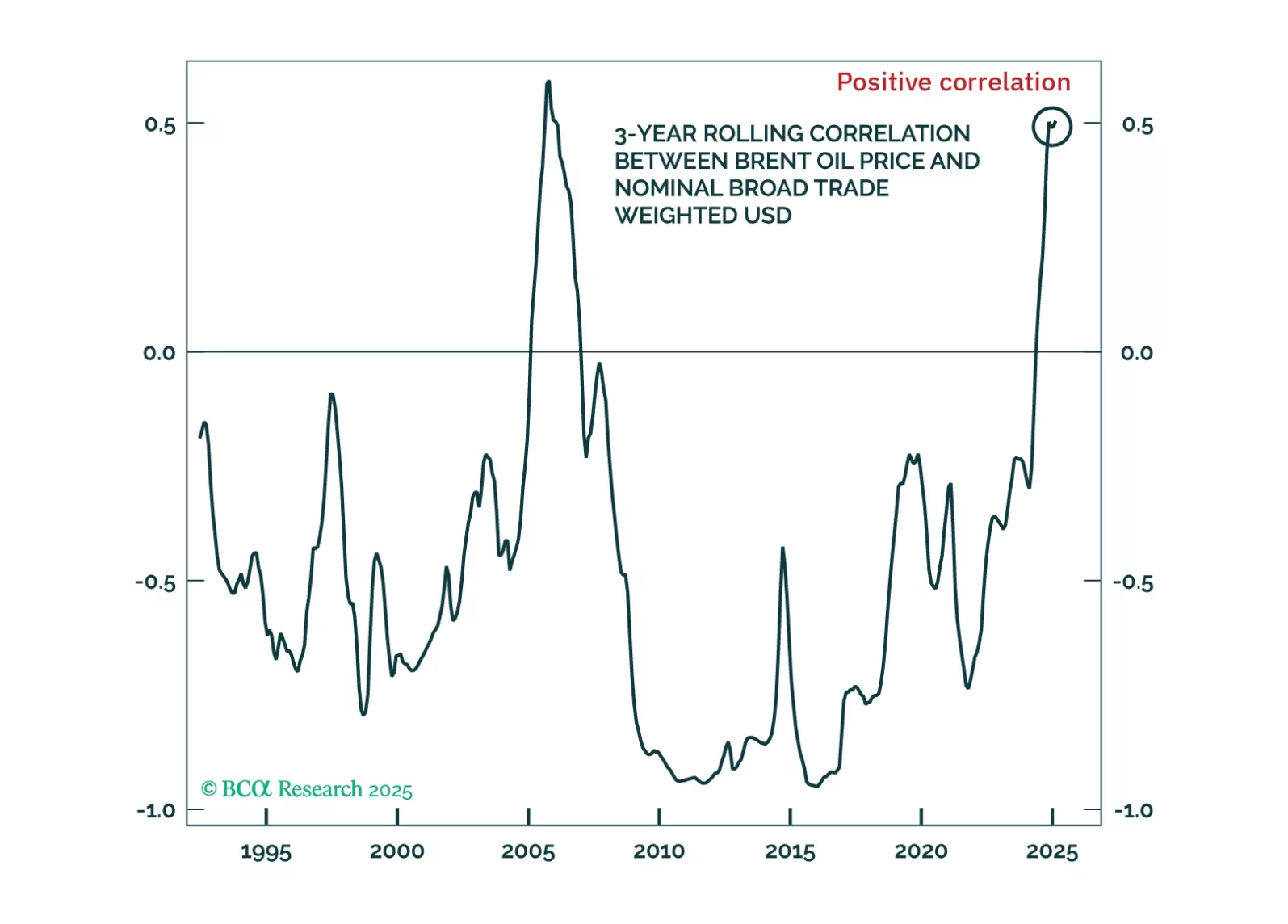

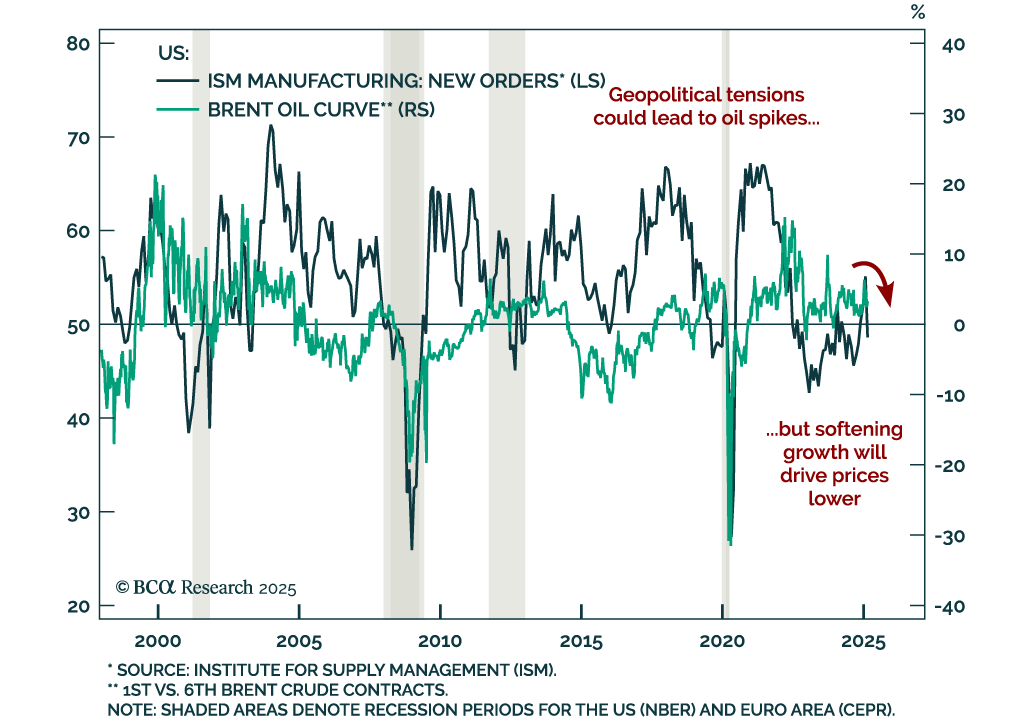

Oil

Commodity prices are succumbing to the risk-off environment triggered by President Trump’s reciprocal tariff announcement. The latest events and market moves raise several important questions about the outlook for commodity markets.

In this Strategy Report we address some of the most pressing questions raised during our recent discussions.

