Monetary

At first blush, the US establishment survey delivered a positive surprise on Friday. The increase in US nonfarm payroll employment jumped from 173 thousand to 216 thousand in December – beating expectations of 175 thousand. Wage growth also surprised to the…

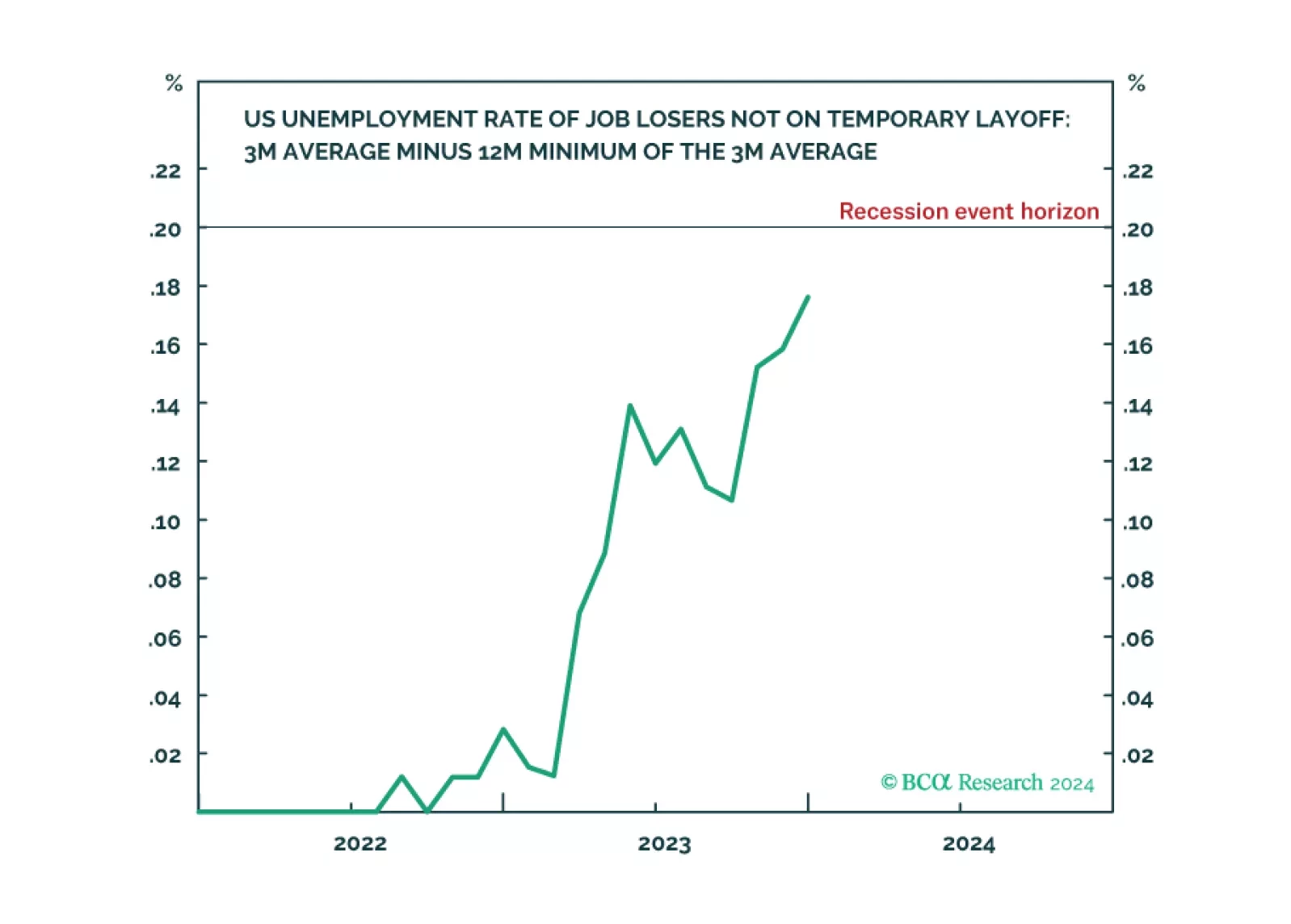

Following today’s US jobs data release, the Joshi rule real-time US recession indicator inched up to 0.18 and is now just a whisker from its recession event-horizon of 0.20.

