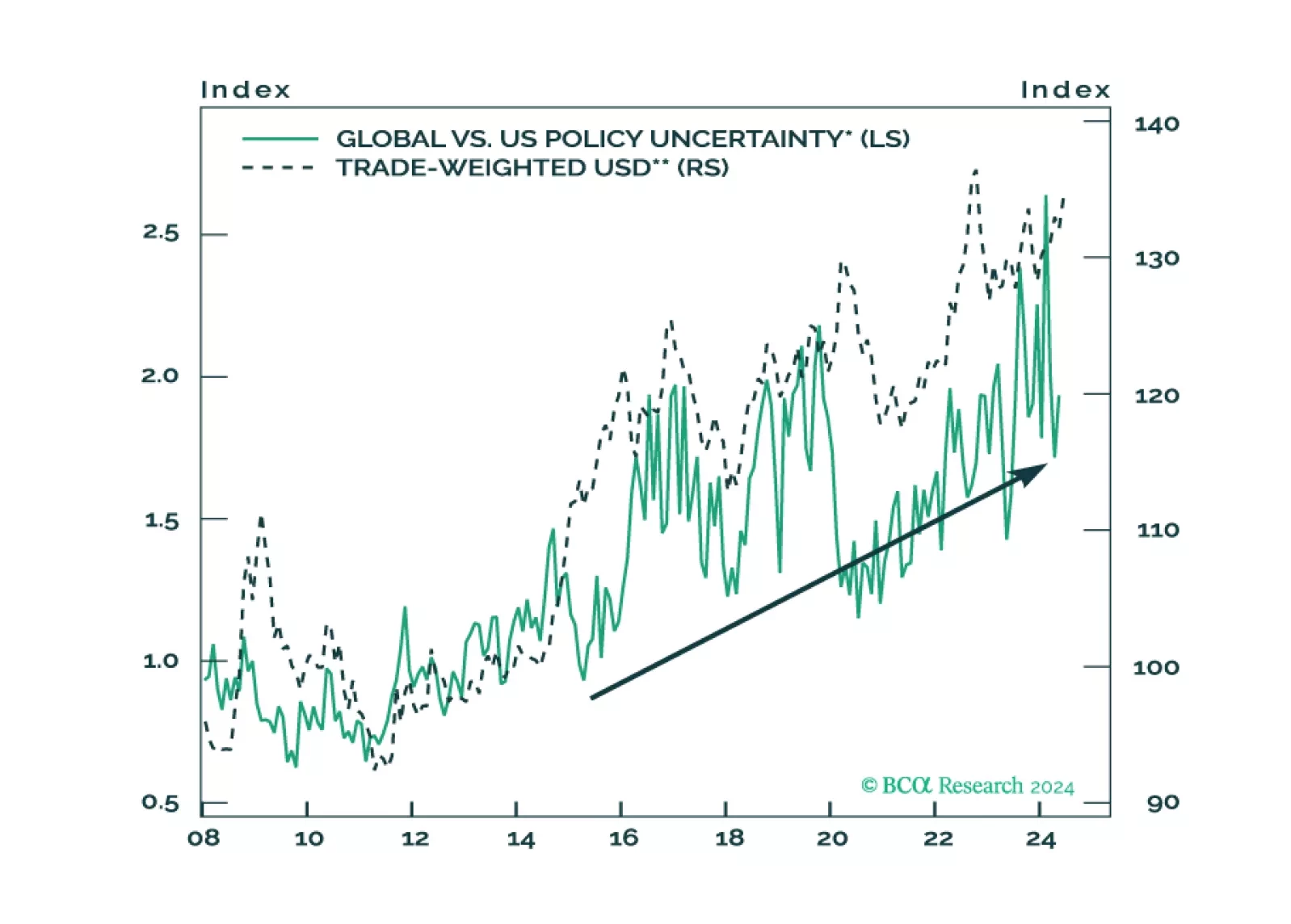

We review some of the key data releases this week that we find have an impact on our currency strategy. Long yen positions make sense today. Long sterling and the euro bets are more of a judgment call, and we will fade any strength in these currencies. This report delves into these nuances, and suggests a few trade ideas.

The four ASEAN stock markets (Indonesia, Malaysia, Thailand, and the Philippines) have fallen in absolute terms over the past year despite the powerful rally in the developed markets. They have also underperformed their EM benchmark. Our Emerging Markets…

Investors should overweight US assets and de-risk their portfolios in anticipation of a major increase in policy uncertainty and geopolitical risk surrounding the US election and its global ramifications.

Don't buy the dip. The equity bull market is over. The US will enter a recession in late 2024 or in early 2025.

The Euro Area economy broadly surprised to the upside in the first half of 2024. Cooling inflation lifted real wages and the global late cycle amelioration benefitted the pro-cyclical Euro Area economy, but these tailwinds are fading. First, monetary…