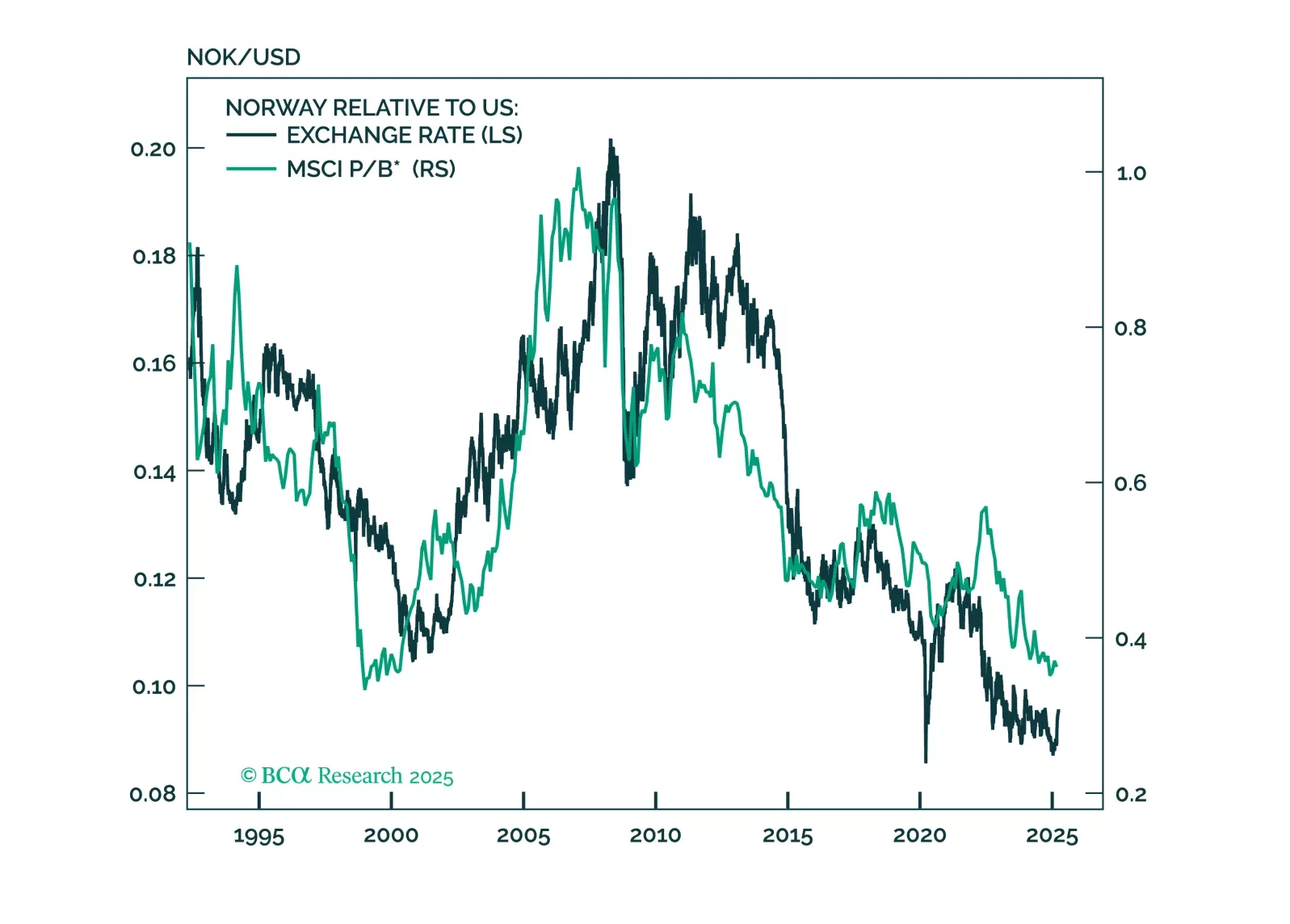

This report looks at investment implications, for Norwegian assets, given the recent meeting, from the Norges Bank.