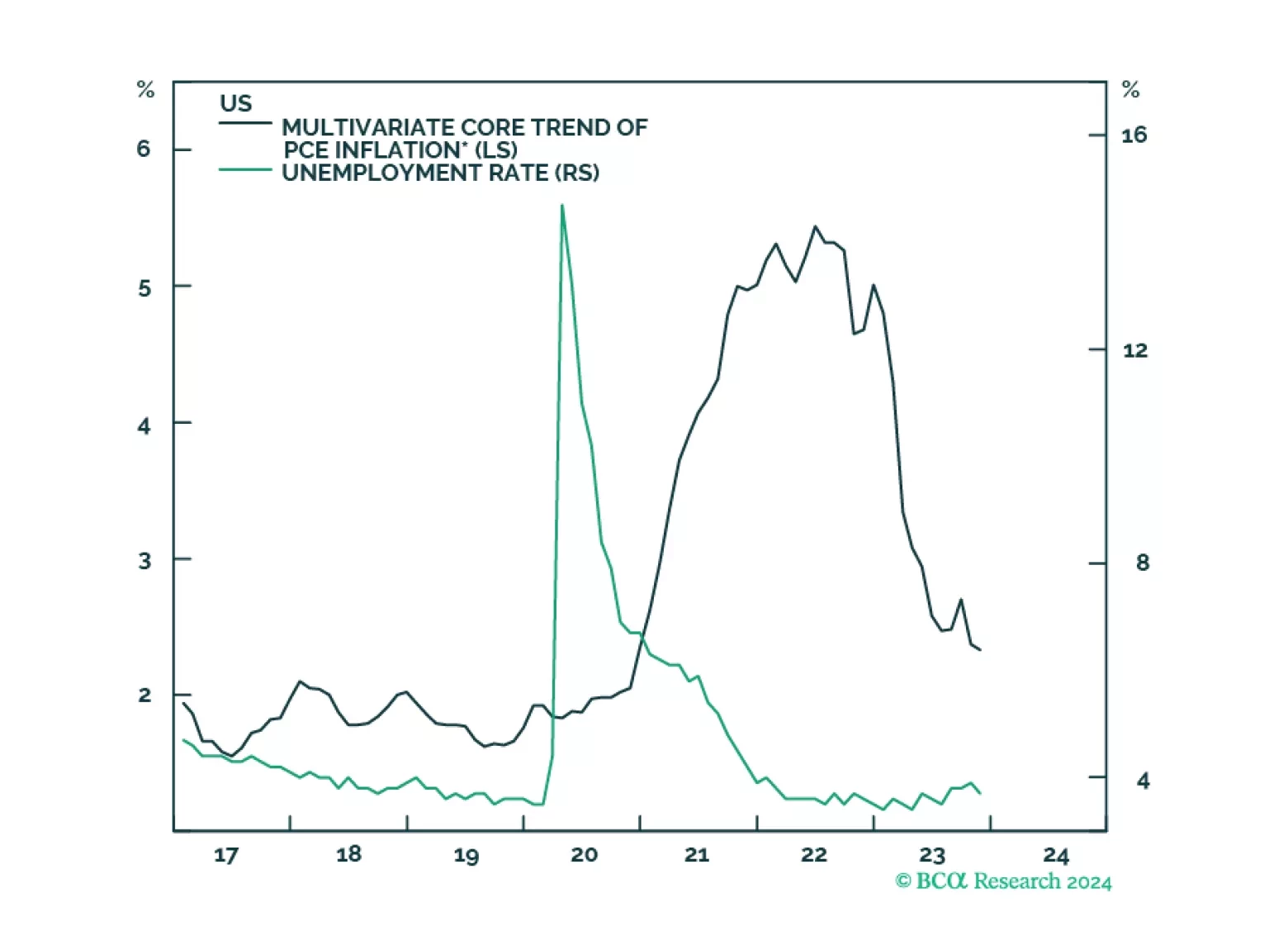

A soft landing can be achieved but not maintained. We are cutting our tactical recommendation on stocks from overweight to neutral and scaling back our long-duration stance.

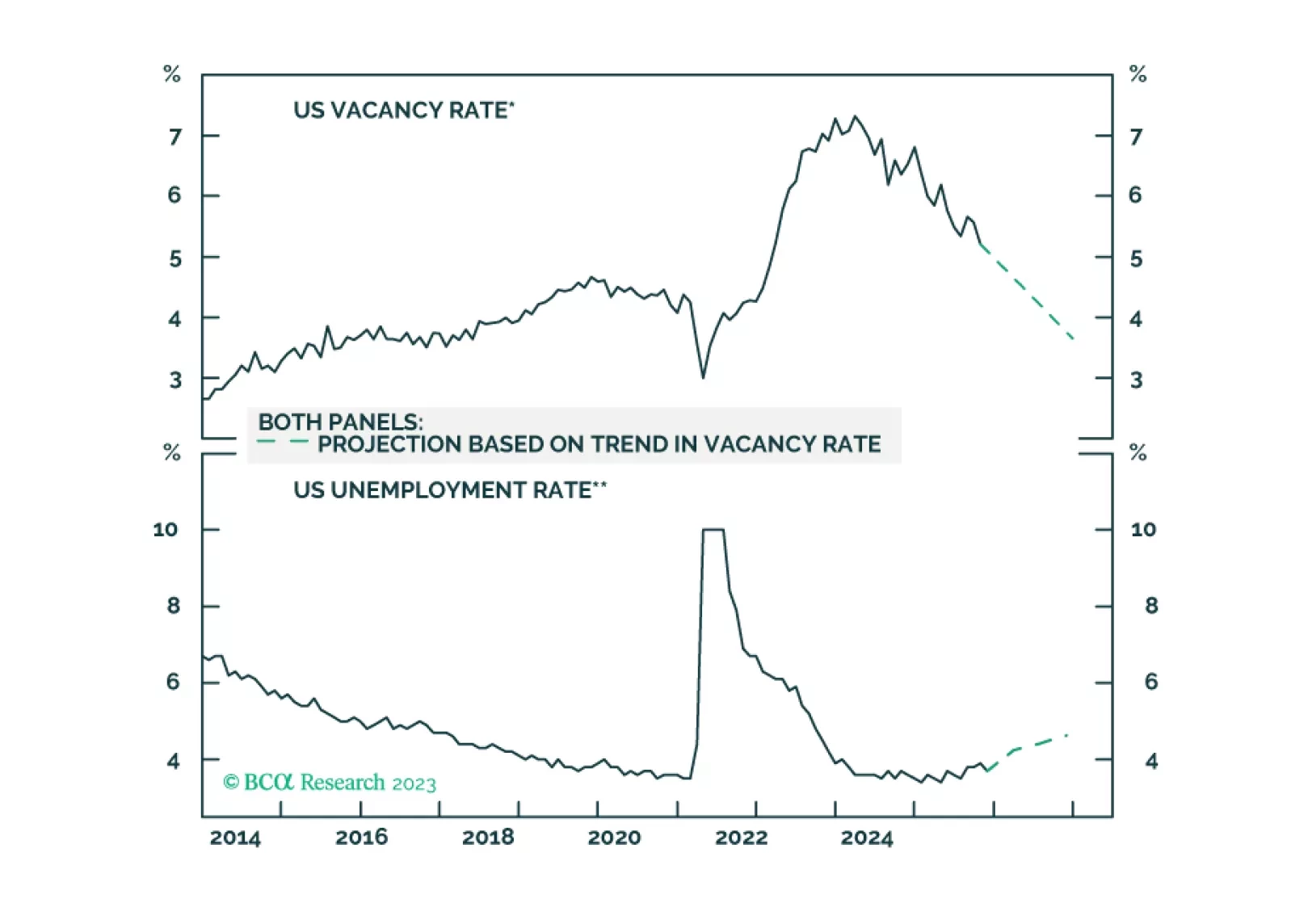

Results of the November JOLTS survey indicate that the US labor market is softening. The number of job openings slowed from 8.85 million to 8.79 million – the lowest since March 2021 and slightly below expectations of 8.82 million. This brings the ratio of…

Minutes from the Fed’s December 12-13 FOMC meeting suggest that policymakers are more confident that inflation is on track to return to target. While they continued to note that inflation remains elevated and that they are highly attentive to inflation risks,…