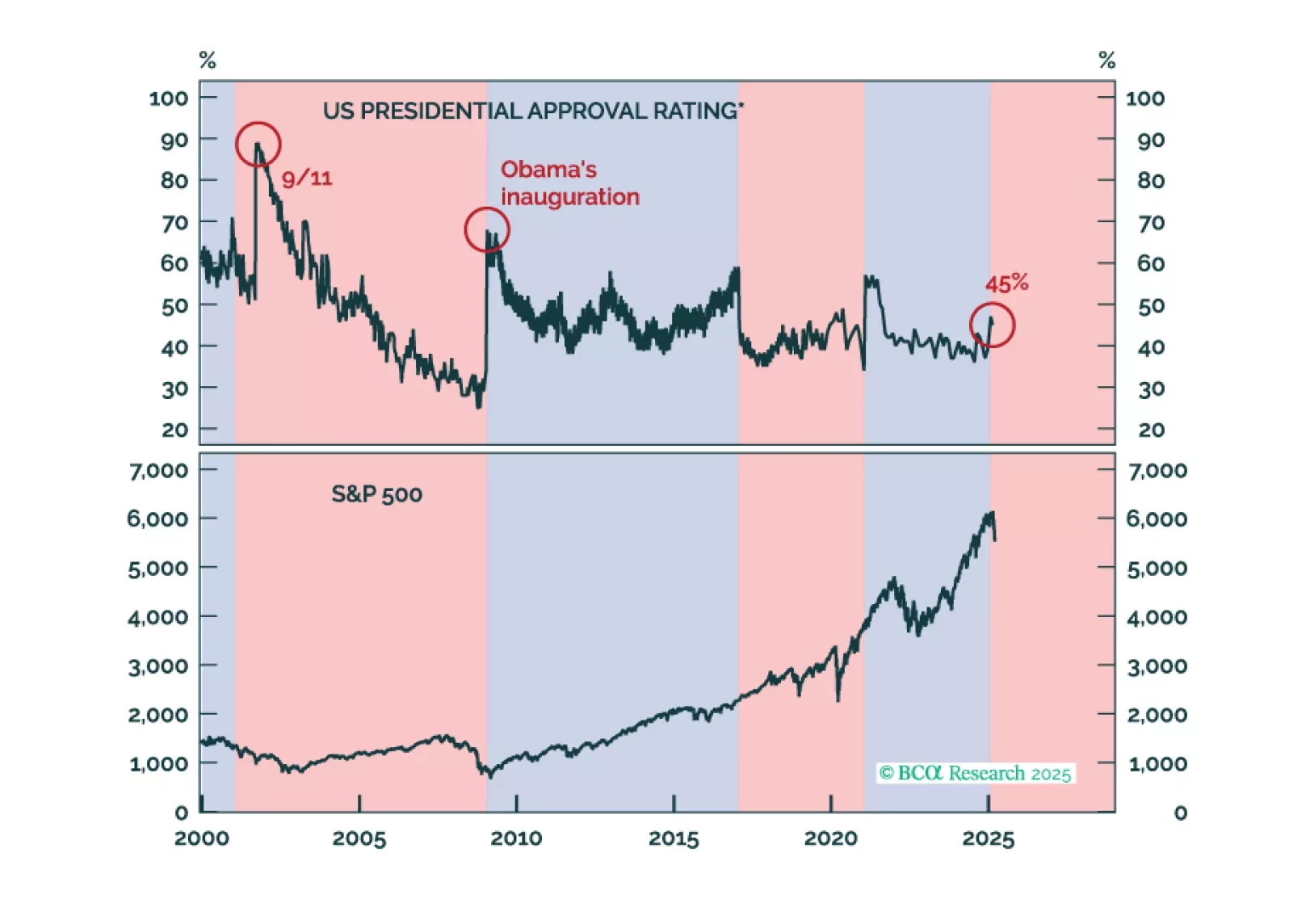

Stocks will continue to struggle in the second quarter as President Trump tries to implement tariffs. Tax cuts will only temporarily dispel growth fears, if at all. Middle Eastern instability will add oil price surprises to an environment that is looking fairly stagflationary.

In this Second Quarter Strategy Outlook, we explore the major trends