According to BCA Research’s European Investment Strategy service, the euro has ample attractive features that justify a positive long-term outlook. However, its pro-cyclicality and the dollar’s negative correlation to risk assets constitute important…

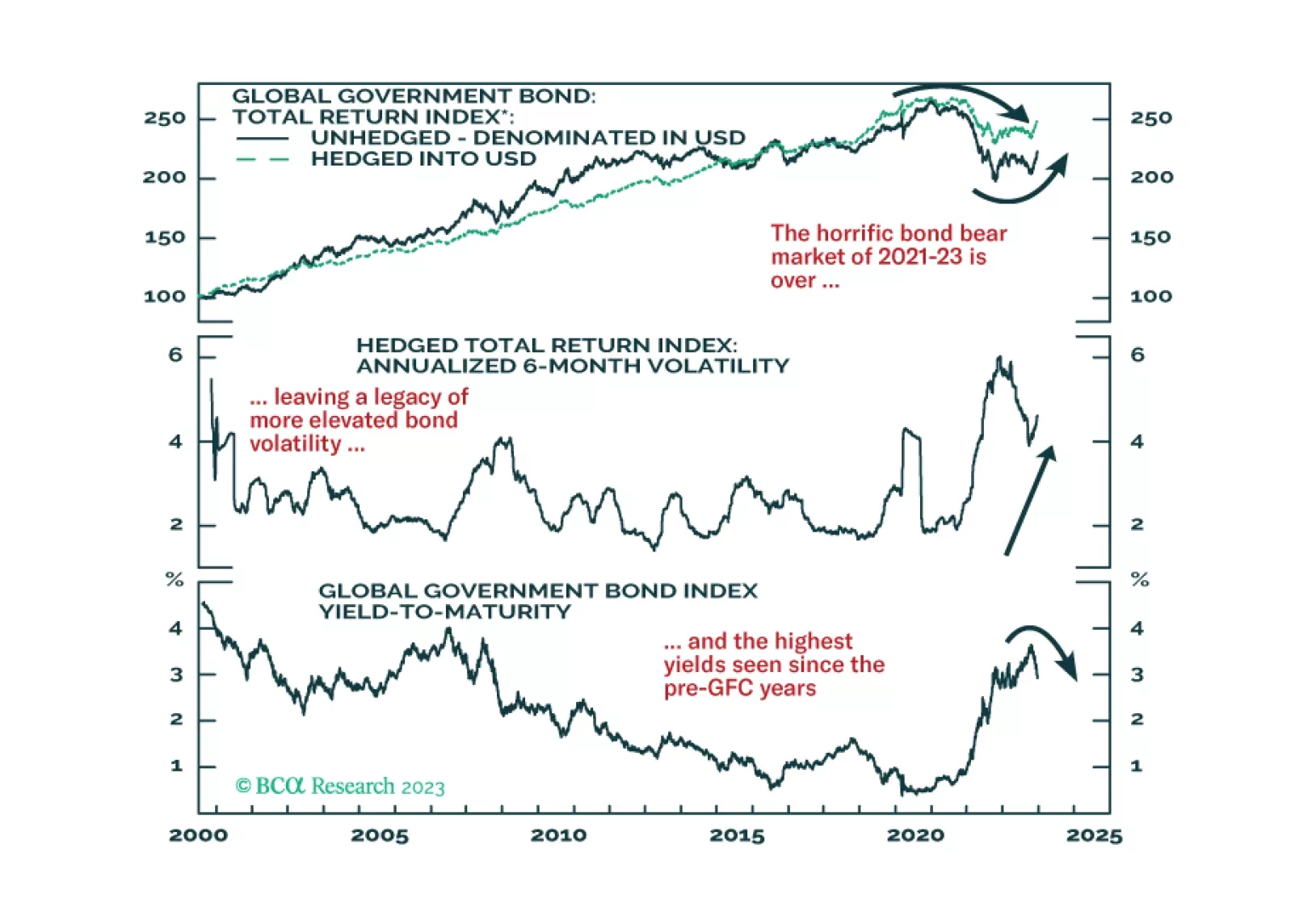

According to BCA Research’s Global Fixed Income Strategy service, the timing and pace of rate cuts in 2024 will differ across countries, representing a big sea change from the highly correlated rate hiking cycles of the past two years. Currently, the…

In this, our final report of the year, we present our main global fixed income investment themes and recommendations for 2024.