that are set to drive financial markets for the rest of 2025 and beyond.

Despite our bearish predisposition towards stocks, we are open-minded to anything that could challenge our thesis. As such, in this report, we review five upside scenarios for equities.

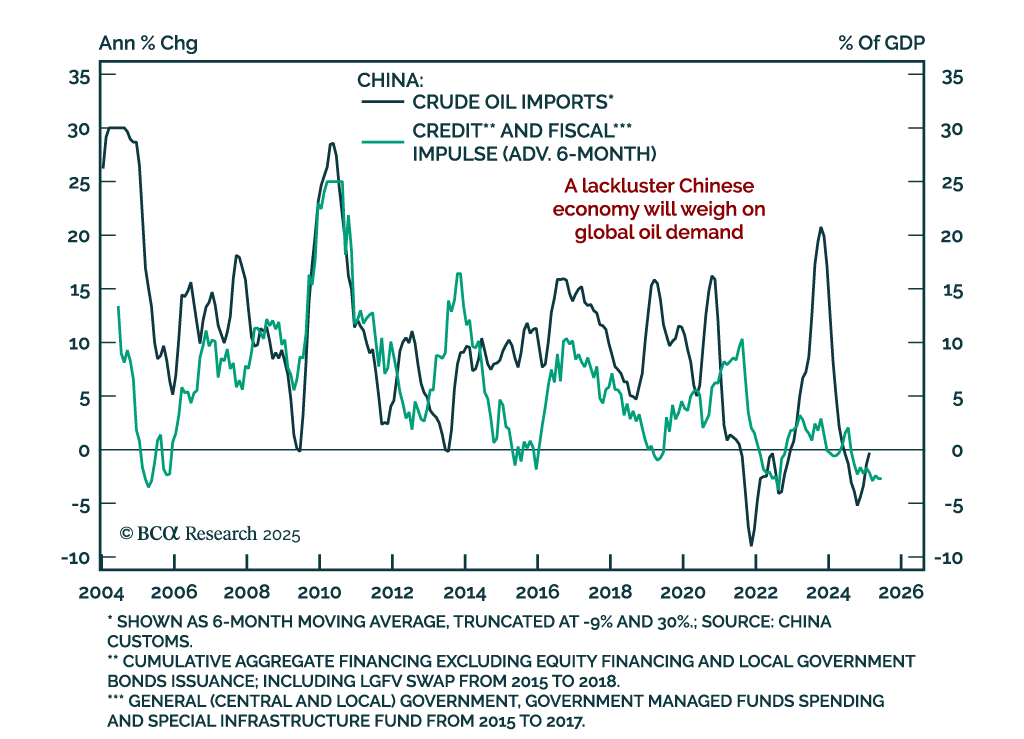

OPEC+ is planning to boost its crude oil output at a time of lingering demand weakness.

What is driving this decision? And will Chinese oil consumption – historically a key contributor to global oil demand growth – reaccelerate and justify the coalition’s decision to bring back more supply to the market?

This report answers these questions and more.

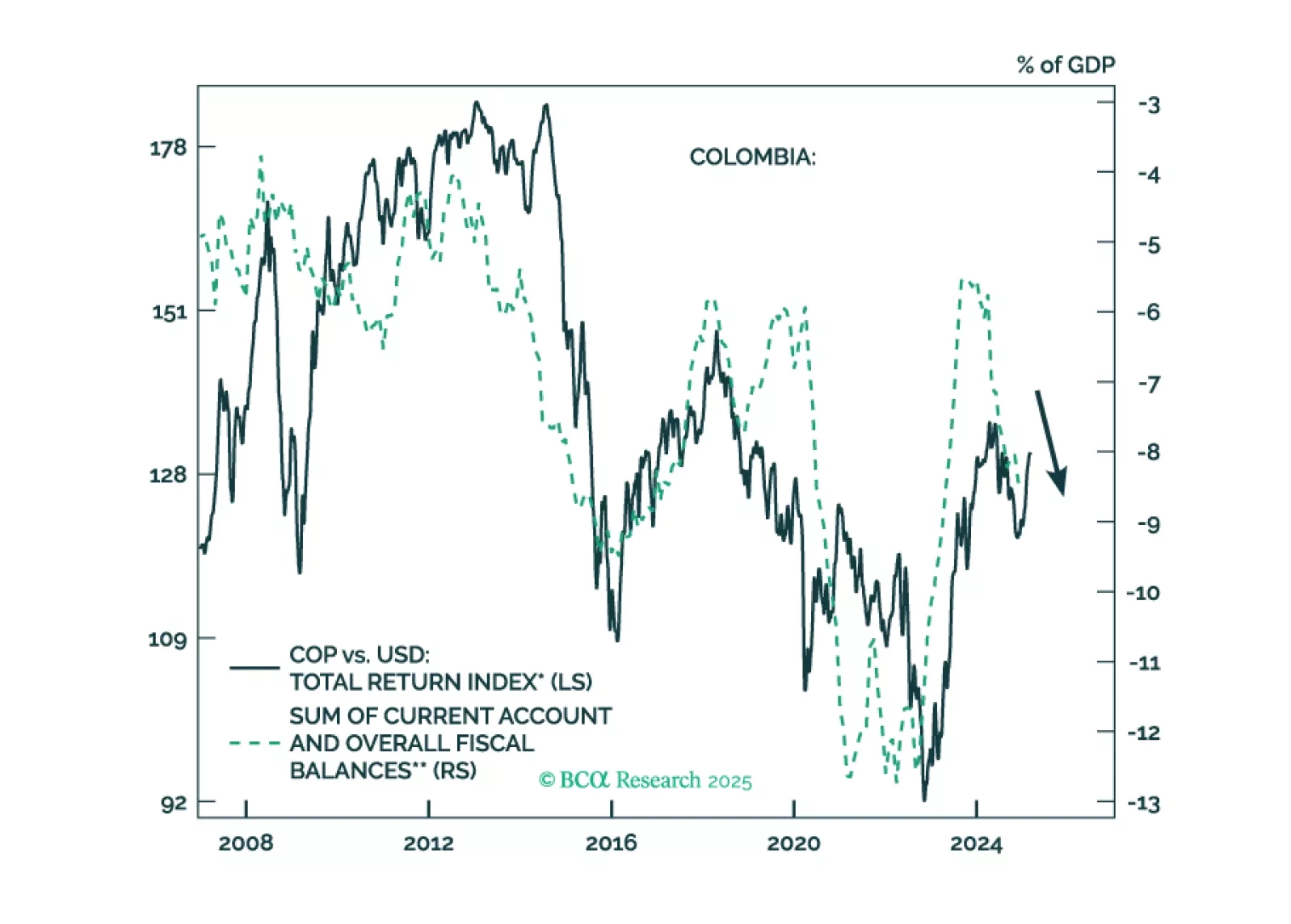

Colombian financial markets have rallied on the expectation that a right-wing government will be elected in 2026. We take a contrarian bearish stance on the nation's financial markets. Colombia is suffering from two structural macro issues – unsustainable public debt and plunging energy exports – that will not be easily solved by a conservative administration in 2026. Continue underweighting Colombia within EM equity and fixed-income portfolios, continue shorting the COP versus the USD and the CLP, and bet on yield curve steepening.