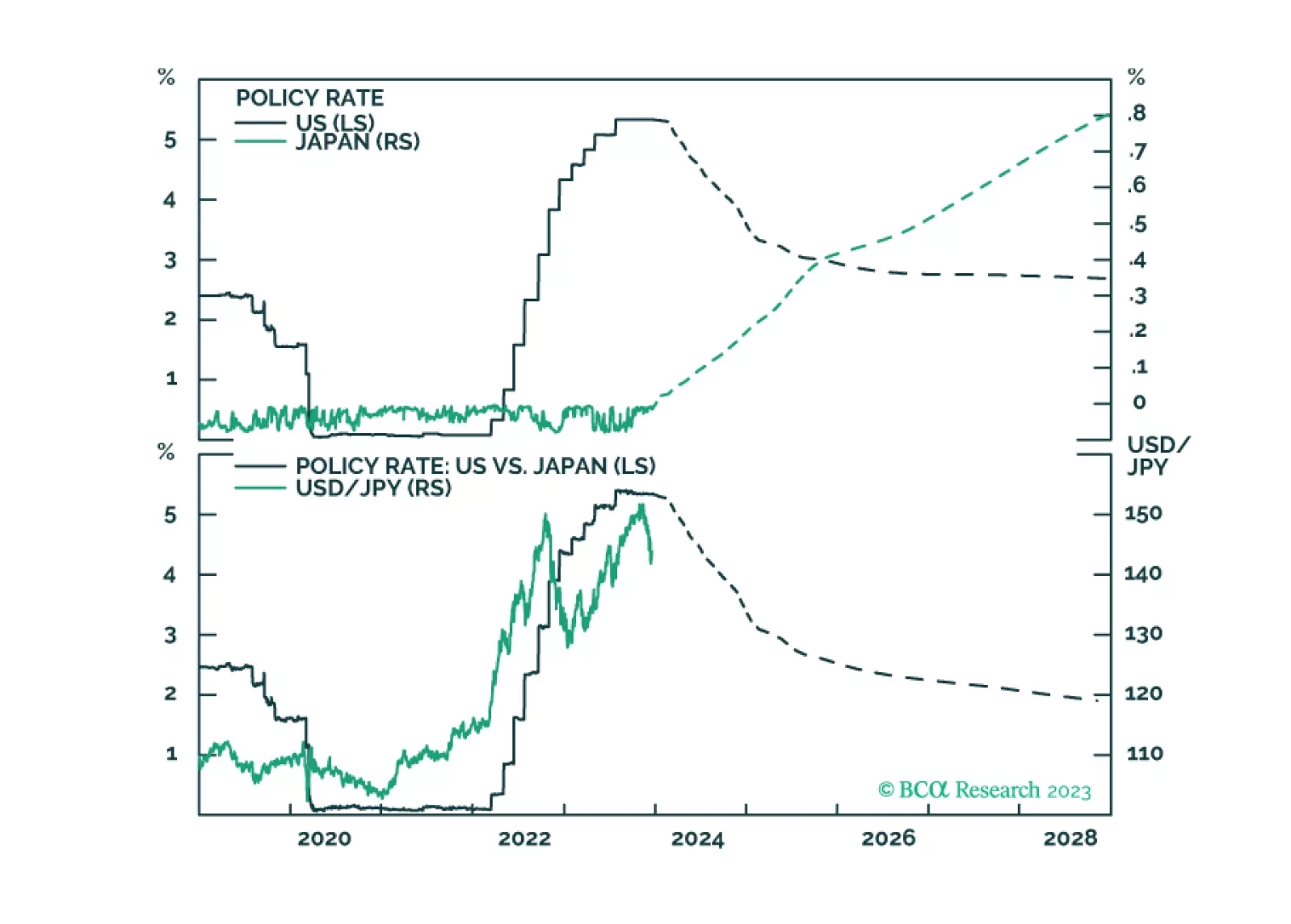

A post-mortem of our trades for the year, and also comments on future yen and sterling moves from the recent BoJ meeting, and the UK inflation report.

Our outlook for the Fed’s interest rate and balance sheet policies in 2024.