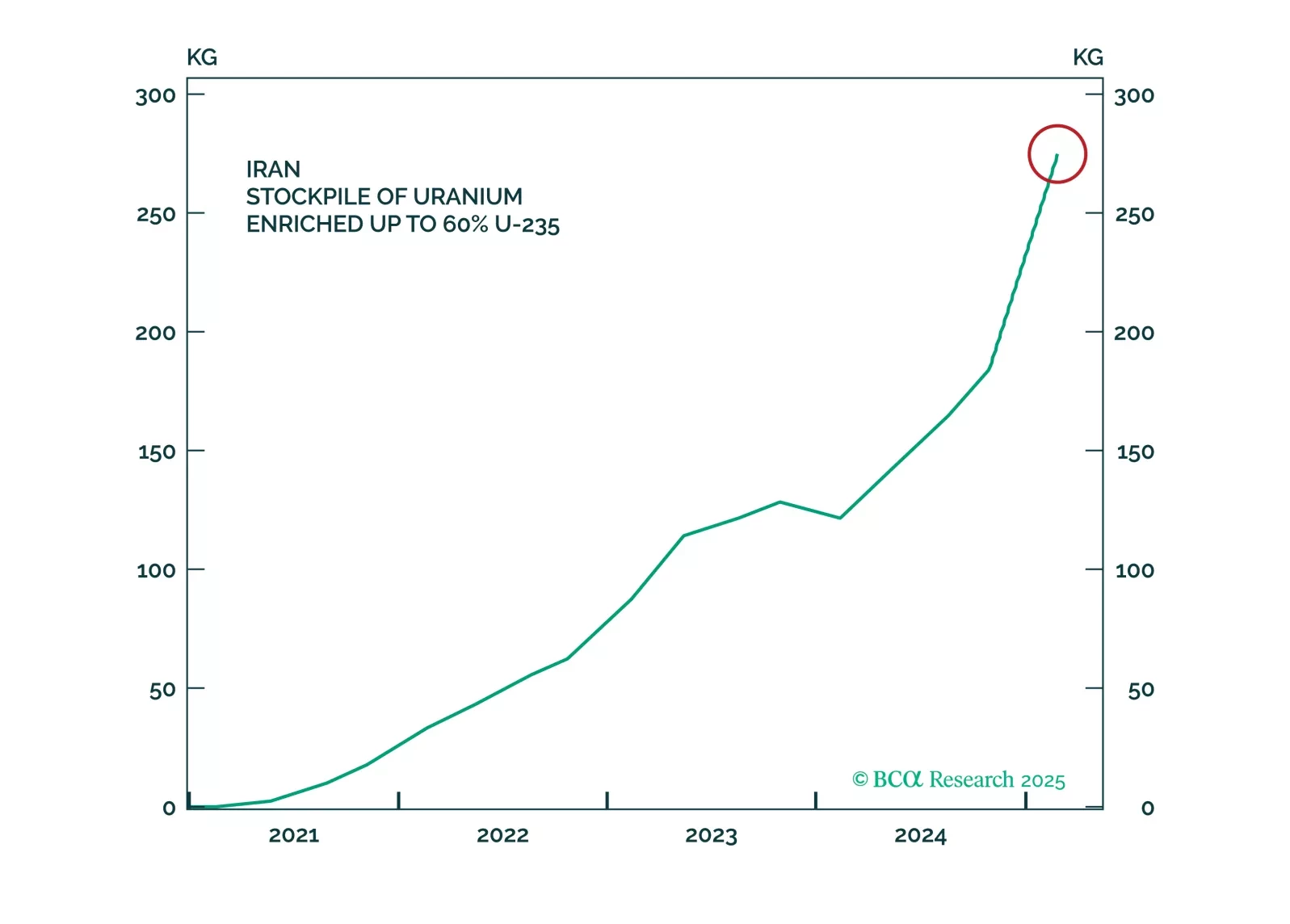

The tariffs on Canada and Mexico will come into effect as scheduled while the tariffs on China will be doubled. In the Middle East, Iranian response to any attack will threaten Middle Eastern oil supply. Meanwhile, Chinese fiscal support will surprise to the upside at the Two Sessions. But Trump's China policy will cause volatility. Now that the stock market is cracking, reinitiate defensive trades, such as long treasuries versus US stocks and long global defensives versus cyclicals.